|

시장보고서

상품코드

1936481

차량용 어시스턴트 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)In-Vehicle Assistant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

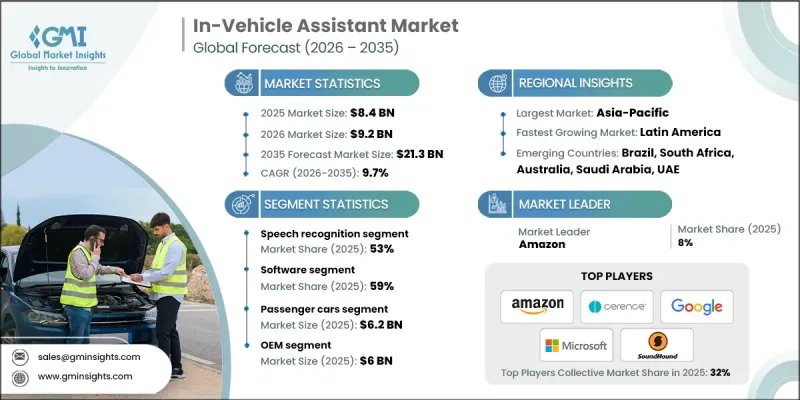

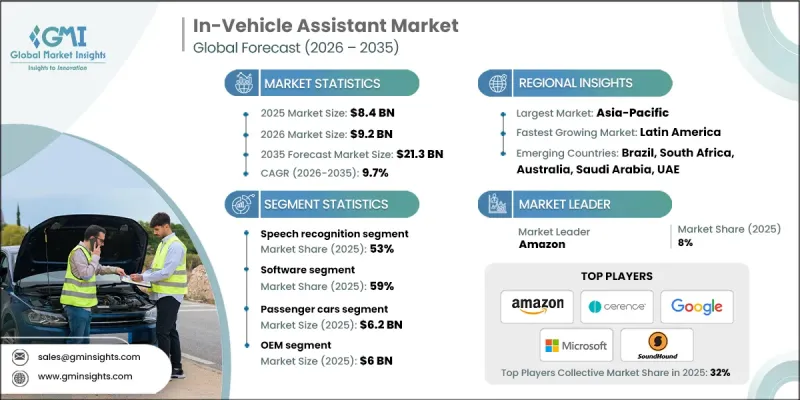

세계의 차량용 어시스턴트 시장은 2025년 84억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.7%로 성장할 전망이며, 213억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경은 안전하고 편리하며 핸즈프리 차량 운영에 대한 소비자 수요 증가와 OEM 제조업체의 전기자동차 및 자동 운전 차량의 대량 도입에 대한 노력을 포함합니다. 음성, 터치 및 제스처 입력을 커넥티드카에 통합하는 자동차 제조업체의 동향에 따라, 멀티 모달인 휴먼 머신 인터페이스(HMI)의 등장이 업계의 변화를 추진하고 있습니다. 대규모 언어 모델(LLM)은 보다 스마트한 플랫폼과 디바이스 개발을 가능하게 하고 직관적인 드라이버 조작을 실현함과 동시에 고급차부터 엔트리 모델까지 폭넓은 차종으로의 채용을 촉진하고 있습니다. COVID-19의 팬데믹에 의해 일시적으로 차량 생산이 중단되어 신차 투입이 지연되었지만, 커넥티드카 및 스마트카 기술에의 지속적인 투자를 배경으로, 통합형 음성 어시스턴트나 선진적인 차재 디지털 체험에 대한 장기적인 수요는 견조하게 추이하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 84억 달러 |

| 예측 금액 | 213억 달러 |

| CAGR | 9.7% |

음성 인식 부문은 2025년에 53%의 점유율을 차지하였고, 2026-2035년 CAGR 8.7%를 나타낼 것으로 예측됩니다. 이 기술은 차량용 어시스턴트 시스템의 핵을 이루고 마이크로 캡처한 음성 신호를 자동 음성 인식(ASR) 알고리즘을 통해 실용적인 텍스트로 변환합니다. 수익원으로는 자동차 전용 ASR 소프트웨어 라이선싱, 빔포밍 마이크, 음향 처리 전용 디지털 신호 처리(DSP) 칩 등을 들 수 있습니다.

소프트웨어 분야는 2025년에 59%의 점유율을 차지하였으며, 2035년까지 연평균 복합 성장률(CAGR) 8.2%를 나타낼 것으로 예측됩니다. 소프트웨어 플랫폼에는 클라우드 기반 자연 언어 처리, 음성 인식 엔진, 소프트웨어 업데이트 관리 시스템, 타사 용도를 통합하는 API 등이 포함됩니다. 라이선싱 모델은 다양하며 기존 벤더는 종종 차량 단위의 구독 계약을 채택합니다.

중국의 차량용 어시스턴트 시장은 2025년 26억 달러 규모에 달했습니다. 이 나라에서는 연간 3,000만 대 이상의 자동차가 생산되고 있으며, '새로운 인프라 정책'과 '스마트 시티 계획' 등 정부 시책이 차량의 연결성을 가속화하고 있습니다. 음성 기반의 긴급 신고 시스템을 의무화하는 규제 및 고급 커넥티드 자동차를 위한 전용 자금이 시장의 성장 궤도를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 공급자

- 기술 플랫폼 제공 기업

- 시스템 통합자

- 자동차 제조업체

- 애프터마켓 유통업체

- 최종 사용자

- 비용 구조

- 이익률

- 각 단계에서 부가가치 창출

- 수직 통합의 동향

- 디스랩터(시장 변혁자)

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 커넥티드카 및 스마트카 보급 확대

- 안전성 및 핸즈프리 조작에 대한 소비자 수요 증가

- 전기자동차 및 자동운전차(EV/AV) 시장 확대

- 애프터마켓 및 소프트웨어 업그레이드의 성장

- 업계의 잠재적 위험 및 과제

- 높은 OEM 통합 비용

- 개인 정보 보호 및 데이터 보안에 대한 우려 사항

- 시장 기회

- AI 구동형 어시스턴트 통합

- 멀티 모달 HMI 도입

- 클라우드 연결성 및 OTA 업데이트

- 스마트 어시스턴트의 지역별 보급 상황

- 성장 촉진요인

- 기술 동향과 혁신 및 에코시스템

- 현행 기술

- 신흥 기술

- 성장 가능성 분석

- 규제 상황

- 북미

- FMVSS 운전자 주의 산만 방지 가이드라인

- 캘리포니아주-ACC 및 ZEV 규제

- 캐나다-운수성 연결 차량 및 인포테인먼트 가이드라인

- 유럽

- EU-일반안전규제(GSR)

- 자동차용 인포테인먼트용 CE 인증

- EU-자동차 형식 인증 지령

- 아시아태평양

- 일본-자동차 전자 기기 안전 기준

- 중국-GB 규격(커넥티드카용)

- 인도-AIS/EMC 가이드라인

- 라틴아메리카

- 브라질-INMETRO 규격

- 콜롬비아-자동차 커넥티드 시스템 가이드라인

- 아르헨티나-차재 전자기기 및 인포테인먼트 규제

- 중동 및 아프리카

- UAE-커넥티드카 및 음성 대응 차량 기준

- 오만-자동차 전자기기 가이드라인

- 남아프리카-SABS 자동차용 음성 및 인포테인먼트 규격

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- OEM 가격 설정 모델

- 애프터마켓 가격 동향

- 정기 구독 모델 및 단품 구입 모델의 비교

- 지역별 가격 차이

- 특허 분석

- 공급망 분석

- 부품 조달 전략

- 반도체 칩 공급 제약

- 클라우드 인프라에 대한 의존성

- 지역별 공급망 동향

- 시장 진출 전략

- 지역별 시장 침투 전략

- 신규 진출 기업의 주요 규제 고려 사항

- 가격 설정, 서비스, 차별화 전략

- 상업적 실현 가능성 및 전개

- 비용 경쟁력 및 프리미엄 오디오의 업셀 가치의 비교

- OEM 조달 매력 및 플랫폼 확장성

- 애프터마켓에서의 업그레이드 가능성 및 딜러 설치의 경제성

- 현지화, 공급의 회복력, 물류의 실용성

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 기술별(2022-2035년)

- 음성 인식

- 자연언어처리(NLP)

- 인공지능(AI)

제6장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

- 소프트웨어

- 임베디드 소프트웨어

- 클라우드 기반 소프트웨어

- AI 탑재 소프트웨어

- 하드웨어

- 마이크

- 스피커

- 제어 유닛

- 디스플레이 패널

- 서비스

- 통합 및 도입

- 보수 및 서포트

- 컨설팅 서비스

제7장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 세단

- 해치백 자동차

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

- 네비게이션

- 엔터테인먼트

- 통신

- 기타

제9장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 거대 기술 기업 및 AI 플랫폼 제공업체

- Amazon

- Apple

- Microsoft

- NVIDIA

- Cerence

- Nuance Communications

- SoundHound

- Tier 1 자동차 공급업체

- Robert Bosch

- Continental

- Denso Corporation

- 삼성

- Aptiv PLC

- Panasonic Automotive Systems Company

- Visteon Corporation

- 자동차 OEM

- Mercedes-Benz Group

- Ford Motor Company

- Hyundai Motor Company

- BMW Group

- General Motors

- Tata Motors Limited

- 신흥 기업 및 전문 기업

- Baidu

- Mihup Communications Private Limited

- Sensory

- NXP Semiconductors

The Global In-Vehicle Assistant Market was valued at USD 8.4 billion in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 21.3 billion by 2035.

Market expansion is driven by increasing consumer demand for safe, convenient, and hands-free vehicle interactions, alongside OEM commitments to introduce large numbers of electric and automated vehicles. The emergence of multimodal Human-Machine Interfaces (HMIs) is reshaping the industry, as automakers integrate voice, touch, and gesture-based inputs into connected vehicles. Large Language Models (LLMs) are enabling the development of smarter platforms and devices, allowing for more intuitive driver interactions and adoption across premium and entry-level vehicles alike. While the COVID-19 pandemic temporarily disrupted vehicle production and delayed new vehicle rollouts, the long-term demand for integrated voice assistants and advanced in-car digital experiences remains strong, supported by ongoing investments in connected and smart vehicle technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.4 Billion |

| Forecast Value | $21.3 Billion |

| CAGR | 9.7% |

The speech recognition segment accounted for 53% share in 2025 and is expected to grow at a CAGR of 8.7% from 2026 to 2035. This technology forms the core of in-vehicle assistant systems, translating audio signals captured by microphones into actionable text via automatic speech recognition (ASR) algorithms. Revenue streams include specialized automotive ASR software licensing, beamforming microphones, and dedicated digital signal processor (DSP) chips for acoustic processing.

The software segment held a 59% share in 2025 and is anticipated to grow at a CAGR of 8.2% through 2035. Software platforms include cloud-based natural language processing, voice recognition engines, software update management systems, and APIs that integrate third-party applications. Licensing models vary, with traditional vendors often employing per-vehicle subscription arrangements.

China In-Vehicle Assistant Market generated USD 2.6 billion in 2025. The country produces over thirty million vehicles annually, and government initiatives, such as the New Infrastructure Policy and Smart City programs, are accelerating vehicle connectivity. Regulations mandating voice-based emergency call systems and dedicated funding for intelligent connected vehicles further reinforce the market's growth trajectory.

Key players in the Global In-Vehicle Assistant Market include Microsoft, Apple, Amazon, Cerence, Continental, Google, Nuance, Panasonic Automotive, Samsung, and SoundHound. Companies in the in-vehicle assistant market are strengthening their position by investing in AI-driven voice recognition, multimodal HMI systems, and cloud platform integration. Strategic partnerships with OEMs ensure early adoption and long-term contracts. Continuous R&D in natural language processing, edge computing, and DSP optimization enhances performance and reliability. Expanding regional footprints, particularly in emerging automotive markets, allows companies to tap new customer bases. Licensing strategies, software subscriptions, and integration with third-party platforms further increase revenue streams while establishing brand presence and technological leadership.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component suppliers

- 3.1.1.2 Technology platform providers

- 3.1.1.3 System integrators

- 3.1.1.4 Automotive OEMs

- 3.1.1.5 Aftermarket distributors

- 3.1.1.6 End-users

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of connected & smart vehicles

- 3.2.1.2 Rising consumer demand for safety & hands-free interaction

- 3.2.1.3 Expansion of electric and autonomous vehicle (EV/AV) market

- 3.2.1.4 Growth of aftermarket & software upgrades

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High OEM integration cost

- 3.2.2.2 Privacy & data security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI-driven assistants

- 3.2.3.2 Multimodal HMI adoption

- 3.2.3.3 Cloud connectivity and OTA updates

- 3.2.3.4 Regional adoption of smart assistants

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 FMVSS Driver Distraction Guidelines

- 3.5.1.2 California ACC & ZEV Regulations

- 3.5.1.3 Transport Canada Connected Vehicle & Infotainment Guidelines

- 3.5.2 Europe

- 3.5.2.1 EU General Safety Regulation (GSR)

- 3.5.2.2 CE Certification for Automotive Infotainment

- 3.5.2.3 EU Vehicle Type Approval Directive

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan Automotive Electronics Safety Standards

- 3.5.3.2 China GB Standards for Connected Vehicles

- 3.5.3.3 India AIS / EMC Guidelines

- 3.5.4 Latin America

- 3.5.4.1 Brazil INMETRO Standards

- 3.5.4.2 Colombia Automotive Connected Systems Guidelines

- 3.5.4.3 Argentina Vehicle Electronics & Infotainment Regulations

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Standards for Connected & Voice-Enabled Vehicles

- 3.5.5.2 Oman Automotive Electronics Guidelines

- 3.5.5.3 South Africa SABS Automotive Voice & Infotainment Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 OEM Pricing models

- 3.8.2 Aftermarket pricing trends

- 3.8.3 Subscription vs one-time purchase models

- 3.8.4 Regional price variations

- 3.9 Patent analysis

- 3.10 Supply chain analysis

- 3.10.1 Component sourcing strategies

- 3.10.2 Semiconductor chip supply constraints

- 3.10.3 Cloud infrastructure dependencies

- 3.10.4 Regional supply chain dynamics

- 3.11 Go-to-market strategies

- 3.11.1 Region-specific market penetration strategies

- 3.11.2 Key regulatory considerations for new entrants

- 3.11.3 Pricing, service, and differentiation strategies

- 3.12 Commercial viability & deployment

- 3.12.1 Cost competitiveness vs. premium audio upsell value

- 3.12.2 OEM sourcing attractiveness and platform scalability

- 3.12.3 Aftermarket upgrade potential and dealer fitment economics

- 3.12.4 Localization, supply resilience, and logistics practicality

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Speech Recognition

- 5.3 Natural Language Processing (NLP)

- 5.4 Artificial Intelligence (AI)

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Software

- 6.2.1 Embedded software

- 6.2.2 Cloud-based software

- 6.2.3 Ai-powered software

- 6.3 Hardware

- 6.3.1 Microphones

- 6.3.2 Speakers

- 6.3.3 Control units

- 6.3.4 Display panels

- 6.4 Service

- 6.4.1 Integration and deployment

- 6.4.2 Maintenance and support

- 6.4.3 Consulting services

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Entertainment

- 8.4 Communication

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Technology Giants & AI Platform Providers

- 11.1.1 Amazon

- 11.1.2 Google

- 11.1.3 Apple

- 11.1.4 Microsoft

- 11.1.5 NVIDIA

- 11.1.6 Cerence

- 11.1.7 Nuance Communications

- 11.1.8 SoundHound

- 11.2 Tier 1 Automotive Suppliers

- 11.2.1 Robert Bosch

- 11.2.2 Continental

- 11.2.3 Denso Corporation

- 11.2.4 Samsung

- 11.2.5 Aptiv PLC

- 11.2.6 Panasonic Automotive Systems Company

- 11.2.7 Visteon Corporation

- 11.3 Automotive OEMs

- 11.3.1 Mercedes-Benz Group

- 11.3.2 Ford Motor Company

- 11.3.3 Hyundai Motor Company

- 11.3.4 BMW Group

- 11.3.5 General Motors

- 11.3.6 Tata Motors Limited

- 11.4 Emerging Players & Specialists

- 11.4.1 Baidu

- 11.4.2 Mihup Communications Private Limited

- 11.4.3 Sensory

- 11.4.4 NXP Semiconductors