|

시장보고서

상품코드

1936498

농업용 벌크 선박 로딩 및 언로딩 장비 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Agri-bulk Ship Loading and Unloading Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

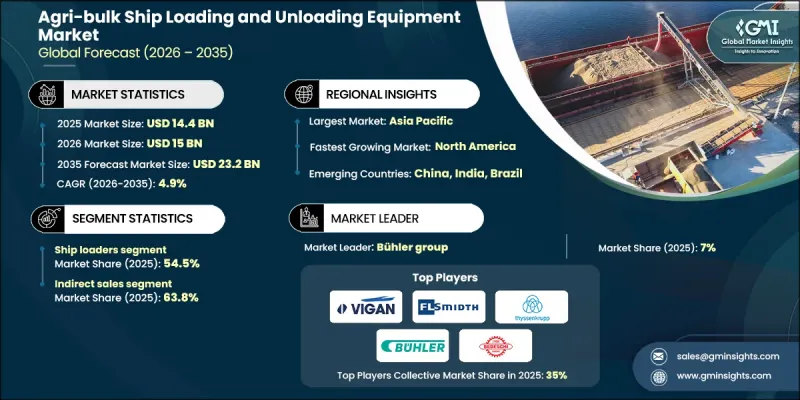

세계의 농업용 벌크 선박 로딩 및 언로딩 장비 시장은 2025년에 144억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.9%로 성장할 전망이며, 232억 달러에 이를 것으로 예측됩니다.

항만 및 벌크 터미널에서 자동화 및 기계화 솔루션으로의 전환이 수요를 견인하고 있으며, 기존의 수작업 및 중력 시스템은 고처리량의 농산물 수출에 비현실적이 되고 있습니다. 현대의 연속식 선박 하역 장치(CSU)는 밀폐형 컨베이어 시스템, 분진 억제, 회생 브레이크 기술을 채용한 환경 친화적인 솔루션으로서 대두하고 있어 에너지 소비를 최대 30-40% 삭감 가능하고, 세계의 지속가능성 목표에 따른 것입니다. 항만 인프라, 곡물 이송 시설, 산업용 해상 허브에 대한 투자가 북미, 유럽, 아시아태평양에서의 도입을 추진하고 있습니다. 곡물 거래업체와 터미널 운영자는 생산성 향상, 제품 손실 최소화, 업무 효율화를 실현하는 대용량 자동화 시스템을 점점 선호하고 있으며, 기술 업그레이드가 시장의 중심 동향이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 144억 달러 |

| 예측 금액 | 232억 달러 |

| CAGR | 4.9% |

2025년 선박 로더 부문은 78억 달러의 수익을 창출해, 54.5%의 점유율을 획득했습니다. 선박 로더는 처리 능력 향상, 선박의 턴어라운드 시간 단축, 운영 안전성 향상을 실현하는 능력으로부터 널리 채용되고 있습니다. 신축식 슛, 자동 위치 결정, 분진 억제 기술 등의 기능 통합으로 효율성 및 신뢰성이 향상되었습니다. 이 부문의 이점은 환경에 미치는 영향을 최소화하면서 성능을 극대화하도록 설계된 고용량 수출 터미널 및 고급 해상 화물 솔루션으로의 산업의 지속적인 전환을 반영합니다.

간접 판매 부문은 2025년에 63.8%의 점유율을 차지했으며, 지역 유통업체 및 엔지니어링 서비스 제공업체에 대한 시장 의존도를 부각시켰습니다. 이 유통모델은 특히 수확기 피크 시에 중요한 부품의 신속한 교환과 현지 보수 계약을 지원합니다. 항만 운영자는 이러한 채널을 통해 지역에 근거한 기술적 전문 지식에 액세스하여 복잡한 장비의 지속적인 운영과 적시 지원을 보장합니다.

미국의 농업용 벌크 선박 로딩 및 언로딩 장비 시장은 2025년에 64.4%의 점유율을 차지했으며, 곡물 수출 인프라에 대한 투자 및 현대화된 항만 물류를 통해 큰 수요를 창출했습니다. 환경 규제 준수, 먼지 대책 및 에너지 효율은 조달 결정을 좌우하는 주요 요소입니다. 보다 엄격한 환경 규제를 준수하면서 운영 처리량 향상에 주력하는 사업자들로 인해 미국 시장은 계속 성장하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계의 식량 안보 및 곡물 무역 확대

- 스마트 항만 구상 및 자동화

- 환경 규제 및 분진 대책

- 업계의 잠재적 위험 및 과제

- 높은 초기 설비 투자(CAPEX) 및 인프라 비용

- 기존 버스의 리노베이션 복잡성

- 기회

- 디지털 트윈 및 예지 보전

- 디지털 트윈 및 예지 보전

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서믄

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

- 수동

- 자동

- 반자동

제6장 시장 추계 및 예측 : 유통 채널별(2022-2035년)

- 직접

- 간접

제7장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- AGI(Ag Growth International)

- AUMUND Group

- Bedeschi Spa

- Buhler Group

- Cargotec(MacGregor)

- Ems-tech Inc.

- FLSmidth

- Konecranes

- Liebherr-International AG

- NEUERO Industrietechnik GmbH

- PNM Bulk Handling

- Siwertell AB

- Thyssenkrupp AG

- VIGAN Engineering SA

- WAMGROUP SpA

The Global Agri-bulk Ship Loading and Unloading Equipment Market was valued at USD 14.4 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 23.2 billion by 2035.

Demand is fueled by a shift toward automated and mechanized solutions in ports and bulk terminals, as traditional manual operations and gravity-fed systems become less viable for high-throughput agricultural exports. Modern continuous ship unloaders (CSUs) are emerging as a greener solution, incorporating closed conveyor systems, dust suppression, and regenerative braking technology, which can reduce energy consumption by up to 30-40%, aligning with global sustainability goals. Investment in port infrastructure, grain transfer facilities, and industrial maritime hubs is driving adoption across North America, Europe, and Asia-Pacific. Grain traders and terminal operators increasingly prefer high-capacity, automated systems that enhance productivity, minimize product loss, and streamline operations, making technological upgrades a central market trend.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.4 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 4.9% |

In 2025, the ship loaders segment generated USD 7.8 billion and capturing 54.5% share. Ship loaders are preferred for their ability to increase throughput, reduce vessel turnaround times, and enhance operational safety. Integration of features like telescopic chutes, automated positioning, and dust suppression technology has improved efficiency and reliability. The segment's dominance reflects the industry's ongoing shift toward high-capacity export terminals and advanced maritime handling solutions designed to maximize performance while minimizing environmental impact.

The indirect sales segment accounted for 63.8% share in 2025, highlighting the market's reliance on regional distributors and engineering service providers. This distribution model supports rapid replacement of critical components and on-site maintenance contracts, particularly during peak harvest seasons. Port operators rely on these channels to access localized technical expertise, ensuring uninterrupted operations and timely support for complex equipment.

U.S. Agri-bulk Ship Loading and Unloading Equipment Market held a 64.4% share in 2025, generating substantial demand through investments in grain export infrastructure and modernized port logistics. Environmental compliance, dust control measures, and energy efficiency are major factors shaping procurement decisions. The U.S. market continues to grow as operators focus on improving operational throughput while adhering to stricter environmental regulations.

Leading players in the Global Agri-bulk Ship Loading and Unloading Equipment Market include AGI (Ag Growth International), AUMUND Group, Bedeschi S.p.a., Buhler Group, Cargotec (MacGregor), Ems-tech Inc., FLSmidth, Konecranes, Liebherr-International AG, NEUERO Industrietechnik GmbH, PNM Bulk Handling, Siwertell AB, Thyssenkrupp AG, VIGAN Engineering S.A., and WAMGROUP S.p.A. Companies in Agri-bulk Ship Loading and Unloading Equipment Market are strengthening their presence through several strategies. They are investing in R&D to develop more energy-efficient, dust-free, and automated shiploader and unloader systems. Strategic partnerships with ports, grain terminals, and distributors enable better regional coverage and faster delivery of service contracts. Firms are expanding manufacturing capacities across Europe, North America, and Asia-Pacific to meet rising demand and reduce lead times. Additionally, companies are offering lifecycle services, predictive maintenance solutions, and modular system upgrades, which increase customer loyalty and reinforce long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global food security and grain trade expansion

- 3.2.1.2 Smart port initiatives and automation

- 3.2.1.3 Environmental regulations and dust control

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial CAPEX & infrastructure costs

- 3.2.2.2 Complexity of retrofitting existing berths

- 3.2.3 Opportunities

- 3.2.3.1 Digital twins and predictive maintenance

- 3.2.3.2 Digital twins and predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Automatic

- 5.4 Semi-automatic

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct

- 6.3 Indirect

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AGI (Ag Growth International)

- 8.2 AUMUND Group

- 8.3 Bedeschi S.p.a.

- 8.4 Buhler Group

- 8.5 Cargotec (MacGregor)

- 8.6 Ems-tech Inc.

- 8.7 FLSmidth

- 8.8 Konecranes

- 8.9 Liebherr-International AG

- 8.10 NEUERO Industrietechnik GmbH

- 8.11 PNM Bulk Handling

- 8.12 Siwertell AB

- 8.13 Thyssenkrupp AG

- 8.14 VIGAN Engineering S.A.

- 8.15 WAMGROUP S.p.A