|

시장보고서

상품코드

1936634

선박용 로더 및 언로더 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Ship Loader and Unloader Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

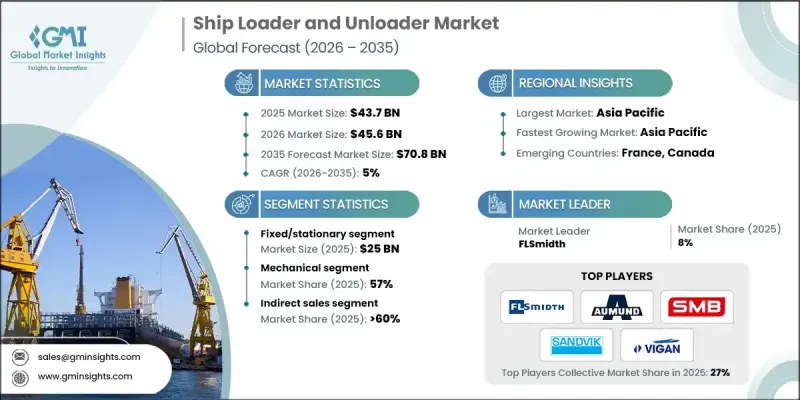

세계의 선박용 로더 및 언로더 시장은 2025년에 437억 달러로 평가되었으며, 2035년까지 CAGR 5%로 성장하여 708억 달러에 달할 것으로 예측됩니다.

국제 무역의 확대, 특히 석탄, 철광석, 곡물, 비료와 같은 벌크 상품에 대한 수요 증가는 대용량 하역 솔루션에 대한 수요를 주도하고 있습니다. 항만은 더 큰 화물을 효율적으로 처리해야 한다는 압력에 직면하고 있으며, 이로 인해 운영자는 자동화 및 기술적으로 진보된 장비의 도입을 촉진하고 있습니다. 대형 선박의 증가와 신속한 화물 처리에 대한 기대가 높아짐에 따라 현대 항만 운영에는 고성능 시스템이 필수적입니다. 세계화와 신흥 시장의 부상으로 인해 신뢰할 수 있는 벌크 자재 취급 인프라의 필요성이 더욱 강조되고 있습니다. 또한, 운영사업자는 IoT 지원 센서, 예지보전 알고리즘, 원격 모니터링 등 디지털 기술 및 스마트 기술을 도입하여 전 세계 항만 시설의 안전 기준과 신뢰성을 향상시키면서 운영 효율성 최적화, 다운타임 감소, 비용 절감을 실현하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 437억 달러 |

| 예측 금액 | 708억 달러 |

| CAGR | 5% |

시장에서는 환경 친화적이고 에너지 효율이 높은 시스템의 채택이 확대되고 있습니다. 전기식 및 하이브리드식 선박용 로더 및 언로더는 탄소 배출량을 줄이고 국제 환경 규제에 대응하기 위해 점점 더 많이 개발되고 있습니다. 최신 설비는 자동화와 AI 탑재 툴을 통합하여 성능 향상과 수동 조작을 최소화합니다. 이를 통해 항만은 지속가능성을 유지하면서 증가하는 물동량 수요에 대응할 수 있습니다.

고정식 부문은 2025년 250억 달러의 시장 규모를 창출했습니다. 고정식 선박 하역기는 높은 처리 능력, 내구성, 연속적인 벌크 자재 흐름을 처리할 수 있는 능력으로 인해 대규모 항만 작업에서 선호되고 있습니다. 견고한 설계로 장기적인 신뢰성과 최소한의 다운타임을 보장하며, 초기 투자비용은 높지만 장비의 수명주기 동안 비용 효율성이 뛰어납니다.

기계 부문은 2025년 57%의 점유율을 차지했습니다. 기계식 시스템은 벌크 재료 취급에서 입증된 신뢰성, 적응성, 비용 효율성으로 인해 주류로 자리 잡았습니다. 컨베이어 벨트, 스크류 컨베이어, 버킷 엘리베이터를 활용하는 이 시스템은 석탄, 광물, 곡물 취급에 있어 항만에서 널리 도입되고 있습니다. 최소한의 에너지 소비로 대량 작업을 관리할 수 있는 능력은 대규모 시설에서 우선적인 선택이 되고 있습니다.

아시아태평양의 선박 적재 및 하역 장비 시장은 2025년 40%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 5.3%로 확대될 것으로 예상됩니다. 중국은 방대한 항만 인프라와 국제 무역에서 확고한 지위를 바탕으로 이 지역을 주도하고 있습니다. 급속한 산업화, 높은 수출량, 첨단 화물 처리 시스템에 대한 지속적인 투자가 수요를 촉진하고 있습니다. 전략적 항만 현대화 계획과 자동화 도입은 시장을 더욱 강화하고 있습니다. 또한, 규제 준수와 환경적 지속가능성에 대한 노력은 에너지 절약 및 분진 억제 기능을 갖춘 설비의 도입을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 기술별, 2022-2035

제7장 시장 추정 및 예측 : 벌크별, 2022-2035

제8장 시장 추정 및 예측 : 용량별, 2022-2035

제9장 시장 추정 및 예측 : 용도별, 2022-2035

제10장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM 26.03.05The Global Ship Loader and Unloader Market was valued at USD 43.7 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 70.8 billion by 2035.

The expansion of international trade, particularly in bulk commodities like coal, iron ore, grains, and fertilizers, is driving demand for high-capacity loading and unloading solutions. Ports are facing increasing pressure to handle larger shipments efficiently, prompting operators to adopt automated and technologically advanced equipment. Larger vessels and faster turnaround expectations have made high-performance systems essential for modern port operations. The rise of globalization and emerging markets further emphasizes the need for reliable bulk material handling infrastructure. Additionally, operators are embracing digital and smart technologies, including IoT-enabled sensors, predictive maintenance algorithms, and remote monitoring, which optimize operational efficiency, reduce downtime, and lower costs while improving safety standards and reliability across port facilities worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $43.7 Billion |

| Forecast Value | $70.8 Billion |

| CAGR | 5% |

The market is witnessing a growing adoption of eco-friendly and energy-efficient systems. Electric and hybrid ship loaders and unloaders are increasingly developed to reduce carbon emissions and comply with international environmental regulations. Modern equipment integrates automation and AI-powered tools to enhance performance and minimize manual intervention, helping ports maintain sustainability while meeting rising throughput demands.

The fixed/stationary segment generated USD 25 billion in 2025. Fixed ship loaders and unloaders are preferred in large-scale port operations due to their high capacity, durability, and ability to handle continuous bulk material flow. Their robust design ensures long-term reliability and minimal downtime, making them cost-efficient over the lifecycle of the equipment despite higher initial investment.

The mechanical segment accounted for 57% share in 2025. Mechanical systems dominate due to their proven dependability, adaptability, and cost-effectiveness in handling bulk materials. Utilizing conveyor belts, screw conveyors, and bucket elevators, these systems are extensively deployed in ports for coal, mineral, and grain handling. Their ability to manage high-volume operations with minimal energy consumption makes them the preferred choice for large facilities.

Asia Pacific Ship Loader and Unloader Market held 40% share in 2025 and is expected to grow at a CAGR of 5.3% from 2026 to 2035. China leads the region due to its vast port infrastructure and strong position in international trade. Rapid industrialization, high export volumes, and continuous investment in advanced cargo handling systems are driving demand. Strategic port modernization initiatives and automation adoption further strengthen the market. Additionally, regulatory compliance and environmental sustainability measures encourage the use of energy-efficient and dust-suppressing equipment.

Major companies operating in the Global Ship Loader and Unloader Market include AMECO, AUMUND, BEUMER, Dana, Buhler, FLSmidth, EMS-Tech, FAM Forderanlagen Magdeburg, Liebherr, NEUERO, Sandvik, Shanghai Zhenhua Heavy Industries, TAKRAF, SMB, and VIGAN Engineering. Companies in the ship loader and unloader market focus on innovation, sustainability, and strategic expansion to reinforce their presence. They invest in R&D to develop high-capacity, automated, and eco-friendly systems that meet global trade demands and regulatory requirements. Collaborations with port operators and technology partners help integrate smart monitoring and predictive maintenance solutions, enhancing operational efficiency. Market players also expand geographically by targeting emerging markets with growing industrial trade and port infrastructure.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Bulk

- 2.2.5 Capacity

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global trade and bulk material handling

- 3.2.1.2 Automation and technological advancements

- 3.2.1.3 Environmental regulations and sustainability goals

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment and maintenance costs

- 3.2.2.2 Space and infrastructure limitations at ports

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of emerging economies and new port developments

- 3.2.3.2 Adoption of eco-friendly and energy-efficient solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By operating system

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fixed/stationary

- 5.3 Mobile

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Mechanical

- 6.4 Pneumatic

Chapter 7 Market Estimates and Forecast, By Bulk, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Dry

- 7.3 Liquid

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Up to 5000 t/h

- 8.3 5000 t/h to 10,000 t/h

- 8.4 10,000 t/h to 20,000 t/h

- 8.5 Above 20,000 t/h

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Mining

- 9.3 Ports and Shipping

- 9.4 Construction

- 9.5 Machinery

- 9.6 Others (power plant industry, etc.)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AMECO

- 12.2 AUMUND

- 12.3 BEUMER

- 12.4 Buhler

- 12.5 Dana

- 12.6 EMS-Tech

- 12.7 FAM Forderanlagen Magdeburg

- 12.8 FLSmidth

- 12.9 Liebherr

- 12.10 NEUERO

- 12.11 Sandvik

- 12.12 Shanghai Zhenhua Heavy Industries

- 12.13 SMB

- 12.14 TAKRAF

- 12.15 VIGAN Engineering