|

시장보고서

상품코드

1936525

의료기기용 열가소성 엘라스토머 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Thermoplastic Elastomers in Medical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

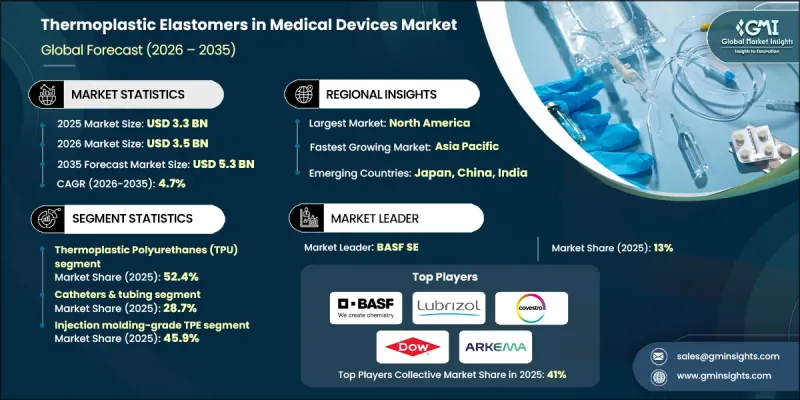

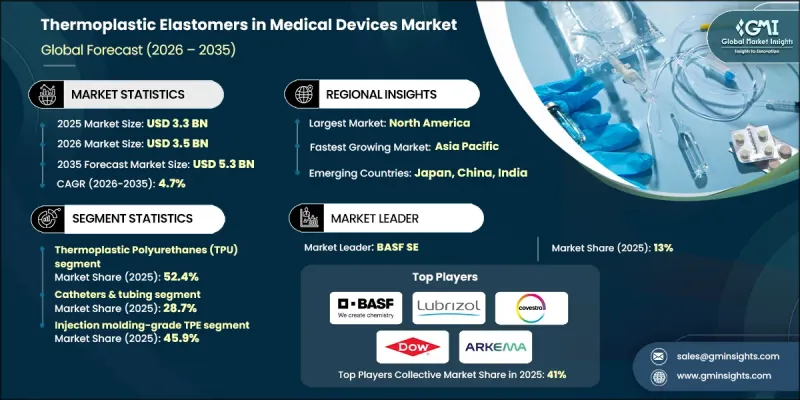

세계의 의료기기용 열가소성 엘라스토머 시장은 2025년 33억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 전망이며, 53억 달러에 이를 것으로 예측됩니다.

열가소성 엘라스토머(TPE)는 틈새 재료에서 현대 의료 제조에서 필수적인 구성요소로 꾸준히 진화해 왔습니다. 그 탄성, 생체 적합성, 효율적인 가공성을 겸비한 특성은 내구성이 뛰어나 환자 친화적인 의료 기술에 대한 수요 증가를 지원하고 있습니다. 의료 제공업체는 지속적인 성능을 발휘하면서 환자의 쾌적성을 향상시키는 솔루션을 점점 더 중시하고 있으며, 차세대 의료기기 개발에서 TPE가 우선하는 재료 클래스로서의 지위를 확립하고 있습니다. 엄격한 안전 기준과 환경 규제에 힘입어 지속가능성과 책임있는 재료 관리는 의료용 TPE 분야의 핵심 과제가 되고 있습니다. 생태계에 미치는 영향이 낮고 멸균 내성이 뛰어난 재생 가능 재료로의 전환은 채택을 가속화하고 있습니다. 지속적인 기술 혁신은 블렌딩의 안전성, 기계적 안정성, 내화학성 및 종합적인 수명을 향상시켜 기존 엘라스토머와 관련된 오랜 우려 사항을 해결합니다. 지속적인 임상 시험 및 환경 시험은 보다 안전한 의료 성과를 지원하면서 재료 과학을 진보시키는 업계의 노력을 반영합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 33억 달러 |

| 예측 금액 | 53억 달러 |

| CAGR | 4.7% |

열가소성 폴리우레탄(TPU)은 2025년에 52.4%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. TPU는 유연성 및 강도의 균형이 뛰어나 구조적 신뢰성을 손상시키지 않고 부드러움을 정밀하게 제어할 수 있기 때문에 의료용 등급의 열가소성 엘라스토머(TPE)로서 가장 널리 채용되고 있습니다. 이러한 특성은 복잡한 의료 엔지니어링 요구 사항을 지원하며 광범위한 의료 용도 분야에서 일관된 성능을 발휘합니다.

카테터 및 튜브 분야는 2025년에 28.7%의 점유율을 차지하였으며, 2026-2035년 CAGR 5.5%로 성장할 것으로 예측됩니다. 이 장점은 장기간 사용 사이클을 통해 생체적합성, 유연성 및 무균성을 유지하는 재료의 특성에 의해 지원됩니다. TPE는 일상적인 의료 절차부터 고급 치료 시스템에 이르기까지 신뢰할 수 있는 성능을 보장하며, 이 분야의 중요성을 더욱 강력하게 하고 있습니다.

북미의 의료기기용 열가소성 엘라스토머 시장은 2025년 35%의 점유율을 차지했습니다. 이 지역은 성숙한 의료 인프라, 엄격한 규제 모니터링, 의료기기 제조업체의 강력한 집적이라는 이점을 가지고 있습니다. 폴리머 조사 및 컴플라이언스 중심의 혁신에 대한 지속적인 투자는 안전 기준, 장비 기능 및 환자 경험 향상을 통해 지역 리더십을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- PVC에서 프탈산이 없는 대체품으로의 전환

- 라텍스 프리 의료 제품에 대한 수요 증가

- 고령화 및 만성질환의 유병률

- 업계의 잠재적 위험 및 과제

- 원재료 비용 상승 및 범용 PVC 비교

- 내열성 제한 및 열경화성 수지

- 시장 기회

- 지속 가능하고 바이오 기반 TPE 배합

- 항균 및 감염 예방 재료

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- TPE 화학 구조별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : TPE 요소별(2022-2035년)

- 열가소성 폴리우레탄(TPU)

- 폴리에테르계 TPU

- 폴리에스테르계 TPU

- 스티렌계 블록 공중합체(TPE-S/SEBS)

- SEBS(수소화 스티렌계)

- SBS 및 기타 스티렌계 변종

- 열가소성 가황체(TPV)

- PP/EPDM 동적 가황물

- 열가소성 코폴리에스테르 엘라스토머(COPE/TPC-ET)

- 폴리에테르글리콜/PBT 블록 공중합체

- 열가소성 폴리아미드 엘라스토머(PEBA/TPE-A)

- 열가소성 올레핀계 엘라스토머(TPE-O/TPO)

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 카테터 및 튜브

- 정맥내(IV) 카테터

- 비뇨기 카테터

- 심혈관 카테터 및 풍선 카테터

- 단강 및 다강 의료용 튜브

- 약물 전달 및 수액 튜브

- 의료기기 및 장치

- 치아 갈림증용 치과용 마우스피스

- 연동 펌프 튜브

- 요도 카테터용 그립 및 구성 부품

- 호흡용 페이스 마스크 및 씰

- 일회용 의료용품

- 인두 스와브 브러쉬

- 검사용 장갑(비라텍스제)

- 일회용 마스크 및 의류

- 의료용 필름, 백 및 포장재

- 점적 백 및 생리 식염수 백

- 바이오 의약품용 보존 백

- 경장 영양 및 정맥 영양 백

- 복막 및 투석 백

- 의료용 칩 및 가스켓

- 주입 병 캡 및 폐쇄 장치

- 주사기용 개스킷 및 플런저 선단부

- 바이알용 마개 및 셉터

- 외과용 및 진단용 기구

- 외과용 기구의 그립 핸들

- 진단 기기 케이스

- 의료용 신발

- 이식형 의료기기 및 그 구성 부품

- 외과용 메쉬(폴리머제)

- 폴리머제 인공 기관 부품

- 엘라스토머제 임플란트 블록

제7장 시장 추계 및 예측 : 가공 방법별(2022-2035년)

- 사출 성형용 등급 TPE

- 압출 성형용 등급 TPE

- 블로우 성형용 등급 TPE

- 오버몰드 코인젝션 등급 TPE

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- BASF SE

- Lubrizol Corporation

- Covestro AG

- Dow Chemical

- Arkema

- Teknor Apex

- Kraiburg TPE

- Hexpol/Elastron

- Kuraray

- RTP Company

- Evonik

- Kraton

- DSM Biomedical

- Trinseo

- Mitsubishi Chemical

The Global Thermoplastic Elastomers in Medical Devices Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 5.3 billion by 2035.

Thermoplastic elastomers have steadily evolved from niche materials into indispensable components within modern medical manufacturing. Their combination of elasticity, biocompatibility, and efficient processing supports the growing demand for durable, patient-friendly medical technologies. Healthcare providers increasingly prioritize solutions that deliver consistent performance while improving patient comfort, positioning TPEs as a preferred material class for next-generation device development. Sustainability and responsible material management have become central to the medical TPE landscape, driven by strict safety standards and environmental regulations. The shift toward recyclable materials with lower ecological impact and high sterilization resistance continues to accelerate adoption. Ongoing innovation addresses long-standing concerns related to conventional elastomers by improving formulation safety, mechanical stability, chemical resistance, and overall lifespan. Continuous clinical and environmental testing reflects the industry's commitment to advancing material science while supporting safer healthcare outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.7% |

Thermoplastic Polyurethanes accounted for 52.4% share in 2025 and are forecast to grow at a CAGR of 5% through 2035. TPU remains the most widely adopted medical-grade TPE due to its balance of flexibility and strength, which allows precise control over softness without compromising structural reliability. These attributes support complex medical engineering requirements and contribute to consistent performance across a wide range of medical applications.

The catheters and tubing segment held a 28.7% share in 2025 and is anticipated to grow at a CAGR of 5.5% during 2026-2035. This dominance is supported by the material's ability to maintain biocompatibility, flexibility, and sterility throughout extended use cycles. TPEs ensure reliable performance across both routine medical procedures and advanced therapeutic systems, reinforcing their importance within this segment.

North America Thermoplastic Elastomers in Medical Devices Market held a 35% share in 2025. The region benefits from a mature healthcare infrastructure, rigorous regulatory oversight, and a strong concentration of medical device manufacturers. Continued investment in polymer research and compliance-focused innovation strengthens regional leadership by enhancing safety standards, device functionality, and patient experience.

Key companies operating in the Global Thermoplastic Elastomers in Medical Devices Market include Lubrizol Corporation, BASF SE, Covestro AG, Arkema, Dow Chemical, Kuraray, Kraiburg TPE, Teknor Apex, Hexpol/Elastron, RTP Company, Kraton, Evonik, Mitsubishi Chemical, Trinseo, and DSM Biomedical. Companies operating in the Thermoplastic Elastomers in Medical Devices Market focus on material innovation, regulatory alignment, and long-term partnerships to strengthen their competitive position. Manufacturers invest heavily in research to improve formulation safety, mechanical performance, and sterilization compatibility while meeting evolving compliance requirements. Strategic collaborations with medical device producers allow early integration of customized materials into product design cycles. Firms also prioritize sustainability initiatives by developing recyclable and low-impact elastomer solutions. Capacity expansion, geographic diversification, and portfolio optimization further support market penetration, while consistent quality assurance and clinical validation help build trust with healthcare providers and regulatory bodies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 TPE Chemistry

- 2.2.3 Application

- 2.2.4 Processing Method

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift from PVC to phthalate-free alternatives

- 3.2.1.2 Growing demand for latex-free medical products

- 3.2.1.3 Aging population & chronic disease prevalence

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher material cost vs. Commodity PVC

- 3.2.2.2 Limited high-temperature resistance vs. Thermosets

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable & bio-based TPE formulations

- 3.2.3.2 Antimicrobial & infection-prevention materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By TPE Chemistry

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By TPE Chemistry, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic Polyurethanes (TPU)

- 5.2.1 Polyether-Based TPU

- 5.2.2 Polyester-Based TPU

- 5.3 Styrenic Block Copolymers (TPE-S/SEBS)

- 5.3.1 SEBS (Hydrogenated Styrenic)

- 5.3.2 SBS & Other Styrenic Variants

- 5.4 Thermoplastic Vulcanizates (TPV)

- 5.4.1 PP/EPDM Dynamic Vulcanizates

- 5.5 Thermoplastic Copolyester Elastomers (COPE/TPC-ET)

- 5.5.1 Polyether Glycol/PBT Block Copolymers

- 5.6 Thermoplastic Polyamide Elastomers (PEBA/TPE-A)

- 5.7 Thermoplastic Olefin Elastomers (TPE-O/TPO)

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Catheters & tubing

- 6.2.1 Intravenous (iv) catheters

- 6.2.2 Urological catheters

- 6.2.3 Cardiovascular catheters & balloon catheters

- 6.2.4 Single & multi-lumen medical tubing

- 6.2.5 Drug delivery & infusion tubing

- 6.3 Medical equipment & devices

- 6.3.1 Dental guards for bruxism disease

- 6.3.2 Peristaltic pump tubes

- 6.3.3 Urine catheter grips & components

- 6.3.4 Respiratory face masks & seals

- 6.4 Disposable medical goods

- 6.4.1 Throat swab brushes

- 6.4.2 Examination gloves (non-latex)

- 6.4.3 Disposable masks & garments

- 6.5 Medical films, bags & packaging

- 6.5.1 Iv & saline bags

- 6.5.2 Biopharmaceutical storage bags

- 6.5.3 Enteral & parenteral nutrition bags

- 6.5.4 Peritoneal & dialysis bags

- 6.6 Medical tips & gaskets

- 6.6.1 Infusion bottle caps & closures

- 6.6.2 Syringe gaskets & plunger tips

- 6.6.3 Vial stoppers & septa

- 6.7 Surgical & diagnostic instruments

- 6.7.1 Surgical instrument grips & handles

- 6.7.2 Diagnostic equipment housings

- 6.8 Medical footwear

- 6.9 Implantable devices & components

- 6.9.1 Surgical meshes (polymeric)

- 6.9.2 Polymeric prostheses components

- 6.9.3 Elastomeric implant blocks

Chapter 7 Market Estimates and Forecast, By Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Injection Molding-Grade TPE

- 7.3 Extrusion-Grade TPE

- 7.4 Blow Molding-Grade TPE

- 7.5 Overmolding & Co-Injection Grade TPE

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Lubrizol Corporation

- 9.3 Covestro AG

- 9.4 Dow Chemical

- 9.5 Arkema

- 9.6 Teknor Apex

- 9.7 Kraiburg TPE

- 9.8 Hexpol/Elastron

- 9.9 Kuraray

- 9.10 RTP Company

- 9.11 Evonik

- 9.12 Kraton

- 9.13 DSM Biomedical

- 9.14 Trinseo

- 9.15 Mitsubishi Chemical