|

시장보고서

상품코드

1936587

내시경 치료 기기 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Endotherapy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

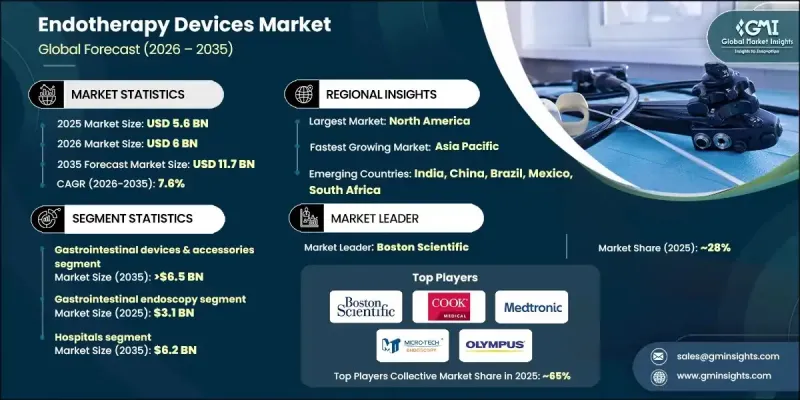

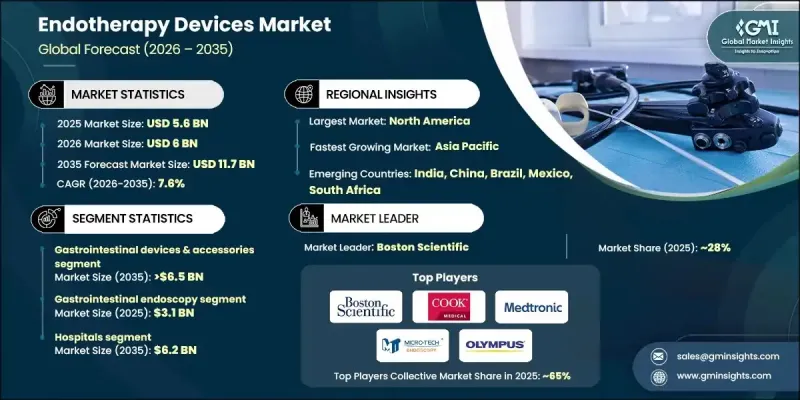

세계의 내시경 치료 기기 시장은 2025년에 56억 달러로 평가되었으며, 2035년까지 CAGR 7.6%로 성장하여 117억 달러에 달할 것으로 예측됩니다.

시장 확대의 주요 요인으로는 최소침습적 치료 접근법으로의 전환 가속화, 치료용 내시경 기술의 급속한 혁신, 외래 및 통원 치료 시설의 증가 등을 꼽을 수 있습니다. 내시경 치료 기기는 내시경 접근을 통해 이루어지는 치료 시술을 지원하기 위해 고안된 특수 기구로, 큰 외과적 절개 없이 체내 치료를 가능하게 합니다. 이러한 장치를 통해 임상의는 정확도를 높이고 환자의 회복 시간을 단축하는 동시에 표적화된 치료적 개입을 수행할 수 있습니다. 의료 시스템 전반에 걸쳐 시술 건수의 증가는 첨단 내시경 치료 솔루션에 대한 수요를 더욱 증가시키고 있습니다. 가시성 향상, 장비의 유연성, 에너지 공급 시스템, 자동화 기술의 지속적인 발전으로 시술의 정확성과 환자의 안전성이 향상되고 있습니다. 이러한 발전으로 내시경으로 관리할 수 있는 질환의 범위가 넓어지고, 기존 수술에 대한 의존도가 낮아지고 있습니다. 의료 서비스 제공자들이 더 나은 임상 결과와 운영 효율성을 제공하는 최신 시스템을 우선시하는 가운데, 지속적인 기술 업그레이드도 교체 수요에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 56억 달러 |

| 예측 금액 | 117억 달러 |

| CAGR | 7.6% |

내시경 치료 플랫폼은 고화질 영상, 강화된 콘트라스트 시각화, 첨단 광학 기술을 통합하여 점점 더 고도화되고 있습니다. 이러한 기능은 탐지 능력 향상과 보다 정확한 치료 투여를 지원하고, 임상적 신뢰성을 강화하며, 시술 성공률을 향상시킵니다. 가시성 향상은 의료기관 전반의 도입 확대에 있어서도 여전히 핵심적인 역할을 하고 있습니다.

2025년에는 소화기 장치 및 액세서리 부문이 56.4%의 점유율을 차지했습니다. 이는 일관되게 높은 시술 건수와 일상적인 내시경 치료에서 치료 도구를 광범위하게 사용하는 것에 기인합니다. 이 부문은 진단 및 중재적 시술에 소화기 내시경 치료를 광범위하게 적용함으로써 선도적인 위치를 유지하고 있습니다. 내시경 치료법의 사용 확대는 이 카테고리의 전문 액세서리 및 기기에 대한 지속적인 수요를 뒷받침하고 있습니다.

병원 부문은 2025년 54.6%의 점유율을 차지했으며, 2026년부터 2035년까지 62억 달러에 달할 것으로 전망됩니다. 병원은 다양한 환자 사례를 관리하고, 복잡하고 다학제적인 시술을 대량으로 시행하기 때문에 첨단 내시경 치료 기술에 대한 수요가 지속적으로 발생하고 있습니다. 이들 시설은 종합적인 내시경 인프라, 첨단 영상 진단 시스템, 전문 임상 노하우를 갖추고 있어 시장 도입에 있어 우위를 점하고 있습니다.

미국 내시경 치료 장비 시장은 2025년 23억 달러로 평가됐습니다. 내시경 검사에 대한 강력한 상환 제도와 지원적인 의료 자금 구조는 현대 내시경 치료 장비에 대한 투자를 지속적으로 촉진하고 모든 의료 현장에서 높은 이용률을 유지하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035

제6장 시장 추정 및 예측 : 용도별, 2022-2035

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSMThe Global Endotherapy Devices Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 11.7 billion by 2035.

Market expansion is driven by the increasing shift toward minimally invasive treatment approaches, rapid innovation in therapeutic endoscopy technologies, and the growing number of outpatient and ambulatory care facilities. Endotherapy devices are specialized instruments designed to support therapeutic procedures performed through endoscopic access, enabling internal treatment without large surgical incisions. These devices allow clinicians to perform targeted therapeutic interventions with improved accuracy and reduced patient recovery time. Rising procedural volumes across healthcare systems are reinforcing demand for advanced endotherapy solutions. Continuous improvements in visualization quality, device flexibility, energy delivery systems, and automation are enhancing procedural precision and patient safety. These advancements are broadening the range of conditions that can be managed endoscopically, reducing reliance on conventional surgery. Ongoing technology upgrades are also contributing to replacement demand, as healthcare providers prioritize modern systems that deliver better clinical outcomes and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 7.6% |

Endotherapy platforms are becoming increasingly sophisticated, integrating high-definition imaging, enhanced contrast visualization, and advanced optical technologies. These features support improved detection capabilities and more accurate therapeutic delivery, strengthening clinical confidence and improving procedural success rates. Enhanced visualization continues to play a central role in expanding adoption across healthcare facilities.

The gastrointestinal devices and accessories segment accounted for 56.4% share in 2025, supported by consistently high procedure volumes and widespread use of therapeutic tools in routine endoscopic care. The segment maintains its leadership position due to the broad application of gastrointestinal endotherapy across diagnostic and interventional procedures. Growing utilization of endoscopic treatment methods continues to support sustained demand for specialized accessories and devices within this category.

The hospitals segment generated 54.6% share in 2025 and is expected to reach USD 6.2 billion during 2026-2035. Hospitals manage a wide range of patient cases and perform a high volume of complex and multidisciplinary procedures, driving consistent demand for advanced endotherapy technologies. These facilities are equipped with comprehensive endoscopy infrastructure, advanced imaging systems, and specialized clinical expertise, reinforcing their dominance in market adoption.

U.S. Endotherapy Devices Market was valued at USD 2.3 billion in 2025. Strong reimbursement coverage for endoscopic procedures and supportive healthcare funding structures continue to encourage investment in modern endotherapy equipment, sustaining high utilization rates across care settings.

Key companies active in the Global Endotherapy Devices Market include Medtronic, OLYMPUS, Boston Scientific, KARL STORZ, FUJIFILM, Johnson & Johnson, Cook Medical, CONMED, Smith+Nephew, Stryker, B. BRAUN, Endo-Med, MICRO-TECH, M.I. Tech, and TAEWOONG MEDICAL. These companies maintain competitive positions through innovation, product breadth, and global distribution networks. To strengthen their presence, companies in the endotherapy devices sector focus heavily on continuous product innovation and technological differentiation. Strategic investments in advanced imaging, energy-based tools, and device miniaturization enhance clinical performance and usability. Manufacturers are expanding geographic reach through partnerships, acquisitions, and distribution agreements to access high-growth markets. Training programs and physician education initiatives are used to drive adoption and long-term customer loyalty.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of gastrointestinal disorders

- 3.2.1.2 Growing demand for minimally invasive procedures

- 3.2.1.3 High volume of endoscopic procedures

- 3.2.1.4 Technological advancements in endoscopic devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced endotherapy devices

- 3.2.2.2 Risk of procedure-related complications

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of single-use endotherapy devices

- 3.2.3.2 Integration of robotics and AI in endotherapy

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Pricing analysis

- 3.10 Start-up scenarios

- 3.11 Consumer insights

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Gastrointestinal devices & accessories

- 5.2.1 Biopsy forceps

- 5.2.1.1 Single-use biopsy forceps

- 5.2.1.2 Reusable biopsy forceps

- 5.2.1.3 Hot biopsy forceps

- 5.2.2 Injection needles

- 5.2.2.1 EUS-guided FNA (fine needle aspiration) needles

- 5.2.2.2 EUS-guided FNB (fine needle biopsy) needles

- 5.2.2.3 Other injection needles

- 5.2.3 Endoscopic submucosal dissection (ESD) knives

- 5.2.3.1 Needle-tipped knives

- 5.2.3.2 Insulation-tipped knives

- 5.2.4 Polypectomy snares

- 5.2.5 Hemoclips

- 5.2.6 Graspers

- 5.2.7 Hemostasis forceps

- 5.2.8 Sclerotherapy needles

- 5.2.9 Other gastrointestinal devices & accessories

- 5.2.1 Biopsy forceps

- 5.3 Endoscopic retrograde cholangiopancreatography (ERCP) devices & accessories

- 5.3.1 Metal stents

- 5.3.2 Sphincterotome

- 5.3.3 Guide wire

- 5.3.4 Catheter

- 5.3.4.1 Guiding catheter

- 5.3.4.2 Dilation catheter

- 5.3.4.3 Drainage catheter

- 5.3.4.4 Other catheters

- 5.3.5 Plastic stents

- 5.3.6 Balloon dilation

- 5.3.7 Extraction basket

- 5.3.8 Extraction balloon

- 5.3.9 Other ERCP devices & accessories

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Gastrointestinal endoscopy

- 6.3 Laparoscopy

- 6.4 Arthroscopy

- 6.5 Urology endotherapy

- 6.6 Bronchoscopy

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. BRAUN

- 9.2 Boston Scientific

- 9.3 CONMED

- 9.4 Cook Medical

- 9.5 Endo-Med

- 9.6 FUJIFILM

- 9.7 Johnson & Johnson

- 9.8 KARL STORZ

- 9.9 M.I. Tech

- 9.10 Medtronic

- 9.11 MICRO-TECH

- 9.12 OLYMPUS

- 9.13 Smith+Nephew

- 9.14 Stryker

- 9.15 TAEWOONG MEDICAL