|

시장보고서

상품코드

1936590

대형 가스 터빈 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Heavy Duty Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

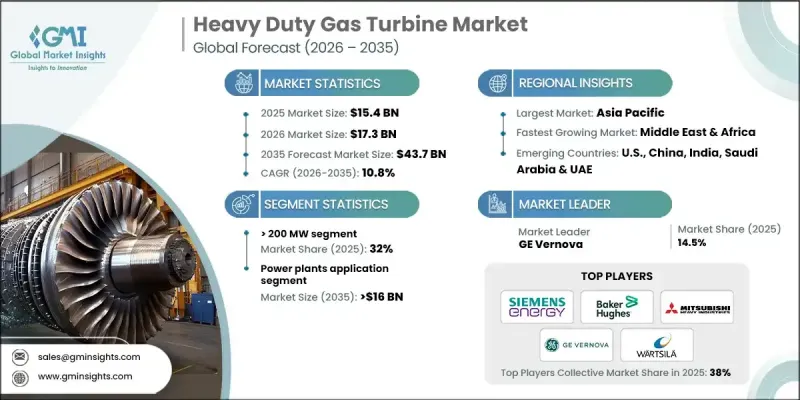

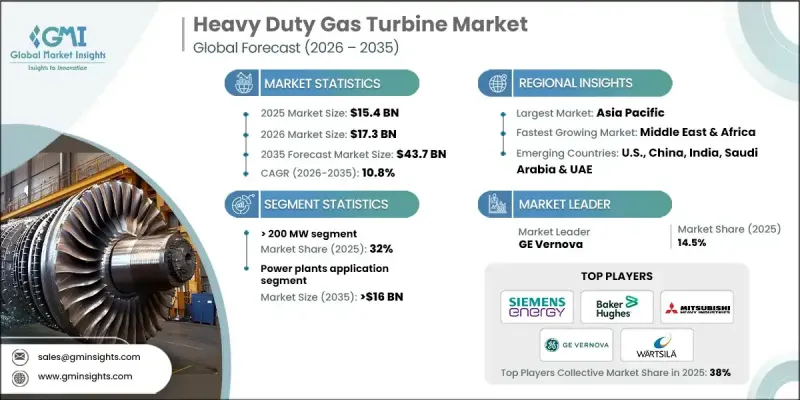

세계의 대형 가스 터빈 시장은 2025년에 154억 달러로 평가되었으며, 2035년까지 CAGR 10.8%로 성장하여 437억 달러에 달할 것으로 예측됩니다.

전 세계 전력 소비의 증가와 저배출 발전으로의 점진적인 전환은 첨단 가스 터빈 솔루션에 대한 수요를 지속적으로 뒷받침하고 있습니다. 정부와 전력 사업자들은 노후화된 인프라를 갱신하고 송전망의 성능을 향상시키면서 과도기적 에너지원으로 가스발전에 대한 의존도를 높이고 있습니다. 대형 가스 터빈은 안정적인 출력, 높은 가동률, 긴 수명을 실현하기 위해 개발된 고도로 설계된 동력 시스템입니다. 이 터빈은 고도의 시스템 통합, 정교한 연소 제어, 정밀한 공기역학적 설계를 통해 열 성능을 극대화하도록 설계되었습니다. 까다로운 조건에서도 안정적인 운전을 실현하는 동시에 변동하는 계통 부하에 대응하는 데 필요한 운영 유연성을 제공합니다. 다양한 연료 경로에 대응할 수 있는 능력은 진화하는 에너지 전략에서 그 중요성이 더욱 커지고 있습니다. 전력 시스템이 효율성과 성능 중심으로 전환하는 가운데, 대형 가스 터빈은 에너지 안보와 장기적인 지속가능성 목표를 모두 지원하는 현대 발전 투자의 핵심으로 남아있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 154억 달러 |

| 예측 금액 | 437억 달러 |

| CAGR | 10.8% |

200MW 이상 부문은 2025년 32%의 점유율을 차지하며 2035년까지 CAGR 10.5%로 성장할 것으로 예상됩니다. 이 부문의 성장은 전력 수요 증가, 더 엄격한 효율성에 대한 기대, 그리고 장기적인 탈탄소화 목표에 의해 뒷받침되고 있습니다. 전력회사들은 진화하는 환경적 요구사항에 대한 적합성을 유지하면서 운영 유연성, 출력 효율 향상, 시스템 최적화를 강화할 수 있는 대용량 터빈을 점점 더 선호하고 있습니다.

석유 및 가스용 대형 가스 터빈 부문은 2025년 23억 달러의 시장 규모를 창출했습니다. 이러한 터빈은 에너지 생산, 운송 및 가공 공정에서 지속적인 기계 구동 및 발전 수요를 지원하는 중요한 역할을 담당하고 있습니다. 원격지 및 혹독한 운영 환경에서의 안정적인 성능에 대한 요구로 인해 수요는 계속 강세를 보이고 있습니다. 운영자는 내구성, 연장된 서비스 간격, 연속 운전 시 안정된 효율성, 그리고 엄격해지는 배기가스 규제에 대한 적합성을 중요하게 생각합니다.

미국 대형 가스 터빈 시장은 2025년 74%의 점유율을 차지하며 26억 달러 규모에 달할 것으로 예상됩니다. 전력 수요 증가, 인프라 갱신, 장기적인 배출량 감축 목표가 시장 성장을 뒷받침하고 있습니다. 전력회사들은 운영 유연성, 계통 안정성, 비용 효율성이 뛰어난 고성능 발전 설비에 대한 투자를 지속하고 있으며, 이는 지역 시장에서의 주도적 지위를 강화하는 요인으로 작용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 용량별, 2022-2035

제6장 시장 규모 및 예측 : 기술별, 2022-2035

제7장 시장 규모 및 예측 : 용도별, 2022-2035

제8장 시장 규모 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global Heavy Duty Gas Turbine Market was valued at USD 15.4 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 43.7 billion by 2035.

Rising global electricity consumption, combined with the gradual shift toward lower-emission power generation, continues to support demand for advanced gas turbine solutions. Governments and power producers increasingly rely on gas-based generation as a transitional energy source while upgrading aging infrastructure and improving grid performance. Heavy duty gas turbines represent highly engineered power systems developed to deliver consistent output, high availability, and long operational life. These turbines are designed to maximize thermal performance through advanced system integration, refined combustion control, and precision-driven aerodynamic design. They operate reliably under demanding conditions while providing the operational flexibility required to respond to fluctuating grid loads. Their ability to accommodate multiple fuel pathways further strengthens their relevance within evolving energy strategies. As power systems become more efficiency-driven and performance-focused, heavy duty gas turbines remain central to modern power generation investments, supporting both energy security and long-term sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.4 Billion |

| Forecast Value | $43.7 Billion |

| CAGR | 10.8% |

The segment rated above 200 MW accounted for 32% share in 2025 and is expected to grow at a CAGR of 10.5% through 2035. Growth in this segment is supported by rising power demand, stricter efficiency expectations, and long-term decarbonization objectives. Utilities increasingly favor large-capacity turbines that offer operational flexibility, improved output efficiency, and enhanced system optimization while maintaining compliance with evolving environmental requirements.

The oil & gas heavy duty gas turbine segment generated USD 2.3 billion in 2025. These turbines play a critical role across energy production, transportation, and processing operations by supporting continuous mechanical drive and power generation needs. Demand remains strong due to the requirement for dependable performance in remote locations and challenging operating environments. Operators emphasize durability, extended service intervals, consistent efficiency under continuous operation, and adherence to increasingly stringent emissions regulations.

US Heavy Duty Gas Turbine Market accounted for 74% share and generated USD 2.6 billion in 2025. Market growth is supported by increasing electricity requirements, infrastructure upgrades, and long-term emissions reduction targets. Utilities continue to invest in high-efficiency power generation assets that offer operational flexibility, grid stability, and cost-effective performance, reinforcing the country's leadership position within the regional market.

Major companies operating in the Global Heavy Duty Gas Turbine Market include Siemens Energy, Mitsubishi Heavy Industries, GE Vernova, Ansaldo Energia, Baker Hughes, Rolls Royce, Wartsila, MAN Energy Solutions, Doosan Enerbility, Kawasaki Heavy Industries, Shanghai Electric Gas Turbine, Harbin Electric, Bharat Heavy Electricals, Solar Turbines, Vericor, Ethos Energy Group, Flex Energy Solutions, Centrax Gas Turbines, Boldrocchi, Nanjing Steam Turbine Motor, Capstone Green Energy, and Destinus Energy. Companies operating in the heavy duty gas turbine market focus on strengthening their market position through continuous performance improvement, lifecycle optimization, and technology differentiation. Many invest heavily in efficiency enhancement, emissions reduction capabilities, and long-term reliability to meet evolving utility and industrial requirements. Strategic partnerships with utilities and energy developers support early-stage project integration and recurring service contracts. Firms also prioritize digitalization to improve asset monitoring, maintenance planning, and operational transparency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Capacity trends

- 2.1.3 Technology trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of heavy duty gas turbines

- 3.8 Price trend analysis (USD/MW)

- 3.8.1 By region

- 3.8.2 By capacity

- 3.9 Emerging opportunities & technological trends

- 3.10 Investment landscape & future prospects

- 3.11 Digital transformation & industry 4.0 integration

- 3.12 Sustainability initiatives & decarbonization strategies

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Open cycle

- 6.3 Combined cycle

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Power plants

- 7.3 Oil & gas

- 7.4 Process plants

- 7.5 Aviation

- 7.6 Marine

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Finland

- 8.3.8 Greece

- 8.3.9 Denmark

- 8.3.10 Romania

- 8.3.11 Poland

- 8.3.12 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 India

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Thailand

- 8.4.8 Malaysia

- 8.4.9 Bangladesh

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 Bahrain

- 8.5.9 Iraq

- 8.5.10 Jordan

- 8.5.11 Lebanon

- 8.5.12 South Africa

- 8.5.13 Nigeria

- 8.5.14 Algeria

- 8.5.15 Kenya

- 8.5.16 Ghana

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Peru

Chapter 9 Company Profiles

- 9.1 Ansaldo Energia

- 9.2 Baker Hughes

- 9.3 Boldrocchi

- 9.4 Bharat Heavy Electricals

- 9.5 Capstone Green Energy

- 9.6 Centrax Gas Turbines

- 9.7 Destinus Energy

- 9.8 Doosan Enerbility

- 9.9 Ethos Energy Group

- 9.10 Flex Energy Solutions

- 9.11 GE Vernova

- 9.12 Harbin Electric

- 9.13 Kawasaki Heavy Industries

- 9.14 MAN Energy Solutions

- 9.15 Mitsubishi Heavy Industries

- 9.16 Nanjing Steam Turbine Motor

- 9.17 Rolls Royce

- 9.18 Siemens Energy

- 9.19 Shanghai Electric Gas Turbine

- 9.20 Solar Turbines

- 9.21 Vericor

- 9.22 Wartsila