|

시장보고서

상품코드

1936613

자동차 회생제동 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Regenerative Braking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

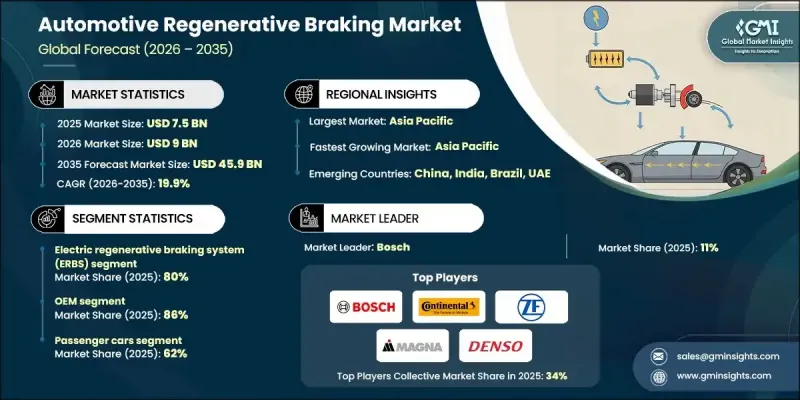

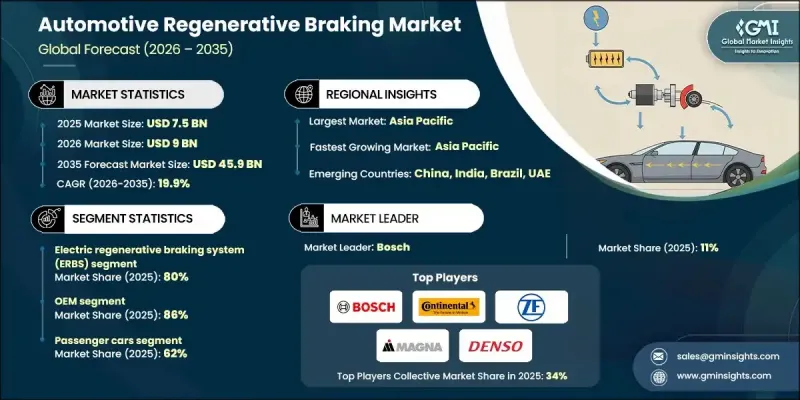

세계의 자동차 회생제동 시장은 2025년에 75억 달러로 평가되었으며, 2035년까지 CAGR 19.9%로 성장하여 459억 달러에 달할 것으로 예측됩니다.

회생제동시스템은 감속 시 운동 에너지를 회수하여 재사용 가능한 전기 에너지로 변환함으로써 자동차 산업의 전동화 및 지속가능성으로의 전환을 지원합니다. 이러한 시스템은 전기식, 유압식, 운동에너지식, 공압식 기술에 이르기까지 승용차, 상용차, 이륜차, 특수목적 차량에 광범위하게 적용되고 있습니다. 정밀한 제동 성능과 효율적인 에너지 회수를 실현하여 자율주행 시스템 및 ADAS(첨단 운전자 보조 시스템)에서 중요한 역할을 담당하고 있습니다. 첨단 센서, 실시간 데이터 처리, 기계 학습을 통해 다양한 주행 조건에서 에너지 회수를 극대화합니다. 배출량 감축을 위한 정부 규제와 배터리, 슈퍼커패시터, 파워 일렉트로닉스 분야의 혁신이 결합되어 성능이 크게 향상되고 있습니다. 리튬이온 배터리는 현재 250Wh/kg 이상의 성능을 달성했으며, 탄화규소 반도체는 에너지 변환 손실을 40-50% 감소시켜 회생 제동 효율을 70%에서 90% 이상으로 향상시켰습니다. 자동차 산업의 디지털화, 전동화, 에너지 효율적인 모빌리티 솔루션에 대한 관심이 시장 성장을 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 75억 달러 |

| 예측 금액 | 459억 달러 |

| CAGR | 19.9% |

전기 회생제동시스템(ERBS) 부문은 2025년에 80%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 20.3%의 성장률을 기록할 것으로 예측됩니다. ERBS는 트랙션 모터의 발전기 모드를 통해 운동 에너지를 전기로 변환하여 차량 배터리에 저장합니다. 이 기술은 높은 에너지 변환 효율, 전기 및 하이브리드 파워트레인과의 완벽한 통합, 첨단 차량 제어 시스템과의 호환성을 제공합니다. ERBS는 배터리 전기자동차 및 플러그인 하이브리드 차량에 광범위하게 적용되고 있으며, 48볼트 시스템을 탑재한 마일드 하이브리드 차량에 대한 도입도 확대되고 있습니다.

OEM 부문은 2025년 86%의 점유율을 차지할 것이며, 2035년까지 연평균 20.2%의 성장률을 기록할 것으로 예상됩니다. OEM 채널에는 차량 생산 공정에 통합되는 회생제동시스템이 포함되며, 공장 출하 장치 및 자동차 제조업체를 위한 조립 공급품이 포함됩니다. 제조 공정에서의 통합은 차량 파워트레인 및 제어 시스템과의 호환성을 보장하고, 공급망의 안정성을 제공하며, 여러 차량 프로그램 및 모델 연도에 걸친 공동 개발을 촉진합니다.

중국 자동차 회생 브레이크 시장은 2026년부터 2035년까지 CAGR 20.3%로 성장할 것으로 예상됩니다. 연간 자동차 판매량 2,600만 대를 자랑하는 중국은 보조금, 인허가 특혜, 기존 엔진 규제를 통해 전기자동차 보급을 촉진하는 정부 정책에 힘입어 전 세계 전기자동차 보급을 선도하고 있습니다. 국내 제조사들은 회생제동장치를 표준 장비로 채택하고, 자사 차량 라인업 전체에 기술 적용을 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술별, 2022-2035

제6장 시장 추정 및 예측 : 차종별, 2022-2035

제7장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제8장 시장 추정 및 예측 : 추진력별, 2022-2035

제9장 시장 추정 및 예측 : 지역별, 2022-2035

제10장 기업 개요

KSM 26.03.05The Global Automotive Regenerative Braking Market was valued at USD 7.5 billion in 2025 and is estimated to grow at a CAGR of 19.9% to reach USD 45.9 billion by 2035.

Regenerative braking systems capture kinetic energy during deceleration and convert it into reusable electrical energy, supporting the automotive industry's shift toward electrification and sustainability. These systems span electric, hydraulic, kinetic, and pneumatic technologies and are used across passenger vehicles, commercial vehicles, two-wheelers, and specialized applications. They play an essential role in autonomous and advanced driver-assistance systems (ADAS) by delivering precise braking and recovering energy efficiently. With advanced sensors, real-time data processing, and machine learning, these systems maximize energy recovery under diverse driving conditions. Government regulations aimed at reducing emissions, coupled with innovations in batteries, supercapacitors, and power electronics, have significantly enhanced performance. Lithium-ion batteries now surpass 250 Wh/kg, and silicon carbide semiconductors reduce energy conversion losses by 40-50%, improving regenerative braking efficiency from 70% to over 90%. Market growth is fueled by the automotive sector's increasing focus on digitalization, electrification, and energy-efficient mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.5 Billion |

| Forecast Value | $45.9 Billion |

| CAGR | 19.9% |

The electric regenerative braking systems (ERBS) segment accounted for 80% share in 2025 and is expected to grow at a CAGR of 20.3% from 2026 to 2035. ERBS converts kinetic energy into electricity via the traction motor's generator mode, storing it in the vehicle battery. This technology offers high energy conversion efficiency, seamless integration with electric and hybrid powertrains, and compatibility with advanced vehicle control systems. ERBS is widely used in battery electric and plug-in hybrid vehicles, with adoption expanding in mild hybrids with 48-volt systems.

The OEM segment held 86% share in 2025 and is growing at a CAGR of 20.2% through 2035. OEM channels involve regenerative braking systems integrated during vehicle production, including factory-installed units and those supplied to automakers for assembly. Integration during manufacturing ensures compatibility with vehicle powertrains and control systems, offering supply chain stability and facilitating collaborative development across multiple vehicle programs and model years.

China Automotive Regenerative Braking Market is expected to grow at a CAGR of 20.3% from 2026 to 2035. With annual vehicle sales of 26 million, China leads global adoption, supported by government policies promoting EV use through subsidies, licensing incentives, and restrictions on conventional engines. Domestic manufacturers have established regenerative braking as a standard feature, accelerating technology deployment across their vehicle portfolios.

Key companies operating in the Global Automotive Regenerative Braking Market include Brembo, Aisin Seiki, Denso, BorgWarner, Robert Bosch, Continental, Valeo, Magna, Hitachi Astemo, and ZF Friedrichshafen. Market players are strengthening their presence by developing next-generation regenerative braking solutions with higher energy recovery efficiency and seamless integration with electrified powertrains. They are forming strategic partnerships with automakers to ensure early adoption across multiple vehicle platforms. Investments in R&D focus on advanced sensors, real-time energy management, and machine learning to optimize system performance. Companies are also expanding production capabilities and supply chain networks to meet growing demand. Additionally, collaborations with battery and power electronics manufacturers enhance system efficiency and reliability, while marketing efforts highlight sustainability and compliance with evolving global emission standards, reinforcing competitive positioning and market credibility.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Vehicles

- 2.2.4 Sales Channel

- 2.2.5 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rapid adoption of EVs, HEVs, and PHEVs.

- 3.2.1.3 Stricter emission regulations and environmental awareness.

- 3.2.1.4 Rising demand for fuel-efficient vehicles.

- 3.2.1.5 Technological advancements in braking systems.

- 3.2.1.6 Shift toward smart and connected vehicles.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of regenerative braking systems

- 3.2.2.2 Complex integration with existing vehicle systems

- 3.2.3 Market opportunities

- 3.2.3.1 Rising electric and hybrid vehicle adoption

- 3.2.3.2 Expansion of EV charging infrastructure

- 3.2.3.3 Growing demand for fuel-efficient and eco-friendly vehicles

- 3.2.3.4 Government incentives and subsidies

- 3.2.3.5 Integration with smart and connected vehicle technologies

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- FMVSS regulating braking and energy recovery systems

- 3.4.1.2 Canada - MVSR covering brake system performance and safety compliance

- 3.4.2 Europe

- 3.4.2.1 Germany- EU Regulation 168/2013 on advanced braking systems

- 3.4.2.2 UK- UK road vehicles (Construction and Use) regulations 1986

- 3.4.2.3 France- RE2020 promoting energy-efficient braking

- 3.4.2.4 Italy- PNRR road safety mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB/T vehicle safety standards

- 3.4.3.2 India- Motor vehicles (Amendment) Act 2019

- 3.4.3.3 Japan- i-Construction and road traffic act

- 3.4.3.4 Australia- ADR covering regenerative braking integration

- 3.4.4 LATAM

- 3.4.4.1 Mexico- Official Mexican standard NOM-036-SCFI-2018

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing analysis

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Use cases & success stories

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric regenerative braking system (ERBS)

- 5.3 Hydraulic regenerative braking system (HRBS)

- 5.4 Kinetic regenerative braking system (KRBS)

- 5.5 Pneumatic regenerative braking

Chapter 6 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Medium commercial vehicles (MCVs)

- 6.3.3 Heavy commercial vehicles (HCVs)

- 6.4 Two-Wheelers

- 6.4.1 Electric scooters

- 6.4.2 Electric motorcycles

- 6.5 Others

- 6.5.1 Buses

- 6.5.2 Specialty vehicles

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Internal combustion engine (ICE) vehicles

- 8.3 Hybrid electric vehicles (HEV)

- 8.4 Plug-in hybrid electric vehicles (PHEV)

- 8.5 Battery electric vehicles (BEV)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aisin Seiki

- 10.1.2 BorgWarner

- 10.1.3 Continental

- 10.1.4 Delphi Technologies

- 10.1.5 Denso

- 10.1.6 Eaton

- 10.1.7 Hitachi Astemo

- 10.1.8 Hyundai Mobis

- 10.1.9 Magna International

- 10.1.10 Robert Bosch

- 10.1.11 Valeo

- 10.1.12 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 ADVICS

- 10.2.2 Akebono Brake Industry

- 10.2.3 Brembo

- 10.2.4 General Motors

- 10.2.5 Honda Motor

- 10.2.6 Mando

- 10.2.7 Mazda Motor

- 10.2.8 Nissin Kogyo

- 10.2.9 Schaeffler

- 10.2.10 Toyota Motor

- 10.3 Emerging Technology Innovators

- 10.3.1 Faurecia

- 10.3.2 Punch Powertrain

- 10.3.3 Skeleton Technologies