|

시장보고서

상품코드

1936661

자동차 에어백 인플레이터 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Airbag Inflator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

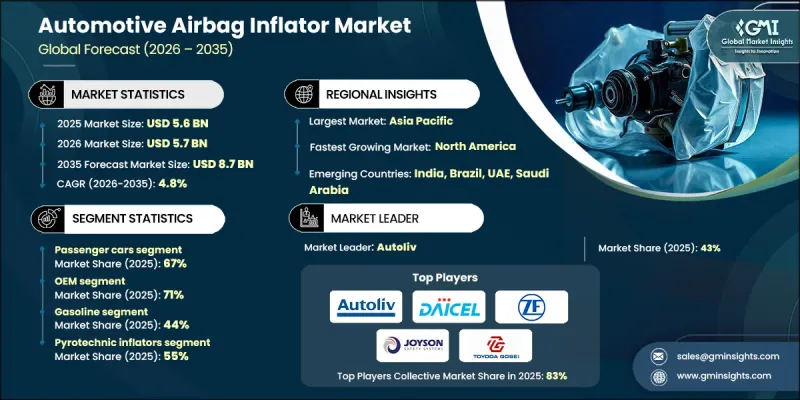

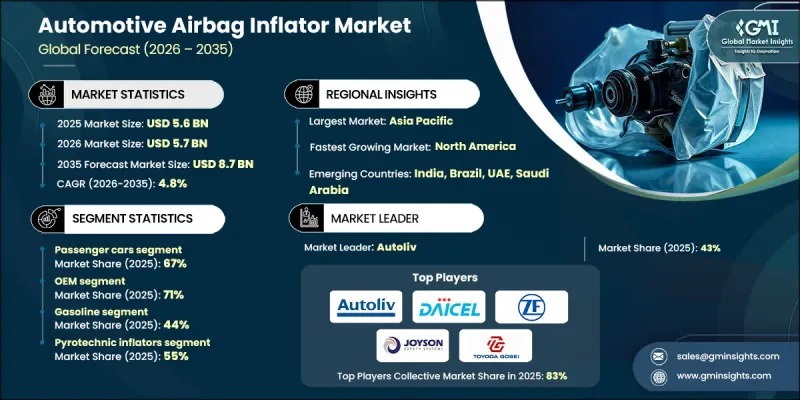

세계의 자동차 에어백 인플레이터 시장은 2025년에 56억 달러로 평가되었으며, 2035년까지 CAGR 4.8%로 성장하여 87억 달러에 달할 것으로 예측됩니다.

세계 자동차 생산량 증가가 이러한 성장의 주요 촉진요인으로 작용하고 있습니다. 제조업체들이 급증하는 수요에 대응하기 위해 생산량을 늘리면서 신차 1대당 여러 개의 에어백 인플레이터가 필요하기 때문에 설치율이 상승하고 장기 공급 계약이 강화되고 있습니다. 이러한 생산량 증가는 규모의 경제를 향상시키고, 다양한 차종 부문에서 첨단 인플레이터 기술의 채택을 가속화하고 있습니다. 소비자들은 차량 구매 시 수동적 안전 시스템과 충돌 보호 기능을 점점 더 중요시하는 경향이 있으며, 자동차 제조업체들은 중급 모델에도 고성능 멀티 에어백 시스템을 통합하고 있습니다. 예측 센서와 지능형 충돌 대응 메커니즘을 포함한 스마트 커넥티드카 시스템의 통합을 위해서는 신속하고 효율적으로 작동하는 인플레이터가 필요합니다. 탑승자 보호와 ADAS(첨단 운전자 보조 시스템)의 연계로 인해 차세대 인플레이터에 대한 수요가 증가하고 있으며, 이는 시장에서 공급업체에게 큰 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 56억 달러 |

| 예측 금액 | 87억 달러 |

| CAGR | 4.8% |

승용차 부문은 2025년 67%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 4.7%의 성장률을 기록할 것으로 전망됩니다. 엔트리 모델을 포함한 모든 승용차에 에어백 장착을 의무화하는 규제가 성장을 견인하는 주요 요인입니다. 전면, 측면, 커튼 에어백 등 다중 에어백 시스템을 의무화하는 법은 차량 당 인플레이터 수를 직접적으로 증가시킵니다. 각 지역별로 규제 적용 시한이 다가옴에 따라 제조사들은 에어백 시스템 장착에 박차를 가하고 있으며, 공급업체 입장에서는 규제 주도로 인한 꾸준한 성장이 예상됩니다.

2025년 기준 OEM(자동차 제조업체) 부문은 71%의 점유율을 차지하며, 2026년부터 2035년까지 CAGR 4.5%로 성장할 것으로 예상됩니다. OEM이 진화하는 안전 규정을 엄격하게 준수하는 것은 리콜, 처벌, 평판 훼손을 피하는 데 효과적입니다. 고품질의 혁신적인 인플레이터를 통해 OEM은 여러 차량 플랫폼에서 충돌 보호 기준의 일관성을 유지할 수 있습니다. 이러한 규정 준수와 안전에 대한 집중은 인플레이터 공급업체와의 장기 계약을 촉진하여 안정적인 수요와 지속적인 기술 혁신을 가져왔습니다.

중국 자동차 에어백 인플레이터 시장은 2025년 8억 4,530만 달러 규모로 40%의 점유율을 차지할 것으로 예상됩니다. 세계 최대 자동차 생산기지인 중국에서는 연간 수백만 대의 승용차가 생산되고 있으며, 모든 차종 부문에서 인플레이터에 대한 높은 수요가 발생하고 있습니다. 현지 및 합작 OEM 제조업체의 지속적인 생산능력 확대는 인플레이터 소비의 견조한 추세를 뒷받침하고 공급업체의 지속적인 성장을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 차량별, 2022-2035

제6장 시장 추정 및 예측 : 인플레이터별, 2022-2035

제7장 시장 추정 및 예측 : 에어백별, 2022-2035

제8장 시장 추정 및 예측 : 추진력별, 2022-2035

제9장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제10장 시장 추정 및 예측 : 도입 형태별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM 26.03.05The Global Automotive Airbag Inflator Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 8.7 billion by 2035.

The rising production of motor vehicles worldwide is a significant driver of this growth. As manufacturers ramp up output to meet surging demand, each new vehicle requires multiple airbag inflators, which elevates installation rates and strengthens long-term supply agreements. This higher production volume also improves economies of scale and accelerates the adoption of advanced inflator technologies across different vehicle segments. Consumers are increasingly prioritizing passive safety systems and crash protection when purchasing vehicles, leading automakers to integrate high-performance multi-airbag systems even in mid-tier models. The integration of smart, connected vehicle systems, including predictive sensors and intelligent crash-response mechanisms, requires inflators that deploy quickly and efficiently. By aligning occupant protection with advanced driver-assistance systems (ADAS), next-generation inflators are seeing higher demand, creating substantial opportunities for suppliers in the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 4.8% |

The passenger vehicles segment accounted for 67% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Regulatory mandates requiring airbags in all passenger vehicles, including entry-level models, are a key factor driving growth. Laws enforcing multiple airbag systems, frontal, side, and curtain, directly increase the number of inflators per vehicle. As compliance deadlines approach across various regions, manufacturers are accelerating the installation of airbag systems, ensuring steady, regulation-driven growth for suppliers.

The original equipment manufacturers (OEMs) segment held a 71% share in 2025 and is projected to grow at a CAGR of 4.5% from 2026 to 2035. OEMs' strict adherence to evolving safety regulations helps them avoid recalls, penalties, and reputational damage. High-quality, innovative inflators allow OEMs to maintain consistency in crash protection standards across multiple vehicle platforms. This focus on compliance and safety drives long-term contracts with inflator suppliers, providing stable demand and continuous technological advancements.

China Automotive Airbag Inflator Market held 40% share, generating USD 845.3 million in 2025. Being the world's largest automotive manufacturing hub, China produces millions of passenger vehicles annually, resulting in high demand for inflators across all vehicle segments. Ongoing capacity expansions by local and joint-venture OEMs support strong inflator consumption and encourage sustained growth for suppliers.

Key players operating in the Global Automotive Airbag Inflator Market include ARC Automotive, Autoliv, Joyson Safety Systems, Toyoda Gosei, Daicel, Ashimori Industry, Hyundai Mobis, ITW Automotive, Nippon Kayaku, and ZF. Companies in the automotive airbag inflator market are focusing on several strategies to strengthen their market presence and competitive position. They are investing heavily in research and development to create next-generation, high-performance inflators that meet evolving safety standards. Long-term supply agreements with OEMs are being secured to ensure stable demand and foster collaboration for technological innovation. Strategic mergers, acquisitions, and partnerships are also employed to expand global footprints and leverage complementary capabilities. Additionally, manufacturers are diversifying their product portfolios to cater to passenger vehicles, commercial vehicles, and connected vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Inflator

- 2.2.4 Airbag

- 2.2.5 Propulsion

- 2.2.6 Sales channel

- 2.2.7 Deployment mode

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Stringent safety regulations

- 3.2.1.3 Growth of multi-airbag architectures

- 3.2.1.4 Inflator technology advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Recall and liability risks

- 3.2.2.2 Raw material cost volatility

- 3.2.3 Market opportunities

- 3.2.3.1 EV & autonomous vehicle growth

- 3.2.3.2 Emerging market safety adoption

- 3.2.3.3 Aftermarket & recall replacements

- 3.2.3.4 Sustainable inflator materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US National Highway Traffic Safety Administration (NHTSA) Regulations

- 3.4.1.2 Environmental Protection Agency (EPA) Emission Standards

- 3.4.1.3 California Air Resources Board (CARB) Standards

- 3.4.2 Europe

- 3.4.2.1 European Union General Safety Regulation (EU GSR)

- 3.4.2.2 EU Directive on End-of-Life Vehicles (ELV)

- 3.4.2.3 European Commission Safety Standards for Passenger Vehicles

- 3.4.2.4 European Union Type Approval Process

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for Vehicle Safety

- 3.4.3.2 India Bureau of Indian Standards (BIS) Airbag Regulations

- 3.4.3.3 Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT) Regulations

- 3.4.3.4 ASEAN Road Safety Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Department (DENATRAN) Standards

- 3.4.4.2 Argentina National Road Safety Agency (ANSV) Regulations

- 3.4.4.3 Mexico Secretariat of Communications and Transport (SCT) Regulations

- 3.4.4.4 MERCOSUR Harmonization of Vehicle Safety Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Vehicle Safety Law

- 3.4.5.2 Saudi Arabian Standards Organization (SASO) Vehicle Safety Regulations

- 3.4.5.3 South African Bureau of Standards (SABS) Automotive Regulations

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.12.1 Airbag Inflator Component Costs

- 3.12.2 R&D and Innovation Costs

- 3.12.3 Manufacturing and Assembly Costs

- 3.12.4 Logistics and Distribution Costs

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.2.4 Others

- 5.3 Commercial vehicle

- 5.3.1 Light commercial vehicle (LCV)

- 5.3.2 Medium commercial vehicle (MCV)

- 5.3.3 Heavy commercial vehicle (HCV)

Chapter 6 Market Estimates & Forecast, By Inflator, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Pyrotechnic inflators

- 6.3 Stored gas inflators

- 6.4 Hybrid inflators

Chapter 7 Market Estimates & Forecast, By Airbag, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Frontal

- 7.3 Side

- 7.4 Curtain

- 7.5 Knee

- 7.6 Pedestrian

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 BEV

- 8.5 PHEV

- 8.6 HEV

- 8.7 FCEV

- 8.8 CNG/LPG

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Single-stage

- 10.3 Multi-stage

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Autoliv

- 12.1.2 Bosch

- 12.1.3 Continental

- 12.1.4 Daicel

- 12.1.5 Delphi

- 12.1.6 Denso

- 12.1.7 Hyundai Mobis

- 12.1.8 Joyson Safety Systems

- 12.1.9 ZF

- 12.2 Regional Players

- 12.2.1 ARC Automotive

- 12.2.2 Ashimori Industry

- 12.2.3 ITW Automotive

- 12.2.4 Kolon Industries

- 12.2.5 Nippon Kayaku

- 12.2.6 Seiren

- 12.2.7 Toyoda Gosei

- 12.3 Emerging Players

- 12.3.1 Jinheng Automotive Safety Technology

- 12.3.2 Nihon Plast

- 12.3.3 Swicofil

- 12.3.4 Tenaris