|

시장보고서

상품코드

1936662

근위 경골 절골술용 플레이트 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)High Tibial Osteotomy Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

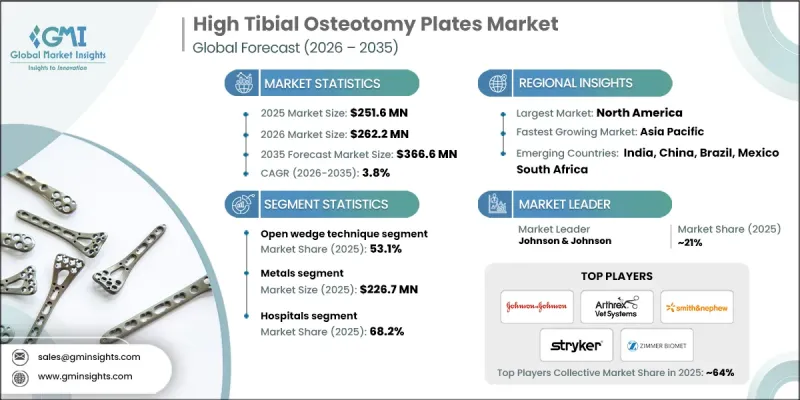

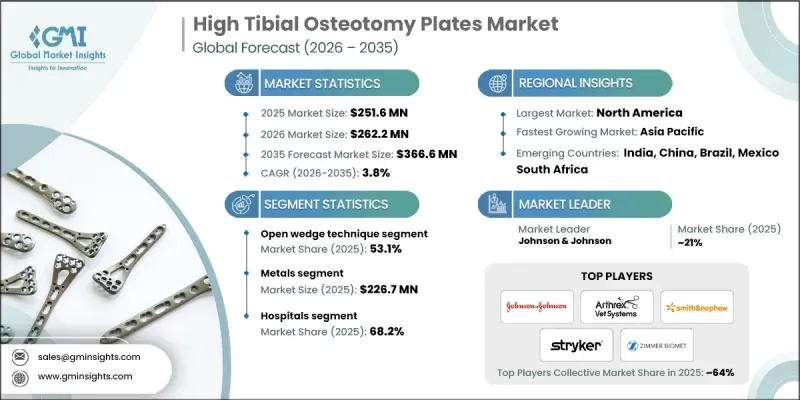

세계의 근위 경골 절골술용 플레이트 시장은 2025년에 2억 5,160만 달러로 평가되었으며, 2035년까지 CAGR 3.8%로 성장하여 3억 6,660만 달러에 달할 것으로 예측됩니다.

이러한 꾸준한 성장은 슬관절 전치환술보다 관절 보존 수술이 선호되는 추세와 더불어, 플레이트 디자인, 고정 기술, 수술 기법의 지속적인 혁신에 힘입은 바 큽니다. 또한, 젊은 연령층과 활동적인 계층의 슬관절염 발병률 증가로 인해 환자와 외과의사는 관절 기능을 유지하고 슬관절 전치환술을 지연시키거나 피할 수 있는 대안을 찾고 있습니다. HTO 플레이트는 교정 절골술 후 경골을 안정화시키기 위해 설계된 전문 정형외과용 장치로, 회복 기간 동안 최적의 뼈 정렬과 하중 분산을 보장합니다. 해부학적인 형태 개선, 얇은 디자인, 잠금식 스크류 시스템 채택으로 안정성이 향상되고, 치유 합병증이 감소하며, 외과 의사의 확신이 높아졌습니다. 기술의 발전과 함께 현대의 HTO 플레이트는 비유합, 임플란트 실패, 수술 후 정렬 불량 등의 위험을 최소화하면서 회복을 촉진하고 장기적인 관절 기능의 좋은 결과를 가져오는 능력으로 인해 더 널리 받아들여지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 3억 6,660만 달러 |

| 예측 금액 | 3억 6,660만 달러 |

| CAGR | 3.8% |

2025년 오픈웨지법 부문은 53.1%의 점유율을 차지했습니다. 이는 다른 수술법에 비해 수술의 유연성, 사지 정렬 교정의 정확성, 신경혈관 손상 위험 감소 등의 장점이 있기 때문입니다. 이 방법을 통해 경골의 각도를 정확하게 조정할 수 있기 때문에 외과의사는 원하는 기계적 정렬을 달성하고 과교정이나 과교정을 피할 수 있습니다. 이러한 정밀성으로 인해 수술 후 치료 성적이 향상되고 기능 회복이 촉진되어 현대 정형외과 진료에서 폐쇄형 웨지법보다 선호되는 기술로 자리 잡고 있습니다.

금속 부문은 2025년 2억 2,670만 달러의 시장 규모를 기록했으며, 2026년부터 2035년까지 연평균 4%의 성장률을 기록할 것으로 예상됩니다. 금속 HTO 플레이트는 주로 티타늄 또는 스테인리스 스틸로 제조되어 우수한 강도와 강성을 제공합니다. 이를 통해 초기 하중 단계에서도 안정적인 고정이 보장됩니다. 이 플레이트는 최신 잠금식 스크류 시스템을 지원하며, 각도의 안정성과 장기적인 교정 효과를 제공합니다. 이를 통해 안전한 조기 이동과 회복을 촉진할 수 있습니다. 외과 의사는 기계적 신뢰성, 내구성 및 첨단 수술 기술과의 호환성 때문에 활동적인 환자를 위해 금속판을 선호하는 경우가 많습니다.

북미 근위 경골 절골술용 플레이트 시장은 2025년 45%의 점유율을 차지했습니다. 이 지역에서는 특히 중장년층의 슬관절염 유병률 증가와 함께 내반변형 및 내측 구획 퇴행의 발생률 증가로 인해 관절 보존 수술에 대한 수요가 증가하고 있습니다. 병원과 정형외과 전문의들은 조기 인공 슬관절 전치환술의 대안으로 해부학적 형태와 잠금식 스크류 디자인을 갖춘 첨단 HTO 플레이트를 점차적으로 채택하고 있습니다. 첨단 의료 인프라와 혁신적인 정형외과 솔루션에 대한 높은 인지도는 이 지역의 시장 확대를 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술별, 2022-2035

제6장 시장 추정 및 예측 : 재료별, 2022-2035

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.03.05The Global High Tibial Osteotomy Plates Market was valued at USD 251.6 million in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 366.6 million by 2035.

The steady growth is driven by the increasing preference for joint-preserving surgeries over total knee replacements, alongside ongoing innovations in plate design, fixation technologies, and surgical techniques. Rising incidences of knee osteoarthritis in younger and more active populations are also fueling demand, as patients and surgeons seek alternatives that maintain joint functionality and delay or avoid full knee replacement. HTO plates are specialized orthopedic devices designed to stabilize the tibia following corrective osteotomy procedures, ensuring optimal bone alignment and load distribution during recovery. Improved anatomical contours, low-profile designs, and locking screw systems have enhanced stability, reduced healing complications, and increased surgeon confidence. As technology continues to advance, modern HTO plates are gaining wider acceptance due to their ability to minimize risks like non-union, implant failure, and postoperative misalignment, while promoting faster recovery and better long-term joint outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $366.6 Million |

| Forecast Value | $366.6 Million |

| CAGR | 3.8% |

In 2025, the open wedge technique segment held a 53.1% share, owing to its surgical flexibility, precision in limb alignment correction, and reduced risk of neurovascular injuries compared to alternative approaches. This method allows exact angular adjustment of the tibia, enabling surgeons to achieve the desired mechanical alignment and avoid over- or under-correction. Such precision improves postoperative outcomes and accelerates functional recovery, making it the preferred technique over closed wedge methods in modern orthopedic practices.

The metals segment generated USD 226.7 million in 2025 and is expected to grow at a CAGR of 4% during 2026-2035. Metal HTO plates, typically made from titanium or stainless steel, provide superior strength and rigidity, ensuring stable fixation even during early weight-bearing phases. These plates support modern locking screw systems, delivering angular stability and long-term correction, which enables safe early mobilization and enhanced recovery. Surgeons often favor metal plates for active patients due to their mechanical reliability, durability, and compatibility with advanced surgical techniques.

North America High Tibial Osteotomy Plates Market accounted for 45% share in 2025. The region's growing prevalence of knee osteoarthritis, particularly among middle-aged and elderly populations, combined with increasing rates of varus deformities and medial compartment degeneration, has amplified the demand for joint-preserving procedures. Hospitals and orthopedic specialists are progressively adopting advanced HTO plates with anatomical contouring and locking screw designs to provide alternatives to early total knee replacement. The presence of sophisticated healthcare infrastructure and high awareness of innovative orthopedic solutions further drives market expansion in this region.

Key companies in the Global High Tibial Osteotomy Plates Market include Arthrex, Smith+Nephew, Medacta International, Stryker, ZIMMER BIOMET, Amplitude Surgical, Johnson & Johnson, B. BRAUN, Intercus, Newclip Technics, Hankil Tech Medical, Science and Bio Materials (SBM), Nebula Surgical, Auxein, and Miraclus. Companies in the High Tibial Osteotomy Plates Market strengthen their position by focusing on research and development to enhance plate design, incorporating advanced materials, anatomical contouring, and locking screw systems. Strategic collaborations with orthopedic hospitals and surgical centers enable demonstration of efficacy and foster surgeon trust. Manufacturers also invest in training programs and workshops to educate surgeons on modern osteotomy techniques and device usage.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technique trends

- 2.2.3 Material trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of knee osteoarthritis and musculoskeletal disorders

- 3.2.1.2 Increasing incidence of sports-related injuries and knee deformities

- 3.2.1.3 Growing demand for joint-preserving surgical procedures

- 3.2.1.4 Technological advancements in implant design and materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of HTO plates and procedures

- 3.2.2.2 Potential surgical risks and complications

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of minimally invasive surgical techniques

- 3.2.3.2 Growth in personalized and patient-specific implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Value chain analysis

- 3.8 Start-up scenarios

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technique, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Open wedge technique

- 5.3 Closed wedge technique

- 5.4 Progressive callus distraction

- 5.5 Dome technique

- 5.6 Chevron osteotomy

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Metals

- 6.2.1 Titanium

- 6.2.2 Stainless steel

- 6.3 Polymers

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amplitude Surgical

- 9.2 Arthrex

- 9.3 Auxein

- 9.4 B. BRAUN

- 9.5 Hankil Tech Medical

- 9.6 Intercus

- 9.7 Johnson & Johnson

- 9.8 Medacta International

- 9.9 Miraclus

- 9.10 Nebula Surgical

- 9.11 Newclip Technics

- 9.12 Science and Bio Materials (SBM)

- 9.13 Smith+Nephew

- 9.14 Stryker

- 9.15 ZIMMER BIOMET