|

시장보고서

상품코드

1959290

자동차 구역 아키텍처 및 도메인 컨트롤러 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Zonal Architecture and Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

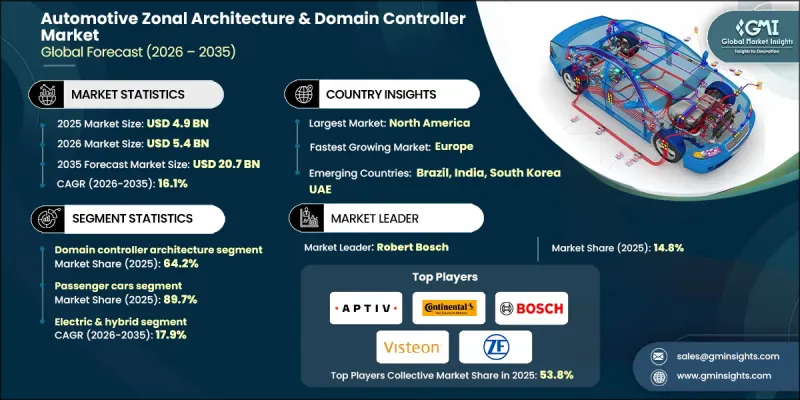

세계의 자동차 구역 아키텍처 및 도메인 컨트롤러 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.1%로 성장하여 207억 달러에 이를 것으로 예측됩니다.

시장 성장은 차량 전장 설계 및 통합 방식의 근본적인 변화에 의해 주도되고 있습니다. 자동차 제조업체들은 고도로 분절된 전자 시스템에서 보다 중앙집중화된 소프트웨어 중심 아키텍처로 전환하고 있습니다. 기존의 차량 설계는 광범위한 배선 네트워크를 통해 연결된 수많은 독립적인 전자 제어 장치에 의존하여 차량 중량, 생산 복잡성 및 제조 비용을 증가시켰습니다. 존 아키텍처는 이러한 접근 방식을 재구성하여 물리적 차량 구역을 기반으로 전자 장치를 구성하고 고속 데이터 네트워크를 통해 연결하여 배선 요구 사항을 크게 줄입니다. 이 간소화된 구조는 에너지 효율을 높이고, 조립 공정을 간소화하며, 기능을 디지털로 업데이트할 수 있는 소프트웨어 정의 차량으로 전환할 수 있도록 돕습니다. 고급 통신 프로토콜은 센서 및 차량 내 시스템의 데이터 처리 속도를 높이고, 개선된 전력 분배는 특히 전동화 플랫폼에서 차량 성능 최적화에 기여합니다. 이러한 장점들이 결합되어 전 세계 자동차 산업에서 채택이 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 49억 달러 |

| 예측 금액 | 207억 달러 |

| CAGR | 16.1% |

도메인 컨트롤러 아키텍처 부문은 64.2%의 점유율을 차지하며 2025년 32억 달러를 창출할 것으로 예측됩니다. 자동차 제조업체들은 여러 차량 기능을 소수의 고성능 유닛에 통합할 수 있기 때문에 중앙 집중식 컴퓨팅 시스템을 선호합니다. 운전 보조, 인포테인먼트, 차체 전자장치 등의 영역을 통합 컨트롤러에 통합함으로써 제조업체는 시스템의 복잡성과 배선 밀도를 줄일 수 있습니다. 이러한 접근 방식은 확장성을 향상시키고, 기존 차량용 전자장치 설계에 비해 고급 소프트웨어 기능을 쉽게 도입할 수 있도록 합니다.

승용차 부문은 2025년 89.7%의 점유율을 차지할 것으로 예상되며, 2035년까지 181억 달러에 달할 것으로 전망됩니다. 첨단 디지털 기능과 커넥티드 기술의 집중화가 진행됨에 따라 이 부문의 채택률이 높아지고 있습니다. 높은 생산량과 소비자의 혁신에 대한 수요로 인해 승용차는 복잡한 차량 기능을 효율적으로 관리할 수 있는 구역별 및 중앙 집중식 전자 시스템을 도입할 수 있는 주요 플랫폼이 되고 있습니다.

미국 자동차 영역별 아키텍처 도메인 컨트롤러 시장은 2025년 14억 달러에 달할 것으로 예측됩니다. 소프트웨어 정의 차량 플랫폼에 대한 강력한 추진력이 지역 시장을 형성하고 있으며, 제조업체들은 원격 소프트웨어 업데이트와 신속한 기능 배포를 지원하는 중앙 집중식 전자 아키텍처에 중점을 두고 있습니다. 이러한 전환으로 인해 전기차 및 차세대 차량 전반에 걸쳐 도메인 컨트롤러 솔루션에 대한 수요가 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 아키텍처별, 2022-2035

제6장 시장 추산 및 예측 : 차량별, 2022-2035

제7장 시장 추산 및 예측 : 추진력별, 2022-2035

제8장 시장 추산 및 예측 : 자율 레벨별, 2022-2035

제9장 시장 추산 및 예측 : 통신 프로토콜별, 2022-2035

제10장 시장 추산 및 예측 : 전압별, 2022-2035

제11장 시장 추산 및 예측 : 용도별, 2022-2035

제12장 시장 추산 및 예측 : 지역별, 2022-2035

제13장 기업 개요

LSH 26.03.18The Global Automotive Zonal Architecture & Domain Controller Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 16.1% to reach USD 20.7 billion by 2035.

Market growth is driven by a fundamental shift in how vehicle electronics are designed and integrated. Automakers are moving away from highly fragmented electronic systems toward more centralized and software-focused architectures. Traditional vehicle designs relied on many independent electronic control units connected through extensive wiring networks, which increased vehicle weight, production complexity, and manufacturing costs. Zonal architecture restructures this approach by organizing electronics based on physical vehicle zones and connecting them through high-speed data networks, significantly reducing wiring requirements. This streamlined structure improves energy efficiency, simplifies assembly processes, and supports the transition toward software-defined vehicles where functionality can be updated digitally. Advanced communication protocols enable faster data handling from sensors and onboard systems, while improved power distribution helps optimize vehicle performance, particularly in electrified platforms. Together, these benefits are accelerating adoption across the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 16.1% |

The domain controller architecture segment held 64.2% share, generating USD 3.2 billion in 2025. Automakers are favoring centralized computing systems because they consolidate multiple vehicle functions into fewer, high-performance units. By integrating areas such as driver assistance, infotainment, and body electronics into unified controllers, manufacturers reduce system complexity and wiring density. This approach also enhances scalability and makes it easier to deploy advanced software capabilities compared to legacy vehicle electronics designs.

The passenger cars segment accounted for 89.7% share in 2025 and is expected to reach USD 18.1 billion by 2035. Adoption is higher in this segment due to the growing concentration of advanced digital features and connected technologies. High production volumes and consumer demand for innovation make passenger vehicles the primary platform for introducing zonal and centralized electronic systems, enabling more efficient management of complex vehicle functions.

U.S. Automotive Zonal Architecture & Domain Controller Market reached USD 1.4 billion in 2025. The regional market is being shaped by strong momentum toward software-defined vehicle platforms, with manufacturers emphasizing centralized electronic architectures to support remote software updates and faster feature deployment. This shift is reinforcing demand for domain controller solutions across electric and next-generation vehicles.

Key companies operating in the Global Automotive Zonal Architecture & Domain Controller Market include Robert Bosch, Aptiv, Continental, ZF, Visteon, Valeo, NXP, Infineon, Qualcomm, and Onsemi. Companies in the automotive zonal architecture and domain controller market are strengthening their market position through heavy investment in advanced semiconductor development and centralized computing platforms. Strategic partnerships with automakers and software providers are helping accelerate the integration of scalable electronic architectures. Many players are expanding research efforts focused on high-speed networking, power management, and cybersecurity to support software-defined vehicles. Portfolio diversification, regional expansion, and early involvement in next-generation vehicle programs are also key priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Architecture

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Autonomy level

- 2.2.6 Communication Protocol

- 2.2.7 Voltage

- 2.2.8 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification

- 3.2.1.2 Increasing software-defined vehicle adoption

- 3.2.1.3 Growing demand for advanced driver assistance systems (ADAS)

- 3.2.1.4 Expansion of over-the-air (OTA) update capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and functional safety challenges

- 3.2.2.2 High development and integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric and hybrid vehicle platforms

- 3.2.3.2 Advancements in automotive ethernet technologies

- 3.2.3.3 Expansion of Software-Centric Automotive Ecosystems

- 3.2.3.4 Emerging opportunities in autonomous commercial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations

- 3.4.2.3 Vehicle Certification Agency

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 Japan Automobile Standards Internationalization Center

- 3.4.3.3 Automotive Industry Standards (AIS)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Association of Automotive Vehicle Manufacturers (ANFAVEA)

- 3.4.4.2 INMETRO

- 3.4.4.3 National Road Safety Commission

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standards Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Architecture & system design

- 3.11.1 Domain controller architecture fundamentals

- 3.11.2 Zonal architecture design principles

- 3.11.3 Hybrid architecture implementation strategies

- 3.11.4 Centralized vs decentralized computing models

- 3.11.5 High-performance computing (HPC) integration

- 3.12 Vehicle server architecture

- 3.12.1 Zonal gateway design and placement

- 3.12.2 Software Defined Vehicle (SDV) Strategy

- 3.12.3 Service-oriented architecture (SOA) implementation

- 3.12.4 Middleware platforms and standards

- 3.13 Zonal architecture in autonomous vehicles

- 3.13.1 ADAS domain integration in zonal systems

- 3.13.2 Sensor fusion architecture for autonomy

- 3.13.3 Real-time data processing requirements

- 3.13.4 Redundancy and fail-operational systems

- 3.13.5 Centralized perception and decision making

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Architecture, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Domain controller architecture

- 5.3 Zonal architecture

- 5.4 Hybrid architecture

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Internal Combustion Engine (ICE) vehicles

- 7.3 Electric & hybrid vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Fuel Cell Electric Vehicles (FCEV)

Chapter 8 Market Estimates & Forecast, By Autonomy level, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Level 1

- 8.3 Level 2

- 8.4 Level 3

- 8.5 Level 4 & Level 5

Chapter 9 Market Estimates & Forecast, By Communication protocol, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 CAN / LIN-based system

- 9.3 Ethernet-based system

Chapter 10 Market Estimates & Forecast, By Voltage, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 12V system

- 10.3 48V system

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 ADAS domain

- 11.3 Powertrain / EV power domain

- 11.4 Body & comfort domain

- 11.5 Cockpit / infotainment domain

- 11.6 Safety domain

- 11.7 Chassis & motion domain

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Robert Bosch

- 13.1.2 Continental

- 13.1.3 Aptiv

- 13.1.4 NXP Semiconductors

- 13.1.5 Infineon

- 13.1.6 Valeo

- 13.1.7 STMicroelectronics

- 13.1.8 Texas Instruments

- 13.1.9 Visteon

- 13.1.10 Harman

- 13.1.11 Panasonic

- 13.1.12 NVIDIA

- 13.1.13 Qualcomm

- 13.1.14 onsemi

- 13.2 Regional players

- 13.2.1 HiRain

- 13.2.2 SemiDrive

- 13.2.3 Sonatus

- 13.2.4 ETAS

- 13.2.5 Elektrobit

- 13.2.6 Lear

- 13.2.7 Magna

- 13.2.8 Marelli

- 13.2.9 DENSO

- 13.3 Emerging players

- 13.3.1 TTTech

- 13.3.2 GuardKnox

- 13.3.3 Ambarella

- 13.3.4 Aurora Labs

- 13.3.5 Rivian

- 13.3.6 AUMOVIO

- 13.3.7 Molex