|

시장보고서

상품코드

1959293

식물성 텍스처링제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Plant Based Texturizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

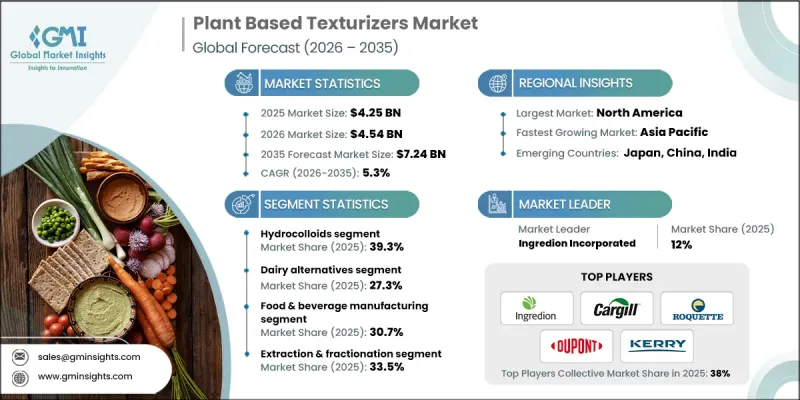

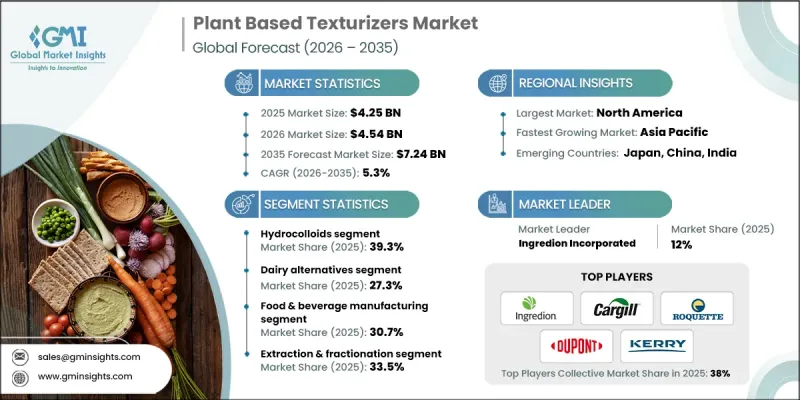

세계의 식물성 텍스처링제 시장은 2025년에 42억 5,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.3%로 성장하여 72억 4,000만 달러에 이를 것으로 예측됩니다.

이 시장은 식감, 안정성 및 균일성이 중요한 성능 특성인 식품, 영양 보충제, 퍼스널케어 및 산업 응용 분야에서 현대 제품 설계에서 매우 중요한 역할을 담당하고 있습니다. 식물 유래 원료는 제한적이고 전문적인 용도를 넘어 이제는 주류 제품 개발에 없어서는 안 될 필수적인 존재가 되었습니다. 이러한 변화는 자연에서 유래하고 투명하며 책임감 있게 조달된 원료에 대한 소비자의 강력한 수요를 반영하고 있습니다. 가공 방법, 원료 정제, 생물학적 최적화의 지속적인 발전으로 식물 유래 텍스처라이저는 더 높은 기능성, 개선된 내열성, 우수한 분산성, 복잡한 배합물과의 높은 호환성을 실현할 수 있게 되었습니다. 이러한 개선을 통해 제조업체는 규제 요건과 지속가능성 목표를 충족시키면서 기존 합성 소재를 대체할 수 있습니다. 보다 친환경적인 공급망과 석유화학 원료에 대한 의존도를 낮추기 위한 기업의 노력은 시장 성장을 더욱 강화하고, 식물 유래 텍스처라이저를 미래지향적인 배합 전략의 기본 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 42억 5,000만 달러 |

| 예측 금액 | 72억 4,000만 달러 |

| CAGR | 5.3% |

하이드로콜로이드 부문은 2025년 39.3%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 4.7%의 성장률을 보일 것으로 전망됩니다. 이러한 원료는 점도 관리, 보습 및 다양한 최종 사용 산업에서 제품의 종합적인 안정성을 지원하는 중요한 구조적 지원을 제공합니다. 이러한 적응성을 통해 배합자는 식감과 입맛을 미세하게 조정할 수 있으며, 기존 제품 라인과 신뢰할 수 있는 천연 유래 성능 특성을 필요로 하는 새로운 식물 유래 혁신 제품 모두에 필수적인 요소로 작용하고 있습니다.

대체 유제품 응용 분야는 2025년 27.3%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 6.9%의 성장률을 보일 것으로 전망됩니다. 식물성 텍스처라이저는 비유제품 배합에 필요한 이상적인 크리미함, 부드러운 일관성, 안정된 유화를 실현하는 데 필수적인 요소입니다. 이러한 원료는 제조, 보관, 유통의 전 과정에서 품질의 일관성을 유지하여 제품의 관능적 매력과 구조적 무결성을 유지하는 동시에 클린 라벨에 대한 기대에 부응합니다.

북미 식물 유래 텍스처라이저 시장은 2025년 37%의 점유율을 차지했습니다. 이 지역은 첨단 가공 기술, 혁신을 주도하는 제조업체, 그리고 지속 가능한 식물 유래 트렌드를 적극적으로 지지하는 탄탄한 소비자층의 혜택을 누리고 있습니다. 탄탄한 규제 체계와 R&D에 대한 적극적인 투자로 이 시장에서 북미의 선도적 입지를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 용도별, 2022-2035

제7장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제8장 시장 추산 및 예측 : 기술별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.18The Global Plant Based Texturizers Market was valued at USD 4.25 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 7.24 billion by 2035.

The market plays a critical role in modern formulation across food, nutraceutical, personal care, and industrial applications, where texture, stability, and consistency are essential performance attributes. Ingredients derived from plant sources have moved beyond limited or specialized use and are now integral to mainstream product development. This shift reflects strong consumer demand for natural, transparent, and responsibly sourced ingredients. Ongoing advancements in processing methods, ingredient refinement, and biological optimization are enabling plant-based texturizers to deliver higher functionality, improved thermal resistance, better dispersibility, and greater compatibility with complex formulations. These improvements enable manufacturers to replace conventional synthetic materials while meeting regulatory requirements and sustainability objectives. Corporate commitments to greener supply chains and reduced dependence on petrochemical inputs are further reinforcing market growth, positioning plant-based texturizers as a foundational component of future-oriented formulation strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.25 Billion |

| Forecast Value | $7.24 Billion |

| CAGR | 5.3% |

The hydrocolloids segment held a share of 39.3% in 2025 and is expected to grow at a CAGR of 4.7% through 2035. These ingredients provide critical structural support by managing viscosity, moisture retention, and overall product stability across multiple end-use industries. Their adaptability allows formulators to fine-tune texture and mouthfeel, making them indispensable for both established product lines and emerging plant-forward innovations that require reliable, naturally sourced performance characteristics.

The dairy alternatives application segment accounted for 27.3% share in 2025 and is forecast to grow at a CAGR of 6.9% from 2026 to 2035. Plant-based texturizers are essential in delivering the desired creaminess, smooth consistency, and stable emulsification required in non-dairy formulations. These ingredients support consistent quality throughout manufacturing, storage, and distribution, ensuring products maintain their sensory appeal and structural integrity while aligning with clean-label expectations.

North America Plant Based Texturizers Market held a 37% share in 2025. The region benefits from advanced processing capabilities, innovation-driven manufacturers, and a well-established consumer base that actively supports sustainable and plant-focused formulation trends. Robust regulatory frameworks and strong investment in research and development further reinforce North America's leadership position in this market.

Key companies operating in the Global Plant Based Texturizers Market include Cargill, Incorporated, Ingredion Incorporated, Kerry Group plc, Roquette Freres, CP Kelco, DuPont Nutrition & Biosciences, Ashland Global Holdings Inc., ICL Food Specialties (ICL Group), Palsgaard A/S, TIC Gums, Fiberstar Inc, PURIS Holdings LLC, Marine Hydrocolloids, Burcon NutraScience Corporation, and Socius Ingredients. Companies in the plant based texturizers market are strengthening their competitive position by focusing on innovation, sustainability, and application-specific solutions. Many players are investing heavily in research to enhance ingredient performance, improve functionality, and expand use across diverse formulation systems. Strategic partnerships with food and personal care manufacturers are being used to accelerate product adoption and co-develop tailored solutions. Firms are also expanding production capacity and sourcing capabilities to ensure supply chain reliability and traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End-User

- 2.2.5 Technology Method

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based foods

- 3.2.1.2 Clean label & natural ingredient trends

- 3.2.1.3 Regulatory support for plant-based alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs vs conventional texturizers

- 3.2.2.2 Sensory & flavor challenges (off-notes, bitterness)

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging protein sources (algae, fungi, novel legumes)

- 3.2.3.2 Functional blends & customized texturizer systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hydrocolloids

- 5.3 Plant proteins (texturized)

- 5.4 Starches

- 5.5 Cellulose derivatives

- 5.6 Other plant-based texturizers

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy Alternatives

- 6.3 Bakery & Confectionery

- 6.4 Meat Alternatives & Analogs

- 6.5 Beverages

- 6.6 Sauces, Dressings & Condiments

- 6.7 Snacks & Convenience Foods

- 6.8 Frozen & Processed Foods

Chapter 7 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage manufacturing

- 7.3 Grain & oilseed processing

- 7.4 Dairy alternative manufacturers

- 7.5 Bakery & confectionery

- 7.6 Foodservice & institutional

- 7.7 Retail & consumer packaged goods

Chapter 8 Market Estimates and Forecast, By Technology Method, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Extrusion technology

- 8.3 Fermentation-based production

- 8.4 Extraction & fractionation

- 8.5 Novel texturization technologies

- 8.6 Chemical/physical modification

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Ingredion Incorporated

- 10.2 Cargill, Incorporated

- 10.3 Roquette Freres

- 10.4 ICL Food Specialties (ICL Group)

- 10.5 DuPont Nutrition & Biosciences

- 10.6 Kerry Group plc

- 10.7 Ashland Global Holdings Inc.

- 10.8 PURIS Holdings LLC

- 10.9 Marine Hydrocolloids

- 10.10 TIC Gums

- 10.11 Palsgaard A/S

- 10.12 Fiberstar Inc

- 10.13 CP Kelco

- 10.14 Socius Ingredients

- 10.15 Burcon NutraScience Corporation