|

시장보고서

상품코드

1959341

커넥티드카 보안 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Connected Car Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

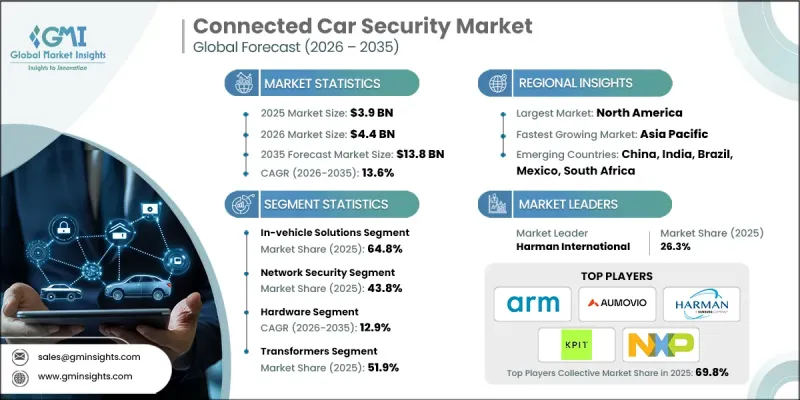

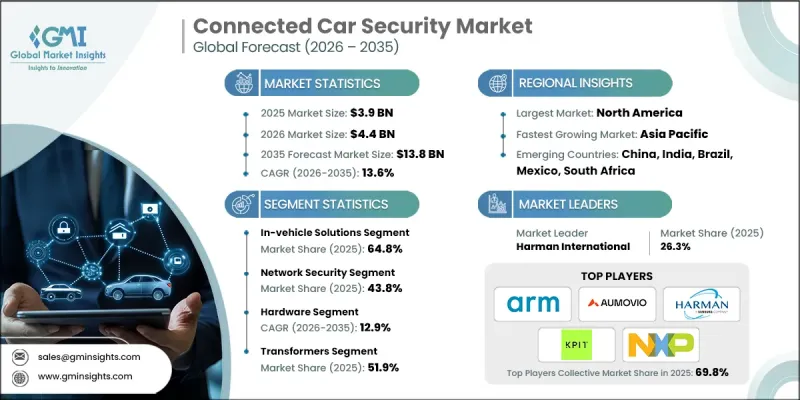

세계의 커넥티드카 보안 시장은 2025년에 39억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 13.6%로 성장하여 138억 달러에 이를 것으로 예측됩니다.

커넥티드카 기술의 급속한 확산에 따라 차량 생태계, 차량 관리 플랫폼, 클라우드 커넥티드 서비스 전반에 걸쳐 강력한 사이버 보안의 필요성이 대두되고 있습니다. 자동차 제조업체와 기업들은 운영 리스크를 줄이고 수동 모니터링에 대한 의존도를 낮추기 위해 차량 전자 아키텍처, 백엔드 서버, 클라우드 플랫폼에 보안 기능을 직접 통합하는 사례가 증가하고 있습니다. 엣지 AI 프로세서, V2X 통신, 차량 소프트웨어 플랫폼의 지속적인 발전으로 보안 솔루션의 성능, 확장성, 응답성이 향상되고 있습니다. 대규모 차량을 보호하기 위해 실시간 침입 감지, 안전한 데이터 교환, 무선 업데이트(OTA)가 표준화되고 있습니다. 자동차 제조업체, 사이버 보안 업체, 클라우드 사업자 간의 전략적 제휴, 합병, 협업으로 차량 라이프사이클, 차량 운영, 모빌리티 서비스에 대한 보안 통합이 가속화되고 있습니다. 커넥티드카 보안은 기존의 모니터링에서 소프트웨어 정의 차량과 모빌리티 플랫폼을 보호하는 AI 기반의 능동적 위협 분석 시스템으로 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 39억 달러 |

| 예측 금액 | 138억 달러 |

| CAGR | 13.6% |

차량용 솔루션 분야는 2025년 64.8%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 12.1%를 나타낼 것으로 예측됩니다. 이 솔루션은 전자 제어 장치, 도메인 컨트롤러, 텔레매틱스 모듈, 인포테인먼트 시스템 전체에 내장된 보안을 제공하여 실시간 모니터링, 침입 방지, 안전한 통신을 실현합니다. 자동차 제조업체들은 규제 및 안전 기준을 충족하고 차량 시스템이 사이버 공격에 대한 내성을 갖출 수 있도록 차량 내 보안을 최우선 과제로 삼고 있습니다.

네트워크 보안 분야는 2025년 43.8%의 점유율을 차지하며 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 12.8%를 나타낼 것으로 예측됩니다. 네트워크 보안은 차량 통신 네트워크, 차량용 데이터 버스, 클라우드 연결을 사이버 위협으로부터 보호하고, 강력한 프로토콜, 실시간 모니터링, 침해 방지 기능을 제공합니다. 시스템 무결성 유지를 위해 OEM 제조업체, 차량 사업자, 모빌리티 서비스 제공업체에게 중요한 요구사항으로 남아있습니다.

미국 커넥티드카 보안 시장은 2025년 14억 달러 규모에 달할 것으로 예상되며, 자동차 제조업체, 차량 사업자, 기술 기업들이 첨단 사이버 보안 플랫폼에 대한 투자를 지속하면서 성장세를 이어가고 있습니다. 각 회사는 통합 하드웨어 및 소프트웨어 솔루션을 도입하여 텔레매틱스, V2X 통신, 차량 내 네트워크를 보호하고 내연기관차와 전기차 모두 안전 표준 및 규제 요건을 준수할 수 있도록 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 증권별, 2022-2035

제6장 시장 추산 및 예측 : 형태별, 2022-2035

제7장 시장 추산 및 예측 : 솔루션별, 2022-2035

제8장 시장 추산 및 예측 : 차량별, 2022-2035

제9장 시장 추산 및 예측 : 추진력별, 2022-2035

제10장 시장 추산 및 예측 : 용도별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.03.18The Global Connected Car Security Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 13.6% to reach USD 13.8 billion by 2035.

The rapid adoption of connected car technologies has created an urgent need for robust cybersecurity across vehicle ecosystems, fleet management platforms, and cloud-connected services. Automakers and enterprises are increasingly embedding security features directly into vehicle electronic architectures, backend servers, and cloud platforms to reduce operational risks and reliance on manual monitoring. Continuous advancements in edge AI processors, V2X communications, and vehicle software platforms are enhancing the performance, scalability, and responsiveness of security solutions. Real-time intrusion detection, secure data exchange, and over-the-air updates are becoming standard to protect large vehicle fleets. Strategic alliances, mergers, and collaborations among automotive OEMs, cybersecurity providers, and cloud operators are accelerating the integration of security into the vehicle lifecycle, fleet operations, and mobility services. Connected car security is evolving from conventional monitoring to AI-powered, proactive threat analysis systems that safeguard software-defined vehicles and mobility platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 13.6% |

The In-vehicle solutions segment held 64.8% share in 2025 and is expected to grow at a CAGR of 12.1% through 2035. These solutions provide embedded security across electronic control units, domain controllers, telematics modules, and infotainment systems, enabling real-time monitoring, intrusion prevention, and secure communications. OEMs prioritize in-vehicle security to meet regulatory and safety standards while ensuring vehicle systems are resilient to cyberattacks.

The network security segment accounted for 43.8% share in 2025 and is projected to grow at a CAGR of 12.8% from 2026 to 2035. Network security safeguards vehicle communication networks, in-vehicle data buses, and cloud connections against cyber threats, providing robust protocols, real-time monitoring, and breach mitigation. It remains a critical requirement for OEMs, fleet operators, and mobility service providers to maintain system integrity.

US Connected Car Security Market generated USD 1.4 billion in 2025, and continues to grow as automakers, fleet operators, and technology firms invest in advanced cybersecurity platforms. Companies deploy integrated hardware and software solutions to protect telematics, V2X communications, and in-vehicle networks, ensuring compliance with safety and regulatory requirements for both internal combustion and electric vehicles.

Leading players in the Global Connected Car Security Market include ARM, AUMOVIO, BlackBerry, Harman International, Intertek, Keysight Technologies, KPIT Technologies, NXP Semiconductors, Secunet Security Networks, and Thales. Companies in the Global Connected Car Security Market are strengthening their foothold by investing in AI-powered intrusion detection, over-the-air threat management, and secure vehicle software stacks. They are forming strategic partnerships with OEMs, mobility service providers, and cloud vendors to integrate security across vehicle lifecycles and connected platforms. Firms are prioritizing R&D for edge AI, V2X protection, and secure telematics modules while expanding global deployment of security solutions. Emphasis is placed on compliance with automotive cybersecurity regulations, predictive threat intelligence, and real-time network monitoring.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Security

- 2.2.3 Form

- 2.2.4 Solution

- 2.2.5 Vehicle

- 2.2.6 Propulsion

- 2.2.7 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of connected and software-defined vehicles

- 3.2.1.2 Increasing cybersecurity threats targeting automotive systems

- 3.2.1.3 Regulatory mandates and safety standards

- 3.2.1.4 Growth of electric, autonomous, and shared mobility vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of securing heterogeneous vehicle architectures

- 3.2.2.2 Data privacy and cross-border regulatory compliance issues

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of security into vehicle software platforms and OTA ecosystems

- 3.2.3.2 Expansion of V2X, 5G, and cloud-based vehicle services

- 3.2.3.3 Rising adoption of hardware-based security solutions

- 3.2.3.4 Growing focus on autonomous driving and ADAS security

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 U.S. Department of Commerce / Bureau of Industry and Security (BIS)

- 3.4.1.3 Federal Trade Commission (FTC)

- 3.4.2 Europe

- 3.4.2.1 UNECE WP.29 Regulations (UN R155 & R156)

- 3.4.2.2 EN / ISO Automotive Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for Vehicle Cybersecurity

- 3.4.3.2 India Automotive Standards (AIS 189 & AIS 190)

- 3.4.4 Latin America

- 3.4.4.1 Brazil: LGPD (Lei Geral de Protecao de Dados)

- 3.4.4.2 Mexico: NOM Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States: IoT & V2X Security Policy

- 3.4.5.2 Saudi Arabia: SDAIA Automotive AI Framework

- 3.4.5.3 African Union (AU): Data Policy Framework

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing trend analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Energy efficiency in production

- 3.10.3 Carbon footprint considerations

- 3.11 Data Governance, Cybersecurity, and Model Risk

- 3.11.1 Data Privacy and Compliance

- 3.11.2 Model Security

- 3.11.3 Operational and Systemic Risks

- 3.12 Security Architecture

- 3.12.1 Multi-layer Security Models

- 3.12.2 Vehicle-to-Everything (V2X) Security

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Security, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Endpoint security

- 5.3 Application security

- 5.4 Network security

- 5.5 Cloud security

Chapter 6 Market Estimates & Forecast, By Form, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 In-Vehicle Solutions

- 6.3 External Cloud Services

Chapter 7 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Software

- 7.3 Hardware

- 7.3.1 Hardware security modules (HSM)

- 7.3.2 Secure microcontrollers

- 7.3.3 Trusted platform modules (TPM)

- 7.3.4 Secure gateways

- 7.3.5 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Hatchback

- 8.3 Sedan

- 8.4 SUV

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Internal combustion engine (ICE)

- 9.3 Electric vehicle

- 9.3.1 Battery electric vehicle (BEV)

- 9.3.2 Plug-in hybrid electric vehicle (PHEV)

- 9.3.3 Hybrid electric vehicle (HEV)

- 9.3.4 Fuel cell electric vehicle (FCEV)

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Telematics control units (TCUS)

- 10.3 Infotainment systems

- 10.4 Adas & autonomous driving systems

- 10.5 Communication modules

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Norway

- 11.3.9 Denmark

- 11.3.10 Netherlands

- 11.3.11 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.4.9 Malaysia

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 BlackBerry

- 12.1.2 NXP Semiconductors

- 12.1.3 Harman International

- 12.1.4 Thales

- 12.1.5 ARM

- 12.1.6 Trend Micro

- 12.1.7 Keysight Technologies

- 12.1.8 Intertek

- 12.1.9 T-Systems International

- 12.1.10 KPIT Technologies

- 12.1.11 Tata Elxsi

- 12.2 Regional players

- 12.2.1 AUMOVIO

- 12.2.2 Vector Informatik

- 12.2.3 ETAS

- 12.2.4 ASTEMO

- 12.2.5 Autocrypt

- 12.2.6 Secunet Security Networks

- 12.2.7 Trustonic

- 12.2.8 Device Authority

- 12.2.9 WirelessCar

- 12.3 Emerging players

- 12.3.1 Upstream Security

- 12.3.2 Trillium Secure

- 12.3.3 Karamba Security

- 12.3.4 Intertrust Technologies

- 12.3.5 GuardKnox