|

시장보고서

상품코드

1959574

항공기용 화장실 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Lavatory Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

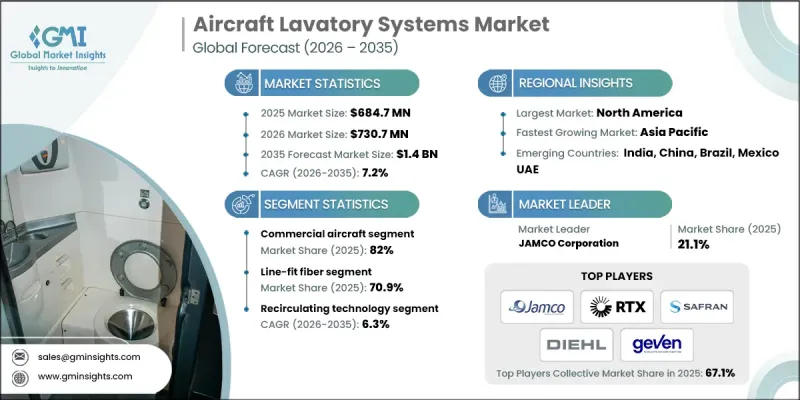

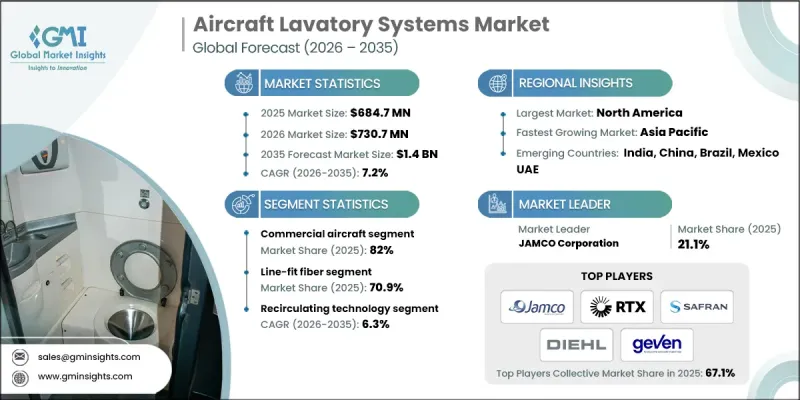

세계의 항공기용 화장실 시스템 시장은 2025년에 6억 8,470만 달러로 평가되었고, 2035년에는 CAGR 7.2%로 성장하여 14억 달러에 이를 것으로 예측됩니다.

시장 확대의 주요 요인으로는 전 세계 항공기 인도량 증가, 개조 및 현대화에 대한 애프터마켓의 강력한 수요, 엄격한 규제 및 안전 기준, 장거리 노선 및 와이드바디 항공기 운항 확대 등을 꼽을 수 있습니다. 신규 항공기에는 라인 핏 생산 시 완전히 통합된 화장실 시스템이 필요하기 때문에 신규 납품이 주요 성장 요인으로 작용할 것입니다. 여객 수송량 증가와 더불어 풀 서비스 항공사와 저가 항공사의 확장과 함께 협동체 항공기, 와이드 바디 항공기, 지역 항공기를 포함한 전체 기체 생산이 가속화되고 있습니다. 또한, 항공사는 승객의 편안함, 위생, 접근성 향상을 위해 노후화된 항공기의 현대화 및 개조를 적극적으로 추진하고 있습니다. 이러한 개조에는 노후화된 모듈 교체, 비접촉식 기술 및 친환경 기술 통합, 객실 레이아웃 최적화 등이 포함됩니다. 경량, 모듈식, 컴팩트한 화장실 시스템은 항공사가 연료 효율, 객실 이용률 및 전반적인 운영 성능을 향상시키려는 노력으로 주목받고 있으며, 전 세계 제조업체들의 지속적인 수요를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 6억 8,470만 달러 |

| 예측 금액 | 14억 달러 |

| CAGR | 7.2% |

2025년 기준, 상업용 항공기 부문은 82%의 점유율을 차지하고 있습니다. 이는 생산량 증가, 항공여행 수요 증가, 그리고 협동체 및 와이드바디 항공기의 대규모 장비 확충이 주요 요인으로 작용하고 있습니다. 항공사의 위생 관리, 규정 준수, 승객의 편안함을 중시하는 항공사는 라인 핏 및 리트로핏 화장실 설비 도입을 촉진하고 있으며, 이는 세계 시장 성장과 보급을 지속적으로 지원하고 있습니다.

리노베이션 부문은 노후화된 기체에서 노후화된 화장실 모듈의 갱신 및 교체 수요로 인해 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.8%로 확대될 것으로 예측됩니다. 항공사들은 승객 경험 향상, 운영 효율성, 규제 준수를 위해 비접촉식, 친환경, 공간 절약형 시스템 도입에 박차를 가하고 있습니다. 이러한 추세는 상용기, 비즈니스기, 지역항공기 애프터마켓에서 지속적인 기회를 창출하고 있습니다.

2025년 기준 북미 항공기 화장실 시스템 시장은 38.9%의 점유율을 차지했습니다. 이러한 성장은 상업용 항공기 인도량 증가, 기체 현대화, 주요 항공사의 지속적인 개보수 프로그램에 의해 촉진되고 있습니다. 연방항공청(FAA)의 엄격한 위생 및 접근성 기준과 지역 및 와이드바디 항공기에 대한 투자가 결합되어 업그레이드 및 교체 수요를 지속적으로 견인하고 있습니다. 항공사들이 연료 효율성 향상, 객실 최적화, 승객 편의성 향상에 집중하면서 경량, 모듈식, 비접촉식 화장실 솔루션의 채택이 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기종별, 2022-2035

제6장 시장 추산 및 예측 : 기술별, 2022-2035

제7장 시장 추산 및 예측 : 적합 유형별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.03.18The Global Aircraft Lavatory Systems Market was valued at USD 684.7 million in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 1.4 billion in 2035.

The market expansion is driven by the increase in global aircraft deliveries, strong aftermarket demand for retrofits and modernization, strict regulatory and safety standards, and the growth of long-haul and widebody operations. Each new aircraft requires fully integrated lavatory systems during line-fit production, making new deliveries a major driver. The growth in air passenger traffic, coupled with the expansion of full-service and low-cost airlines, is accelerating production across narrow-body, wide-body, and regional fleets. Additionally, airlines are increasingly modernizing and retrofitting older aircraft to enhance passenger comfort, hygiene, and accessibility. These retrofits include replacing outdated modules, integrating touchless and environmentally friendly technologies, and optimizing cabin layouts. Lightweight, modular, and compact lavatory systems are gaining traction as airlines aim to improve fuel efficiency, cabin utilization, and overall operational performance, creating a continuous source of demand for manufacturers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $684.7 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 7.2% |

The commercial aircraft segment held an 82% share in 2025, due to high production volumes, growing air travel demand, and extensive fleet expansions across narrow-body and wide-body aircraft. Airlines' emphasis on hygiene, regulatory compliance, and passenger comfort is driving both line-fit and retrofit lavatory installations, supporting sustained market growth and adoption globally.

The retrofit segment is projected to grow at a CAGR of 7.8% through 2026-2035, as aging fleets require updates and replacement of outdated lavatory modules. Airlines are increasingly incorporating touchless, eco-friendly, and space-efficient systems to boost passenger experience, operational efficiency, and regulatory compliance. This trend is creating recurring opportunities in the aftermarket for commercial, business, and regional aircraft.

North America Aircraft Lavatory Systems Market held a 38.9% share in 2025. Growth is fueled by high commercial aircraft deliveries, fleet modernization, and ongoing retrofit programs across major airlines. The FAA's stringent sanitation and accessibility standards, combined with investments in regional and widebody aircraft, continue to drive demand for upgrades and replacements. Adoption of lightweight, modular, and touchless lavatory solutions is increasing, as airlines focus on improving fuel efficiency, cabin optimization, and passenger comfort.

Key players operating in the Global Aircraft Lavatory Systems Market include AeroAid Ltd, FACC AG, AVIC Cabin Systems, Geven Spa, Diehl Stiftung & Co. KG, JAMCO Corporation, ST Engineering, RTX, THE YOKOHAMA RUBBER CO., LTD, EFW GmbH, and Safran S.A. Companies in the aircraft lavatory systems industry are employing several strategies to strengthen their market position. They are focusing on R&D to develop modular, lightweight, and touchless systems that enhance passenger comfort and cabin efficiency. Strategic partnerships with airlines and aircraft manufacturers allow for early adoption of new technologies and integration into both line-fit and retrofit programs. Expanding manufacturing capabilities and establishing local production facilities in key aviation markets ensures timely supply and cost optimization. Firms are also investing in sustainable, eco-friendly lavatory technologies to align with regulatory trends and environmental initiatives.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Aircraft type trends

- 2.2.2 Technology trends

- 2.2.3 Fit type industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in global aircraft deliveries

- 3.2.1.2 Aftermarket demand in retrofit and modernization

- 3.2.1.3 Stringent regulatory and safety standards

- 3.2.1.4 Increase in long-haul and widebody operations

- 3.2.1.5 Focus on lightweight and space-efficient cabins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost and certification complexity

- 3.2.2.2 Cyclicality of aircraft production

- 3.2.3 Market opportunities

- 3.2.3.1 Growing retrofit and replacement cycle

- 3.2.3.2 Rising demand from emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Commercial aircraft

- 5.2.1 Narrow body aircraft

- 5.2.2 Wide body aircraft

- 5.3 Regional aircraft

- 5.4 Business jets

- 5.5 Freighters

- 5.6 Military aircraft

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Vacuum technology

- 6.3 Recirculating technology

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Fit Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Line-fit

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 JAMCO Corporation

- 9.1.2 RTX

- 9.1.3 Safran S.A.

- 9.1.4 Diehl Stiftung & Co. KG

- 9.1.5 Geven SpA

- 9.2 Regional key players

- 9.2.1 AeroAid Ltd

- 9.2.2 AVIC Cabin Systems

- 9.2.3 CIRCOR Aerospace

- 9.2.4 EFW GmbH

- 9.2.5 FACC AG

- 9.2.6 ST Engineering

- 9.2.7 THE YOKOHAMA RUBBER CO., LTD.