|

시장보고서

상품코드

1959605

항공교통 관리 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Air Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

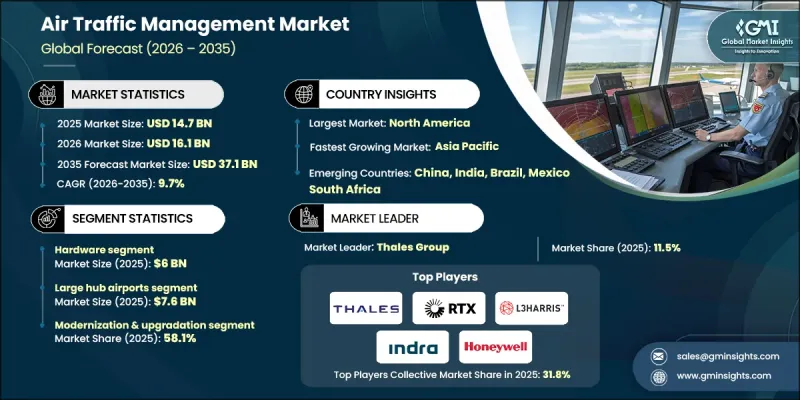

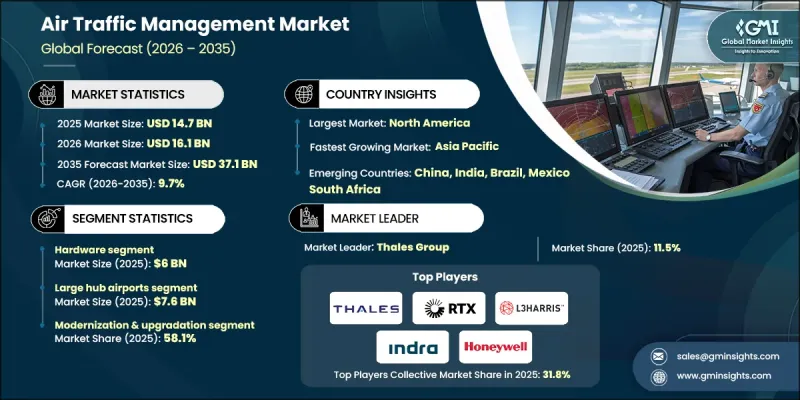

세계의 항공교통 관리 시장은 2025년에 147억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.7%로 성장하여 371억 달러에 이를 것으로 예측됩니다.

시장 성장은 상업용, 국방용, 복합용도 공역에서의 항공 운항이 빠르게 발전하면서 주도하고 있습니다. 항공 교통 관리 솔루션은 비행 경로 조정, 교통 흐름 관리, 통신, 항법 및 감시 기능을 지원하여 혼잡한 공역에서 항공기의 안전하고 효율적인 이동을 보장하는 데 핵심적인 역할을 합니다. 전 세계 항공 교통량이 증가하고 비행 패턴이 복잡해짐에 따라, 항공 생태계 전반의 이해관계자들은 모든 비행 단계에 걸쳐 실시간 상황 인식을 제공하는 첨단 시스템에 많은 투자를 하고 있습니다. 디지털 항공 인프라에 대한 의존도가 높아지면서 혼잡한 공역 조건에서도 성능을 유지할 수 있는 정밀한 항공 교통 관리 플랫폼에 대한 수요가 증가하고 있습니다. 항공 당국과 서비스 제공업체들은 안전, 운영 효율성 및 교통 예측성 향상을 핵심 우선순위로 삼고 있으며, 미래의 영공 요건을 지원하기 위해 기술적으로 진보된 탄력적인 항공 교통 관리 아키텍처를 도입하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 147억 달러 |

| 예측 금액 | 371억 달러 |

| CAGR | 9.7% |

하드웨어 부문은 2025년에 60억 달러의 수익을 창출할 것으로 예측됩니다. 하드웨어는 항공교통관제 인프라에서 여전히 필수적인 요소로 레이더 시스템, 통신 네트워크, 항법장치, 감시 기술을 뒷받침하고 있습니다. 이 부품들은 민간 항공과 국방 항공 모두에서 중요한 역할을 하며, 가혹한 환경에서의 내구성, 신뢰성, 긴 작동 수명으로 평가받고 있습니다. 기존 시스템과의 높은 호환성과 검증된 확장성으로 인해 공항, 항공 교통 서비스 제공업체, 정부 기관에 널리 도입되어 ATM 하드웨어 투자에 대한 지속적인 수요가 강화되고 있습니다.

대규모 허브 공항 부문은 2025년 76억 달러로 세계 항공 네트워크에서 핵심적인 역할을 반영하여 세계 항공 네트워크의 핵심 역할을 반영합니다. 이들 공항은 높은 비행량과 복잡한 공역 상호 운용을 관리하기 때문에 효율성과 안전성을 유지하기 위해 첨단 항공 교통 관리 플랫폼이 필수적입니다. 지속적인 교통 흐름을 관리하기 위해서는 대용량 레이더, 디지털 관제탑, 통합 통신 시스템, 고급 소프트웨어 도구가 필수적입니다. 지속적인 현대화 프로그램과 정부 및 항공사의 강력한 투자가 결합되어 주요 국제 허브 공항에서 첨단 항공 교통 관리 기술의 채택을 지속적으로 지원하고 있습니다.

미국의 항공 교통 관리 시장은 2025년 61억 달러에 달했습니다. 공항 업그레이드, 국방 항공 역량, 차세대 항공 교통 관제 솔루션에 대한 지속적인 투자에 힘입어 성장세를 이어가고 있습니다. 디지털 관제탑 시스템, 예측 분석, 실시간 공역 최적화 플랫폼의 도입 확대가 시장의 모멘텀을 더욱 강화하고 있습니다. 고도의 자동화 및 데이터 기반 교통 관리 프레임워크를 통한 국가 영공 인프라의 지속적인 변화는 ATM 기술의 강력한 장기적 성장 전망을 강조하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제공별, 2022-2035

제6장 시장 추산 및 예측 : 공역 유형별, 2022-2035

제7장 시장 추산 및 예측 : 공항 규모별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 설치 유형별, 2022-2035

제10장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.03.16The Global Air Traffic Management Market was valued at USD 14.7 billion in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 37.1 billion by 2035.

Market growth is driven by the rapid evolution of aviation operations across commercial, defense, and mixed-use airspace. Air traffic management solutions are central to coordinating flight trajectories, managing traffic flows, and supporting communication, navigation, and surveillance functions that ensure safe and efficient aircraft movement in increasingly crowded skies. As global air traffic volumes rise and flight patterns become more complex, stakeholders across the aviation ecosystem are investing heavily in advanced systems that deliver real-time situational awareness across all flight phases. The growing dependence on digital aviation infrastructure has heightened demand for precision-based ATM platforms capable of maintaining performance under congested airspace conditions. Safety enhancement, operational efficiency, and improved traffic predictability remain core priorities, pushing aviation authorities and service providers toward technologically advanced and resilient air traffic management architectures designed to support future airspace requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.7 Billion |

| Forecast Value | $37.1 Billion |

| CAGR | 9.7% |

The hardware segment generated USD 6 billion in 2025. Hardware remains essential to air traffic control infrastructure, supporting radar systems, communication networks, navigation equipment, and surveillance technologies. These components are critical for both civil and defense aviation operations and are valued for their durability, reliability, and long operational life in demanding environments. Strong compatibility with existing systems and proven scalability have driven widespread deployment across airports, air navigation service providers, and government agencies, reinforcing sustained demand for ATM hardware investments.

The large hub airports segment accounted for USD 7.6 billion in 2025, reflecting their central role in global aviation networks. These airports manage high flight volumes and complex airspace interactions, requiring advanced ATM platforms to maintain efficiency and safety. High-capacity radars, digital control towers, integrated communication systems, and advanced software tools are essential for managing continuous traffic flows. Ongoing modernization programs, combined with strong government and airline investment, continue to support the adoption of advanced air traffic management technologies across major international hubs.

U.S. Air Traffic Management Market reached USD 6.1 billion in 2025. Growth in the country is supported by sustained investment in airport upgrades, defense aviation capabilities, and next-generation air traffic control solutions. Increasing deployment of digital tower systems, predictive analytics, and real-time airspace optimization platforms is further strengthening market momentum. Continued transformation of national airspace infrastructure through advanced automation and data-driven traffic management frameworks highlights the strong long-term growth outlook for ATM technologies.

Key companies active in the Global Air Traffic Management Market include Thales Group, Raytheon Technologies Corporation, Honeywell International Inc., Indra Sistemas, S.A., Saab AB, Leonardo S.p.A., L3Harris Technologies, Inc., BAE Systems plc, Frequentis AG, Northrop Grumman Corporation, Adacel Technologies Limited, Aireon LLC, Nav Canada, NATS Holdings Limited, and SITA. Companies operating in the air traffic management market are focusing on long-term strategies that emphasize innovation, system modernization, and global collaboration. Major players invest heavily in research and development to enhance automation, cybersecurity, predictive analytics, and AI-driven traffic optimization. Strategic partnerships with aviation authorities, defense agencies, and airport operators help accelerate system deployment and ensure regulatory alignment. Firms also prioritize modular and scalable solutions that integrate seamlessly with legacy infrastructure. Expanding service portfolios, offering lifecycle support, and providing digital upgrades enable vendors to strengthen customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Airspace Type trends

- 2.2.3 Airport Size trends

- 2.2.4 Application trends

- 2.2.5 Installation Type trends

- 2.2.6 End user trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for advanced aerospace systems

- 3.2.1.2 Drone safety and regulations are driving demand for real-time Air Traffic Managements

- 3.2.1.3 Expansion of commercial aviation

- 3.2.1.4 Focus on maintenance and upgrades

- 3.2.1.5 Miniaturization & advanced sensor technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operating costs and harsh operating environments

- 3.2.2.2 Complex certification, integration, and long development cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in offshore oil and gas projects

- 3.2.3.2 Rising need for fast-start and flexible power plants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Radars & Surveillance

- 5.2.2 Communication & Navigation

- 5.2.3 Controller Working Positions & Displays

- 5.2.4 Meteorological Hardware

- 5.2.5 Others

- 5.3 Software & Systems

- 5.3.1 ATC Automation

- 5.3.2 Air Traffic Flow Management (ATFM)

- 5.3.3 Airspace Management (ASM)

- 5.3.4 Aeronautical Information Management (AIM)

- 5.3.5 Others

- 5.4 Services

- 5.4.1 Integration & Deployment Services

- 5.4.2 Managed & Support Services

- 5.4.3 Training & Simulation Services

Chapter 6 Market Estimates and Forecast, By Airspace Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Terminal Area

- 6.3 En-Route

- 6.4 Oceanic & Remote

Chapter 7 Market Estimates and Forecast, By Airport Size, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Small Airports (<2M Passengers Annually)

- 7.3 Medium Airports (2-15M Passengers Annually)

- 7.4 Large Hub Airports (>15M Passengers Annually)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Communication Management

- 8.3 Navigation Support

- 8.4 Surveillance & Monitoring

- 8.5 Automation Support

Chapter 9 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 New Installation

- 9.3 Modernisation & Upgradation

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Commercial Aviation

- 10.3 Military and Government

- 10.4 Urban Air Mobility (UAM) Operators

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Adacel Technologies Limited

- 12.2 Aireon LLC

- 12.3 BAE Systems plc

- 12.4 Frequentis AG

- 12.5 Honeywell International Inc.

- 12.6 Indra Sistemas, S.A.

- 12.7 L3Harris Technologies, Inc.

- 12.8 Leonardo S.p.A.

- 12.9 NATS Holdings Limited

- 12.10 Nav Canada

- 12.11 Northrop Grumman Corporation

- 12.12 Raytheon Technologies Corporation

- 12.13 Saab AB

- 12.14 SITA

- 12.15 Thales Group