|

시장보고서

상품코드

2007117

항공교통관리 시장 : 운영별, 기술별, 솔루션별, 도입 형태별, 지역별 - 세계 예측(-2030년)Air Traffic Management Market by Operation (ATS, ATFM, ASM, AIM), Technology (Communication, Navigation, Surveillance, Automation Systems), Solution (Hardware, Software, Services), Deployment (New, Upgrade), and Region - Global Forecast to 2030 |

||||||

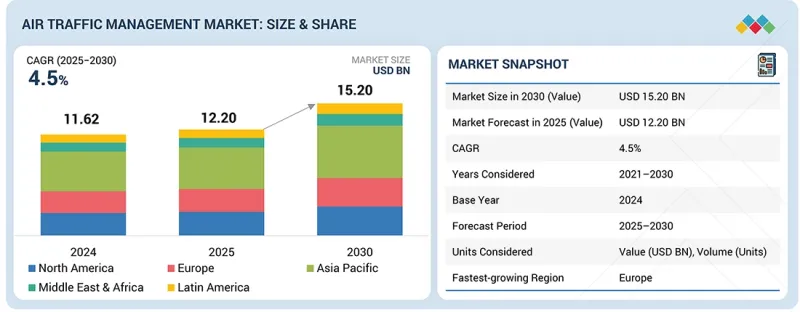

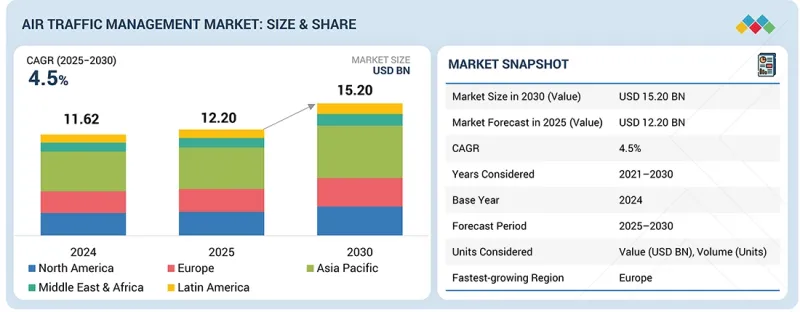

세계의 항공교통관리 시장 규모는 2025년에 122억 달러에 달할 것으로 예측되며, 2025년부터 2030년까지 CAGR 4.5%로 확대되어 2030년에는 152억 달러에 달할 것으로 전망됩니다.

시장의 성장은 매년 증가하는 세계 여객 및 화물 운송량에 의해 주도되고 있습니다. 이러한 꾸준한 성장은 기존 공역 용량에 부담을 주며 운항 관리를 더욱 복잡하게 만들고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(달러) |

| 부문 | 운영, 기술, 솔루션, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

교통량이 증가함에 따라 구식 시스템으로는 효율성을 유지하기가 점점 더 어려워지고 있습니다. 각국 정부와 항공교통관리 서비스 제공업체들은 안전성을 높이고 혼잡을 완화하기 위해 통신, 항법, 감시, 자동화 인프라 업그레이드에 투자하고 있습니다. 또한, 무인항공기 시스템과 첨단 항공 모빌리티 플랫폼의 통합으로 인해 다양한 지역에서 확장성이 높고 디지털화된 항공교통관리 솔루션에 대한 수요가 증가하고 있습니다.

"솔루션별로는 소프트웨어 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

소프트웨어 부문은 주로 디지털화와 데이터 기반 영공 운영으로의 전환으로 인해 가장 빠른 성장을 보일 것으로 예상됩니다. 실시간 데이터 처리, 예측 분석, 통합 의사결정 지원 시스템에 대한 수요가 증가함에 따라 첨단 항공교통관리 소프트웨어 솔루션의 도입이 증가하고 있습니다. 또한, 다양한 이해관계자 간의 원활한 상호운용성에 대한 요구가 증가하고 있으며, 이는 확장 가능한 클라우드 기반 플랫폼에 대한 투자를 촉진하고 있습니다. 이러한 요소들은 운영 효율성 향상, 상황 인식 강화, 항공 교통 흐름 관리 활성화에 기여하고 있습니다.

"통신 시스템별로는 관제사 및 파일럿 데이터 링크(CPDLC) 부문이 가장 높은 CAGR로 성장할 것으로 예상됩니다."

항공교통관리 시장에서 CPDLC 통신 부문이 가장 빠르게 성장할 것으로 예상됩니다. 이는 주로 조종사와 항공 교통 관제사들 사이에서 보다 효율적이고 안정적인 통신에 대한 요구가 증가하고 있기 때문입니다. 항공 교통 혼잡의 증가로 인해 기존의 음성 통신에서 주파수 혼잡을 줄이고 통신 오류를 최소화하기 위한 데이터 링크 시스템으로 전환이 진행되고 있습니다.

동시에, 규제 요건과 현대화 프로그램도 안전성을 유지하면서 공역의 효율성을 높이기 위해 이러한 시스템의 도입을 촉진하고 있습니다. 이러한 발전은 메시지의 정확성을 향상시키고 관제사의 업무 부담을 줄여 항공 교통 운영을 더욱 효율적으로 만들 수 있습니다.

"라틴아메리카는 예측 기간 동안 안정적인 CAGR로 성장할 것으로 예상됩니다."

라틴아메리카 지역에서는 공항 인프라에 대한 투자 확대와 영공 현대화 노력에 힘입어 항공교통관리 시장이 꾸준히 성장할 것으로 예상됩니다. 승객 수 증가와 지역 항공사의 네트워크 확대로 인해 보다 효율적이고 신뢰할 수 있는 항공 교통 시스템에 대한 수요가 증가하고 있습니다. 이러한 추세는 지역 전체에 첨단 항공교통관리 기술의 도입을 점차 촉진하고 있습니다.

세계의 항공교통관리 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 도입 사례, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 규제 상황과 지속가능성에 대한 대처

제8장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제9장 항공교통관리 시장 : 운영별

제10장 항공교통관리 시장 : 기술별

제11장 항공교통관리 시장 : 솔루션별

제12장 항공교통관리 시장 : 도입 형태별

제13장 항공교통관리 시장 : 고객별

제14장 항공교통관리 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.04.28The global air traffic management market is projected to reach USD 12.20 billion in 2025 and is expected to grow to USD 15.20 billion by 2030, at a CAGR of 4.5% from 2025 to 2030. Market growth is driven by the continuous increase in global passenger and cargo traffic each year. This steady growth puts pressure on existing airspace capacity and makes operations more complex to manage.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Operation, Technology, Solution and Region |

| Regions covered | North America, Europe, APAC, RoW |

As traffic volume rises, it becomes more difficult to maintain efficiency with older systems. Governments and air navigation service providers are investing in upgrading communication, navigation, surveillance, and automation infrastructure to enhance safety and reduce congestion. Meanwhile, the integration of unmanned aircraft systems and advanced air mobility platforms is creating a demand for scalable, more digital air traffic management solutions across various regions.

"By solution, the software segment is projected to grow at the highest CAGR during the fore cast period."

The software segment is projected to experience the fastest growth in the air traffic management market, mainly due to the shift toward digital and data-driven airspace operations. The increasing demand for real-time data processing, predictive analytics, and integrated decision support systems is driving the adoption of advanced air traffic management software solutions. There is also a growing need for seamless interoperability among different stakeholders, which is encouraging investments in scalable, cloud-based platforms. These factors are helping improve operational efficiency, boost situational awareness, and make air traffic flow management more effective.

"By communication system, the controller-pilot data link controller (CPDLC) segment is projected to grow at the highest CAGR."

The controller pilot data link communications segment is expected to see the fastest growth in the air traffic management market, mainly due to the increasing need for more efficient and reliable communication between pilots and air traffic controllers. Growing air traffic congestion is driving the shift from traditional voice-based communication to data link systems that help reduce frequency congestion and minimize communication errors.

At the same time, regulatory requirements along with modernization programs support the adoption of these systems to enhance airspace efficiency while maintaining safety. These developments help improve message accuracy, reduce controller workload, and make air traffic operations more streamlined.

"Latin America is projected to grow at a steady CAGR during the forecast period."

The Latin America region is expected to experience steady growth in the air traffic management market, mainly driven by increasing investments in airport infrastructure and airspace modernization efforts. Rising passenger traffic and the expansion of regional airline networks are creating a greater need for more efficient and reliable air traffic systems. These developments are gradually encouraging the adoption of advanced air traffic management technologies across the region.

The breakdown of profiles for primary participants in the air traffic management market is provided below:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East - 10% Rest of the World (RoW) - 5%

Research Coverage:

This market study examines the air traffic management market across various segments and subsegments. It aims to estimate the market's size and growth potential in different regions. The study also provides a detailed competitive analysis of key market players, including their company profiles, product offerings, recent developments, and strategic market initiatives.

Reasons to buy this report:

The report will assist market leaders and new entrants with estimates of the revenue figures for the overall air traffic management market. It will also enable stakeholders to understand the competitive landscape better and gain insights to position their businesses more effectively and develop appropriate go-to-market strategies. Additionally, the report will help stakeholders understand the market dynamics and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Rising Global Air Traffic and Airspace Congestion), Restraints (High Capital Investment and Long Implementation Cycles), Opportunities (Adoption of Artificial Intelligence and Predictive Analytics), Challenges (Escalating Cybersecurity Risks in Digitized Air Traffic Management Infrastructure)

- Market Penetration: Comprehensive information on the air traffic management market offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the air traffic management market.

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the air traffic management market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the air traffic management market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AIR TRAFFIC MANAGEMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AIR TRAFFIC MANAGEMENT MARKET

- 3.2 AIR TRAFFIC MANAGEMENT MARKET, BY DEPLOYMENT

- 3.3 AIR TRAFFIC MANAGEMENT MARKET, BY CUSTOMER

- 3.4 AIR TRAFFIC MANAGEMENT MARKET, BY SOLUTION

- 3.5 AIR TRAFFIC MANAGEMENT MARKET, BY TECHNOLOGY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising global air traffic and airspace congestion

- 4.2.1.2 Government-led airspace modernization programs

- 4.2.1.3 Increasing focus on operational efficiency and cost optimization

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital investment and long implementation cycles

- 4.2.2.2 Integration complexity with legacy systems

- 4.2.2.3 Shortage of skilled air traffic and technical personnel

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of unmanned aircraft systems and advanced air mobility

- 4.2.3.2 Adoption of artificial intelligence and predictive analytics

- 4.2.3.3 Expansion of cross-border airspace harmonization initiatives

- 4.2.4 CHALLENGES

- 4.2.4.1 Escalating cybersecurity risks in digitized air traffic management infrastructure

- 4.2.4.2 Regulatory fragmentation across global jurisdictions

- 4.2.4.3 Managing traffic volatility and unpredictable disruptions

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 STANDARDIZED DIGITAL DATA EXCHANGE ACROSS AVIATION ECOSYSTEM

- 4.3.2 ADVANCED HUMAN-MACHINE COLLABORATION TOOLS FOR CONTROLLERS

- 4.3.3 SCALABLE ATM SOLUTIONS FOR SECONDARY AND REGIONAL AIRPORTS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTEGRATION WITH SMART AIRPORT AND DIGITAL AVIATION ECOSYSTEMS

- 4.4.2 COLLABORATION WITH SPACE-BASED COMMUNICATION AND SATELLITE NAVIGATION PROVIDERS

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL AVIATION INDUSTRY

- 5.2.4 TRENDS IN GLOBAL AIR TRAFFIC MANAGEMENT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 R&D ENGINEERS (~30%)

- 5.3.2 RAW MATERIAL SUPPLIERS (10~%)

- 5.3.3 COMPONENT & PRODUCT MANUFACTURERS (~10%)

- 5.3.4 ASSEMBLERS & INTEGRATORS (~30%)

- 5.3.5 END USERS (~20%)

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 MANUFACTURERS

- 5.4.2 SOLUTION AND SERVICE PROVIDERS

- 5.4.3 END USERS

- 5.5 INVESTMENT & FUNDING SCENARIO

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING OF AIR TRAFFIC HARDWARE TYPES, BY KEY PLAYER

- 5.6.2 INDICATIVE PRICING, BY HARDWARE

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8526)

- 5.7.2 EXPORT SCENARIO (HS CODE 8526)

- 5.8 KEY CONFERENCE & EVENTS, 2025-2026

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 THALES DEPLOYED ADVANCED DIGITAL TOWER PLATFORM USING HIGH-DEFINITION

- 5.10.2 INDRA IMPLEMENTED UNIFIED AIR TRAFFIC MANAGEMENT AUTOMATION PLATFORM

- 5.10.3 FREQUENTIS DEPLOYED IP-BASED VOICE COMMUNICATION CONTROL SYSTEM CONNECTING TOWERS, APPROACH, AND EN-ROUTE CENTERS THROUGH REDUNDANT DIGITAL NETWORK

- 5.11 IMPACT OF 2025 US TARIFF

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRY/REGION

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE SECTORS

- 5.11.4.1 Commercial

- 5.11.4.2 Government & military

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS FROM VARIOUS END USES

- 6.4.1 NEED FOR HIGH AUTOMATION AND DECISION-SUPPORT CAPABILITIES

- 6.4.2 NEED FOR SEAMLESS CROSS-BORDER INTEROPERABILITY

- 6.4.3 NEED FOR FLEXIBLE AND SCALABLE DIGITAL INFRASTRUCTURE

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT REDUCTION

- 7.2.2 ECO-APPLICATIONS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.1 SUSTAINABILITY IMPACT ON AIR TRAFFIC MANAGEMENT MARKET

- 7.3.2 REGULATORY POLICIES DRIVING AIR TRAFFIC MANAGEMENT DEPLOYMENT

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 KEY EMERGING TECHNOLOGIES

- 8.1.1 ARTIFICIAL INTELLIGENCE-DRIVEN AIR TRAFFIC FLOW MANAGEMENT

- 8.1.2 AUTOMATIC DEPENDENT SURVEILLANCE-BROADCAST (ADS-B) AND SPACE-BASED SURVEILLANCE

- 8.1.3 SYSTEM-WIDE INFORMATION MANAGEMENT (SWIM) DATA EXCHANGE PLATFORMS

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 DIGITAL AERONAUTICAL INFORMATION MANAGEMENT (AIM) AND E-CHARTS

- 8.2.2 DIGITAL TWIN SIMULATION AND PREDICTIVE OPERATIONS PLATFORMS

- 8.2.3 QUANTUM-RESILIENT CYBERSECURITY AND SECURE AVIATION NETWORKS

- 8.3 ADJACENT TECHNOLOGIES

- 8.3.1 ADVANCED WEATHER INTELLIGENCE AND NOWCASTING PLATFORMS

- 8.3.2 ADVANCED AIRPORT COLLABORATIVE DECISION-MAKING (A-CDM) INTEGRATED WITH AIRPORT OPERATIONS PLATFORMS

- 8.4 TECHNOLOGY ROADMAP

- 8.5 PATENT ANALYSIS

- 8.6 FUTURE APPLICATIONS

- 8.6.1 CASE STUDIES

- 8.7 IMPACT OF AI/GEN AI

- 8.7.1 IMPACT OF AI/GEN AI: TOP USE CASES AND MARKET POTENTIAL

- 8.7.2 CASE STUDIES: IMPLEMENTATION OF AI

- 8.7.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 8.7.4 CLIENTS' READINESS TO ADOPT GEN AI

- 8.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

9 AIR TRAFFIC MANAGEMENT MARKET, BY OPERATION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 9.1 INTRODUCTION

- 9.2 AIR TRAFFIC SERVICES (ATS)

- 9.2.1 USE CASE: INTEGRATED ATS PLATFORM BY INDRA

- 9.2.2 AIR TRAFFIC CONTROL (ATC)

- 9.2.2.1 Need to manage increasing aircraft movements to drive growth

- 9.2.2.2 Use case: Digital Tower Air Traffic Control Solution by Saab

- 9.2.3 FLIGHT INFORMATION SERVICES (FIS)

- 9.2.3.1 Increasing reliance of pilots on continuous operational updates to drive market

- 9.2.3.2 Use case: Nationwide Air-Ground Communication System by Indra

- 9.2.4 ALERTING SERVICES

- 9.2.4.1 High traffic volumes and extended oceanic and remote-area operations to boost market

- 9.3 AIR TRAFFIC FLOW MANAGEMENT (ATFM)

- 9.3.1 INCREASING NETWORK CONGESTION TO DRIVE ADOPTION OF PREDICTIVE TRAFFIC FLOW OPTIMIZATION

- 9.3.2 USE CASE: TOPSKY FLOW MANAGER BY THALES

- 9.4 AIRSPACE MANAGEMENT (ASM)

- 9.4.1 INCREASING FLEXIBLE AIRSPACE UTILIZATION TO DRIVE ADOPTION OF DYNAMIC AIRSPACE MANAGEMENT

- 9.4.2 USE CASE: AIRSPACE MANAGER BY INDRA

- 9.5 AERONAUTICAL INFORMATION MANAGEMENT (AIM)

- 9.5.1 TRANSITION FROM STATIC PUBLICATIONS TO DIGITAL AERONAUTICAL DATA TO BOOST AERONAUTICAL INFORMATION MANAGEMENT

- 9.5.2 USE CASE: CADAS-AIMDB BY COMSOFT SOLUTIONS

- 9.6 AIRSPACE DESIGN

- 9.6.1 INCREASING DEMAND FOR PERFORMANCE-BASED NAVIGATION TO DRIVE MODERN AIRSPACE DESIGN

- 9.6.2 USE CASE: AIRSPACE OPTIMIZER BY NATS

- 9.7 GEOFENCING

- 9.7.1 INCREASING INTEGRATION OF DRONES AND SENSITIVE AIRSPACE PROTECTION TO DRIVE ADOPTION OF GEOFENCING

- 9.7.2 USE CASE: GEO ZONE GEOFENCING SYSTEM BY DJI

10 AIR TRAFFIC MANAGEMENT MARKET, BY TECHNOLOGY (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 10.1 INTRODUCTION

- 10.2 ASSESSMENT OF BRAND AND PRODUCT USE CASES

- 10.3 COMMUNICATION SYSTEMS

- 10.3.1 DEMAND FOR INCREASING AIR-GROUND COMMUNICATION SYSTEMS TO DRIVE GROWTH

- 10.3.2 USE CASE: VOICE COMMUNICATION CONTROL SYSTEM BY FREQUENTIS

- 10.3.3 VHF VOICE COMMUNICATION

- 10.3.3.1 Use case: Series4200 Software-defined Radio by Rohde & Schwarz

- 10.3.4 CONTROLLER-PILOT DATA LINK COMMUNICATION (CPDLC)

- 10.3.4.1 Use case: Iris Air Traffic Management Service by Inmarsat

- 10.3.5 VOICE COMMUNICATION CONTROL SYSTEM (VCCS)

- 10.3.5.1 Use case: VCS3020X by Frequentis

- 10.3.6 AIR TRAFFIC INFORMATION SYSTEMS (ATIS)

- 10.3.6.1 Use case: D-ATIS by Collins Aerospace

- 10.4 NAVIGATION SYSTEMS

- 10.4.1 TRANSITION TOWARD PERFORMANCE-BASED NAVIGATION TO DRIVE GROWTH IN NAVIGATION SYSTEMS

- 10.4.2 USE CASE: INSTRUMENT LANDING SYSTEM (ILS) BY THALES

- 10.4.3 VOR/DVOR

- 10.4.3.1 Use case: DVOR 5000 by Rohde & Schwarz

- 10.4.4 DME

- 10.4.4.1 Use case: DME 415 by Thales

- 10.4.5 TACAN

- 10.4.5.1 Use case: TACAN 7000 by Rohde & Schwarz

- 10.4.6 NDB

- 10.4.6.1 Use case: NDB 600 by Rohde & Schwarz

- 10.4.7 GNSS/GPS

- 10.4.7.1 Use case: SmartPath Ground-Based Augmentation System by Honeywell

- 10.4.8 PRNAV

- 10.4.8.1 Use case: Required Navigation Performance and PRNAV Procedure Design by NATS

- 10.4.9 ILS

- 10.4.9.1 Use case: ILS 420 by Thales

- 10.5 SURVEILLANCE SYSTEMS

- 10.5.1 INCREASING AIRSPACE COMPLEXITY AND MULTI-SENSOR INTEGRATION TO DRIVE GROWTH IN SURVEILLANCE SYSTEMS

- 10.5.2 USE CASE: MULTI-SENSOR SURVEILLANCE SYSTEM BY THALES

- 10.5.3 PSR

- 10.5.3.1 Use case: STAR NG Primary Surveillance Radar by Thales

- 10.5.4 SSR

- 10.5.4.1 Use case: RSM 970S Secondary Surveillance Radar by HENSOLDT

- 10.5.5 ADS-B

- 10.5.5.1 Use case: Aireon Space-Based ADS-B Service by Aireon

- 10.5.6 MLAT

- 10.5.6.1 Use case: ERA Multilateration System by ERA

- 10.5.7 A-SMGCS

- 10.5.7.1 Use case: A-SMGCS by Thales

- 10.6 AUTOMATION SYSTEMS

- 10.6.1 INCREASING TRAFFIC DENSITY AND OPERATIONAL EFFICIENCY MANDATES TO DRIVE GROWTH IN AUTOMATION SYSTEMS

- 10.6.2 USE CASE: ITEC SKYNEX AUTOMATION PLATFORM BY INDRA

- 10.6.3 FDPS

- 10.6.3.1 Use case: TopSky - Flight Data Processing by Thales

- 10.6.4 SDPS

- 10.6.4.1 Use case: SkyFusion Surveillance Data Processing by Indra

- 10.6.5 AMAN/DMAN

- 10.6.5.1 Use case: TopSky - AMAN/DMAN by Thales

- 10.6.6 STCA/MSAW

- 10.6.6.1 Use case: TopSky - Safety Nets by Thales

- 10.6.7 CONTROL & MONITORING DISPLAYS

- 10.6.7.1 Use case: OneControl Working Position by Indra

- 10.6.8 APOS

- 10.6.8.1 Use case: Airspace Optimizer by NATS

11 AIR TRAFFIC MANAGEMENT MARKET, BY SOLUTION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 11.1 INTRODUCTION

- 11.2 AIR TRAFFIC MANAGEMENT SOLUTIONS: USE CASES

- 11.2.1 DIGITAL TOWERS

- 11.2.1.1 Use case: Digital Tower Suite by Saab

- 11.2.1.2 Use case: Remote Tower Solution by Indra

- 11.2.1.3 Use case: Remote Tower System by Frequentis

- 11.2.2 REMOTE TOWER

- 11.2.2.1 Use case: r-TWR Remote Tower System by Thales

- 11.2.2.2 Use case: Digital Tower Solution by Kongsberg Geospatial

- 11.2.2.3 Use case: Remote Tower Solution by DFS Aviation Services

- 11.2.1 DIGITAL TOWERS

- 11.3 HARDWARE

- 11.3.1 USE CASE: MULTI-SENSOR RADAR HARDWARE DEPLOYMENT BY THALES

- 11.3.2 RADAR SYSTEMS

- 11.3.2.1 Rising airspace security and traffic density to drive growth

- 11.3.2.2 Use case: STAR NG Radar by Thales

- 11.3.3 SENSORS

- 11.3.3.1 Expanding surveillance and environmental monitoring needs to drive growth

- 11.3.3.2 Use case: Aerodrome Weather Observation System (AWOS) by Vaisala

- 11.3.4 ANTENNAS

- 11.3.4.1 Expanding connectivity and spectrum management to drive demand for antennas

- 11.3.4.2 Use case: AV-1745 VHF Airband Antenna by Sensor Systems

- 11.3.5 CAMERAS

- 11.3.5.1 Expanding remote operations and surface monitoring to propel market

- 11.3.5.2 Use case: High-Definition Camera System by Saab Digital Tower

- 11.3.6 DISPLAYS

- 11.3.6.1 Increasing data integration and demand for human-machine interface to drive growth

- 11.3.6.2 Use case: ControlSphere Integrated Display by Thales

- 11.3.7 ENCODERS/DECODERS

- 11.3.7.1 Increasing digital communication and data standardization to drive growth in encoders/decoders for air traffic management

- 11.3.7.2 Use case: Mode S Decoder Unit by Indra

- 11.3.8 AMPLIFIERS

- 11.3.8.1 Increasing signal integrity and coverage requirements to boost growth

- 11.3.8.2 Use case: Solid-State RF Power Amplifier by Rohde & Schwarz

- 11.3.9 OTHERS

- 11.3.9.1 Use case: Integrated Redundant Power & Server Infrastructure by Frequentis

- 11.4 SOFTWARE

- 11.4.1 USE CASE: INTEGRATED ATM SOFTWARE SUITE BY THALES

- 11.4.2 ATM PLATFORMS & SUITES

- 11.4.2.1 Increasing system integration and digital transformation to boost growth

- 11.4.2.2 Use case: TopSky Air Traffic Management Suite by Thales

- 11.4.3 DATABASE MANAGEMENT SYSTEMS

- 11.4.3.1 Growing data volume and integrity requirements to drive market growth

- 11.4.3.2 Use case: Centralized Operational Database by Indra

- 11.4.4 INCIDENT & EVENT MANAGEMENT SOFTWARE

- 11.4.4.1 Increasing operational risk monitoring and regulatory compliance to drive growth of incident & event management software

- 11.4.4.2 Use case: Safety Management System (SMS) Platform by Indra

- 11.4.5 CAPACITY & DEMAND MANAGEMENT SOFTWARE

- 11.4.5.1 Increasing traffic variability and network congestion to spur demand for capacity & demand management software

- 11.4.5.2 Use case: TopSky Flow Manager by Thales

- 11.4.6 COMMUNICATION & RECORDING SOFTWARE

- 11.4.6.1 Increasing regulatory compliance and communication traceability to drive market

- 11.4.6.2 Use case: DIVOS Recording System by Frequentis

- 11.5 SERVICES

- 11.5.1 USE CASE: INTEGRATED LIFECYCLE SERVICES PROGRAM BY THALES

- 11.5.2 SYSTEM INTEGRATION

- 11.5.2.1 Increasing multi-system complexity to drive market growth

- 11.5.2.2 Use case: Integrated ATM Deployment Services by Thales

- 11.5.3 MAINTENANCE & SUPPORT

- 11.5.3.1 Increasing system availability requirements to drive growth of air traffic maintenance & support services

- 11.5.3.2 Use case: Lifecycle Support Services by Indra

- 11.5.4 UPGRADE & MODERNIZATION SERVICES

- 11.5.4.1 Accelerating digital transformation to drive growth

- 11.5.4.2 Use case: ATM Modernization Program by Thales

- 11.5.5 TRAINING & SIMULATION SERVICES

- 11.5.5.1 Rising traffic complexity and technology transition to drive demand

- 11.5.5.2 Use case: ATC Simulation Platform by Indra

12 AIR TRAFFIC MANAGEMENT MARKET, BY DEPLOYMENT (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 12.1 INTRODUCTION

- 12.2 ASSESSMENT OF AIRPORT CLASSES

- 12.2.1 COMMERCIAL AIRPORTS

- 12.2.1.1 Class I (Large international/Hub airports)

- 12.2.1.1.1 Rising international traffic and hub connectivity to drive growth in Class I (Large international/hub airports)

- 12.2.1.1.2 Use case: TopSky - AMAN/DMAN Suite by Thales

- 12.2.1.2 Class II (Major Regional/National Airports)

- 12.2.1.2.1 Expanding regional air connectivity to drive investments in Class II (Major regional/national airports)

- 12.2.1.2.2 Use case: TopSky AMAN by Thales

- 12.2.1.3 Class III (Small commercial/domestic airports)

- 12.2.1.3.1 Regional air mobility expansions to drive modernization in Class III (Small commercial/domestic airports)

- 12.2.1.3.2 Use case: Remote Tower System by Saab

- 12.2.1.4 Class IV (Regional/Remote/General aviation airports)

- 12.2.1.4.1 Cost-efficient airspace oversight to drive growth in Class IV (Regional/Remote/General aviation airports)

- 12.2.1.4.2 Use case: ADS-B Ground Station Solution by Indra

- 12.2.1.1 Class I (Large international/Hub airports)

- 12.2.2 MILITARY AIRPORTS

- 12.2.2.1 Class M-I (Major military air bases - Strategic/Joint operations)

- 12.2.2.1.1 Increasing strategic air defense integration to drive growth in Class M-I (Major military air bases - Strategic/Joint operations)

- 12.2.2.1.2 Use case: Integrated Military ATC System by Indra

- 12.2.2.2 Class M-II (Operational/Tactical air bases)

- 12.2.2.2.1 Increasing tactical mission readiness to drive modernization in Class M-II (Operational/Tactical air bases)

- 12.2.2.2.2 Use case: Deployable ATC System by Thales

- 12.2.2.3 Class M-III (Forward Operating bases/deployed airfields)

- 12.2.2.3.1 Rapid deployment and expeditionary air operations to drive growth in Class M-III (Forward operating bases/deployed airfields)

- 12.2.2.3.2 Use case: Deployable Tactical Radar System by Indra

- 12.2.2.4 Class M-IV (Training, UAV & Auxiliary Airfields)

- 12.2.2.4.1 Expanding unmanned operations and pilot training programs to drive growth in Class M-IV (Training, UAV, auxiliary airfields)

- 12.2.2.4.2 Use case: Deployable Tactical Radar System by Indra

- 12.2.2.1 Class M-I (Major military air bases - Strategic/Joint operations)

- 12.2.3 VERTIPORT

- 12.2.3.1 Emergence of advanced air mobility to drive growth in vertiport infrastructure

- 12.2.3.2 Use case: Urban Air Traffic Management Platform by Thales

- 12.2.1 COMMERCIAL AIRPORTS

- 12.3 NEW INSTALLATION

- 12.3.1 EXPANSION OF AVIATION INFRASTRUCTURE AND GREENFIELD PROJECTS TO DRIVE GROWTH

- 12.3.1.1 Use case: Integrated Greenfield ATM Deployment by Indra

- 12.3.1 EXPANSION OF AVIATION INFRASTRUCTURE AND GREENFIELD PROJECTS TO DRIVE GROWTH

- 12.4 UPGRADE & MODERNIZATION

- 12.4.1 AGING INFRASTRUCTURE AND DIGITAL TRANSITION TO DRIVE GROWTH

- 12.4.1.1 Use case: ATM Modernization Program by Thales

- 12.4.1 AGING INFRASTRUCTURE AND DIGITAL TRANSITION TO DRIVE GROWTH

13 AIR TRAFFIC MANAGEMENT MARKET, BY CUSTOMER (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 13.1 INTRODUCTION

- 13.2 CIVIL AVIATION AUTHORITIES

- 13.2.1 REGULATORY MODERNIZATION AND AIRSPACE SAFETY MANDATES TO DRIVE GROWTH

- 13.2.1.1 National ATM Modernization Program by Indra

- 13.2.1 REGULATORY MODERNIZATION AND AIRSPACE SAFETY MANDATES TO DRIVE GROWTH

- 13.3 AIRPORT OPERATORS

- 13.3.1 INCREASING PASSENGER THROUGHPUT AND OPERATIONAL EFFICIENCY REQUIREMENTS TO PROPEL MARKET

- 13.3.1.1 Use case: Advanced Surface Movement Guidance & Control System by Thales

- 13.3.1 INCREASING PASSENGER THROUGHPUT AND OPERATIONAL EFFICIENCY REQUIREMENTS TO PROPEL MARKET

- 13.4 AIR NAVIGATION SERVICE PROVIDERS (ANSPS)

- 13.4.1 INCREASING AIRSPACE COMPLEXITY AND CAPACITY OPTIMIZATION MANDATES TO DRIVE GROWTH

- 13.4.1.1 Use case: iTEC SkyNex by Indra

- 13.4.1 INCREASING AIRSPACE COMPLEXITY AND CAPACITY OPTIMIZATION MANDATES TO DRIVE GROWTH

- 13.5 MILITARY & GOVERNMENT ORGANIZATIONS

- 13.5.1 FOCUS ON STRENGTHENING NATIONAL AIRSPACE SECURITY AND DEFENSE MODERNIZATION TO DRIVE GROWTH

- 13.5.1.1 Use case: Integrated Military Airspace Management System by Thales

- 13.5.1 FOCUS ON STRENGTHENING NATIONAL AIRSPACE SECURITY AND DEFENSE MODERNIZATION TO DRIVE GROWTH

- 13.6 UTM OPERATORS

- 13.6.1 RAPID EXPANSION OF UNMANNED AIRCRAFT OPERATIONS TO DRIVE GROWTH

- 13.6.1.1 Use case: Integrated Military Airspace Management System by Thales

- 13.6.1 RAPID EXPANSION OF UNMANNED AIRCRAFT OPERATIONS TO DRIVE GROWTH

14 AIR TRAFFIC MANAGEMENT MARKET, BY REGION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Air traffic control modernization programs to drive market

- 14.2.2 CANADA

- 14.2.2.1 Expansion of remote air navigation services to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Implementation of 'UK Airspace Modernization Strategy' to drive market

- 14.3.2 GERMANY

- 14.3.2.1 Upgrade of national air navigation infrastructure to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Investments in remote and digital tower capabilities and improved communication networks to drive market

- 14.3.4 SWEDEN

- 14.3.4.1 Continuous deployment of digital air navigation services to drive market

- 14.3.5 ITALY

- 14.3.5.1 Integration of performance-based navigation procedures and upgraded surveillance systems to drive market

- 14.3.6 SPAIN

- 14.3.6.1 Airport capacity optimization and digital air traffic system deployment to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Increase in passenger traffic and rigorous airport construction to drive market

- 14.4.2 INDIA

- 14.4.2.1 Rapid aviation growth to drive market

- 14.4.3 JAPAN

- 14.4.3.1 High aircraft movement density around metropolitan areas to drive market

- 14.4.4 AUSTRALIA

- 14.4.4.1 Adoption of satellite-based surveillance and advanced traffic flow management systems to drive market

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Smart airport programs and high traffic density to drive market

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.5.1.1 UAE

- 14.5.1.1.1 Rapid passenger growth and expansion of cargo operations to drive market

- 14.5.1.2 Saudi Arabia

- 14.5.1.2.1 Expansion of aviation industry under national transport and tourism development programs to drive market

- 14.5.1.1 UAE

- 14.5.2 SOUTH AFRICA

- 14.5.2.1 Need to strengthen aviation safety and improve regional connectivity to drive market

- 14.5.3 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.6 LATIN AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Strong domestic aviation demand and increased aircraft movements to drive market

- 14.6.2 MEXICO

- 14.6.2.1 Rising passenger volumes and increasing regional connectivity to drive market

- 14.6.3 ARGENTINA

- 14.6.3.1 Emphasis on strengthening aviation safety and improving connectivity to drive market

- 14.6.4 REST OF LATIN AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2021-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 BRAND/PRODUCT COMPARISON

- 15.6 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Technology footprint

- 15.7.5.4 Solution footprint

- 15.7.5.5 Customer footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING

- 15.8.5.1 List of startups/SMEs

- 15.8.5.2 Competitive benchmarking of startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 15.9.2 DEALS

- 15.9.3 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 THALES

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/developments

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Other developments

- 16.1.2 RTX

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Other developments

- 16.1.3 L3HARRIS TECHNOLOGIES, INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.3.2 Other developments

- 16.1.4 INDRA

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Other developments

- 16.1.5 SAAB AB

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Other developments

- 16.1.6 KONGSBERG DEFENSE & AEROSPACE

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Other developments

- 16.1.7 SITA

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches/developments

- 16.1.7.3.2 Deals

- 16.1.7.3.3 Other developments

- 16.1.8 BAE SYSTEMS

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Other developments

- 16.1.9 FREQUENTIS AG

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Other developments

- 16.1.10 HONEYWELL INTERNATIONAL, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.2.1 Deals

- 16.1.10.2.2 Other developments

- 16.1.11 ADVANCED NAVIGATION AND POSITIONING CORPORATION

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Other developments

- 16.1.12 LEIDOS

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Other developments

- 16.1.13 INTELCAN TECHNOSYSTEMS INC.

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Other developments

- 16.1.14 AMADEUS IT GROUP, SA

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.15 LEONARDO S.P.A.

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.15.3.2 Other developments

- 16.1.16 NAV CANADA

- 16.1.16.1 Business overview

- 16.1.16.2 Products offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Product launches/developments

- 16.1.16.3.2 Deals

- 16.1.16.3.3 Other developments

- 16.1.1 THALES

- 16.2 OTHER PLAYERS

- 16.2.1 SEARIDGE TECHNOLOGIES

- 16.2.2 AIREON

- 16.2.3 SKYSOFT-ATM

- 16.2.4 ANRA TECHNOLOGIES

- 16.2.5 ONESKY

- 16.2.6 ALOFT TECHNOLOGIES

- 16.2.7 AEROBITS

- 16.2.8 UNIFLY

- 16.2.9 MOSAIC ATM

- 16.2.10 SKYGRID, LLC

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary interview participants

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Insights from industry experts

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 BASE NUMBER CALCULATION

- 17.3 FACTOR ANALYSIS

- 17.3.1 SUPPLY-SIDE INDICATORS

- 17.3.2 DEMAND-SIDE INDICATORS

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS