|

시장보고서

상품코드

1959617

폴리백 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Polybags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

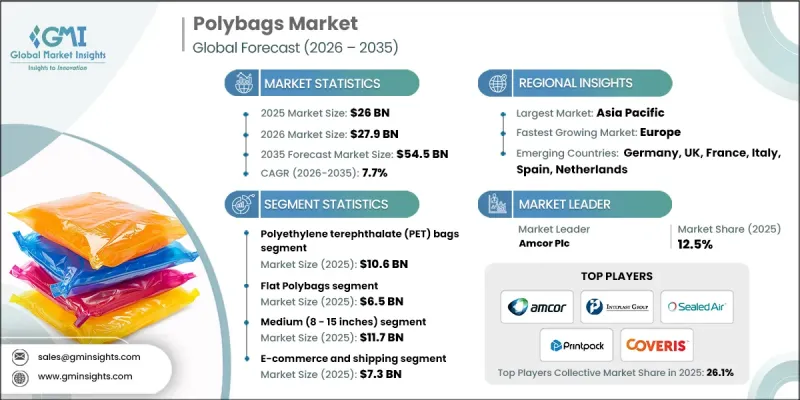

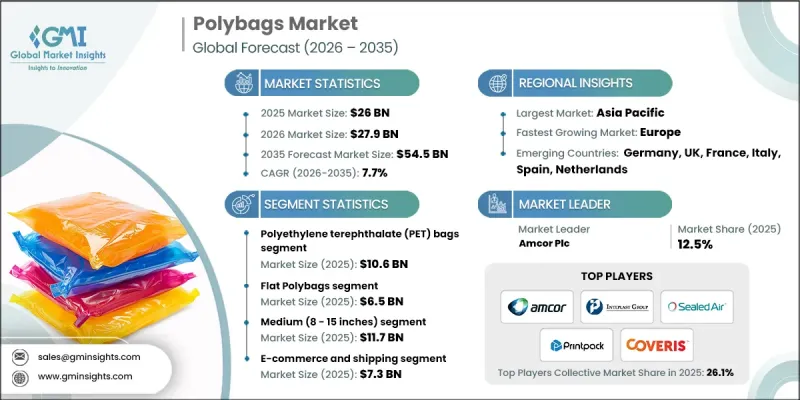

세계의 폴리백 시장은 2025년에 260억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.7%로 성장하여 545억 달러에 이를 것으로 예측되고 있습니다.

폴리백은 주로 폴리에틸렌으로 만들어지며, 가정부터 산업까지 폭넓게 사용되는 다용도의 연포장 솔루션입니다. 상품의 보관, 운송, 보호에 활용되며, 가볍고 내구성이 뛰어나며 비용 효율성이 뛰어나 높은 인기를 얻고 있습니다. 투명 유형과 컬러 유형이 있으며, LDPE(저밀도 폴리에틸렌), HDPE(고밀도 폴리에틸렌), LLDPE(선형 저밀도 폴리에틸렌) 등의 폴리머를 사용하여 제조됩니다. 강도, 두께, 유연성은 재료의 품질에 따라 결정됩니다. 고급 압출 및 블로우 성형 기술이 생산 공정의 주류이며, 자외선 저항성, 인쇄 품질 및 기계 내구성을 향상시키기 위해 첨가제를 첨가하는 것이 일반적입니다. 이러한 기술 표준을 통해 균일한 성능과 신뢰성을 보장합니다. 폴리백은 식품, 소비재, 의류 포장에 사용되며 습기, 먼지, 물리적 손상에 대한 장벽 기능을 제공합니다. 저비용, 편리성, 폭넓은 적용성이 세계 시장 확대를 지속적으로 견인하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 260억 달러 |

| 예측 금액 | 545억 달러 |

| CAGR | 7.7% |

폴리에틸렌 테레프탈레이트(PET) 가방 부문은 2025년 106억 달러를 차지했습니다. 높은 인장 강도, 투명성, 신축 및 수축에 대한 내성으로 유명한 PET 봉투는 내구성과 시각적으로 매력적인 포장을 필요로 하는 산업에서 선호되고 있습니다. 특히 소매업 및 식품 산업에서 냉장 및 냉동 식품 등의 용도로 인기가 있습니다. 다른 유형의 폴리백에는 복합재, 라미네이트, 생분해성 플라스틱 또는 특정 산업의 성능 요구 사항을 충족하도록 설계된 특수 필름 등이 있습니다.

중형 비닐봉지(8-15인치)는 2025년 117억 달러 시장 규모를 기록하여 가장 큰 점유율을 차지했습니다. 균형 잡힌 크기는 소비재, 서류, 의류, 식품 포장에 적합합니다. 중간 정도의 크기는 취급의 편의성을 유지하면서 충분한 용량을 제공하기 때문에 소매 후 유통, 물류, 전자상거래 용도에 특히 적합합니다.

미국 비닐봉지 시장은 2025년 59억 달러에 달했습니다. 소매, 전자상거래, 식품 포장 분야의 견조한 성장과 함께 일회용 플라스틱 사용을 줄이기 위한 규제가 수요를 견인하고 있습니다. 지속가능성에 대한 노력은 특히 2차 및 3차 포장재에서 재활용, 재사용, 바이오 비닐봉지로의 전환을 촉진하고 있습니다. 물류 및 의류 포장의 높은 소비는 국내 수요를 강화하는 한편, 주정부 차원의 플라스틱 백 금지 및 세금 부과로 인해 제조업체는 퇴비화 가능하고 친환경적인 대안을 개발하도록 장려하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 재료별, 2022-2035

제6장 시장 추산 및 예측 : 제품별, 2022-2035

제7장 시장 추산 및 예측 : 사이즈별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.16The Global Polybags Market was valued at USD 26 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 54.5 billion by 2035.

Polybags, primarily made from polyethylene, are versatile, flexible packaging solutions widely used across households and industries for the storage, transport, and protection of goods. Their lightweight, durable, and cost-effective nature makes them highly popular. Available in both transparent and colored variants, polybags are manufactured using polymers such as LDPE, HDPE, and LLDPE, with strength, thickness, and flexibility determined by material quality. Advanced extrusion and blowing techniques dominate manufacturing processes, often supplemented with additives to improve UV resistance, print quality, and machine durability. These technical standards ensure uniform performance and reliability. Polybags are used for packaging food, consumer products, and apparel, offering a barrier against moisture, dust, and physical damage. Their low cost, convenience, and wide applicability continue to drive market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26 Billion |

| Forecast Value | $54.5 Billion |

| CAGR | 7.7% |

The polyethylene terephthalate (PET) bags segment accounted for USD 10.6 billion in 2025. Known for high tensile strength, clarity, and resistance to stretching and shrinking, PET bags are favored in industries requiring durable and visually appealing packaging. They are particularly popular in retail and food sectors for applications including refrigerated and frozen goods. Other types of polybags include composite materials, laminates, biodegradable plastics, or specialty films designed to meet specific performance requirements in certain industries.

The medium-sized polybags, measuring 8 to 15 inches, generated USD 11.7 billion in 2025 and held the largest market share. Their balanced size makes them ideal for packaging consumer products, documents, apparel, and food items. The medium dimensions allow for convenient handling while offering sufficient capacity, making them especially suitable for post-retail, logistics, and e-commerce applications.

U.S. Polybags Market reached USD 5.9 billion in 2025. Demand is fueled by strong growth in retail, e-commerce, and food packaging sectors, alongside regulations aimed at reducing single-use plastics. Sustainability initiatives have prompted a shift toward recyclable, reusable, and biobased polybags, particularly in secondary and tertiary packaging. High consumption in logistics and apparel packaging reinforces domestic demand, while state-level bans and taxes on plastic bags push manufacturers to innovate with compostable and environmentally friendly alternatives.

Major companies operating in the Global Polybags Market include Novolex, Sealed Air Corporation, Winpak Ltd., Inteplast Group, A-Pac Manufacturing Co., Inc., Coveris AG, Huhtamaki Group, Printpack, Inc., Amcor Plc, PPC Flex, and Arihant Packers. Leading players in the polybags market focus on innovation, sustainability, and market expansion to strengthen their presence. Companies are investing in R&D to develop recyclable, biodegradable, and reusable packaging options that meet regulatory and consumer demands. Advanced material technologies enhance durability, flexibility, and print quality to differentiate products. Strategic partnerships with retailers and e-commerce platforms expand distribution networks, while competitive pricing supports adoption across diverse markets. Sustainability initiatives, branding, and marketing campaigns emphasize environmental responsibility and building consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material

- 2.2.2 Product

- 2.2.3 Size

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from packaging industry

- 3.2.1.2 Expansion of e-commerce and logistics

- 3.2.1.3 Low manufacturing and material cost

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Recycling infrastructure limitations

- 3.2.2.2 Volatility in raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Development of biodegradable polybags

- 3.2.3.2 Technological advancements in manufacturing

- 3.2.3.3 Customization and branding demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE) bags

- 5.3 Polypropylene (PP) bags

- 5.4 Polyethylene Terephthalate (PET) bags

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Flat polybags

- 6.3 Gusseted polybags

- 6.4 Ziplock polybags

- 6.5 Wicketed polybags

- 6.6 Poly mailers

- 6.7 Bubble mailers

- 6.8 Other polybags

Chapter 7 Market Estimates and Forecast, By Size, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Small (Below 8 Inches)

- 7.3 Medium (8 - 15 Inches)

- 7.4 Large (Above 15 Inches)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Retail and packaging

- 8.2.1 Small (Below 8 Inches)

- 8.2.2 Medium (8 - 15 Inches)

- 8.2.3 Large (Above 15 Inches)

- 8.3 Food packaging

- 8.3.1 Small (Below 8 Inches)

- 8.3.2 Medium (8 - 15 Inches)

- 8.3.3 Large (Above 15 Inches)

- 8.4 Medical and healthcare

- 8.4.1 Small (Below 8 Inches)

- 8.4.2 Medium (8 - 15 Inches)

- 8.4.3 Large (Above 15 Inches)

- 8.5 Industrial and manufacturing

- 8.5.1 Small (Below 8 Inches)

- 8.5.2 Medium (8 - 15 Inches)

- 8.5.3 Large (Above 15 Inches)

- 8.6 Agriculture

- 8.6.1 Small (Below 8 Inches)

- 8.6.2 Medium (8 - 15 Inches)

- 8.6.3 Large (Above 15 Inches)

- 8.7 E-commerce and Shipping

- 8.7.1 Small (Below 8 Inches)

- 8.7.2 Medium (8 - 15 Inches)

- 8.7.3 Large (Above 15 Inches)

- 8.8 Others

- 8.8.1 Small (Below 8 Inches)

- 8.8.2 Medium (8 - 15 Inches)

- 8.8.3 Large (Above 15 Inches)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Amcor Plc

- 10.2 Sealed Air Corporation

- 10.3 Novolex

- 10.4 Coveris AG

- 10.5 Inteplast Group

- 10.6 Huhtamaki Group

- 10.7 Printpack, Inc.

- 10.8 Winpak Ltd.

- 10.9 A-Pac Manufacturing Co., Inc.

- 10.10 Arihant Packers

- 10.11 PPC Flex