|

시장보고서

상품코드

1959634

풍력 터빈 피치 및 요 구동장치 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Wind Turbine Pitch and Yaw Drive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

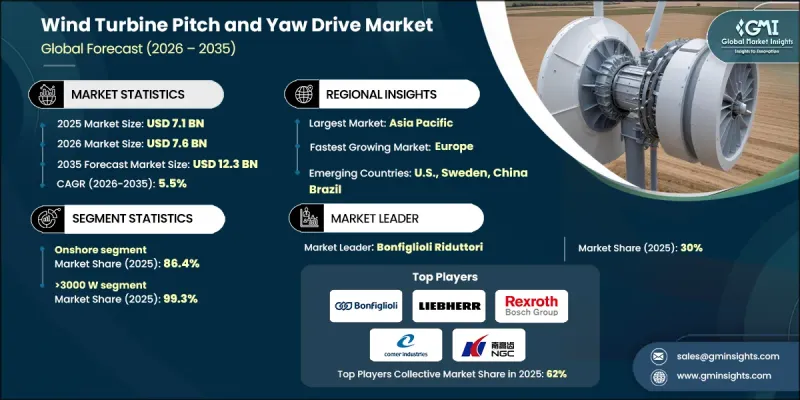

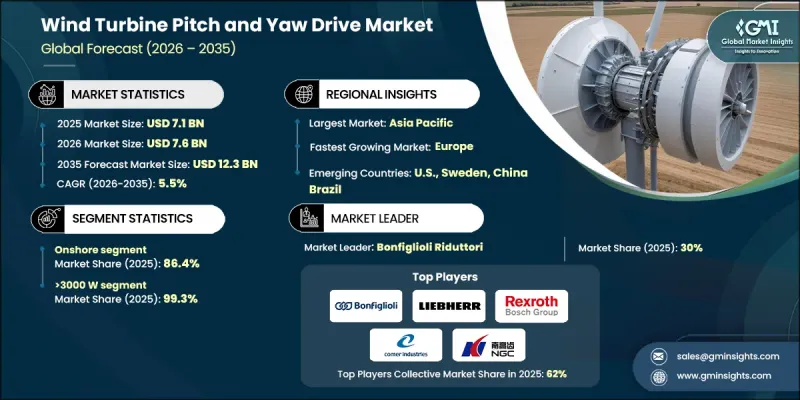

세계의 풍력 터빈 피치 및 요 구동장치 시장은 2025년에 71억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.5%로 성장하여 123억 달러에 이를 것으로 예측됩니다.

이 시장 전망은 풍력 터빈의 성능과 안전에서 이러한 시스템이 수행하는 중요한 역할과 밀접한 관련이 있습니다. 피치 구동 시스템은 변화하는 풍속에 따라 블레이드의 각도를 조정하는 데 사용되어 터빈이 효율적으로 작동할 수 있도록 하는 동시에 과도한 기계적 부하를 방지하고 필요에 따라 제어된 정지를 가능하게 합니다. 요 구동 시스템은 터빈이 바람의 흐름에 따라 적절한 방향을 유지하여 일관된 에너지 출력을 지원하고 구조물의 피로를 줄여줍니다. 재생에너지 도입과 배출량 감축 목표에 대한 전 세계적인 노력 증가는 시장의 모멘텀을 더욱 강화시키고 있습니다. 풍력 발전은 여전히 가장 비용 효율적인 재생에너지 솔루션 중 하나이며, 터빈의 효율성, 내구성 및 자동화의 지속적인 개선으로 장기적인 도입 전망이 강화되고 있습니다. 재료, 제어 기술 및 제조 정밀도의 발전으로 시스템의 신뢰성과 비용 효율성이 더욱 향상되어 전 세계 풍력 발전 설비에 대한 지속적인 수요를 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 71억 달러 |

| 예측 금액 | 123억 달러 |

| CAGR | 5.5% |

육상 설치 부문은 2025년 86.4%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 4.5%의 성장률을 보일 것으로 전망됩니다. 이러한 장점은 낮은 설치 및 유지보수 비용, 확립된 공급 네트워크, 확장 가능한 생산 능력에 의해 뒷받침됩니다. 블레이드 길이와 타워 높이를 연장한 대형 터빈의 지속적인 개발로 에너지 포집 효율이 향상되고, 고부하에 대응하고 긴 수명을 보장할 수 있는 견고한 피치-요 시스템에 대한 수요가 증가하고 있습니다.

1000W-3000W 용량 부문은 2035년까지 연평균 복합 성장률(CAGR) 9%를 나타낼 것으로 예측됩니다. 이 범위의 성장은 노후화된 터빈 그룹의 갱신, 송전망 및 설치 공간이 제한된 지역에 대한 적응성, 개발도상국 시장에서의 도입 확대와 관련이 있습니다. 이 카테고리의 시스템은 일반적으로 성숙한 기술 플랫폼과 검증된 공급망에 의해 뒷받침되는 액티브 피치 요(Active Pitch-Yaw) 메커니즘을 채택하여 비용 효율적인 도입을 지원합니다.

북미의 풍력 터빈 피치 및 요 구동 장치 시장은 2025년 14.8%의 점유율을 차지할 것으로 예측됩니다. 이 지역 시장은 터빈 효율을 높이고 도입 가능성을 확대하기 위한 지속적인 기술 연구와 혁신의 혜택을 누리고 있습니다. 캐나다는 지역 내에서 규모는 작지만 꾸준히 성장하고 있는 기여국입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 최종 용도별, 2022-2035

제6장 시장 규모와 예측 : 유형별, 2022-2035

제7장 시장 규모와 예측 : 피치 시스템별, 2022-2035

제8장 시장 규모와 예측 : 블레이드 장별, 2022-2035

제9장 시장 규모와 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.16The Global Wind Turbine Pitch and Yaw Drive Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 12.3 billion by 2035.

The market outlook is tied to the critical role these systems play in wind turbine performance and safety. Pitch drive systems are used to adjust blade angles in response to changing wind speeds, allowing turbines to operate efficiently while preventing excessive mechanical loads and enabling controlled shutdowns when required. Yaw drive systems ensure that turbines remain properly oriented toward wind flow, supporting consistent energy output and reducing structural fatigue. Growing global commitment to renewable energy adoption and emission reduction targets continues to reinforce market momentum. Wind power remains one of the most cost-effective renewable solutions, and ongoing improvements in turbine efficiency, durability, and automation are strengthening long-term deployment prospects. Advancements in materials, control technologies, and manufacturing precision are further improving system reliability and cost efficiency, driving sustained demand across global wind installations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $12.3 Billion |

| CAGR | 5.5% |

The onshore installations segment accounted for 86.4% share in 2025 and is expected to grow at a CAGR of 4.5% from 2026 to 2035. This dominance is supported by lower installation and servicing expenses, established supply networks, and scalable production capabilities. Continued development of larger turbines with extended blade lengths and increased tower heights has improved energy capture, driving the need for robust pitch and yaw systems capable of handling higher loads and ensuring long operational lifespans.

The 1000 W to 3000 W capacity segment is projected to grow at a CAGR of 9% through 2035. Growth in this range is linked to the modernization of aging turbine fleets, suitability for regions with grid or space limitations, and increasing deployment across developing markets. Systems within this category commonly utilize active pitch and yaw mechanisms supported by mature technology platforms and proven supply chains, supporting cost-effective adoption.

North America Wind Turbine Pitch and Yaw Drive Market accounted for 14.8% share in 2025. The regional market benefits from ongoing technological research and innovation aimed at improving turbine efficiency and expanding deployment feasibility. Canada represents a smaller yet steadily expanding contributor within the regional landscape.

Key companies operating in the Global Wind Turbine Pitch and Yaw Drive Market include Siemens Gamesa Renewable Energy, Vestas Wind Systems, General Electric, ABB, Bosch Rexroth, Bonfiglioli, Schaeffler Group, Nordex, Nidec Conversion, Mitsubishi Heavy Industries, Liebherr, Goldwind Science and Technologies, ZOLLERN GmbH, Dana SAC UK, Nabtesco Corporation, KEBA, Comer Industries, ABM Greiffenberger, SIPCO-MLS, and Nanjing High Speed Gear Manufacturing. Companies in the wind turbine pitch and yaw drive market are strengthening their competitive positions through continuous innovation and system optimization. Many players are investing in advanced control technologies and durable materials to enhance performance and reduce lifecycle costs. Strategic partnerships with turbine manufacturers and energy developers are being used to secure long-term supply agreements. Firms are also expanding manufacturing footprints and local service capabilities to improve responsiveness and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.2 Mathematical impact of growth parameters on forecast

- 1.3.2 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 End Use trends

- 2.4 Type trends

- 2.5 Pitch System trends

- 2.6 Blade Length trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.5.1 By type

- 3.5.2 By region

- 3.6 Cost structure analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Onshore

- 5.3 Offshore

Chapter 6 Market Size and Forecast, By Type, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 <1000 W

- 6.3 1000 W - 3000 W

- 6.4 >3000 W

Chapter 7 Market Size and Forecast, By Pitch System, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Electric

- 7.3 Mechanical

- 7.4 Hydraulic

Chapter 8 Market Size and Forecast, By Blade Length, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Small

- 8.3 Medium

- 8.4 Large

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Spain

- 9.3.3 UK

- 9.3.4 France

- 9.3.5 Italy

- 9.3.6 Sweden

- 9.3.7 Poland

- 9.3.8 Denmark

- 9.3.9 Portugal

- 9.3.10 Netherlands

- 9.3.11 Ireland

- 9.3.12 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Australia

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Vietnam

- 9.4.7 Thailand

- 9.4.8 Philippines

- 9.4.9 Taiwan

- 9.5 Middle East & Africa

- 9.5.1 South Africa

- 9.5.2 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Chile

- 9.6.3 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 ABM Greiffenberger

- 10.3 Bosch Rexroth AG

- 10.4 Bonfiglioli S.p.A

- 10.5 Comer Industries

- 10.6 Dana SAC UK

- 10.7 General Electric

- 10.8 Goldwind Science and Technologies

- 10.9 KEBA

- 10.10 Liebherr

- 10.11 Mitsubishi Heavy Industries

- 10.12 Nabtesco Corporation

- 10.13 Nanjing High Speed Gear Manufacturing

- 10.14 Nidec Conversion

- 10.15 Nordex

- 10.16 SIPCO-MLS

- 10.17 Siemens Gamesa Renewable Energy

- 10.18 Schaeffler Group

- 10.19 Vestas Wind Systems

- 10.20 ZOLLERN GmbH