|

시장보고서

상품코드

2011932

풍력 터빈용 복합재료 시장 예측(-2030년) : 섬유 유형별, 수지 유형별, 제조 프로세스별, 컴포넌트별, 용도별, 지역별Wind Turbine Composites Market by Fiber Type (Glass, Carbon), Resin Type (Epoxy, Polyurethane), Manufacturing Process, Component (Blades, Nacelles), Application (Onshore, Offshore) and Region - Global Forecast to 2030 |

||||||

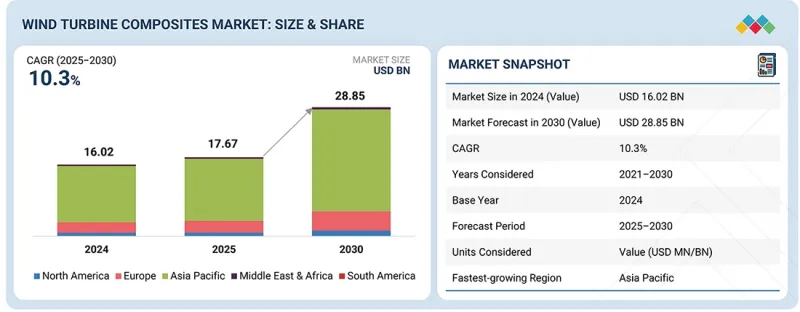

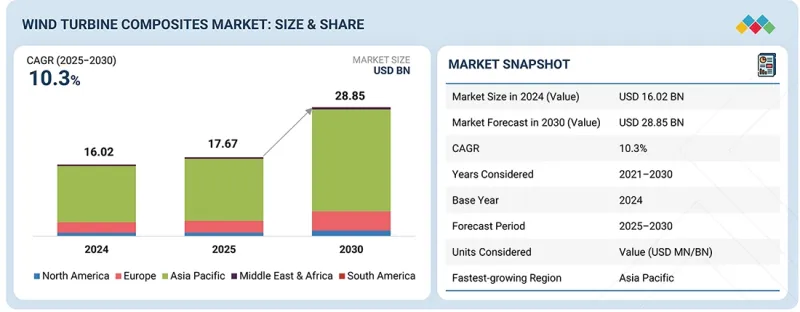

세계의 풍력 터빈용 복합재료 시장 규모는 2025년 176억 7,000만 달러로 추정되며, 예측기간(CAGR) 동안 10.3%의 성장률을 기록하여, 2030년에는 288억 5,000만 달러에 달할 것으로 예측됩니다.

재생 에너지로의 세계적인 전환 추세와 더불어 더욱 크고 성능이 뛰어난 터빈에 대한 수요 증가가 풍력 터빈 복합재 시장의 성장을 견인하고 있습니다. 제조업체들이 저풍속 조건에서도 에너지를 포착하기 위해 사용하는 더욱 길고 공기역학적인 블레이드 개발에는 최적의 강도 대비 무게 성능을 제공하는 소재가 필요합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만/10억 달러 |

| 부문 | 섬유 유형, 수지 유형, 제조 프로세스, 컴포넌트, 용도 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

유리섬유와 탄소섬유 강화 폴리머의 조합은 터빈이 큰 기계적 하중을 견디면서 터빈 구동계와 타워 지지 구조물의 경량화를 실현하는 데 필수적인 재료 특성을 제공합니다. 해상 풍력발전소의 존재감이 확대되고, 가동 기간 중 구조적 무결성을 유지하면서 터빈의 유지보수 비용을 절감하기 위해 이러한 재료의 채택이 빠르게 증가하고 있습니다.

"금액 기준으로는 에폭시 수지가 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. "

에폭시 수지는 기계적 특성으로 인해 대형 터빈 블레이드를 지지할 수 있으므로 풍력 터빈용 복합재료 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 에폭시 수지가 시장을 주도하고 있는 것은 제조업체들이 진공 함침 공법(VARTM)으로 전환하고 있기 때문입니다. 이 공정에서는 가볍고 고성능의 제품을 생산하기 위해 에폭시 수지 특유의 저수축성과 강한 접착력이 요구됩니다. 해상 풍력발전 설비에 대한 수요 증가와 재활용 가능한 에폭시 수지 시스템의 개발은 강력한 성장 궤도를 가져오고 있습니다.

"금액 기준으로는 육상 풍력 터빈 부문이 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 보입니다. "

육상 풍력발전 용도는 주로 전 세계적인 보급과 해상 설비에 비해 높은 비용 효율성으로 인해 풍력 터빈용 복합재료 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 육상 풍력발전은 이미 구축된 공급망과 간단한 설치 방법의 혜택을 받아 빠르게 확장할 수 있는 반면, 해상 풍력발전은 잠재력을 최대한 발휘하기까지 시간이 걸립니다. 이 분야가 견고한 성장세를 유지하고 있는 이유는 업계가 기존 터빈을 첨단 복합소재 블레이드로 지속적으로 업데이트하여 저풍속에서도 보다 효율적인 에너지 회수를 가능하게 하고 있기 때문입니다.

"금액 기준으로는 유럽이 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 보입니다. "

유럽은 풍력 터빈용 복합재료 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 이는 이 지역이 광범위한 해상풍력 프로젝트를 시행하고 있을 뿐만 아니라, 2030년까지 재생에너지 기술 채택률을 40%로 의무화하는 NZIA(Net Zero Industry Act)를 통해 엄격한 집행 메커니즘을 구축하고 있기 때문입니다. 이 지역의 성장은 성숙한 연구개발(R&D) 생태계에 의해 더욱 가속화되고 있습니다. 이 생태계는 유럽의 지속가능성 기준에 부합하는 완전 재활용 가능한 블레이드 연구를 통해 순환 경제 프로그램을 구축하고 있습니다. 또한 노후화된 풍력발전소를 더 크고 고효율의 터빈으로 교체하는 현재의 추세는 에너지 효율을 향상시키는 첨단 탄소섬유 및 유리섬유 복합재료에 대한 수요를 촉진하고 있습니다.

세계의 풍력 터빈용 복합재료 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 채택에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 풍력 터빈용 복합재료 시장 : 수지 유형별

제10장 풍력 터빈용 복합재료 시장 : 섬유 유형별

제11장 풍력 터빈용 복합재료 시장 : 제조 프로세스별

제12장 풍력 터빈용 복합재료 시장 : 컴포넌트별

제13장 풍력 터빈용 복합재료 시장 : 용도별

제14장 풍력 터빈용 복합재료 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.05.04The wind turbine composites market is estimated at USD 17.67 billion in 2025 and is projected to reach USD 28.85 billion by 2030, at a CAGR of 10.3% during the forecast period. The global transition to renewable energy sources, together with the rising need for bigger and better-performing turbines, leads to increased growth in the wind turbine composites market. The development of longer and more aerodynamic blades, which manufacturers use to capture energy from low wind conditions, needs materials that deliver optimal strength-to-weight performance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Fiber Type, Resin Type, Manufacturing Process, Component, Application |

| Regions covered | Europe, North America, Asia Pacific, the Middle East & Africa, and South America |

The combination of glass fiber and carbon fiber reinforced polymers delivers essential material properties that enable turbines to withstand high mechanical loads while keeping their weight low for turbine drivetrain and tower support. The adoption of these materials has grown faster because offshore wind farms have expanded their presence to maintain structural integrity while decreasing turbine maintenance expenses throughout their operational time.

"In terms of value, epoxy resin is expected to register the second-highest CAGR during the forecast period."

The epoxy resin type is expected to witness the second-highest CAGR in the wind turbine composites market, as its mechanical properties enable it to sustain larger turbine blades. Epoxy maintains market leadership because manufacturers are transitioning to vacuum-assisted resin infusion (VARTM), which requires epoxy's low shrinkage and strong adhesion properties to create lightweight, high-performance products. The growing demand for offshore wind installations and the development of recyclable epoxy systems provide a strong growth trajectory.

"In terms of value, the onshore wind turbine segment is expected to register the second-highest CAGR during the forecast period."

The onshore application is expected to register the second-highest CAGR in the wind turbine composites market, primarily due to its extensive global adoption and cost-efficiency compared to offshore installations. Onshore wind power benefits from established supply chains and straightforward installation methods, which enable rapid expansion, whereas offshore wind power requires time to reach its full potential. The established segment maintains strong growth because the industry keeps updating existing turbines with advanced composite blades, which enable better energy capture at decreased wind speeds.

"In terms of value, Europe is expected to register the second-highest CAGR during the forecast period."

The Europe region is expected to record the second-highest CAGR in the wind turbine composites market, because the region has implemented extensive offshore wind projects and established strict enforcement mechanisms through the Net Zero Industry Act (NZIA), which mandates 40% renewable energy technology adoption by 2030. The region's growth is further accelerated by a mature R&D ecosystem, which establishes circular economy programs through its research on fully recyclable blades that comply with European sustainability standards. The current trend of replacing old wind farms with bigger, more efficient turbines drives the demand for advanced carbon and glass fiber composites, which improve energy efficiency.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

- By Designation: C-level - 33%, Director-level - 33%, and Managers - 34%

- By Region: North America - 15%, Europe - 25%, Asia Pacific - 30%, the Middle East & Africa - 20%, and South America - 10%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market are China Jushi Co., Ltd. (China), DowAksa (Turkey), Teijin Limited (Japan), SGL Carbon (Germany), Hexcel Corporation (US), Gurit Services AG (Switzerland), China National Building Material Group Corporation (China), Toray Industries, Inc. (Japan), Rochling SE & Co. KG (Germany), Exel Composites (Finland), Evonik (Germany), Arkema (France), Owens Corning (US), ExxonMobil Corporation (US), and Huntsman International LLC (US).

Research Coverage

This research report categorizes the wind turbine composites market by fiber type (glass fiber, carbon fiber), resin type (epoxy, polyurethane), manufacturing process (VARTM/VI, filament winding), component (blades, nacelles), application (onshore wind turbines, offshore wind turbines), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the wind turbine composites market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, and recent developments in the wind turbine composites market. This report includes a competitive analysis of upcoming startups in the wind turbine composites market ecosystem.

Reasons to buy this report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall wind turbine composites market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increasing installations of new wind turbines), restraints (higher raw material costs), opportunities (frequent cable re-penetration and airflow management, expansion of offshore wind projects), and challenges (high capital investments) are influencing the growth of the wind turbine composites market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the wind turbine composites market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the wind turbine composites market across varied regions

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the wind turbine composites market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like China Jushi Co., Ltd. (China), DowAksa (Turkey), Teijin Limited (Japan), SGL Carbon (Germany), Hexcel Corporation (US), Gurit Services AG (Switzerland), China National Building Material Group Corporation (China), Toray Industries, Inc. (Japan), Rochling SE & Co. KG (Germany), Exel Composites (Finland), Evonik (Germany), Arkema (France), Owens Corning (US), ExxonMobil Corporation (US), and Huntsman International LLC (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WIND TURBINE COMPOSITES MARKET

- 3.2 WIND TURBINE COMPOSITES MARKET, BY APPLICATION AND REGION

- 3.3 WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 3.4 WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 3.5 WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 3.6 WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 3.7 WIND TURBINE COMPOSITES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing installations of new wind turbines

- 4.2.1.2 Technological advancements in blade design

- 4.2.1.3 Government incentives and policies boosting wind installations

- 4.2.2 RESTRAINTS

- 4.2.2.1 Higher raw material costs

- 4.2.2.2 Limited blade recycling technology

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of recyclable resin

- 4.2.3.2 Expansion of offshore wind projects

- 4.2.4 CHALLENGES

- 4.2.4.1 Geopolitical instability

- 4.2.4.2 High capital investments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN WIND TURBINE COMPOSITES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL WIND ENERGY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 7019)

- 5.6.2 EXPORT SCENARIO (HS CODE 7019)

- 5.6.3 IMPORT SCENARIO (HS CODE 681511)

- 5.6.4 EXPORT SCENARIO (HS CODE 681511)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 FIBERGLASS BLADES BOOST WIND TURBINE PERFORMANCE FOR BERGEY WINDPOWER

- 5.10.2 QUANTUM'S RESIN INFUSION TRANSFORMS WIND TURBINE COMPONENTS

- 5.10.3 CARBON FIBER REINFORCED PLASTIC SPAR CAPS: BOOSTING RIGIDITY IN MEGA WIND BLADES

- 5.11 IMPACT OF 2025 US TARIFF ON WIND TURBINE COMPOSITES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 VACUUM ASSISTED RESIN TRANSFER MOLDING (VARTM)

- 6.1.2 FILAMENT WINDING

- 6.1.3 PULTRUSION

- 6.1.4 PREPREG MOLDING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED FIBER PLACEMENT (AFP)

- 6.2.2 ADDITIVE MANUFACTURING (3D PRINTING)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 LIST OF PATENTS BY GEN ELECTRIC

- 6.5 FUTURE APPLICATIONS

- 6.5.1 FLOATING WIND FARMS: ADVANCED LIGHTWEIGHT COMPOSITE BLADES AND STRUCTURES FOR DEEP-WATER INSTALLATIONS

- 6.5.2 ULTRA-LARGE ROTOR SYSTEMS: HIGH-STRENGTH COMPOSITES ENABLING >100M BLADES FOR HIGHER ENERGY YIELD

- 6.5.3 RECYCLABLE BLADE TECHNOLOGIES: SUSTAINABLE THERMOPLASTIC AND BIO-BASED COMPOSITE SOLUTIONS

- 6.5.4 OFFSHORE HARSH ENVIRONMENTS: CORROSION-RESISTANT COMPOSITE STRUCTURES FOR EXTENDED TURBINE LIFESPAN

- 6.5.5 HYBRID MATERIAL SYSTEMS: INTEGRATION OF CARBON AND GLASS FIBER COMPOSITES FOR OPTIMIZED PERFORMANCE

- 6.6 IMPACT OF AI/GEN AI ON WIND TURBINE COMPOSITES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN WIND TURBINE COMPOSITES PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN WIND TURBINE COMPOSITES MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN WIND TURBINE COMPOSITES MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 SIEMENS GAMESA: AI-DRIVEN MANUFACTURING & QUALITY ASSURANCE

- 6.7.2 VESTAS: DIGITAL TWIN INTEGRATION FOR STRUCTURAL HEALTH

- 6.7.3 LM WIND POWER: GENERATIVE DESIGN & CIRCULAR ECONOMY

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF WIND TURBINE COMPOSITES

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF WIND TURBINE COMPOSITES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 9.1 INTRODUCTION

- 9.2 EPOXY

- 9.2.1 EXCELLENT ADHESION AND RESISTANCE TO FATIGUE TO DRIVE DEMAND

- 9.3 POLYURETHANE

- 9.3.1 LOW VISCOSITY AND COST EFFICIENCY TO DRIVE DEMAND

- 9.4 OTHER RESIN TYPES

10 WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 10.1 INTRODUCTION

- 10.2 GLASS FIBER

- 10.2.1 HIGH PERFORMANCE AND COST-EFFECTIVENESS TO DRIVE MARKET

- 10.3 CARBON FIBER

- 10.3.1 HIGH TENSILE STRENGTH AND LIGHTWEIGHT PROPERTIES TO FUEL DEMAND

- 10.4 OTHER FIBER TYPES

11 WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 11.1 INTRODUCTION

- 11.2 VARTM/VI

- 11.2.1 LIGHTWEIGHT STRUCTURES AND MINIMUM WASTE TO FUEL DEMAND

- 11.3 FILAMENT WINDING

- 11.3.1 HIGH FIBER VOLUME FRACTIONS AND REDUCED WASTE TO DRIVE DEMAND

- 11.4 OTHER MANUFACTURING PROCESSES

12 WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 12.1 INTRODUCTION

- 12.2 BLADES

- 12.2.1 ADVANCED MATERIAL DYNAMICS AND STRUCTURAL SCALING TO DRIVE MARKET

- 12.3 NACELLES

- 12.3.1 ENHANCED STRUCTURAL INTEGRITY AND CORROSION RESISTANCE TO DRIVE DEMAND

- 12.4 OTHER COMPONENTS

13 WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 ONSHORE WIND TURBINES

- 13.2.1 SCALING ONSHORE CAPACITY AND REPOWERING STRATEGIES TO DRIVE MARKET

- 13.3 OFFSHORE WIND TURBINES

- 13.3.1 STRUCTURAL DEMANDS OF NEXT-GENERATION TURBINES TO DRIVE DEMAND

14 WIND TURBINE COMPOSITES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 14.2.2 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 14.2.3 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 14.2.4 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 14.2.5 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 14.2.6 NORTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY COUNTRY

- 14.2.6.1 US

- 14.2.6.1.1 Presence of major manufacturers with surge in offshore wind activity to drive market

- 14.2.6.2 Canada

- 14.2.6.2.1 Advancements in composite material technologies and greater demand for sustainable energy solutions to drive market

- 14.2.6.3 Mexico

- 14.2.6.3.1 Established manufacturing infrastructure and proximity to major wind energy markets to support investment

- 14.2.6.1 US

- 14.3 EUROPE

- 14.3.1 EUROPE: WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 14.3.2 EUROPE: WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 14.3.3 EUROPE: WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 14.3.4 EUROPE: WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 14.3.5 EUROPE: WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 14.3.6 EUROPE: WIND TURBINE COMPOSITES MARKET, BY COUNTRY

- 14.3.6.1 Germany

- 14.3.6.1.1 Growing shift toward circular economy goals to drive market

- 14.3.6.2 France

- 14.3.6.2.1 Rise in composite demand driven by new fixed-bottom and floating offshore projects in France

- 14.3.6.3 Sweden

- 14.3.6.3.1 Increase in shift toward recycling of wind blades to support market growth

- 14.3.6.4 Spain

- 14.3.6.4.1 Growing turbine scale driving composite demand

- 14.3.6.5 Finland

- 14.3.6.5.1 Bio-based resins and recycling breakthroughs to drive market

- 14.3.6.6 Netherlands

- 14.3.6.6.1 Policy-driven offshore growth accelerating composite demand

- 14.3.6.7 UK

- 14.3.6.7.1 Investments in more efficient turbines and clean energy projects to drive market

- 14.3.6.8 Rest of Europe

- 14.3.6.1 Germany

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 14.4.2 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 14.4.3 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 14.4.4 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 14.4.5 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 14.4.6 ASIA PACIFIC: WIND TURBINE COMPOSITES MARKET, BY COUNTRY

- 14.4.6.1 China

- 14.4.6.1.1 High renewable energy production and investments in both onshore and offshore wind projects to drive demand

- 14.4.6.2 India

- 14.4.6.2.1 Rising investments in wind power projects to propel market

- 14.4.6.3 Japan

- 14.4.6.3.1 Strong renewable energy push and policy support to drive market

- 14.4.6.4 Australia

- 14.4.6.4.1 Increase in shift toward renewable energy to drive market

- 14.4.6.5 South Korea

- 14.4.6.5.1 Expansion of wind power projects and innovation in composite materials to drive market

- 14.4.6.6 Rest of Asia Pacific

- 14.4.6.1 China

- 14.5 SOUTH AMERICA

- 14.5.1 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 14.5.2 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 14.5.3 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 14.5.4 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 14.5.5 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 14.5.6 SOUTH AMERICA: WIND TURBINE COMPOSITES MARKET, BY COUNTRY

- 14.5.6.1 Brazil

- 14.5.6.1.1 Rapid expansion of wind energy capacity and government-backed policies supporting domestic manufacturing to drive market

- 14.5.6.2 Argentina

- 14.5.6.2.1 Increased onshore wind capacity, supportive policies, and high potential to drive growth

- 14.5.6.3 Rest of South America

- 14.5.6.1 Brazil

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY FIBER TYPE

- 14.6.2 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY RESIN TYPE

- 14.6.3 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY MANUFACTURING PROCESS

- 14.6.4 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY COMPONENT

- 14.6.5 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY APPLICATION

- 14.6.6 MIDDLE EAST & AFRICA: WIND TURBINE COMPOSITES MARKET, BY COUNTRY

- 14.6.6.1 Egypt

- 14.6.6.1.1 Ongoing investments in wind energy infrastructure for electricity generation from large-scale projects in Gulf regions to drive market

- 14.6.6.2 Morocco

- 14.6.6.2.1 Rising wind installations with ambitious renewable energy goals to drive market

- 14.6.6.3 Rest of Middle East & Africa

- 14.6.6.1 Egypt

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS

- 15.4 MARKET SHARE ANALYSIS

- 15.4.1 TORAY INDUSTRIES, INC.:

- 15.4.2 EXXONMOBIL CORPORATION:

- 15.4.3 EVONIK:

- 15.4.4 CHINA JUSHI CO., LTD.:

- 15.4.5 CHINA NATIONAL BUILDING MATERIAL GROUP CORPORATION:

- 15.5 BRAND/PRODUCT COMPARISON

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Fiber type footprint

- 15.6.5.4 Resin type footprint

- 15.6.5.5 Manufacturing process footprint

- 15.6.5.6 Component footprint

- 15.6.5.7 Application footprint

- 15.6.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.6.7 PROGRESSIVE COMPANIES

- 15.6.8 RESPONSIVE COMPANIES

- 15.6.9 DYNAMIC COMPANIES

- 15.6.10 STARTING BLOCKS

- 15.6.11 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.6.11.1 Detailed list of key startups/SMEs

- 15.6.11.2 Competitive benchmarking of key startups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 COMPETITIVE SCENARIO

- 15.8.1 PRODUCT LAUNCHES

- 15.8.2 DEALS

- 15.8.3 EXPANSIONS

- 15.8.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 GURIT SERVICES AG

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 CHINA NATIONAL BUILDING MATERIAL GROUP CORPORATION

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 MnM view

- 16.1.2.3.1 Key strengths

- 16.1.2.3.2 Strategic choices

- 16.1.2.3.3 Weaknesses and competitive threats

- 16.1.3 HEXCEL CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 MnM view

- 16.1.3.3.1 Key strengths

- 16.1.3.3.2 Strategic choices

- 16.1.3.3.3 Weaknesses and competitive threats

- 16.1.4 TORAY INDUSTRIES, INC.

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 MnM view

- 16.1.4.3.1 Key strengths

- 16.1.4.3.2 Strategic choices

- 16.1.4.3.3 Weaknesses and competitive threats

- 16.1.5 CHINA JUSHI CO., LTD.

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Expansions

- 16.1.5.3.2 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 ROCHLING SE & CO. KG

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 MnM view

- 16.1.6.3.1 Key strengths

- 16.1.6.3.2 Strategic choices

- 16.1.6.3.3 Weaknesses and competitive threats

- 16.1.7 SGL CARBON

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Expansions

- 16.1.7.4 MnM view

- 16.1.7.4.1 Key strengths

- 16.1.7.4.2 Strategic choices

- 16.1.7.4.3 Weaknesses and competitive threats

- 16.1.8 DOWAKSA

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.3.2 Expansions

- 16.1.8.4 MnM view

- 16.1.8.4.1 Key strengths

- 16.1.8.4.2 Strategic choices

- 16.1.8.4.3 Weaknesses and competitive threats

- 16.1.9 EXEL COMPOSITES

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Other developments

- 16.1.9.4 MnM view

- 16.1.9.4.1 Key strengths

- 16.1.9.4.2 Strategic choices

- 16.1.9.4.3 Weaknesses and competitive threats

- 16.1.10 EVONIK

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 MnM view

- 16.1.10.3.1 Key strengths

- 16.1.10.3.2 Strategic choices

- 16.1.10.3.3 Weaknesses and competitive threats

- 16.1.11 ARKEMA

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Other developments

- 16.1.11.4 MnM view

- 16.1.11.4.1 Key strengths

- 16.1.11.4.2 Strategic choices

- 16.1.11.4.3 Weaknesses and competitive threats

- 16.1.12 TEIJIN LIMITED

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 MnM view

- 16.1.12.3.1 Key strengths

- 16.1.12.3.2 Strategic choices

- 16.1.12.3.3 Weaknesses and competitive threats

- 16.1.13 OWENS CORNING

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 MnM view

- 16.1.13.3.1 Key strengths

- 16.1.13.3.2 Strategic choices

- 16.1.13.3.3 Weaknesses and competitive threats

- 16.1.14 EXXONMOBIL CORPORATION

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.14.4 MnM view

- 16.1.14.4.1 Key strengths

- 16.1.14.4.2 Strategic choices

- 16.1.14.4.3 Weaknesses and competitive threats

- 16.1.15 HUNTSMAN INTERNATIONAL LLC

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product launches

- 16.1.15.4 MnM view

- 16.1.15.4.1 Key strengths

- 16.1.15.4.2 Strategic choices

- 16.1.15.4.3 Weaknesses and competitive threats

- 16.1.1 GURIT SERVICES AG

- 16.2 OTHER PLAYERS

- 16.2.1 PULTREX

- 16.2.2 EPSILON COMPOSITE

- 16.2.3 AERON COMPOSITE LIMITED

- 16.2.4 WESTLAKE CORPORATION

- 16.2.5 ELAN COMPOSITES

- 16.2.6 NORTHERN LIGHT COMPOSITES

- 16.2.7 JIUDING NEW MATERIAL CO., LTD.

- 16.2.8 HS HYOSUNG ADVANCED MATERIALS

- 16.2.9 INDORE COMPOSITE

- 16.2.10 RELIANCE INDUSTRIES LTD.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key primary interview participants

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 BASE NUMBER CALCULATION

- 17.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 17.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 17.4 MARKET FORECAST APPROACH

- 17.4.1 SUPPLY SIDE

- 17.4.2 DEMAND SIDE

- 17.5 DATA TRIANGULATION

- 17.6 FACTOR ANALYSIS

- 17.7 RESEARCH ASSUMPTIONS

- 17.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS