|

시장보고서

상품코드

1982293

자동차 긴급 출동 서비스 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Vehicle Roadside Assistance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

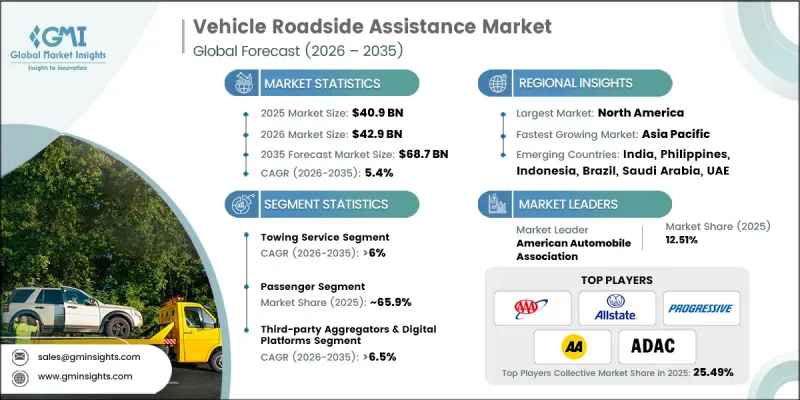

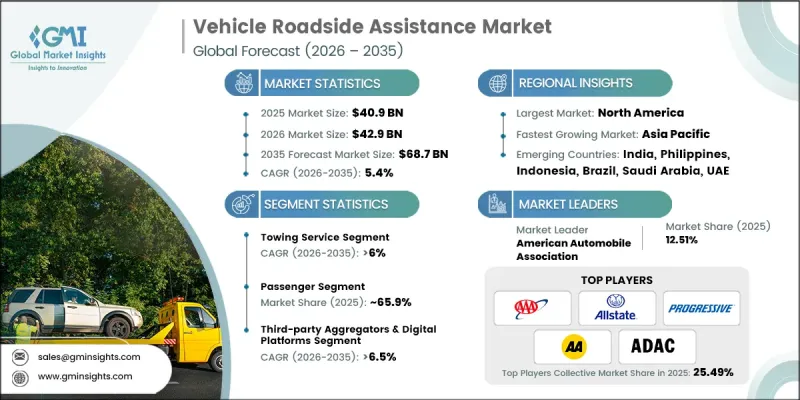

세계의 자동차 긴급 출동 서비스 시장은 2025년 409억 달러로 평가되었고, CAGR은 5.4%를 나타낼 것으로 보이며, 2035년까지 687억 달러에 이를 것으로 추정됩니다.

세계의 자동차 보유 대수 증가, 교통 체증 심각화, 현대 자동차의 기술적 진보에 따라 차량 긴급 출동 서비스(VRA) 업계는 큰 변화를 겪고 있습니다. 자동차 긴급 출동 서비스는 더 이상 단순한 고장 주도에 국한되지 않으며, 이제는 운전자의 안전을 보장하고 차량 가동 중지 시간을 최소화하며 서비스 연속성을 유지하기 위해 설계된 포괄적인 모빌리티 지원 네트워크로 운영되고 있습니다. 신뢰성과 편의성에 대한 기대가 높아짐에 따라 자동차 긴급 출동 서비스는 보험 패키지, OEM 보증 프로그램, 차량 관리 솔루션 및 구독형 모빌리티 서비스의 필수 컴포넌트로 자리 잡고 있습니다. 커넥티드 카 기술과 디지털 플랫폼의 통합이 확대됨에 따라 지원 서비스 제공 방식도 변화하고 있습니다. 차량 시스템이 점점 더 복잡해짐에 따라, 전문적인 자동차 긴급 출동 서비스는 개인 운전자와 상업용 차량 운영자 모두에게 없어서는 안 될 필수 요소가 되고 있으며, 이는 선진국과 신흥 경제국 전반에 걸친 장기적인 시장 확장을 뒷받침하고 있습니다

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 409억 달러 |

| 예측 금액 | 687억 달러 |

| CAGR | 5.4% |

현대의 자동차 긴급 출동 서비스 플랫폼은 기술 중심의 다기능입니다. 주도, 배터리 지원, 타이어 교체, 연료 공급, 잠금 해제 지원, 경미한 기계적 수리 등의 서비스는 이제 GPS 기반 출동 도구, 텔레매틱스 연결성, 예측 진단 및 모바일 애플리케이션의 지원을 받습니다. 서비스 제산업체들은 대응 시간을 단축하고, 디지털 청구 처리를 간소화하며, 실시간 차량 추적 기능을 도입하여 운영 효율성과 고객 만족도를 높이고 있습니다. 보험사, 자동차 제조사, 텔레매틱스 기업, 독립 서비스 제산업체 및 디지털 모빌리티 플랫폼 간의 협력이 강화되고 있습니다. 구독형 보장 모델, 보험 부가 상품, 사용량 기반 서비스, 앱 기반 온디맨드 솔루션은 차량 자동차 긴급 출동 서비스 시장 내 수익 모델과 서비스 접근성을 재정의하고 있습니다.

주도 서비스 부문은 2025년 시장 점유율의 33%를 차지했으며, 2035년까지 연평균 성장률(CAGR) 6%로 성장할 것으로 전망됩니다. 주도 서비스는 여전히 차량 소유주와 차량 관리자들이 가장 자주 요청하는 자동차 긴급 출동 서비스입니다. 수요는 승용차와 상용차 전반에 걸쳐 있으며, 도시 및 고속도로 네트워크 전반에서 고장 복구, 사고 대응, 장거리 운송 요구를 충족시킵니다. 주도 서비스의 필수적인 특성은 업계 내 지배적인 위치를 공고히 하는 기반이 되고 있습니다.

승용차 부문은 2025년 65.9%의 점유율을 기록했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 4.2%로 성장할 것으로 전망됩니다. 높은 개인 차량 보유율, 도시 인구 증가, 빠르고 신뢰할 수 있는 자동차 긴급 출동 서비스 서비스에 대한 의존도 증대가 이 부문의 성장을 주도하고 있습니다. 승용차는 다양한 자동차 긴급 출동 서비스에 대한 상당한 수요를 창출합니다. 디지털 플랫폼과 커넥티드 차량 시스템의 도입은 개별 운전자에게 더 빠른 출동, 개선된 통신, 향상된 사용자 경험을 제공합니다.

북미의 차량 긴급 출동 서비스 시장은 2025년에 33.5%의 점유율을 차지하고 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 나타낼 것으로 예측됩니다. 높은 차량 소유율, 광범위한 보험 보급률, 커넥티드 및 전기차의 급속한 확산이 이 지역의 성장에 주요 요인으로 작용하고 있습니다. 기존 자동차 클럽, OEM 지원 프로그램, 디지털 온디맨드 지원 플랫폼의 존재는 광범위한 서비스 커버리지를 보장합니다. 또한 물류 업체와 상업용 차량 운용사는 가동 중단 시간을 줄이고 운영 효율성을 유지하기 위해 통합 자동차 긴급 출동 솔루션에 점점 더 의존하고 있어, 지역 시장 성과를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 자동차 보유 대수 증가

- 보험 연계 자동차 긴급 출동 서비스 증가

- 커넥티드 카 및 OEM 프로그램의 급증

- 도시화 및 도로 안전 의식 고취

- 업계의 잠재적 위험 및 과제

- 신흥 시장의 낮은 보급률

- 서비스 중복으로 인한 증분 수익 감소

- 시장 기회

- 전기자동차(EV)용 서비스 증가

- 상업용 차량 증가 및 공유 모빌리티

- 디지털 및 애그리게이터 플랫폼의 확장

- 신흥 시장 자동차 보유 대수 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 연방자동차운송안전국(FMCSA)의 긴급 출동 서비스 및 긴급 서비스 가이드라인

- 미국 도로 교통 안전국(NHTSA)의 차량 안전 리콜 및 지원 프로그램

- 유럽

- EU 긴급 출동 서비스 지령(2006/126/EC)

- 독일 : 도로 교통 차량 등록 규칙(StVZO)에 근거한 자동차 긴급 출동 서비스의 규정 준수

- 영국 : 로드사이드 복구 및 차량 지원에 관한 규제

- 프랑스 : 도로 교통법- 차량 고장시의 긴급 출동 서비스

- 아시아태평양

- 중국 : 도로 교통 안전법- 자동차 긴급 출동 서비스 가이드라인

- 일본 : 도로 운송 차량법- 자동차 긴급 출동 서비스에 관한 규제

- 한국 : 자동차 관리법 - 자동차 긴급 출동 서비스에 관한 규정

- 싱가포르 : 도로 교통법- 차량 고장 및 자동차 긴급 출동 서비스

- 라틴아메리카

- 브라질 : ANTT의 자동차 긴급 출동 서비스 규제

- 멕시코 : 연방 도로 안전 및 차량 지원에 관한 기준

- 칠레 : 도로 운송 안전 및 지원에 관한 지침

- 중동 및 아프리카

- UAE : 연방운송국의 긴급 출동 서비스 및 긴급 서비스에 관한 정책

- 사우디아라비아 : 비전 2030-차량 자동차 긴급 출동 서비스의 틀

- 남아프리카 : 국가 도로 교통법 - 자동차 긴급 출동 서비스에 관한 규제

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 가격 분석과 비용 구조

- 서비스 유형별 평균 가격

- 구독 모델과 종량 과금 모델의 비교

- 비용 구조 내역 : 인건비, 연료비, 보험료

- 지역별 가격 변동

- 비용 상승의 동향과 영향

- 지속가능성 및 환경영향 분석

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 향후 전망과 기회

- 지속가능성 및 환경영향 분석

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 향후 전망과 기회

- 서비스 레벨 계약(SLA)과 성과 지표

- 업계 표준 SLA 벤치마크

- 서비스 유형별 평균 응답 시간

- 첫회 해결율

- 고객 만족도 점수(CSAT) 지표

- 넷 프로모터 스코어(NPS)의 벤치마크

- 단위 경제성 및 수익성의 벤치마크

- 서비스 콜당 평균 수익

- 서비스 이벤트당 비용

- 서비스 유형별 공헌 이익

- 고객 획득 비용(CAC)

- 고객 생애 가치(LTV)

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 서비스별(2022-2035년)

- 주도 서비스

- 타이어 교체 서비스

- 배터리 지원 서비스

- 연료 공급 서비스

- 잠금 해제 지원, 경미한 기계적 수리

- 윈칭 및 주도 서비스

- 기타

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 세단

- SUV 및 크로스오버

- 해치백

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제7장 시장 추계 및 예측 : 서비스 채널별(2022-2035년)

- OEM 네트워크

- 보험사의 네트워크

- 독립 서비스 제산업체

- 타사 어그리게이터 및 디지털 플랫폼

제8장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 개인/소매 고객

- 상업용 차량 사업자

- 자동차 판매점

- 렌탈 및 리스 회사

- 기타

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Automobile Association(AA)

- Agero

- Allianz Global Assistance

- Allstate Insurance

- American Automobile Association(AAA)

- AXA Assistance USA

- Europ Assistance

- GEICO

- Liberty Mutual Insurance

- Nationwide

- Progressive Insurance

- RAC Limited

- Travelers Insurance

- 지역 기업

- ADAC

- Better World Club

- Japan Automobile Federation(JAF)

- RACE

- 신흥 기업

- ARC

- Five Star Roadside

- HONK Technologies

The Global Vehicle Roadside Assistance Market was valued at USD 40.9 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 68.7 billion by 2035.

The vehicle roadside assistance (VRA) industry is undergoing significant evolution as global vehicle ownership rises, traffic congestion intensifies, and modern vehicles become more technologically advanced. Roadside assistance is no longer limited to basic breakdown towing; it now operates as a comprehensive mobility support network designed to ensure driver safety, minimize vehicle downtime, and maintain service continuity. Growing expectations for reliability and convenience are positioning roadside assistance as an essential component of insurance packages, OEM warranty programs, fleet management solutions, and subscription-based mobility services. Increasing integration of connected vehicle technologies and digital platforms is reshaping how assistance is delivered. As vehicle systems become more complex, professional roadside support services are becoming indispensable to both individual drivers and commercial fleet operators, supporting long-term market expansion across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.9 Billion |

| Forecast Value | $68.7 Billion |

| CAGR | 5.4% |

Modern vehicle roadside assistance platforms are technology-driven and multi-functional. Services such as towing, battery support, tire replacement, fuel delivery, lockout assistance, and minor mechanical repairs are now supported by GPS-enabled dispatch tools, telematics connectivity, predictive diagnostics, and mobile applications. Providers are improving response times, streamlining digital claims processing, and enabling real-time vehicle tracking to enhance operational efficiency and customer satisfaction. Collaboration among insurers, automotive manufacturers, telematics firms, independent service providers, and digital mobility platforms is intensifying. Subscription-based coverage models, insurance add-ons, usage-based services, and app-enabled on-demand solutions are redefining revenue models and service accessibility within the vehicle roadside assistance market.

The towing services segment accounted for 33% share in 2025 and is projected to grow at a CAGR of 6% through 2035. Towing remains the most frequently requested roadside service among vehicle owners and fleet managers. Demand spans across personal and commercial vehicles, addressing breakdown recovery, accident response, and long-distance transport needs across urban and highway networks. The essential nature of towing services continues to anchor its dominant position within the industry.

The passenger vehicle segment held 65.9% share in 2025 and is anticipated to grow at a CAGR of 4.2% between 2026 and 2035. High levels of private vehicle ownership, expanding urban populations, and increased dependence on fast and reliable emergency assistance services are driving this segment's growth. Passenger vehicles generate substantial demand for a wide range of roadside support services. The adoption of digital platforms and connected vehicle systems enables quicker dispatch, improved communication, and enhanced user experience for individual motorists.

North America Vehicle Roadside Assistance Market accounted for 33.5% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. Strong vehicle ownership rates, widespread insurance penetration, and rapid adoption of connected and electric vehicles are key contributors to regional growth. The presence of established automotive clubs, OEM-supported programs, and digital on-demand assistance platforms ensures extensive service coverage. Additionally, logistics providers and commercial fleets increasingly rely on integrated roadside assistance solutions to reduce downtime and maintain operational efficiency, further strengthening regional market performance.

Major companies operating in the Global Vehicle Roadside Assistance Market include American Automobile Association, Allianz, Allstate, GEICO, Progressive, ADAC, Automobile Association, Japan Automobile Federation (JAF), Better World Club, and RACE. Companies in the Vehicle Roadside Assistance Market are reinforcing their competitive position through digital transformation and strategic partnerships. Leading providers are investing in telematics integration, AI-powered dispatch systems, and mobile application platforms to enhance response speed and service transparency. Collaboration with insurance companies, automotive OEMs, and fleet operators is expanding bundled service offerings and subscription-based coverage models. Firms are also focusing on data analytics to predict service demand and optimize resource allocation. Expansion into electric vehicle support services and specialized fleet solutions is creating new revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Service

- 2.2.4 Service Channel

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global vehicle ownership

- 3.2.1.2 Increase in insurance-bundled roadside assistance

- 3.2.1.3 Surge in connected cars and OEM programs

- 3.2.1.4 Growth in urbanization and road safety awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low penetration in emerging markets

- 3.2.2.2 Overlap in coverage reducing incremental revenue

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in electric vehicle (EV) specific services

- 3.2.3.2 Growth in commercial fleets and shared mobility

- 3.2.3.3 Expansion of digital and aggregator platforms

- 3.2.3.4 Increase in vehicle ownership in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Motor Carrier Safety Administration (FMCSA) Roadside Assistance & Emergency Service Guidelines

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) Vehicle Safety Recall & Assistance Programs.

- 3.4.2 Europe

- 3.4.2.1 EU Roadside Assistance Directive (2006/126/EC)

- 3.4.2.2 Germany: Straßenverkehrs-Zulassungs-Ordnung (StVZO) Emergency Assistance Compliance

- 3.4.2.3 UK: Roadside Recovery & Vehicle Assistance Regulations

- 3.4.2.4 France: Code de la Route - Vehicle Breakdown Assistance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Road Traffic Safety Law - Roadside Assistance Guidelines

- 3.4.3.2 Japan: Road Transport Vehicle Act - Roadside Service Regulations

- 3.4.3.3 South Korea: Motor Vehicle Management Act - Emergency Assistance Provisions

- 3.4.3.4 Singapore: Road Traffic Act - Vehicle Breakdown & Roadside Support

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTT Roadside Assistance Regulations

- 3.4.4.2 Mexico: Federal Road Safety & Vehicle Assistance Norms

- 3.4.4.3 Chile: Road Transport Safety & Assistance Guidelines

- 3.4.5 MEA

- 3.4.5.1 UAE: Federal Transport Authority Roadside Assistance & Emergency Services Policy

- 3.4.5.2 Saudi Arabia: Vision 2030 - Vehicle Roadside Support Framework

- 3.4.5.3 South Africa: National Road Traffic Act - Roadside Assistance Regulations

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Pricing analysis & cost structure

- 3.9.1 Average service pricing by type

- 3.9.2 Subscription vs. pay-per-use models

- 3.9.3 Cost structure breakdown: labor, fuel, insurance

- 3.9.4 Regional price variations

- 3.9.5 Cost inflation trends & impact

- 3.10 Sustainability and environmental impact analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook & opportunities

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Service level agreement (SLA) & performance metrics

- 3.14.1 Industry-standard SLA benchmarks

- 3.14.2 Average response time by service type

- 3.14.3 First-call resolution rates

- 3.14.4 Customer Satisfaction Score (CSAT) metrics

- 3.14.5 Net Promoter Score (NPS) benchmarking

- 3.15 Unit Economics & Profitability Benchmarking

- 3.15.1 Average revenue per service call

- 3.15.2 Cost per service event

- 3.15.3 Contribution margin by service type

- 3.15.4 Customer acquisition cost (CAC)

- 3.15.5 Customer lifetime value (LTV)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Towing Services

- 5.3 Tire Replacement Services

- 5.4 Battery Assistance Services

- 5.5 Fuel Delivery Services

- 5.6 Lockout & Replacement Key Services

- 5.7 Winching & Extraction Services

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger Cars

- 6.2.1 Sedans

- 6.2.2 SUVs & Crossovers

- 6.2.3 Hatchbacks

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Medium Commercial Vehicles (MCVs)

- 6.3.3 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Service Channel, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 OEM Networks

- 7.3 Insurance Company Networks

- 7.4 Independent Service Providers

- 7.5 Third-Party Aggregators & Digital Platforms

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Individual/Retail Customers

- 8.3 Commercial Fleet Operators

- 8.4 Automotive Dealerships

- 8.5 Rental & Leasing Companies

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Automobile Association (AA)

- 10.1.2 Agero

- 10.1.3 Allianz Global Assistance

- 10.1.4 Allstate Insurance

- 10.1.5 American Automobile Association (AAA)

- 10.1.6 AXA Assistance USA

- 10.1.7 Europ Assistance

- 10.1.8 GEICO

- 10.1.9 Liberty Mutual Insurance

- 10.1.10 Nationwide

- 10.1.11 Progressive Insurance

- 10.1.12 RAC Limited

- 10.1.13 Travelers Insurance

- 10.2 Regional Players

- 10.2.1 ADAC

- 10.2.2 Better World Club

- 10.2.3 Japan Automobile Federation (JAF)

- 10.2.4 RACE

- 10.3 Emerging Players

- 10.3.1 ARC

- 10.3.2 Five Star Roadside

- 10.3.3 HONK Technologies