|

시장보고서

상품코드

1982306

유동 화학 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Flow Chemistry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

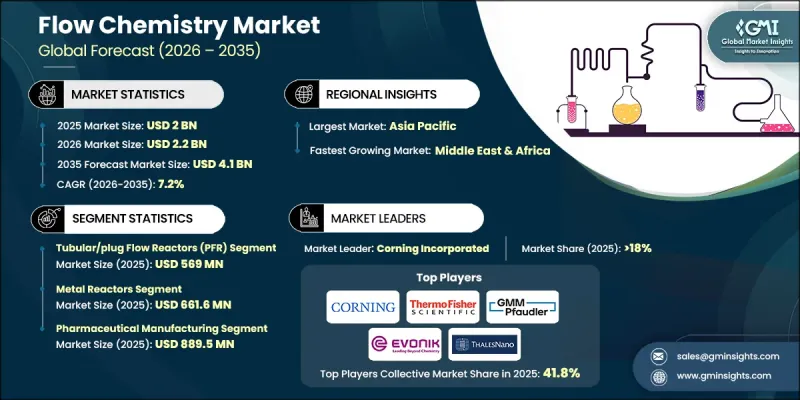

세계의 유동 화학 시장은 2025년 20억 달러로 평가되었고 CAGR은 7.2%를 나타낼 것으로 보이며, 2035년까지 41억 달러에 이를 것으로 추정됩니다.

제약 업계에서 연속 제조로의 전환이 가속화되면서 시장 확대에 크게 기여하고 있습니다. 미국 FDA와 같은 규제 기관들은 제품 품질 개선, 공정 제어 강화, 생산 기간 단축이 가능하다는 점을 근거로 연속 공정을 적극 장려하고 있습니다. 유동 화학은 고반응성 중간체를 안전하게 취급할 수 있게 해주며, 실시간 모니터링을 지원함으로써 ‘품질 설계(Quality by Design)’ 원칙 및 첨단 공정 최적화와 부합합니다. 제약 제조사들이 생산 시설을 현대화함에 따라 유동 기반 시스템에 대한 수요는 지속적으로 증가하고 있습니다. 지속 가능하고 친환경적인 화학 관행에 대한 강조가 커짐에 따라 도입 속도는 더욱 가속화되고 있습니다. 연속 유동 공정은 기존 배치 방식에 비해 용매 소비량이 적고, 폐기물 발생량이 적으며, 일반적으로 에너지 소비도 적습니다. 강화되는 환경 규제와 글로벌 지속 가능성 이니셔티브는 제조업체들이 더 깨끗한 생산 기술로 전환하도록 장려하고 있습니다. 유동 화학은 환경적 영향을 최소화하면서 반응을 보다 정밀하게 제어할 수 있게 함으로써 이러한 목표를 뒷받침합니다. 마이크로 반응기 공학 및 모듈형 유동 플랫폼의 발전 또한 확장성, 유연성 및 운영 대응력을 향상시켜 시장을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 20억 달러 |

| 예측 금액 | 41억 달러 |

| CAGR | 7.2% |

관형/플러그 흐름 반응기(PFR) 부문은 2025년 5억 6,900만 달러에 달했습니다. 반응기 유형별 세분화는 제조업체들이 적응성, 확장성, 운영 성능 간의 균형을 맞추고자 함에 따라 화학 공정 전략의 명확한 변화를 반영합니다. 배치 반응기는 다양한 제품 라인을 처리할 수 있는 다용도성과 중소 규모 생산에서 정밀한 제어가 가능하다는 점 덕분에 여전히 높은 채택률을 유지하고 있습니다. 그러나 화학 공학 기술의 발전과 더불어 더욱 엄격해진 안전 및 환경 규제로 인해 기업들은 기존의 배치 구성 방식을 재검토하고 있습니다. 이러한 전환은 높은 열전달 요구 사항이나 유해한 중간체가 포함된 공정에서 특히 두드러지는데, 이러한 경우 연속식 시스템이 종종 향상된 제어 및 안전상의 이점을 제공합니다.

금속 반응기 부문은 2025년 6억 6,160만 달러 시장 규모를 기록했습니다. 산업계가 특정 화학 용도 및 연속 공정 요구 사항에 맞춤화된 시스템을 도입함에 따라 반응기 선정의 전문화가 심화되고 있습니다. 관형/플러그 흐름 반응기(PFR)와 연속 교반 탱크 반응기(CSTR)는 운영 신뢰성과 확장성 덕분에 여전히 널리 선호되고 있습니다. 촉매 용도에서는 촉매 상호작용과 전반적인 반응 효율을 향상시키기 때문에 충전층 및 고정층 반응기가 산업계에서 더욱 널리 수용되고 있습니다. 동시에, 미세 구조 반응기는 소형 구성으로 뛰어난 열 및 물질 전달 성능을 제공하여 정밀하게 제어되는 합성 공정을 지원함에 따라 연구계의 관심이 점점 더 높아지고 있습니다.

북미의 유동 화학 시장은 2025년 2억 9,950만 달러 규모에 이르렀습니다. 이 지역의 성장은 제약, 특수 화학, 생명공학 부문 전반에 걸친 연속 제조의 확대 도입에 힘입고 있습니다. 미국은 공정 혁신에 대한 상당한 투자, 첨단 합성 기술의 광범위한 채택, 그리고 연구 기관 및 계약 개발 및 제조 기관(CDMO)의 강력한 네트워크를 바탕으로 이 지역에서 압도적인 점유율을 차지하고 있습니다. 제조업체들은 특히 복잡하고 고위험인 화학 공정에서 반응 효율을 높이고, 운영 안전성을 강화하며, 규제 준수를 보장하기 위해 유동 화학 기술을 점점 더 많이 활용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 제약 업계에서 연속 제조 도입 확대

- 친환경 및 지속 가능한 화학에 대한 강력한 추진

- 마이크로 리액터 및 모듈식 시스템의 기술 발전

- 업계의 잠재적 위험 및 과제

- 높은 초기 자본 투자

- 기존 인프라와의 통합 문제

- 시장 기회

- 광화학이나 전기화학 등의 새로운 용도 확대

- 맞춤형, 모듈형 및 스키드 장착 시스템에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형

- 장래 시장 동향

- 기술 및 혁신의 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 동향

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경 배려형 이니셔티브

- 탄소발자국에 관한 고찰

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 반응기 유형별(2022-2035년)

- 관형/플러그 흐름 반응기(PFR)

- 미세구조 반응기

- 충전층/고정층 반응기

- 연속 교반 탱크 반응기(CSTR)

- 광화학 유동 반응기

- 전기화학 유동 반응기

- 진동 반응기(OFR)

- 하이브리드 및 통합 시스템

- 기타

제6장 시장 추계 및 예측 : 재료 유형별(2022-2035년)

- 폴리머 기반 반응기

- 금속 반응기

- 유리/석영 기반 반응기

- 세라믹/실리콘 반응기

- 기타 재료

제7장 시장 추계 및 예측 : 용도별(2022-2035년)

- 의약품

- 정밀 화학 생산

- 석유화학 가공

- 농약 제조

- 기타

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Thermo Fisher Scientific

- Xylem Inc.

- Alfa Laval AB

- SPX Technologies Inc.

- Sulzer Ltd.

- Corning Incorporated

- Syrris Ltd.

- Vapourtec Ltd.

- Chemtrix BV

- Evonik

- Zibo Taiji Industrial Enamel Co.,Ltd

- GMM Pfaudler

The Global Flow Chemistry Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 4.1 billion by 2035.

The rising shift toward continuous manufacturing in the pharmaceutical sector is significantly contributing to market expansion. Regulatory bodies such as the U.S. FDA actively encourage continuous processing due to its ability to improve product quality, enhance process control, and shorten production timelines. Flow chemistry enables the safe handling of highly reactive intermediates while supporting real-time monitoring, aligning with Quality by Design principles and advanced process optimization. As pharmaceutical manufacturers modernize production facilities, demand for flow-based systems continues to grow. Growing emphasis on sustainable and green chemistry practices is further accelerating adoption. Continuous flow processes consume less solvent, generate lower waste volumes, and typically require reduced energy compared to conventional batch operations. Increasing environmental regulations and global sustainability initiatives are encouraging manufacturers to transition toward cleaner production technologies. Flow chemistry supports these objectives by enabling more controlled reactions with minimized environmental impact. Advancements in microreactor engineering and modular flow platforms are also strengthening the market by improving scalability, flexibility, and operational responsiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 7.2% |

The tubular or plug flow reactors (PFR) segment reached USD 569 million in 2025. Segmentation by reactor type reflects a clear shift in chemical processing strategies, as manufacturers aim to balance adaptability, scalability, and operational performance. Batch reactors continue to maintain strong adoption due to their versatility in handling multiple product lines and enabling precise control in small- to mid-scale production. However, advancements in chemical engineering technologies, along with more rigorous safety and environmental regulations, are prompting companies to reassess traditional batch configurations. This transition is particularly evident in processes involving high heat transfer demands or hazardous intermediates, where continuous systems often provide enhanced control and safety advantages.

The metal reactors segment captured USD 661.6 million in 2025. Increasing specialization in reactor selection is evident as industries adopt systems tailored to specific chemical applications and continuous processing requirements. Tubular or plug flow reactors (PFR) and continuous stirred-tank reactors (CSTR) remain widely preferred due to their operational reliability and scalability. In catalytic applications, packed-bed and fixed-bed reactors are gaining stronger industry acceptance because they improve catalyst interaction and overall reaction efficiency. At the same time, microstructured reactors are drawing growing research attention, as their compact configurations enable superior heat and mass transfer performance, supporting highly controlled and precise synthesis processes.

North America Flow Chemistry Market generated USD 299.5 million in 2025. The region's expansion is driven by the growing implementation of continuous manufacturing across pharmaceuticals, specialty chemicals, and biotechnology sectors. The United States holds the dominant regional share, supported by significant investments in process innovation, widespread adoption of advanced synthesis technologies, and a strong network of research institutions and contract development and manufacturing organizations. Manufacturers are increasingly leveraging flow chemistry to improve reaction efficiency, enhance operational safety, and ensure regulatory compliance, particularly in complex and high-risk chemical processes.

Key participants in the Global Flow Chemistry Market include Evonik, Corning Incorporated, GMM Pfaudler, Thermo Fisher Scientific, Sulzer Ltd., Vapourtec Ltd., Zibo Taiji Industrial Enamel Co. Ltd, Syrris Ltd., SPX Technologies Inc., Chemtrix BV, Xylem Inc., and Alfa Laval AB. Companies operating in the Global Flow Chemistry Market are implementing strategic initiatives to strengthen their competitive positioning and expand their global footprint. Major players are investing in advanced reactor technologies, modular system design, and digital process integration to enhance efficiency and scalability. Strategic collaborations with pharmaceutical manufacturers and specialty chemical producers enable customized solutions and long-term supply agreements. Firms are also focusing on expanding production capabilities and regional distribution networks to improve market accessibility. Continuous investment in research and development supports innovation in microreactor platforms and automation technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Reactor Type

- 2.2.3 Material Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of continuous manufacturing in pharmaceuticals

- 3.2.1.2 Strong push for green and sustainable chemistry

- 3.2.1.3 Technological advancements in microreactors and modular systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment

- 3.2.2.2 Integration Issues with Legacy Infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Emerging Applications like Photochemistry & Electrochemistry

- 3.2.3.2 Growing Demand for Custom, Modular, and Skid Mounted Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Reactor Type, 2022 - 2035 (USD million) (Tons)

- 5.1 Key trends

- 5.2 Tubular/Plug Flow Reactors (PFR)

- 5.3 Microstructured Reactors

- 5.4 Packed-Bed/Fixed-Bed Reactors

- 5.5 Continuous Stirred-Tank Reactors (CSTR)

- 5.6 Photochemical Flow Reactors

- 5.7 Electrochemical Flow Reactors

- 5.8 Oscillatory Flow Reactors (OFR)

- 5.9 Hybrid & Integrated Systems

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD million) (Tons)

- 6.1 Key trends

- 6.2 Polymer-Based Reactors

- 6.3 Metal Reactors

- 6.4 Glass/Quartz Reactors

- 6.5 Ceramic/Silicon Reactors

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Tons)

- 7.1 Key trends

- 7.2 Pharmaceutical manufacturing

- 7.3 Fine chemicals production

- 7.4 Petrochemical processing

- 7.5 Agrochemical manufacturing

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Thermo Fisher Scientific

- 9.2 Xylem Inc.

- 9.3 Alfa Laval AB

- 9.4 SPX Technologies Inc.

- 9.5 Sulzer Ltd.

- 9.6 Corning Incorporated

- 9.7 Syrris Ltd.

- 9.8 Vapourtec Ltd.

- 9.9 Chemtrix BV

- 9.10 Evonik

- 9.11 Zibo Taiji Industrial Enamel Co.,Ltd

- 9.12 GMM Pfaudler