|

시장보고서

상품코드

1982359

상용 발전기 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Commercial Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

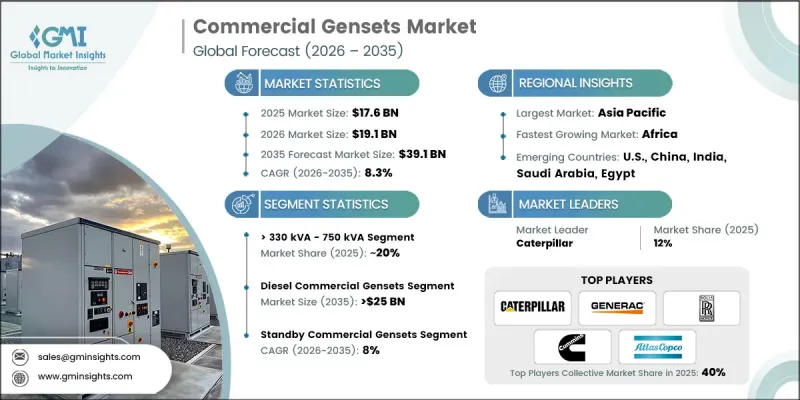

세계의 상용 발전기 시장은 2025년 176억 달러로 평가되었으며 CAGR 8.3%로 성장해 2035년까지 391억 달러에 이를 것으로 추정됩니다.

시장의 성장은 상업 인프라의 확대, 전기 수요 증가 및 사업 운영의 무정전화에 대한 요구 증가에 의해 견인되고 있습니다. 광범위한 산업 조직은 재무 손실을 피하고 중요한 장비를 보호하며 원활한 서비스 제공을 유지하기 위해 안정적인 백업 전원 시스템을 선호합니다. 상용 발전기는 신속한 시동, 유연한 용량 옵션 및 안정적인 성능을 제공하며 에너지 탄력성 전략의 필수 요소로 자리를 잡고 있습니다. 기업이 디지털 시스템, 보안 시스템 및 자동화된 업무에서 지속적인 전력 공급에 대한 의존도를 높이면서 고효율 발전기에 대한 수요는 계속 가속화되고 있습니다. 이러한 시스템은 송전망 공급이 불안정해지거나 이용할 수 없게 된 경우에도 안정된 전력을 공급하도록 설계되어 업무 환경에서의 업무의 연속성을 확보합니다. 설계, 지능형 제어 및 통합 모니터링 기술의 지속적인 발전이 경쟁 구도를 지속적으로 개선하고 있습니다. 현대 발전기는 자동화, 임베디드 센서, 데이터 구동 분석 기능을 탑재하여 성능 향상, 유지 보수 요구 사항 감소 및 가동 수명 연장을 실현합니다. 원격 진단 및 예측 유지 보수 기능은 장기적인 가치를 더욱 향상시키고 보다 광범위한 상업적 도입을 촉진합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 176억 달러 |

| 예측 금액 | 391억 달러 |

| CAGR | 8.3% |

50-125kVA 용량 부문은 2025년에 27억 달러 시장 규모를 기록했습니다. 이는 신뢰할 수 있는 예비 전원을 요구하는 중소기업의 강한 수요를 반영한 것입니다. 이 부문 시장 확대는 인프라의 현대화에 대한 노력과 에너지에 민감한 상업 환경에서 신뢰할 수 있는 전력 공급에 대한 요구에 의해 뒷받침됩니다. 산업 동향은 연료 효율 향상, 배출 가스 감소, 디지털 제어 시스템, 운영 최적화 및 지속가능성 향상을 위한 하이브리드 에너지 구성과의 통합을 포함합니다.

하이브리드 상용 발전기 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 10.5%를 나타낼 것으로 예측됩니다. 기업은 기존 발전기 기술과 축전지 또는 재생에너지 구성 요소를 결합한 저배출 백업 전원 시스템에 대한 투자를 점점 늘리고 있습니다. 이러한 통합 시스템은 연료 사용량을 줄이고 소음 수준을 최소화하며 운영 비용을 줄입니다. 환경 책임, 에너지 안보 및 지능형 전력 관리 솔루션에 대한 관심이 높아짐에 따라 현대적인 상업시설 전반에 걸쳐 도입이 가속화되고 있습니다.

2025년 시점에서 미국 상용 발전기 시장은 80%의 점유율을 차지하고 15억 달러 시장 규모를 기록했습니다. 상업개발 프로젝트와 분산 에너지 인프라에 대한 투자 증가는 미국 수요를 뒷받침하고 있습니다. 시장 진출기업은 고객 충성도를 높이고 경쟁력을 강화하기 위해 제품 혁신, 소음 감소 기술 및 종합적인 애프터 서비스 프로그램에 주력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 가용성 및 조달 분석

- 생산 능력 평가

- 공급망의 탄력성과 위험요인

- 유통 네트워크 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 규제 상황

- 성장 가능성 분석

- 가격 동향 분석(달러/유닛)

- 지역별

- 정격 출력별

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

- 상용 발전기의 비용 구조 분석

- 새로운 기회와 동향

- 디지털화와 IoT의 통합

- 미개척 시장 및 용도에서의 성장

- 투자 분석 및 미래 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동

- 아프리카

- 라틴아메리카

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 규모 및 예측 : 출력별(2022-2035년)

- 50kVA 이하

- 50-125kVA

- 125-200kVA

- 200-330kVA

- 330-750kVA

- 750kVA 초과

제6장 시장 규모 및 예측 : 연료별(2022-2035년)

- 디젤

- 가스

- 하이브리드

제7장 시장 규모 및 예측 : 최종 용도별(2022-2035년)

- 통신

- 헬스케어

- 데이터센터

- 교육기관

- 정부기관

- 접객

- 소매 판매

- 부동산

- 복합상업시설

- 인프라

- 기타

제8장 시장 규모 및 예측 : 용도별(2022-2035년)

- 대기

- 피크 셰이빙

- 프라임 및 연속

제9장 시장 규모 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 러시아

- 영국

- 독일

- 프랑스

- 스페인

- 오스트리아

- 이탈리아

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 필리핀

- 미얀마

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 튀르키예

- 이란

- 오만

- 아프리카

- 이집트

- 나이지리아

- 알제리

- 남아프리카

- 앙골라

- 모잠비크

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

제10장 기업 프로파일

- AB Volvo Penta

- AKSA POWER GENERATION

- Ashok Leyland

- Atlas Copco

- Briggs & Stratton

- Caterpillar

- Cummins

- Deere &Company

- Denyo Co.

- Generac Power Systems

- HIMOINSA

- HUU TOAN GROUP

- Kirloskar

- MAHINDRA POWEROL

- MITSUBISHI HEAVY INDUSTRIES

- Rolls-Royce

- Sudhir Group

- Wartsila

- Yamaha Motor Co.

- Yanmar Holdings Co.

The Global Commercial Gensets Market was valued at USD 17.6 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 39.1 billion by 2035.

Market growth is fueled by expanding commercial infrastructure, rising electrification requirements, and the growing need for uninterrupted business operations. Organizations across multiple industries are prioritizing reliable backup power systems to avoid financial losses, safeguard critical equipment, and maintain seamless service delivery. Commercial generator sets provide fast activation, flexible capacity options, and dependable performance, positioning them as essential components of energy resilience strategies. As enterprises become increasingly dependent on continuous electricity for digital systems, security frameworks, and automated operations, demand for high-efficiency gensets continues to accelerate. These systems are engineered to deliver stable power when the grid supply becomes unstable or unavailable, ensuring operational continuity in professional settings. Ongoing advancements in engineering design, intelligent controls, and integrated monitoring technologies are reshaping the competitive landscape. Modern gensets now incorporate automation, embedded sensors, and data-driven analytics to enhance performance, reduce service requirements, and extend operational lifespan. Remote diagnostics and predictive maintenance capabilities are further strengthening long-term value and driving broader commercial adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.6 Billion |

| Forecast Value | $39.1 Billion |

| CAGR | 8.3% |

The 50 kVA to 125 kVA capacity segment generated USD 2.7 billion in 2025, reflecting strong demand from small and mid-sized enterprises seeking dependable standby power. Market expansion in this segment is supported by infrastructure modernization efforts and the need for a reliable electricity supply in energy-sensitive commercial environments. Industry trends include improved fuel efficiency, lower emission profiles, digital control systems, and integration with hybrid energy configurations to enhance operational optimization and sustainability.

The hybrid commercial gensets segment is anticipated to grow at a CAGR of 10.5% between 2026 and 2035. Businesses are increasingly investing in low-emission backup power systems that combine conventional generator technology with battery storage or renewable energy components. These integrated systems reduce fuel usage, minimize noise levels, and lower operating expenditures. Heightened emphasis on environmental responsibility, energy security, and intelligent power management solutions is accelerating adoption across modern commercial facilities.

U.S. Commercial Gensets Market accounted for 80% share in 2025, generating USD 1.5 billion. Rising investment in commercial development projects and distributed energy infrastructure is reinforcing demand across the country. Market participants are concentrating on product innovation, sound reduction technologies, and comprehensive after-sales service programs to enhance customer loyalty and strengthen competitive positioning.

Leading companies operating in the Global Commercial Gensets Market include Caterpillar, Cummins, Generac Power Systems, Rolls-Royce, Mitsubishi Heavy Industries, Atlas Copco, AB Volvo Penta, Yanmar Holdings Co., Wartsila, Briggs & Stratton, Kirloskar, Ashok Leyland, Denyo Co., MAHINDRA POWEROL, AKSA POWER GENERATION, HIMOINSA, Deere & Company, Yamaha Motor Co., Sudhir Group, and HU TOAN GROUP. Companies within the Global Commercial Gensets Market are enhancing their competitive edge through product innovation, digital integration, and strategic expansion initiatives. Leading manufacturers are investing in advanced engine technologies, hybrid configurations, and emissions reduction systems to align with evolving environmental standards. Many firms are incorporating smart monitoring platforms and IoT-enabled controls to improve operational efficiency and predictive maintenance capabilities. Strategic partnerships with distributors and service providers are expanding geographic reach and strengthening after-sales support networks. Businesses are also focusing on customized power solutions tailored to specific commercial requirements, improving customer retention and brand differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Fuel trends

- 2.1.4 End use trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By power rating

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of commercial gensets

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Hybrid

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Telecom

- 7.3 Healthcare

- 7.4 Data Centers

- 7.5 Educational institutions

- 7.6 Government centers

- 7.7 Hospitality

- 7.8 Retail sales

- 7.9 Real estate

- 7.10 Commercial complex

- 7.11 Infrastructure

- 7.12 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 Standby

- 8.3 Peak shaving

- 8.4 Prime/continuous

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Russia

- 9.3.2 UK

- 9.3.3 Germany

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.4.8 Thailand

- 9.4.9 Vietnam

- 9.4.10 Philippines

- 9.4.11 Myanmar

- 9.5 Middle East

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Turkey

- 9.5.5 Iran

- 9.5.6 Oman

- 9.6 Africa

- 9.6.1 Egypt

- 9.6.2 Nigeria

- 9.6.3 Algeria

- 9.6.4 South Africa

- 9.6.5 Angola

- 9.6.6 Mozambique

- 9.7 Latin America

- 9.7.1 Brazil

- 9.7.2 Mexico

- 9.7.3 Argentina

- 9.7.4 Chile

Chapter 10 Company Profiles

- 10.1 AB Volvo Penta

- 10.2 AKSA POWER GENERATION

- 10.3 Ashok Leyland

- 10.4 Atlas Copco

- 10.5 Briggs & Stratton

- 10.6 Caterpillar

- 10.7 Cummins

- 10.8 Deere & Company

- 10.9 Denyo Co.

- 10.10 Generac Power Systems

- 10.11 HIMOINSA

- 10.12 HUU TOAN GROUP

- 10.13 Kirloskar

- 10.14 MAHINDRA POWEROL

- 10.15 MITSUBISHI HEAVY INDUSTRIES

- 10.16 Rolls-Royce

- 10.17 Sudhir Group

- 10.18 Wartsila

- 10.19 Yamaha Motor Co.

- 10.20 Yanmar Holdings Co.