|

시장보고서

상품코드

1982365

음료 포장 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Beverage Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

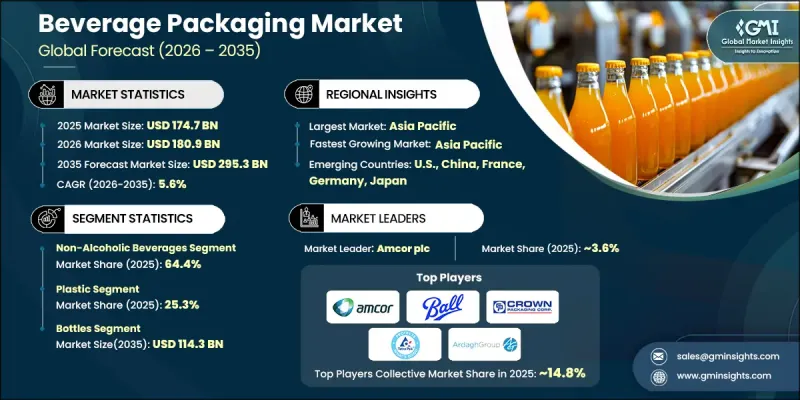

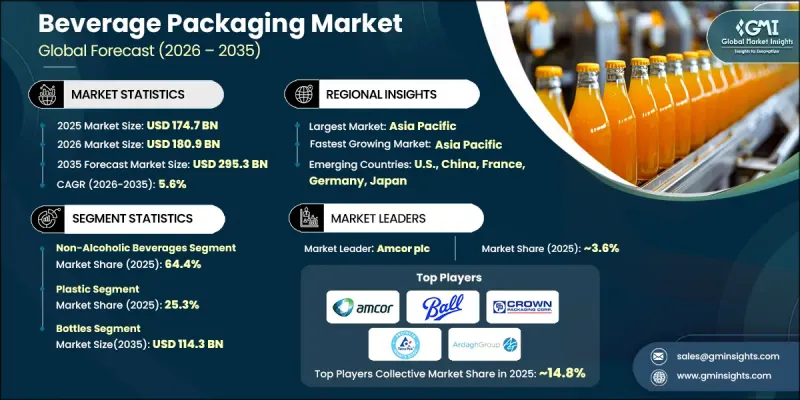

세계의 음료 포장 시장은 2025년에 1,747억 달러로 평가되었으며, CAGR 5.6%로 성장하여 2035년까지 2,953억 달러에 이를 것으로 추정됩니다.

이러한 강력한 성장은 선진국과 신흥국에서 패키지 음료의 소비 확대에 견인되고 있습니다. 급속한 도시화, 바쁜 소비자의 라이프스타일, 편리하고 1회분용으로 소분되어, 운반 가능한 음료 형태에 대한 기호의 고조가, 경량 병, 캔, 종이팩, 플렉서블 파우치 수요를 가속화하고 있습니다. 생수, 탄산음료, 즉시 음용 차 및 커피, 건강 지향 음료의 판매 확대가 시장의 지속적인 기세를 지원하고 있습니다. 제조업체 각사는 제품의 안전성을 높이고 보존 기간을 연장하고 브랜드 인지도를 향상시키는 포장 디자인에 주력하고 있습니다. 동시에 소재 및 제조 공정에서 기술의 발전으로 효율성과 비용 최적화가 진행되고 있습니다. 프리미엄화, 커스터마이징 및 기능성 음료 제공으로의 전환은 계속 포장 혁신을 촉진하고 있습니다. 소매 시장으로의 침투가 진행되고 현대 유통 채널이 확대되고 있는 것도 세계 수요를 더욱 강화하고 있습니다. 전반적으로, 음료 포장 산업은 소비자의 선호 변화, 규제 동향, 밸류체인 전반에 걸쳐 지속적인 소재 혁신에 힘입어 안정적인 1자리수 중반 성장이 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 1,747억 달러 |

| 예측 금액 | 2,953억 달러 |

| CAGR | 5.6% |

환경의 지속가능성은 음료 포장 시장 상황을 재구성하는데 있어서 매우 중요한 역할을 합니다. 환경에 미치는 영향에 대한 규제 강화와 소비자 의식 증가로 인해 기업은 재활용 가능, 생분해성 및 저배출 포장 소재의 채택을 촉진하고 있습니다. Amcor plc, Ball Corporation, Tetra Pak International SA와 같은 업계 리더는 지속가능성 목표에 부합하기 때문에 순환형 경제 활동, 경량화 솔루션 및 재생 소재 함량 향상에 투자하고 있습니다. 병행하여, 스마트하고 연결된 포장 기술도 주목을 받고 있습니다. 디지털 라벨링, 추적성 툴, 인터랙티브 포장 형식 등의 기능은 공급망의 투명성을 높이고, 특히 프리미엄 음료 카테고리에서 소비자의 참여를 강화하고 있습니다. 게다가 전자상거래와 D2C(Direct-to-Consumer) 유통 모델의 급속한 상승으로 제조업체는 운송 중 내구성, 구조적 강도 및 보존 기간의 성능을 향상시킨 포장 설계를 강요하고 있습니다.

알코올 음료 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 4.7%를 나타낼 것으로 예측됩니다. 프리미엄 알코올 음료와 간편하게 마실 수 있는 즉석 음료에 대한 수요 증가가 유리 및 재활용 가능한 금속 포장 솔루션의 혁신을 견인하고 있습니다. 가처분 소득 증가, 소비 패턴 변화 및 미적으로 매력적인 포장에 대한 수요가 이 부문의 성장에 기여하고 있습니다. 지속 가능하고 가벼운 포장 형태 외에도 온라인 소매 유통의 확대는 소비자 지향적이고 환경 친화적인 포장 디자인에 대한 투자를 촉진합니다.

플라스틱 부문은 2025년 25.3%의 점유율을 차지했습니다. 성장은 비용 효율성, 경량성 및 PET 소재가 고속 생산 라인과 호환됨으로써 지원됩니다. 플라스틱 포장은 세계 생수, 청량 음료 및 기능성 음료 카테고리에서 널리 사용되고 있습니다. 사용한 재활용 소재의 활용 확대와 재활용 기술의 발전으로 지속가능성 실적이 향상되었습니다. 또한 진행 중 경량화 노력으로 원재료 소비를 줄이고 운송 효율을 최적화하고 있습니다.

2025년 북미 음료 포장 시장은 21.3%의 점유율을 차지했습니다. 지역적 확장은 지속가능하고 재활용 가능한 포장 형태에 대한 선호도 증가와 더불어 편리한 휴대용 음료 솔루션에 대한 강한 수요에 의해 견인되고 있습니다. 첨단 제조 능력과 지속적인 제품의 프리미엄화가 시장 발전을 추진하고 있습니다. 경량 PET 병, 알루미늄 캔 및 스마트 포장 기술에 대한 투자는 운영 효율성과 소비자 간의 관계를 향상시킵니다. 기능성 음료 및 즉석형 제품의 성장은 미국, 캐나다, 멕시코 전역에서 포장 혁신을 더욱 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속가능성과 친환경 포장에 대한 수요 증가

- RTD(Ready-to-Drink) 음료 소비 확대

- 프리미엄 음료에 대한 소비자의 선호도 증가

- 독자적인 브랜딩과 개인화된 포장에 주력

- 도시화의 진전과 라이프 스타일의 변화

- 업계의 잠재적 위험 및 과제

- 원재료 비용 상승

- 세계 재활용 능력의 불균일성

- 시장 기회

- 순환형 경제 및 폐쇄형 순환 솔루션 도입

- 스마트하고 인터랙티브한 포장 기술의 통합

- 성장 촉진요인

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 특허 및 지적재산 분석

- 지정학적 및 무역의 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적 비교

- 매출액

- 이익률

- 연구개발(R&D)

- 제품 포트폴리오 비교

- 제품 라인업의 폭

- 기술

- 혁신

- 지역 전개 비교

- 세계 전개의 분석

- 서비스 네트워크 커버 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더

- 챌린저

- 팔로워

- 틈새 기업

- 전략적 전망 매트릭스

- 재무실적 비교

- 주요 발전, 2022-2025년

- 합병 및 인수

- 파트너십 및 제휴

- 기술적 진보

- 사업 확대 및 투자 전략

- 디지털 전환의 대처

- 신흥/스타트업 경쟁기업의 동향

제5장 시장 추계 및 예측 : 포장 유형별(2022-2035년)

- 경질 포장

- 반경질 포장

- 연질 포장

제6장 시장 추계 및 예측 : 제품 유형별(2022-2035년)

- 병

- 캔

- 카톤

- 파우치 및 사쉐

- 케그 및 배럴

- 기타

제7장 시장 추계 및 예측 : 재료별(2022-2035년)

- 플라스틱

- 유리

- 금속

- 종이 및 판지

- 기타

제8장 시장 추계 및 예측 : 음료 종류별(2022-2035년)

- 무알코올 음료

- 알코올 음료

제9장 시장 추계 및 예측 : 최종 사용 산업별(2022-2035년)

- 무균 포장

- 핫필 포장

- 저온 충전 및 기존 포장

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Amcor plc

- Ardagh Group SA

- Ball Corporation

- CANPACK

- CCL Container

- CPMC Holdings

- Crown

- Graham Packaging

- Graphic Packaging International, LLC

- Novelis

- Plastipak Holdings, Inc.

- SIG.

- Silgan Plastics

- Smurfit Westrock

- Stora Enso

- Tetra Pak International SA

- Visy

The Global Beverage Packaging Market was valued at USD 174.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 295.3 billion by 2035.

Strong growth is driven by rising consumption of packaged beverages across developed and emerging economies. Rapid urban expansion, fast-paced consumer lifestyles, and increasing preference for convenient, single-serve, and portable beverage formats are accelerating demand for lightweight bottles, cans, cartons, and flexible pouches. Expanding sales of bottled water, carbonated drinks, ready-to-drink tea and coffee, and health-oriented beverages are supporting sustained market momentum. Manufacturers are focusing on packaging designs that enhance product safety, extend shelf life, and improve brand visibility. At the same time, technological advancements in materials and production processes are improving efficiency and cost optimization. The shift toward premiumization, customization, and functional beverage offerings continues to stimulate packaging innovation. Growing retail penetration and the expansion of modern trade channels are further strengthening global demand. Overall, the beverage packaging industry is positioned for steady mid-single-digit growth, supported by evolving consumer preferences, regulatory developments, and ongoing material innovation across the value chain.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $174.7 Billion |

| Forecast Value | $295.3 Billion |

| CAGR | 5.6% |

Environmental sustainability plays a pivotal role in reshaping the beverage packaging market landscape. Stricter regulations and heightened consumer awareness regarding environmental impact are encouraging companies to adopt recyclable, biodegradable, and low-emission packaging materials. Industry leaders such as Amcor plc, Ball Corporation, and Tetra Pak International S.A. are investing in circular economy initiatives, lightweight solutions, and higher recycled content integration to align with sustainability targets. In parallel, smart and connected packaging technologies are gaining traction. Features such as digital labeling, traceability tools, and interactive packaging formats are enhancing supply chain transparency and strengthening consumer engagement, particularly within premium beverage categories. Additionally, the rapid rise of e-commerce and direct-to-consumer distribution models is prompting manufacturers to design packaging that offers improved durability, structural integrity, and shelf-life performance during transportation.

The alcoholic beverages segment is expected to grow at a CAGR of 4.7% between 2026 and 2035. Increasing demand for premium alcoholic drinks and convenient ready-to-consume formats is driving innovation in glass and recyclable metal packaging solutions. Rising disposable income levels, evolving consumption patterns, and demand for aesthetically appealing packaging are contributing to segment growth. Sustainable and lightweight packaging formats, along with expanding online retail distribution, are encouraging investment in consumer-focused and environmentally responsible packaging designs.

The plastic segment accounted for 25.3% share in 2025. Growth is supported by the cost efficiency, lightweight characteristics, and compatibility of PET materials with high-speed production lines. Plastic packaging remains widely used across bottled water, soft drinks, and functional beverage categories worldwide. Increased utilization of post-consumer recycled materials and advancements in recycling technologies are strengthening sustainability performance. Ongoing lightweighting initiatives are also reducing raw material consumption and optimizing transportation efficiency.

North America Beverage Packaging Market held 21.3% share in 2025. Regional expansion is driven by rising preference for sustainable and recyclable packaging formats, combined with strong demand for convenient, on-the-go beverage solutions. Advanced manufacturing capabilities and continued product premiumization are reinforcing market development. Investments in lightweight PET bottles, aluminum cans, and smart packaging technologies are enhancing operational efficiency and consumer interaction. Growth in functional beverages and ready-to-drink products is further accelerating packaging innovation across the United States, Canada, and Mexico.

Prominent companies operating in the Global Beverage Packaging Market include Ardagh Group S.A., Crown, Smurfit Westrock, CANPACK, Novelis, Graham Packaging, CPMC Holdings, Plastipak Holdings, Inc., Silgan Plastics, Graphic Packaging International, LLC, SIG, Stora Enso, Visy, CCL Container, and Amcor plc. Companies in the Global Beverage Packaging Market are strengthening their competitive position through continuous investment in sustainable materials, lightweight designs, and recyclable packaging innovations. Strategic mergers, acquisitions, and partnerships are expanding production capabilities and geographic reach. Many firms are enhancing research and development efforts to introduce advanced barrier technologies and smart packaging features that improve traceability and consumer engagement. Optimization of supply chains and automation of manufacturing processes are helping reduce operational costs and improve efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Deployment model trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for sustainability & eco friendly packaging

- 3.2.1.2 Increased consumption in ready to drink (RTD) beverages

- 3.2.1.3 Increasing consumer preference for premium drinks

- 3.2.1.4 Focus on unique branding and personalized packaging

- 3.2.1.5 Rising urbanization & changing lifestyles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising raw material costs

- 3.2.2.2 Inconsistent global recycling capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of circular economy & closed loop solutions

- 3.2.3.2 Integration of smart and interactive packaging technologies

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors' landscape

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Billion, Units)

- 5.1 Key trends

- 5.2 Rigid Packaging

- 5.3 Semi-Rigid Packaging

- 5.4 Flexible Packaging

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion, Units)

- 6.1 Key trends

- 6.2 Bottles

- 6.3 Cans

- 6.4 Cartons

- 6.5 Pouches & Sachets

- 6.6 Kegs & Barrels

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion, Units)

- 7.1 Key trends

- 7.2 Plastic

- 7.3 Glass

- 7.4 Metal

- 7.5 Paper & Boards

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Beverage Type, 2022 - 2035 (USD Billion, Units)

- 8.1 Key trends

- 8.2 Non-Alcoholic Beverages

- 8.3 Alcoholic Beverages

Chapter 9 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion, Units)

- 9.1 Key trends

- 9.2 Aseptic Packaging

- 9.3 Hot-Fill Packaging

- 9.4 Cold-Fill & Conventional Packaging

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amcor plc

- 11.2 Ardagh Group S.A.

- 11.3 Ball Corporation

- 11.4 CANPACK

- 11.5 CCL Container

- 11.6 CPMC Holdings

- 11.7 Crown

- 11.8 Graham Packaging

- 11.9 Graphic Packaging International, LLC

- 11.10 Novelis

- 11.11 Plastipak Holdings, Inc.

- 11.12 SIG.

- 11.13 Silgan Plastics

- 11.14 Smurfit Westrock

- 11.15 Stora Enso

- 11.16 Tetra Pak International S.A.

- 11.17 Visy