|

시장보고서

상품코드

1982381

자동차용 HVAC 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Automotive HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

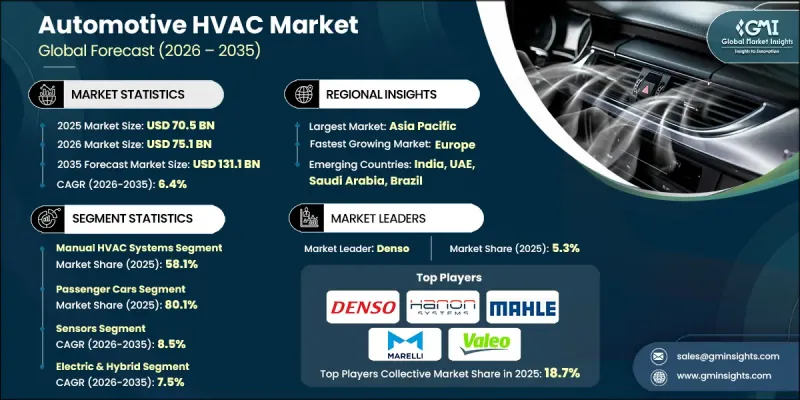

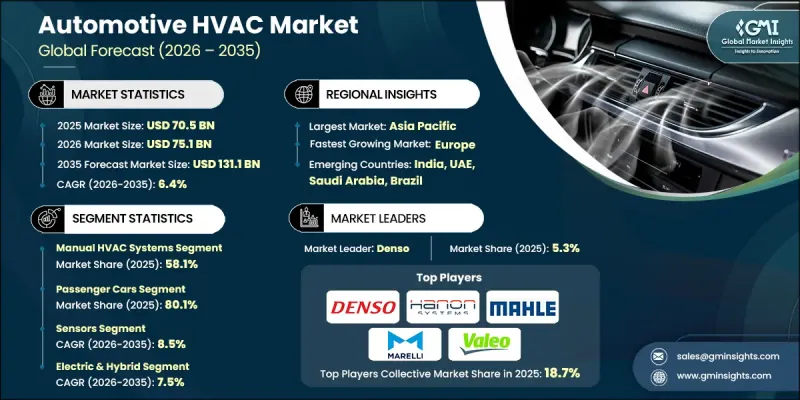

세계의 자동차용 HVAC 시장은 2025년 705억 달러로 평가되었으며 CAGR 6.4%로 성장해 2035년까지 1,311억 달러에 이를 것으로 추정됩니다.

시장의 성장은 가처분 소득 증가와 소비자의 이동성에 대한 선호의 변화에 힘입어 세계 자동차 보유 대수 증가에 의해 견인되고 있습니다. 더 많은 소비자가 자가용 차량을 구입함에 따라 고급 HVAC 시스템에 대한 수요는 계속 가속화되고 있습니다. 중급차 및 고급차 카테고리에서는 차 안의 쾌적성과 에어컨 제어 성능을 향상시키는 고급 HVAC 기술이 점점 채용되고 있습니다. 동시에 제조업체는 탑승자가 기류 및 온도 설정을 개별적으로 조정할 수 있는 고급 감지 기술을 갖춘 지능형 에어컨 솔루션을 통합합니다. 전기자동차의 급속한 보급으로 HVAC의 효율성이 더욱 중요해지고 있습니다. 이 시스템은 배터리 성능과 총 주행 거리에 직접 영향을 미치기 때문입니다. 이에 대응하기 위해 각 회사는 히트펌프 시스템이나 첨단 열 관리 모듈 등 에너지 효율적인 솔루션을 개발하고 있습니다. 병행하여 환경규제 강화로 지구온난화 계수가 낮은 냉매, 개선된 씰 시스템, 재활용 가능한 부품의 채용이 촉진되어 지속가능한 자동차용 HVAC 기술로의 전환이 뒷받침되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 705억 달러 |

| 예측 금액 | 1,311억 달러 |

| CAGR | 6.4% |

2025년 현재 수동 HVAC 시스템 부문은 58.1%의 점유율을 차지했으며 409억 달러 시장 규모를 창출했습니다. 주도적인 지위는 자동 시스템에 비해 비용 효율적이고 설계 구조가 간소화되어 제조 및 유지보수 비용이 낮기 때문입니다. 전자 부품 및 센서의 수가 적기 때문에 이러한 시스템은 신뢰할 수 있는 성능과 간편한 유지보수를 제공하여 대량 생산되는 대형 차량에서 매우 매력적인 옵션이 되었습니다. 내구성과 기술적 복잡성의 감소는 지속적인 수요를 더욱 지원합니다.

승용차 부문은 2025년에 80.1%의 점유율을 차지했으며, 2035년까지 1,076억 달러에 달할 것으로 예측됩니다. 상용차에 비해 승용차의 세계 생산량과 판매량이 많기 때문에 이 범주에서 HVAC 시스템 수요가 크게 증가하고 있습니다. 자동차 제조업체는 소비자의 기대에 부응하기 때문에 차내 쾌적성의 향상에 계속 주력하고 있어, 이것이 같은 부문의 우위성을 강화하고 있습니다. 승용차는 승무원의 쾌적성과 차내 체험을 우선하기 때문에 고급 공조 제어 기술의 통합이 더욱 진행되고 있습니다.

미국의 자동차용 HVAC 시장은 높은 자동차 보유율과 쾌적성을 중시하는 소비자의 강한 선호에 힘입어 2025년에는 780만 달러에 달했습니다. 또한 에너지 효율적인 HVAC 시스템을 필요로 하는 전기자동차 및 하이브리드 자동차의 판매 확대가 시장 성장을 가속하고 있습니다. 영역 관리 및 연결 제어를 포함한 스마트 공조 제어 기술은 OEM 및 애프터마켓 채널 모두에서 널리 사용되고 있습니다. 규제 조치는 차량의 에너지 효율을 점점 더 중시하고 있으며 시스템 설계 및 부품 최적화의 혁신을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 탑승자의 쾌적성에 대한 수요 증가

- 세계 자동차 생산 증가

- 전기자동차 및 하이브리드 자동차의 성장

- HVAC 시스템의 기술적 진보

- 업계의 잠재적 위험 및 과제

- HVAC 시스템 통합의 복잡성

- 엄격한 환경 규제

- 시장 기회

- 신흥 시장 수요 증가

- EV용 경량 및 컴팩트 HVAC 설계

- 애프터마켓용 HVAC 업그레이드 및 개조

- IoT 및 커넥티드카 시스템과 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 도로교통안전국(NHTSA)

- 미국 환경보호청(EPA)

- 캘리포니아주 대기자원국(CARB)

- 캐나다 규격 협회(CSA)

- 유럽

- 유럽 자동차 공업회(ACEA)

- 유럽연합 배출량 거래제도(EU ETS)

- 유럽표준화위원회(CEN)

- 유럽 환경청(EEA)

- 아시아태평양

- 도로 운수 및 고속도로성(MoRTH)

- 에너지 효율국(BEE)

- 중국 자동차 기술 연구센터(CATARC)

- 일본 자동차 공업회(JAMA)

- 라틴아메리카

- INMETRO

- 운수성

- 국가 육상 교통국(ANTT)

- 중동 및 아프리카

- 걸프 협력 회의 표준화 기구(GSO)

- 아랍에미리트(UAE) 표준화 및 계량청(ESMA)

- 사우디아라비아 표준, 계량 및 품질 기구(SASO)

- 남아프리카 표준국(SABS)

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- HVAC 시스템의 전동화

- 듀얼 존 및 멀티 존 공조 제어

- 차내 공기 여과 및 정화 시스템

- 차량 텔레매틱스 및 인포테인먼트와의 통합

- 신흥기술

- 열전식 HVAC 시스템

- 태양광 발전식 HVAC 유닛

- 스마트 및 AI 탑재형 공조 제어

- EV용 경량 및 컴팩트 HVAC 설계

- 현재의 기술 동향

- 가격 동향

- 지역별

- 제품별

- 비용 내역 분석

- 지속가능성과 환경에 미치는 영향

- 환경 영향 평가

- 사회적 영향과 지역사회 공헌

- 거버넌스와 기업의 사회적 책임

- 지속 가능한 금융 및 투자 동향

- 전기화가 HVAC 아키텍처에 미치는 영향

- 고전압과 저전압 HVAC 시스템의 비교

- 차내 환경의 사전 조정 전략과 에너지 관리

- 항속 거리 불안의 해소

- 듀얼 소스 난방 시스템

- OEM의 통합 전략과 플랫폼 접근

- 모듈형 HVAC 플랫폼 개발

- 차량 아키텍처 통합의 과제(ICE 대 EV)

- OEM과 공급업체 간의 공동 개발 파트너십

- 커스터마이즈 대 표준화

- 건강 및 웰빙 기능의 통합

- HEPA 필터 및 PM2.5 제거 기능

- 항균 및 항바이러스 코팅 기술

- 건강 최적화를 위한 습도 제어

- 알레르겐 및 병원체 검출 시스템

- 아로마테라피 및 공기 이온화 기능

- 사례 연구

- 앞으로의 전망과 기회

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 시스템별(2022-2035년)

- 자동 HVAC 시스템

- 수동 HVAC 시스템

제6장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

- 센서

- 온도 센서

- 습도 센서

- 대기질 센서

- 기타

- 열교환기

- 컨덴서

- 증발기

- 컴프레서

- 확장 장치

- 리시버 및 드라이어

- 블로어 모터

- 기타

제7장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- LCV

- MCV

- HCV

제8장 시장 추계 및 예측 : 추진력별(2022-2035년)

- 내연기관(ICE)

- 전기 및 하이브리드

- BEV

- HEV

- PHEV

- FCEV

제9장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 체코 공화국

- 벨기에

- 러시아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계기업

- Denso

- Valeo

- Mahle

- Hanon Systems

- Sanden

- Marelli

- Delphi

- Visteon

- Johnson Electric

- 지역 기업

- Air International Thermal Systems

- Subros

- Songz

- Shanghai Velle

- Hubei Meibiao

- Bergstrom

- 신흥기업

- Gentherm

- Behr Hella Service

- Trans Air Manufacturing

- Motherson

- Modine

The Global Automotive HVAC Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 131.1 billion by 2035.

Market growth is driven by increasing vehicle ownership worldwide, supported by rising disposable income and shifting consumer mobility preferences. As more consumers invest in personal vehicles, demand for advanced heating, ventilation, and air conditioning systems continues to accelerate. Mid-range and premium vehicle categories are increasingly incorporating enhanced HVAC technologies that deliver improved cabin comfort and climate control performance. At the same time, manufacturers are integrating intelligent climate solutions equipped with advanced sensing technologies that allow occupants to personalize airflow and temperature settings. The rapid growth of electric vehicles has further elevated the importance of HVAC efficiency, as these systems directly influence battery performance and overall driving range. To address this, companies are developing energy-efficient solutions such as heat pump systems and advanced thermal management modules. In parallel, evolving environmental regulations are encouraging the adoption of low global warming potential refrigerants, improved sealing systems, and recyclable components, reinforcing the shift toward sustainable automotive HVAC technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $131.1 Billion |

| CAGR | 6.4% |

The manual HVAC systems segment accounted for 58.1% share in 2025, generating USD 40.9 billion. Their leadership position stems from cost efficiency, simplified design architecture, and lower production and maintenance expenses compared to automatic systems. With fewer electronic components and sensors, these systems offer dependable performance and straightforward servicing, making them highly attractive across large vehicle production volumes. Their durability and reduced technical complexity further support sustained demand.

The passenger cars segment held 80.1% share in 2025 and is forecast to reach USD 107.6 billion by 2035. Higher global production and sales volumes of passenger vehicles compared to commercial vehicles significantly increase HVAC system demand within this category. Automakers continue to enhance cabin comfort features to meet consumer expectations, reinforcing segment dominance. Passenger vehicles prioritize occupant comfort and interior experience, which drives greater integration of advanced climate control technologies.

U.S. Automotive HVAC Market reached USD 7.8 million in 2025, supported by high vehicle ownership rates and strong consumer preference for comfort-oriented features. Growth is further driven by the expansion of electric and hybrid vehicle sales, which require optimized energy-efficient HVAC systems. Smart climate control technologies, including zonal management and connected controls, are gaining traction in both OEM and aftermarket channels. Regulatory measures increasingly emphasize vehicle energy efficiency, reinforcing innovation in system design and component optimization.

Leading companies operating in the Global Automotive HVAC Market include Valeo, Denso, Marelli, Hanon Systems, Sensata, Mahle, Air International Thermal Systems, Sanden, Johnson Electric, and Visteon. Companies in the Global Automotive HVAC Market are strengthening their competitive positions through continuous innovation and strategic partnerships. Major players are investing in advanced thermal management technologies, energy-efficient compressors, and intelligent climate control systems tailored for electric and hybrid vehicles. Collaboration with automakers enables early integration of next-generation HVAC platforms into new vehicle architectures. Firms are expanding global manufacturing footprints to improve supply chain resilience and reduce production costs. Research and development efforts focus on lightweight materials, smart sensors, and environmentally friendly refrigerants to comply with tightening emission regulations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for passenger comfort

- 3.2.1.2 Rising vehicle production globally

- 3.2.1.3 Growth in electric and hybrid vehicles

- 3.2.1.4 Technological advancements in HVAC systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity in HVAC system integration

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging markets

- 3.2.3.2 Lightweight and compact HVAC designs for EVs

- 3.2.3.3 Aftermarket HVAC upgrades and retrofitting

- 3.2.3.4 Integration with IoT and connected vehicle systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Environmental Protection Agency (EPA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Canadian Standards Association (CSA)

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.2 European Union Emissions Trading System (EU ETS)

- 3.4.2.3 European Committee for Standardization (CEN)

- 3.4.2.4 European Environment Agency (EEA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Road Transport and Highways (MoRTH)

- 3.4.3.2 Bureau of Energy Efficiency (BEE)

- 3.4.3.3 China Automotive Technology & Research Center (CATARC)

- 3.4.3.4 Japan Automobile Manufacturers Association (JAMA)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO

- 3.4.4.2 Ministry of Transport

- 3.4.4.3 National Agency for Land Transportation (ANTT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization & Metrology (ESMA)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.4 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrification of HVAC Systems

- 3.7.1.2 Dual-Zone and Multi-Zone Climate Control

- 3.7.1.3 Cabin Air Filtration and Purification Systems

- 3.7.1.4 Integration with Vehicle Telematics and Infotainment

- 3.7.2 Emerging technologies

- 3.7.2.1 Thermoelectric HVAC Systems

- 3.7.2.2 Solar-Powered HVAC Units

- 3.7.2.3 Smart and AI-Enabled Climate Control

- 3.7.2.4 Lightweight and Compact HVAC Designs for EVs

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Electrification impact on HVAC architecture

- 3.11.1 High voltage vs. low voltage HVAC system comparison

- 3.11.2 Cabin preconditioning strategies and energy management

- 3.11.3 Range anxiety mitigation

- 3.11.4 Dual-source heating systems

- 3.12 OEM integration strategies and platform approaches

- 3.12.1 Modular HVAC platform development

- 3.12.2 Vehicle architecture integration challenges (ICE vs. EV)

- 3.12.3 Co-development partnerships between OEMs and suppliers

- 3.12.4 Customization vs. standardization

- 3.13 Health and wellness feature integration

- 3.13.1 HEPA filtration and PM2.5 removal capabilities

- 3.13.2 Antimicrobial and antiviral coating technologies

- 3.13.3 Humidity control for health optimization

- 3.13.4 Allergen and pathogen detection systems

- 3.13.5 Aromatherapy and air ionization features

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Automatic HVAC systems

- 5.3 Manual HVAC systems

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Sensors

- 6.2.1 Temperature sensors

- 6.2.2 Humidity sensors

- 6.2.3 Air quality sensors

- 6.2.4 Others

- 6.3 Heat exchangers

- 6.3.1 Condenser

- 6.3.2 Evaporator

- 6.4 Compressor

- 6.5 Expansion device

- 6.6 Receiver/drier

- 6.7 Blower motor

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric & hybrid

- 8.3.1 BEV

- 8.3.2 HEV

- 8.3.3 PHEV

- 8.3.4 FCEV

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Czech Republic

- 10.3.7 Belgium

- 10.3.8 Russia

- 10.3.9 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Denso

- 11.1.2 Valeo

- 11.1.3 Mahle

- 11.1.4 Hanon Systems

- 11.1.5 Sanden

- 11.1.6 Marelli

- 11.1.7 Delphi

- 11.1.8 Visteon

- 11.1.9 Johnson Electric

- 11.2 Regional players

- 11.2.1 Air International Thermal Systems

- 11.2.2 Subros

- 11.2.3 Songz

- 11.2.4 Shanghai Velle

- 11.2.5 Hubei Meibiao

- 11.2.6 Bergstrom

- 11.3 Emerging players

- 11.3.1 Gentherm

- 11.3.2 Behr Hella Service

- 11.3.3 Trans Air Manufacturing

- 11.3.4 Motherson

- 11.3.5 Modine