|

시장보고서

상품코드

1939081

자동차용 HVAC : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

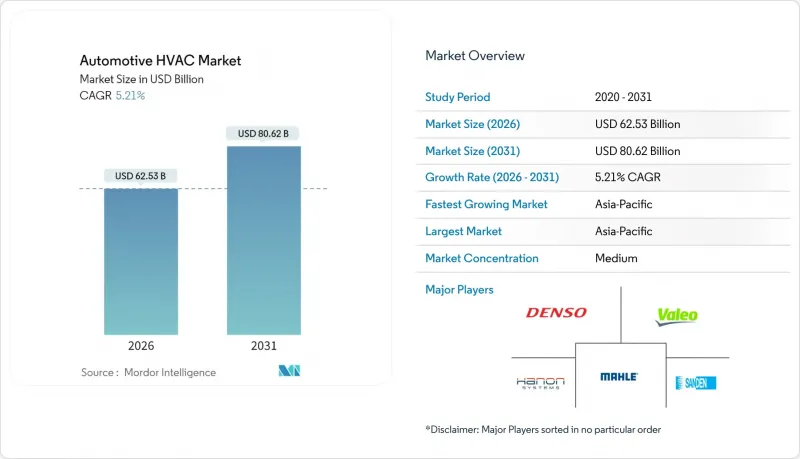

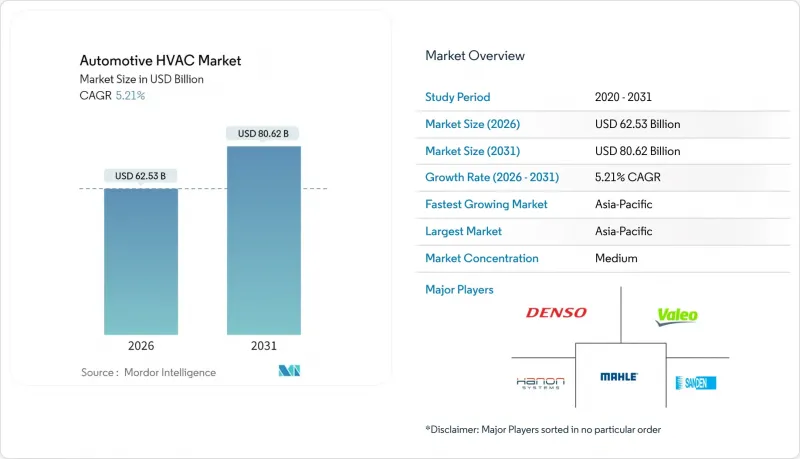

자동차용 HVAC 시장은 2025년에 594억 4,000만 달러로 평가되며, 2026년 625억 3,000만 달러에서 2031년까지 806억 2,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 5.21%로 전망되고 있습니다.

이러한 꾸준한 확대는 전기 파워트레인으로의 전환, 편의성에 대한 규제 강화, 그리고 높아진 소비자 기대치를 반영합니다. 아시아태평양은 여전히 주요 제조 거점이며, 배출가스 규제 강화로 인해 열 관리 기술이 지속적으로 개선되고 있습니다. 한편, 자동 공조 제어 시스템이 양산 차종에 도입되면서 과거 고급차 모델에 한정되었던 가격 프리미엄이 축소되고 있습니다. 부품 공급업체들은 전자제어, 첨단 필터 기술, 저 GWP 냉매 호환성을 통해 차별화를 꾀하고 있으며, HVAC를 보조적인 편의 모듈에서 차량 전동화의 핵심 추진 요소로 재포지셔닝하고 있습니다.

세계 자동차 HVAC 시장 동향과 인사이트

EV 히트펌프 시스템의 HVAC 효율 요구 사항

BEV의 보급으로 HVAC는 항속거리와 직결되는 중요한 서브시스템으로 변모했습니다. -10℃ 환경에서 성능계수 3.0 이상을 달성하는 히트펌프는 겨울철 300km 주행시 최대 11kWh의 전력 절감을 실현하며, 저항 히터 사용시 발생하는 40%의 항속거리 감소를 크게 줄여줍니다. 자동차 제조업체는 배터리, 파워 일렉트로닉스, 캐빈 사이에 냉각 루프를 통합하여 폐열을 회수하고 있습니다. 이에 따라 공급업체는 저온 증기 주입에 맞게 조정된 멀티포트 밸브와 인버터 구동 압축기를 제공해야 합니다. 중국 산업정보화부(MIIT) 크레딧과 같은 차량 효율성 평가에 대한 규제 인센티브로 인해 OEM은 엔트리급 EV에서도 프리미엄 HVAC를 지정하도록 장려하고 있습니다.

자동 공조 제어의 편안함에 대한 수요

차량이 원격 사전 공조 설정, 음성 명령, 사용자 프로파일 학습이 가능한 커넥티드 아키텍처로 이동함에 따라 자동 시스템에 대한 소비자 선호도가 높아지고 있습니다. 정밀한 온도 유지는 운전자의 피로와 산만함을 줄여주며, SUV의 대용량화 추세에 따라 안전 우선순위에 부합합니다. OEM은 평균 거래 가격을 높이기 위해 자동 HVAC를 인포테인먼트 패키지와 번들로 제공하고 있으며, 센서 비용의 감소는 소형 모델에 탑재를 촉진하고 있습니다. 소득 향상과 함께 편안함에 대한 기대가 높아지는 신흥 경제국에서는 보급이 가속화되고 있습니다. BEV(배터리 전기자동차)의 경우, 자동 제어가 에너지 효율적인 차량내 난방 전략을 조정하여 도시 출퇴근시 배터리 충전 상태를 유지합니다.

자동 공조 시스템의 단가 및 복잡성 증가

전자식 팽창 밸브, 스테퍼 모터 액추에이터, 멀티 센서 클러스터로 인해 부품 원가가 수동 시스템에 비해 최대 50%까지 상승하여 엔트리 부문 해치백 차량에 대한 보급을 제한하고 있습니다. 서비스 네트워크는 진단 스캔 툴와 기술자 재교육이 필요하며, 이는 수명주기 비용을 더욱 증가시킵니다. 반도체 부족으로 인한 조달 변동으로 인해 브라질과 인도네시아의 자동차 제조업체들은 소비자들의 관심에도 불구하고 자동 공조 시스템 표준화를 늦추고 있습니다.

부문 분석

센서 가격의 하락과 텔레매틱스 플랫폼을 활용한 편의성 구독 서비스 제공으로 자동 시스템의 점유율이 점차 증가하고 있습니다. 2025년 기준, 수동 및 반자동 솔루션이 자동차 HVAC 시장 점유율의 58.12%를 차지하며 여전히 주류였습니다. 그러나 자동식 시스템은 2031년까지 연평균 복합 성장률(CAGR) 9.25%로 확대되어 약 168억 달러의 부가가치를 창출할 것으로 예측됩니다. AI 기반 학습 프로파일이 사용자 경험을 향상시키는 동시에 배터리 예열 기능과의 통합은 BEV(배터리 전기자동차)에 이점을 가져다줍니다.

C 부문 차량의 단일 구역 자동 제어의 표준화는 수동식 로터리 다이얼과의 비용 차이를 줄일 수 있습니다. 프리미엄 모델의 경우, 듀얼 존 및 트리플 존 구성은 추가 가격 책정의 기반이 됩니다. 자체 알고리즘 개발을 습득한 공급업체는 소프트웨어 컨설팅의 크로스셀링을 전개하고, 기존 기계 제조업체는 경쟁력을 유지하기 위해 마이크로컨트롤러 전문업체와 제휴하고 있습니다.

2025년 기준 승용차가 자동차 HVAC 시장 점유율의 79.62%를 차지할 것으로 예상되지만, 정부의 승객 편의성 규제 법제화에 따라 버스-코치 시장은 2031년까지 연평균 복합 성장률(CAGR) 6.55%로 승용차를 추월할 것으로 전망됩니다. 라이드셰어용 미니버스 서비스에서는 지자체 계약 획득을 위해 HEPA 필터가 내장된 지붕 장착형 유닛을 선호합니다.

라스트 마일 물류를 담당하는 소형 상용차는 엔진 정지 시에도 화물 배송이 가능한 보조 전기 에어컨을 채택하여 저공해 지역에서의 공회전 벌칙을 경감하고 있습니다. 인도, 인도네시아, 멕시코의 중대형 트럭은 새로운 안전 규제에 대응하기 위해 공장 장착형 에어컨으로 전환하고 있으며, 먼지가 많은 운전 사이클을 견딜 수 있는 견고한 컴프레서 설계에 대한 수요가 증가하고 있습니다.

지역별 분석

아시아태평양은 2025년 자동차 HVAC 시장 점유율 48.55%를 차지할 것으로 예상되며, 2031년까지 연평균 5.55%의 성장률로 선두를 유지할 것으로 전망됩니다. 중국의 2025년 신에너지 자동차 판매 할당량에 따라 현지 OEM 업체들은 북방 겨울철(-20℃)에도 효율적으로 작동할 수 있는 통합형 히트펌프 모듈을 채택할 수밖에 없습니다. 인도에서 대형 트럭의 에어컨 전차종 장착 의무화로 인해 고진동 환경에 대응하는 고강도 컴프레서의 대량 주문이 증가하고 있습니다. 일본과 한국은 고정밀 전자식 팽창밸브를 수출하고 있으며, 이 지역의 밸류체인의 완성도를 높이고 있습니다.

북미는 성숙하면서도 기술적으로 진보적인 시장을 반영하고 있습니다. 픽업트럭과 SUV는 대형 캐빈에 대응하는 대용량 커패시터를 필요로 하며, 캐나다와 미국 북부의 극한 기후는 한랭지용 히트펌프의 성능을 입증하고 있습니다. 미쓰비시전기가 켄튀르키예 공장에 1억 4,350만 달러를 투자해 가변속 컴프레서 라인을 개조한 것은 이 지역이 EV용 HVAC의 국내 조달에 전략적으로 집중하고 있음을 보여줍니다.

유럽에서 가장 엄격한 저 GWP 냉매 도입 일정이 시행되면서 R1234yf의 채택이 가속화되고 있으며, 2030년 이후 규제 대응을 위해 공급업체들은 천연 냉매 R744의 프로토타입 개발에 박차를 가하고 있습니다. 독일과 프랑스의 시내버스 전동화 프로그램에서는 입찰 요건을 충족하기 위해 에너지 효율이 높은 히트펌프 시스템을 규정하고 있습니다. ISO 13043:2011은 성능 표준을 설정하고, 이는 공급업체의 품질관리 시스템에 파급 효과를 가져와 대륙 전체에서 시스템 일관성을 보장합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The automotive HVAC market was valued at USD 59.44 billion in 2025 and estimated to grow from USD 62.53 billion in 2026 to reach USD 80.62 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

This steady expansion reflects the sector's transition toward electrified powertrains, stricter comfort regulations, and rising consumer expectations. Asia-Pacific remains the principal manufacturing hub, and its tightening emissions rules spur continuous upgrades of thermal-management technology. Meanwhile, automatic climate-control systems enter mass-market vehicle lines, compressing the price premium that once confined them to luxury models. Component suppliers differentiate through electronic control, advanced filtration, and low-GWP refrigerant compatibility, repositioning HVAC from an auxiliary comfort module to a critical enabler of vehicle electrification.

Global Automotive HVAC Market Trends and Insights

HVAC Efficiency Requirements for EV Heat-Pump Systems

BEV adoption turns HVAC into a range-critical subsystem. Heat pumps that achieve a coefficient of performance above 3.0 at -10 °C can save up to 11 kWh during a 300 km winter drive, mitigating the 40% range penalty seen with resistive heaters. Automakers integrate coolant loops among battery, power electronics, and cabin to harvest waste heat, prompting suppliers to deliver multi-port valves and inverter-driven compressors tuned for low-temperature vapor injection. Regulatory incentives that reward vehicle efficiency, such as China's MIIT credits, incentivize OEMs to specify premium HVAC even for entry-segment EVs.

Demand for Automatic Climate-Control Comfort

Consumer preference for automatic systems intensifies as vehicles migrate to connected architectures that enable remote pre-conditioning, voice commands, and user-profile learning. Precise temperature maintenance reduces driver fatigue and distraction, aligning with safety priorities as SUVs with larger cabin volumes proliferate. OEMs bundle automatic HVAC with infotainment packages to lift average transaction prices, and falling sensor costs encourage deployment in compact models. Uptake accelerates in emerging economies where rising incomes elevate comfort expectations. In BEVs, automatic control also orchestrates energy-efficient cabin warming strategies that preserve battery state of charge during urban commutes.

Higher Unit Cost and Complexity for Automatic HVAC

Electronic expansion valves, stepper-motor actuators, and multi-sensor clusters elevate bill-of-materials cost by up to 50% relative to manual systems, limiting penetration in entry-segment hatchbacks. Service networks require diagnostic scan tools and technician retraining, further inflating lifecycle expense. Semiconductor shortages introduce procurement volatility, encouraging OEMs in Brazil and Indonesia to delay standardization of automatic climate control despite consumer interest.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Focus on Cabin Air-Quality and Filtration

- Safety and Comfort Regulations in Emerging Markets

- HVAC Load Cutting EV Driving-Range Targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic systems capture incremental share as sensor prices fall and OEMs exploit telematics platforms to deliver comfort subscriptions. In 2025, manual and semi-automatic solutions still dominated with a 58.12% of the automotive HVAC market share in 2025. However, automatic setups will expand at a 9.25% CAGR through 2031, adding nearly USD 16.8 billion in incremental value. AI-based learning profiles elevate the user experience, while integration with battery preconditioning benefits BEVs.

Standardizing single-zone automatic control in C-segment cars compresses the cost gap relative to manual rotary dials. In premium models, dual- and tri-zone configurations underpin add-on pricing. Suppliers that mastered in-house algorithm development now cross-sell software consultancy, while legacy mechanical firms partner with microcontroller specialists to stay competitive.

Passenger cars account for 79.62% of the automotive HVAC market share in 2025, yet buses and coaches will outpace at a 6.55% CAGR to 2031 as governments legislate passenger comfort mandates. Ride-sharing minibus services favor roof-mounted units with integrated HEPA filtration to win municipal contracts.

Light commercial vehicles serving last-mile logistics adopt auxiliary electric air-conditioning to allow engine-off parcel drops, reducing idling penalties in low-emission zones. Medium and heavy trucks in India, Indonesia, and Mexico shift toward factory-fit AC to comply with new safety rules, enlarging volume for robust compressor designs that tolerate dusty duty cycles.

The Automotive HVAC Market Report is Segmented by Technology Type (Manual/Semi-automatic HVAC and Automatic HVAC), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Compressor, Condenser, and More), Propulsion Type (ICE Vehicles, Hybrid and Plug-In Hybrid Vehicles, and More), Sales Channel (OEM Factory-Fit and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 48.55% of the automotive HVAC market share in 2025 and is set to maintain the lead with a 5.55% CAGR through 2031. China's 2025 NEV sales quota compels local OEMs to adopt integrated heat-pump modules that operate efficiently in -20 °C northern winters. India's blanket AC mandate for heavy trucks fuels bulk orders for rugged compressors built to tolerate high vibration. Japan and South Korea export high-precision electronic expansion valves, reinforcing the region's value-chain completeness.

North America reflects a mature yet technologically progressive market. Pickup trucks and SUVs require high-capacity condensers to serve large cabin volumes, and frigid climates in Canada and the northern United States validate cold-weather heat-pump performance. Mitsubishi Electric's USD 143.5 million retrofit of its Kentucky plant for variable-speed compressor lines underscores the region's strategic focus on domestically sourced HVAC for EV applications.

Europe enforces the most aggressive low-GWP refrigerant timeline, accelerating the adoption of R1234yf and pushing suppliers toward natural refrigerant R744 prototypes for post-2030 compliance. Urban bus electrification programs in Germany and France stipulate energy-efficient heat-pump systems to meet tender requirements. ISO 13043:2011 sets performance benchmarks that ripple through supplier quality-management systems, ensuring system integrity across the continent .

- Denso Corporation

- Valeo Group

- Hanon Systems Co., Ltd.

- MAHLE GmbH

- Sanden Corporation

- Marelli Holdings Co., Ltd.

- Keihin Corporation

- Japan Climate Systems Corporation

- Mitsubishi Heavy Industries, Ltd.

- Samvardhana Motherson International Limited

- HELLA GmbH & Co. KGaA

- Subros Ltd.

- Aisin Corporation

- Eberspacher Group

- Brose Fahrzeugteile

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 HVAC Efficiency Requirements for EV Heat-Pump Systems

- 4.2.2 Demand for Automatic Climate-Control Comfort

- 4.2.3 Post-Pandemic Focus on Cabin Air-Quality and Filtration

- 4.2.4 Safety and Comfort Regulations in Emerging Markets

- 4.2.5 Ride-Hailing Fleet Retro-Fit Demand Surge

- 4.2.6 AI-Based Predictive and Zonal Climate Functions

- 4.3 Market Restraints

- 4.3.1 Higher Unit Cost and Complexity for Automatic HVAC

- 4.3.2 HVAC Load Cutting EV Driving-Range Targets

- 4.3.3 Costly Transition to Low-GWP Refrigerants

- 4.3.4 Shortage of Technicians Trained on New Refrigerants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Technology Type

- 5.1.1 Manual / Semi-automatic HVAC

- 5.1.2 Automatic HVAC

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCV)

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Buses and Coaches

- 5.3 By Component

- 5.3.1 Compressor

- 5.3.2 Condenser

- 5.3.3 Evaporator

- 5.3.4 Expansion Valve / Orifice Tube

- 5.3.5 Receiver-Dryer and Accumulator

- 5.3.6 Electronic and Sensor Suite

- 5.4 By Propulsion Type

- 5.4.1 ICE Vehicles

- 5.4.2 Hybrid and Plug-in Hybrid Vehicles

- 5.4.3 Battery-Electric Vehicles

- 5.5 By Sales Channel

- 5.5.1 OEM Factory-Fit

- 5.5.2 Aftermarket Retro-Fit and Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Denso Corporation

- 6.4.2 Valeo Group

- 6.4.3 Hanon Systems Co., Ltd.

- 6.4.4 MAHLE GmbH

- 6.4.5 Sanden Corporation

- 6.4.6 Marelli Holdings Co., Ltd.

- 6.4.7 Keihin Corporation

- 6.4.8 Japan Climate Systems Corporation

- 6.4.9 Mitsubishi Heavy Industries, Ltd.

- 6.4.10 Samvardhana Motherson International Limited

- 6.4.11 HELLA GmbH & Co. KGaA

- 6.4.12 Subros Ltd.

- 6.4.13 Aisin Corporation

- 6.4.14 Eberspacher Group

- 6.4.15 Brose Fahrzeugteile

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment