|

시장보고서

상품코드

1998708

외상 고정 기기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Trauma Fixation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

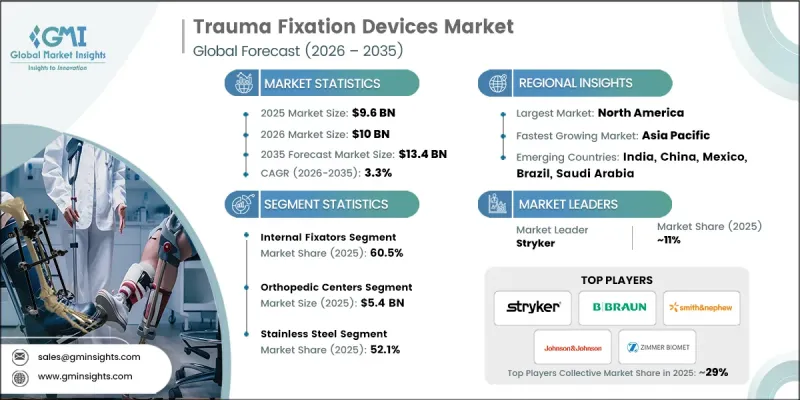

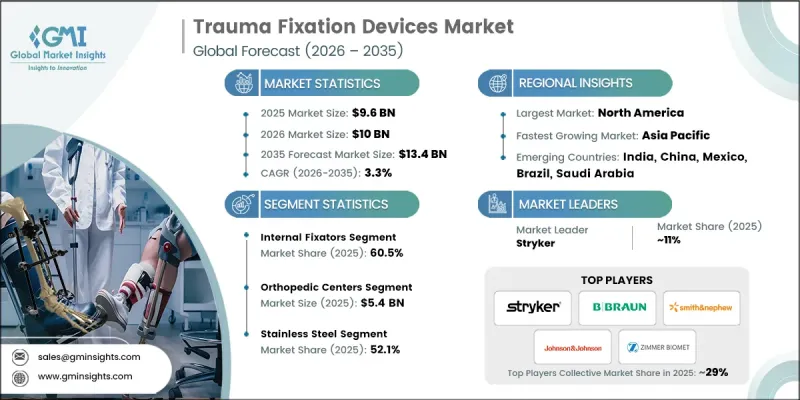

세계의 외상 고정 디바이스 시장은 2025년에 96억 달러로 평가되며, 2035년까지 CAGR 3.3%로 성장하며, 134억 달러에 달할 것으로 추정되고 있습니다.

시장 성장은 외상 및 정형외과적 손상의 유병률 증가, 최소 침습 수술에 대한 수요 증가, 내부 고정 기술의 지속적인 발전으로 인해 주도되고 있습니다. 외상 고정용 장치는 플레이트, 스크류, 로드, 핀, 외고정장치 등 골절된 뼈를 안정시키는데 필수적인 임플란트 및 기구로, 치유 과정에서 골절된 뼈를 안정시키는데 필수적인 임플란트 및 기구입니다. 교통사고, 스포츠 부상, 낙상 사고의 급증과 더불어 골절 및 골다공증에 취약한 고령 인구 증가로 인해 이러한 장치에 대한 수요가 증가하고 있습니다. 3D 프린팅의 도입, 맞춤형 기기, 스마트 기술, IoT 지원 솔루션, 티타늄 및 기타 첨단 재료의 사용과 같은 추세는 임상 결과와 수술의 정확성을 더욱 향상시키고 전체 시장의 확장을 촉진하며 세계 정형외과 의료의 미래를 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 96억 달러 |

| 예측액 | 134억 달러 |

| CAGR | 3.3% |

2025년, 내부 고정 장치 부문은 60.5%의 점유율을 차지했습니다. 이는 복잡한 골절을 안정화시키고, 우수한 생체역학적 강도를 발휘하며, 정확한 해부학적 정렬을 지원하는 능력에 의해 지원됩니다. 골내 못, 플레이트, 스크류와 같은 장치는 최소 침습적 접근을 가능하게 하고, 근육과 조직의 손상을 줄이고, 회복을 촉진하며, 일관된 뼈 치유를 보장합니다.

2025년 스테인리스강 부문은 52.1%의 점유율을 차지했습니다. 티타늄에 비해 가격이 저렴하므로 비용에 민감한 의료 현장이나 신흥 시장에서 쉽게 사용할 수 있는 선택이 될 수 있습니다. 또한 높은 인장 강도와 내구성을 갖추고 있으며, 고부하가 걸리는 응용 분야에서 플레이트, 스크류, 로드를 지지하여 전 세계 정형외과 시설에서 채택을 촉진하고 있습니다.

북미 외상 고정 기기 시장은 높은 외상 사례 발생률, 첨단 의료 인프라 및 전문 정형외과 센터의 지원으로 2025년 54.8%의 점유율을 차지할 것으로 예측됩니다. 골절의 다발성 골절과 더불어 기술적으로 진보된 고정 장치에 대한 접근이 가능해짐에 따라 환자의 치료 결과가 향상되어 지역적 수요를 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035

제6장 시장 추산·예측 : 재료별2022-2035

제7장 시장 추산·예측 : 부위별, 2022-2035

제8장 시장 추산·예측 : 최종 용도별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Trauma Fixation Devices Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 3.3% to reach USD 13.4 billion by 2035.

Market growth is driven by the rising prevalence of trauma and orthopedic injuries, increasing demand for minimally invasive procedures, and ongoing advancements in internal fixation technologies. Trauma fixation devices are essential implants and instruments that stabilize fractured bones during the healing process, including plates, screws, rods, pins, and external fixators. The surge in road accidents, sports-related injuries, and falls, combined with a growing elderly population prone to fractures and osteoporosis, is intensifying the need for these devices. Trends such as the integration of 3D printing, device customization, smart technology, IoT-enabled solutions, and the use of titanium and other advanced materials are further enhancing clinical outcomes, surgical precision, and overall market expansion, shaping the future of orthopedic care globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $13.4 Billion |

| CAGR | 3.3% |

The internal fixators segment held a share of 60.5% in 2025, driven by their ability to stabilize complex fractures, deliver superior biomechanical strength, and support precise anatomical alignment. Devices such as intramedullary nails, plates, and screws allow minimally invasive approaches that reduce muscle and tissue trauma, accelerate recovery, and ensure consistent bone healing.

The stainless steel segment held a 52.1% share in 2025. Its affordability compared to titanium makes it an accessible option for cost-sensitive healthcare settings and emerging markets. It also provides high tensile strength and durability, supporting plates, screws, and rods in high-load-bearing applications, thereby enhancing adoption across global orthopedic facilities.

North America Trauma Fixation Devices Market held a 54.8% share in 2025, fueled by a high incidence of trauma cases, advanced healthcare infrastructure, and specialized orthopedic centers. The prevalence of fractures, coupled with access to technologically advanced fixation devices, ensures better patient outcomes, driving regional demand.

Prominent players in the Global Trauma Fixation Devices Market include Acumed, Arthrex, B Braun, Bioretec, CONMED, Implanet, Integra, Johnson & Johnson, KLS Martin, Medicon, Orthofix, Smith & Nephew, Stryker, Wright Medical, and Zimmer Biomet. Key strategies adopted by companies to strengthen their Trauma Fixation Devices Market presence include investing in R&D to develop next-generation internal and external fixation solutions, launching minimally invasive and customizable devices, leveraging 3D printing for patient-specific implants, expanding into emerging markets, forming partnerships with hospitals and orthopedic centers, enhancing supply chain efficiency, integrating IoT-enabled and smart technologies for real-time monitoring, providing comprehensive surgeon training and support programs, and focusing on cost-effective stainless steel and titanium-based products to capture both premium and value-driven segments. These approaches enable sustained growth, technological leadership, and improved adoption across global trauma care markets.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Material trends

- 2.2.4 Site trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of degenerative bone diseases

- 3.2.1.2 Rising incidence of injuries

- 3.2.1.3 Growing technological advancements in trauma fixation devices

- 3.2.1.4 Increasing demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Post-surgery complication

- 3.2.2.2 Stringent regulation

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing R&D investment and product-development activities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Number of fatalities in road accidents, by region, 2022-2025

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 MEA

- 3.8 Pipeline analysis

- 3.9 Patent analysis

- 3.10 Pricing analysis, 2025 (Driven by primary research)

- 3.11 Customer insights (Driven by primary research)

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Internal fixators

- 5.2.1 Plates

- 5.2.2 Nails

- 5.2.3 Screws

- 5.2.4 Other internal fixators

- 5.3 External fixators

- 5.3.1 Unilateral and bilateral

- 5.3.2 Hybrid

- 5.3.3 Circular

Chapter 6 Market Estimates and Forecast, By Material 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Titanium

- 6.4 Other materials

Chapter 7 Market Estimates and Forecast, By Site, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Lower extremities

- 7.2.1 Foot & ankle

- 7.2.2 Knee

- 7.2.3 Lower leg

- 7.2.4 Hip and pelvic

- 7.2.5 Thigh

- 7.3 Upper extremities

- 7.3.1 Arm

- 7.3.2 Hand & wrist

- 7.3.3 Shoulder

- 7.3.4 Elbow

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedic centers

- 8.3 Hospitals

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Acumed

- 10.2 Arthrex

- 10.3 B Braun

- 10.4 Bioretec

- 10.5 CONMED

- 10.6 Implanet

- 10.7 Integra

- 10.8 Johnson & Johnson

- 10.9 KLS Martin

- 10.10 Medicon

- 10.11 Orthofix

- 10.12 Smith+Nephew

- 10.13 Stryker

- 10.14 Wright Medical

- 10.15 Zimmer Biomet