|

시장보고서

상품코드

1844696

외상 고정 장치 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Trauma Fixation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

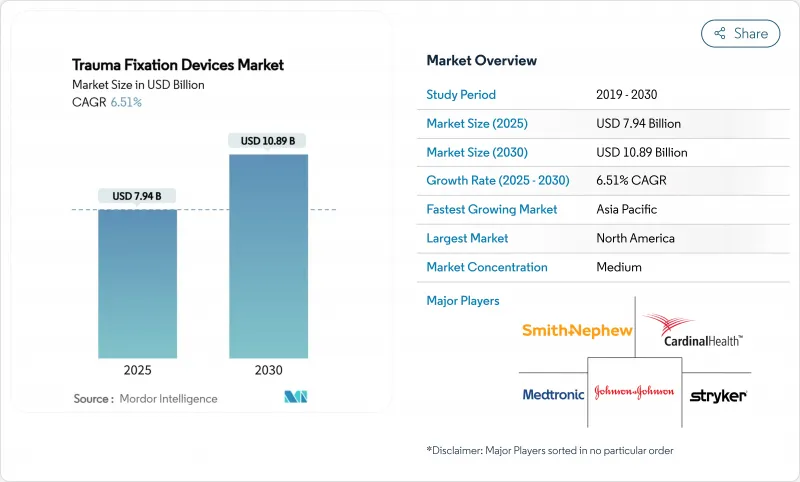

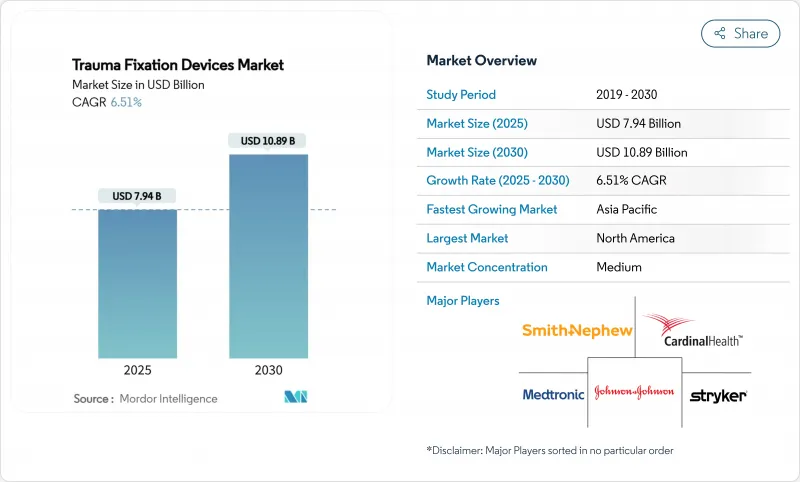

외상 고정 장치 시장 규모는 현재 2025년에 79억 4,000만 달러로 평가되었고, 2030년에 108억 9,000만 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 6.51%를 나타낼 전망입니다.

생체흡수성 금속의 내부 혁신, 약물 방출형 플레이트 및 나사의 신속한 도입, 외래 골절 치료에 대한 선호도 증가는 이러한 성장세를 유지하는 세 가지 핵심 동력이다. 골다공증, 인구 고령화, 도시 지역의 높은 사고 노출률로 인한 인구학적 압박은 환자 풀을 확대하고 있으며, 가치 기반 보상 체계는 입원 기간 단축 및 2차 제거 수술을 방지하는 임플란트로 병원 구매를 전환시키고 있다. 티타늄과 니티놀의 공급망 리스크는 계속해서 마진 압박을 가하지만, 동시에 제조사들이 새로운 합금 화학 성분을 탐구하도록 유도하고 있습니다. 경쟁 전략은 3D 프린팅 환자 맞춤형 하드웨어, 항균 코팅, 그리고 시술 속도와 정확도를 향상시키는 통합 디지털 수술 플랫폼에 집중되고 있습니다.

세계의 외상 고정 장치 시장 동향 및 인사이트

골퇴행성 질환 및 골다공증 유병률 증가

전 세계적으로 약 5억 명이 골다공증으로 고통받고 있으며, 이는 취약해진 뼈 질에 맞춤화된 고정 솔루션 수요를 재편하고 있다. 과거 고에너지 외상으로 발생하던 입원 사례가 이제 취약성 골절로 대체되면서, 장치 제조사들은 나사와 플레이트에 직접 골형성 약물을 통합하고 있다. 미국 의료 시스템은 연간 250억 달러 이상의 골절 관련 비용을 부담하며, 재골절을 방지하는 예방적 임플란트에 대한 보험사 자금 지원을 촉구하고 있다. 이에 따라 제조사들은 골유착을 강화하면서 치유 중인 뼈에 가해지는 스트레스를 점진적으로 분산시키는 생체활성 구조물의 유효성 입증을 서두르고 있다. 이 추세는 고령화 곡선이 가장 가파르고 보험급여가 고가 임플란트를 지원하는 북미와 유럽에서 가장 두드러지게 나타난다. 장기적으로 이 동인은 외상 고정 장치 시장의 연평균 복합 성장률(CAGR은)에 1.2% 포인트를 추가할 것으로 예상된다.

교통사고와 외상 발생률 증가

WHO 기록에 따르면 매년 440만 명이 부상으로 사망하며, 아시아 태평양 지역은 안전 인프라보다 자동차 보급률이 더 빠르게 증가하면서 가장 큰 부담을 안고 있습니다. 도시 스포츠 문화와 산업 현장의 확대는 골절 치료의 복잡성을 더해, 단일 수술로 여러 뼈를 안정화할 수 있는 모듈식 고정 시스템이 요구됩니다. 기기 제조사들은 수술 시간을 단축하고 재고를 효율화하는 통합 플랫폼을 도입하고 있습니다. 중기적 관점에서 인도, 중국, 동남아시아의 외상 노출 증가가 외상 고정 장치 시장의 예상 연평균 성장률에 0.8% 포인트를 추가할 전망이다.

높은 수술 비용과 장치 비용

고가의 생분해성 및 약물 방출 임플란트는 초기 비용이 높아 저소득 환경에서의 도입을 제한한다. 포괄적 지불 방식은 병원 및 외래 진료 센터로 하여금 총 치료 비용을 면밀히 검토하도록 유도하며, 재고 예산을 효율적으로 활용할 수 있는 모듈식 시스템을 선택하는 경우가 많습니다. 이러한 비용 마찰은 단기적 외상 고정 장치 시장 성장률을 0.7% 포인트 하락시킵니다.

부문 분석

2024년 외상 고정 장치는 2024년 외상 고정 장치 시장 점유율의 64.51%를 차지했으며, 해당 하위 부문는 2030년까지 연평균 복합 성장률(CAGR은) 8.25%를 기록할 것으로 예상되어 모든 장치 카테고리 중 가장 빠른 성장세를 보일 것입니다. 생체흡수성 나사가 소아과 및 노인 의학 분야에서 주목받으면서, 내부 고정 장치에 기인한 외상 고정 장치 시장 규모는 전체 산업 성장률을 앞지를 전망이다. 동적 압축 슬롯이 장착된 플레이트는 골유합 촉진을 위한 제어된 미세운동을 허용하며, 지머 바이오메트의 모션록 나사가 이러한 기능을 대표한다.

스마트 합금과 모듈식 트레이 레이아웃의 등장으로 외과의는 수술 중 고정 장치 강성을 조정할 수 있어 재고량을 최대 30%까지 절감할 수 있습니다. 약물 방출 코팅은 기계적 지지와 생물학적 치료를 결합하여 내부 하드웨어의 차별화를 더욱 강화합니다. 외상 고정 장치는 복잡한 개방 골절 및 손상 통제 정형외과 수술에 여전히 필수적이지만, 보험 급여 압박으로 인해 사례당 비용을 낮추는 재사용 가능한 프레임 키트에 대한 관심이 높아지고 있습니다. 이러한 추세들은 내부 솔루션의 우위를 유지시키지만 시장 점유율 보호를 위한 지속적인 혁신을 요구합니다.

지역 분석

북미는 2024년 글로벌 매출의 39.32%를 차지했으며, 강력한 보험급여와 높은 수술 기술 밀도를 바탕으로 2030년까지 선두를 유지할 전망입니다. 2024년 11월 FDA의 골판 및 나사에 대한 지침은 심사 기준을 강화하면서도 승인 절차를 명확히 하여 디지털 대응 임플란트의 승인 주기를 단축시켰습니다. 미국 보험사들은 2차 수술을 피하기 위해 생분해성 임플란트에 적극적으로 투자하는 반면, 캐나다 병원들은 더 작은 절개와 빠른 환자 회전을 목표로 로봇 수술 기술에 투자하고 있습니다.

아시아태평양 지역은 2025-2030년 동안 의료 시스템이 정형외과 수술실과 외상센터를 확장함에 따라 가장 빠른 연평균 7.71% 성장률을 기록할 것으로 전망된다. 중국과 인도는 도시 교통 및 건설과 연계된 외상 환자 급증으로 다용도 모듈식 고정장치 조달이 촉진되고 있다. 일본의 초고령 사회는 노인 전용 내고정 시스템 수요를 촉진하는 반면, 한국은 AI 기반 골절 치료 계획 수립을 선도하고 있다. 중국 내 OEM 업체들이 티타늄 플레이트 글로벌 공급망에 진입하며 경쟁이 가열되고 있다.

유럽은 엄격한 CE 인증 심사 및 강력한 의료진-산업계 협력을 바탕으로 안정적인 제3의 축으로 자리매김하고 있습니다. 독일과 영국은 환경 지침에 부합하는 생분해성 임플란트 임상시험을 주도하고 있습니다. 남유럽 시장은 지출 억제를 위해 재사용 최적화 외상 고정 장치 도입을 가속화하고 있습니다. 중동부 유럽에서는 EU 구조 기금이 외상 치료 시설을 업그레이드하며 다국적 기업에 새로운 입찰 기회를 제공하고 있습니다.

중동 및 아프리카와 남미는 정부가 석유 수익과 회복 기금을 3차 병원에 투입함에 따라 합산 중단위 성장률을 기록 중이다. 걸프 국가들은 프리미엄 내비게이션 지원 시스템을 구매하는 반면, 사하라 이남 아프리카는 재사용 가능한 외상 고정 프레임을 추구하는 기부자 지원 골절 프로그램에 의존한다. 라틴 아메리카 전역에서 브라질 공공 의료 서비스는 당뇨병성 발 골절 예방을 위한 약물 방출형 플레이트의 보험 적용을 확대하며 지역 조달 기준을 높이고 있다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 골퇴행성 질환 및 골다공증 유병률 증가

- 교통사고와 외상 증가

- 골절 취약 고령 인구 증가

- 생체적합성 및 생체흡수성 고정재 기술 발전

- 정형생물학적 강화 고정술(약물 방출 플레이트/나사)

- 가치 기반 조달이 신흥 시장에서 모듈식 재사용 외상 고정 장치 채택 촉진

- 시장 성장 억제요인

- 높은 수술 비용 및 장치 비용

- 엄격하고 시간 소모적인 규제 승인 절차

- 의료용 티타늄 및 니티놀 합금의 공급망 위험

- 증가하는 임플란트 관련 다제내성균(MDR) 감염 우려

- 기술적 전망

- Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 장치 유형별

- 내부 고정 장치

- 플레이트

- 나사

- 네일

- 기타

- 외상 고정 장치

- 단측 및 양측 고정 장치

- 원형 고정 장치

- 하이브리드 고정 장치

- 내부 고정 장치

- 수술 부위별

- 하지

- 고관절 및 골반

- 발관절

- 무릎

- 기타

- 상지

- 손과 손목

- 어깨

- 척추

- 기타

- 하지

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Arthrex Inc.

- B. Braun Melsungen AG

- Cardinal Health Inc.

- CONMED Corporation

- Johnson & Johnson(DePuy Synthes)

- Orthofix Medical Inc.

- Medtronic plc

- Smith & Nephew plc

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Invibio Ltd

- Globus Medical Inc.

- Acumed LLC

- Wright Medical Group NV

- NuVasive Inc.

- MicroPort Orthopedics Inc.

- OsteoMed LLC

- Integra LifeSciences Holdings Corp.

- Bio-Medical Enterprises Inc.

- Orthopaedic Implant Company

제7장 시장 기회와 전망

HBR 25.11.07The trauma fixation devices market size is currently valued at USD 7.94 billion in 2025 and is forecast to reach USD 10.89 billion by 2030, expanding at a 6.51% CAGR over 2025-2030.

Internal innovation in bioabsorbable metals, rapid adoption of drug-eluting plates and screws, and the growing preference for outpatient fracture care are the three strongest forces sustaining this momentum. Demographic pressures from osteoporosis, population ageing, and higher accident exposure in urban centers are widening the patient pool, while value-based reimbursement is shifting hospital purchasing toward implants that shorten length of stay and avert secondary removal surgery. Supply-chain risk in titanium and nitinol continues to create margin pressure but is simultaneously nudging manufacturers to explore novel alloy chemistries. Competitive strategies center on 3D-printed patient-specific hardware, antimicrobial coatings, and integrated digital surgery platforms that improve procedural speed and accuracy.

Global Trauma Fixation Devices Market Trends and Insights

Rising Prevalence of Bone-Degenerative Diseases & Osteoporosis

Global osteoporosis affects an estimated 500 million people and is reshaping demand for fixation solutions tailored to compromised bone quality. Fragility fractures now drive hospital admissions that once stemmed from high-energy trauma, prompting device makers to integrate bone-building pharmaceuticals directly into screws and plates. Health systems in the United States incur annual fracture costs above USD 25 billion, forcing payers to fund preventive implants that avert refracture. Manufacturers are therefore racing to validate bioactive constructs that strengthen osseointegration while gradually off-loading stress to healing bone. The trend is most visible in North America and Europe where aging curves are steepest and reimbursement supports premium implants. Over the long term, this driver is expected to add 1.2 percentage points to the trauma fixation devices market CAGR.

Increasing Incidence of Road Traffic Accidents & Trauma Injuries

WHO records show injuries claim 4.4 million lives each year, with Asia-Pacific bearing the heaviest load as motorization outpaces safety infrastructure. Expanding urban sports cultures and industrial workplaces add further fracture complexity, demanding modular fixation systems capable of stabilizing multiple bones in a single session. Device makers are introducing integrated platforms that cut operating time and streamline inventory. In medium-term horizons, rising trauma exposure in India, China, and Southeast Asia injects 0.8 percentage points into the projected CAGR for the trauma fixation devices market.

High Procedure & Device Costs

Premium bioabsorbable and drug-eluting implants cost more up front, limiting uptake in lower-income settings. Bundled payments push hospitals and ambulatory centers to scrutinize total episode cost, often opting for modular systems that stretch inventory budgets. This cost friction shaves 0.7 percentage points off short-term trauma fixation devices market growth.

Other drivers and restraints analyzed in the detailed report include:

- Growing Geriatric Population Vulnerable to Fractures

- Technological Advances in Bio-Compatible & Bio-Absorbable Fixation Materials

- Rising Implant-Associated MDR-Infection Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Internal fixators generated 64.51% of trauma fixation devices market share in 2024, while their sub-segment is set to log an 8.25% CAGR to 2030, the fastest across all device categories. The trauma fixation devices market size attributed to internal fixators will thus outpace overall industry expansion as bioabsorbable screws gain traction in pediatrics and geriatrics. Plates equipped with dynamic compression slots permit controlled micromotion that encourages callus formation; Zimmer Biomet's MotionLoc screw exemplifies this capability.

The advent of smart alloys and modular tray layouts lets surgeons adjust construct stiffness intraoperatively, cutting inventory by up to 30%. Drug-eluting coatings further differentiate internal hardware by merging mechanical support with biologic therapy. External fixators remain indispensable for complex open fractures and damage-control orthopedics, yet reimbursement pressures drive interest toward reusable frame kits that lower per-case expenditure. Together, these trends keep internal solutions ahead but invite continuous innovation to protect share.

The Trauma Fixation Devices Market Report is Segmented by Device Type (Internal Fixators [Plates, Screws, and More], External Fixators [Unilateral & Bilateral Fixators, and More]), Surgical Site (Lower Extremities [Hip & Pelvic, and More], and Upper Extremities), End User (Hospitals, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 39.32% of global revenue in 2024 and will maintain its lead through 2030 on the back of robust reimbursement and high surgical skill density. The November 2024 FDA guidance for bone plates and screws has sharpened review criteria yet also clarified pathways, shortening approval cycles for digital-ready implants. United States payers actively fund bioabsorbable implants to dodge secondary surgery, while Canadian hospitals invest in robotics aimed at smaller incisions and quicker turnover.

Asia-Pacific is forecast to clock the fastest 7.71% CAGR over 2025-2030 as healthcare systems expand orthopedic theaters and trauma centers. China and India witness rapid trauma growth tied to urban transportation and construction, prompting procurement of versatile modular fixators. Japan's super-aged society pushes geriatric-specific nailing systems, whereas South Korea pioneers AI-driven fracture planning. Domestic OEMs in China are entering global supply chains for titanium plates, adding competitive heat.

Europe remains a stable third pillar, buffered by tight CE-Mark scrutiny and strong clinician-industry collaboration. Germany and the United Kingdom spearhead biodegradable implant trials aligned with environmental directives. Southern European markets accelerate adoption of reuse-optimized external fixators to curb spending. In Central-Eastern Europe, EU structural funds upgrade trauma units, giving multinationals fresh tenders.

The Middle East and Africa, alongside South America, collectively offer mid-single-digit expansion as governments channel oil proceeds and recovery funds into tertiary hospitals. Gulf states buy premium navigation-enabled systems, whereas Sub-Saharan Africa leans on donor-funded fracture programs that seek reusable ex-fix frames. Across Latin America, Brazil's public health service increasingly reimburses drug-eluting plates for diabetic foot fracture prevention, nudging regional procurement norms higher.

- Arthrex

- B. Braun

- Cardinal Health

- Conmed

- Johnson & Johnson

- Orthofix

- Medtronic

- Smiths Group

- Stryker

- Zimmer Biomet

- Invibio

- Globus Medical

- Acumed

- Wright Medical Group

- NuVasive

- MicroPort

- OsteoMed LLC

- Integra LifeSciences Holdings Corp.

- Bio-Medical Enterprises Inc.

- Orthopaedic Implant Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Bone-Degenerative Diseases & Osteoporosis

- 4.2.2 Increasing Incidence Of Road Traffic Accidents & Trauma Injuries

- 4.2.3 Growing Geriatric Population Vulnerable To Fractures

- 4.2.4 Technological Advances In Bio-Compatible & Bio-Absorbable Fixation Materials

- 4.2.5 Orthobiologic-Enhanced Fixation (Drug-Eluting Plates / Screws)

- 4.2.6 Value-Based Procurement Driving Modular Reusable External Fixators In EMs

- 4.3 Market Restraints

- 4.3.1 High Procedure & Device Costs

- 4.3.2 Stringent & Time-Consuming Regulatory Approvals

- 4.3.3 Supply-Chain Risk For Medical-Grade Ti & Nitinol Alloys

- 4.3.4 Rising Implant-Associated MDR-Infection Concerns

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Internal Fixators

- 5.1.1.1 Plates

- 5.1.1.2 Screws

- 5.1.1.3 Nails

- 5.1.1.4 Others

- 5.1.2 External Fixators

- 5.1.2.1 Unilateral & Bilateral Fixators

- 5.1.2.2 Circular Fixators

- 5.1.2.3 Hybrid Fixators

- 5.1.1 Internal Fixators

- 5.2 By Surgical Site

- 5.2.1 Lower Extremities

- 5.2.1.1 Hip & Pelvic

- 5.2.1.2 Foot & Ankle

- 5.2.1.3 Knee

- 5.2.1.4 Others

- 5.2.2 Upper Extremities

- 5.2.2.1 Hand & Wrist

- 5.2.2.2 Shoulder

- 5.2.2.3 Spine

- 5.2.2.4 Others

- 5.2.1 Lower Extremities

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Cardinal Health Inc.

- 6.3.4 CONMED Corporation

- 6.3.5 Johnson & Johnson (DePuy Synthes)

- 6.3.6 Orthofix Medical Inc.

- 6.3.7 Medtronic plc

- 6.3.8 Smith & Nephew plc

- 6.3.9 Stryker Corporation

- 6.3.10 Zimmer Biomet Holdings Inc.

- 6.3.11 Invibio Ltd

- 6.3.12 Globus Medical Inc.

- 6.3.13 Acumed LLC

- 6.3.14 Wright Medical Group N.V.

- 6.3.15 NuVasive Inc.

- 6.3.16 MicroPort Orthopedics Inc.

- 6.3.17 OsteoMed LLC

- 6.3.18 Integra LifeSciences Holdings Corp.

- 6.3.19 Bio-Medical Enterprises Inc.

- 6.3.20 Orthopaedic Implant Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment