|

시장보고서

상품코드

1998713

타이어 재생 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Tire Retreading Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

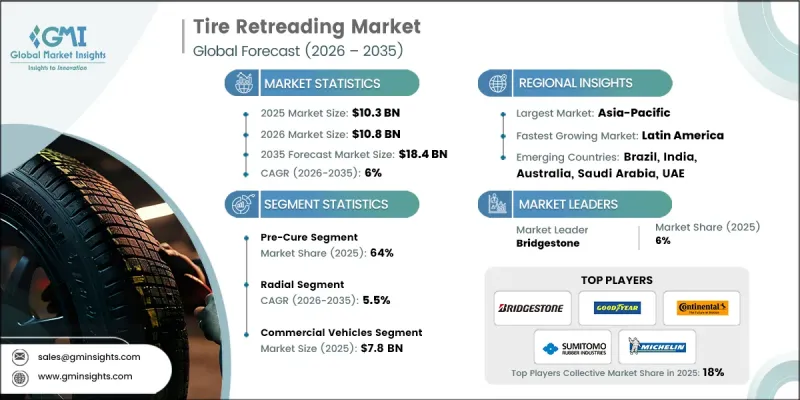

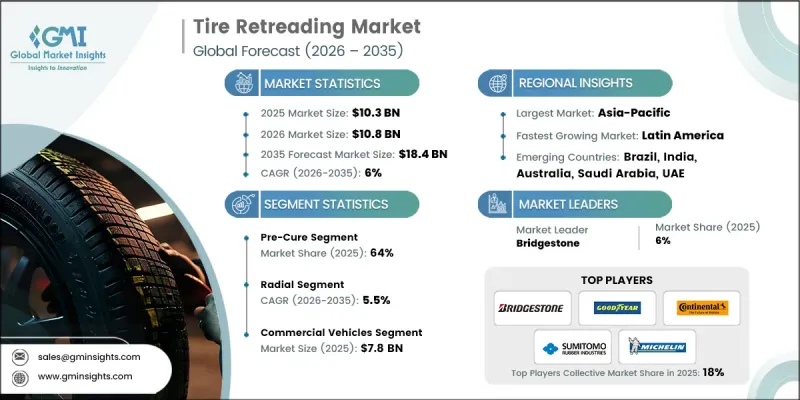

세계의 타이어 재생 시장은 2025년에 103억 달러로 평가되며, CAGR 6%로 성장하며, 2035년까지 184억 달러에 달할 것으로 추정되고 있습니다.

재생 타이어의 비용 절감 효과와 환경적 이점을 인식한 제조업체와 차량 운영업체들이 현대식 재생 타이어 공장에 대한 투자를 늘리면서 재생 타이어 시장은 강력한 성장세를 보이고 있습니다. 자동화는 검사, 연마, 트레드 부착을 위한 첨단 기계를 도입하여 업무의 효율성과 일관성을 향상시켜 생산에 혁명을 일으키고 있습니다. 이를 통해 정확도와 생산성이 향상되었습니다. 아시아태평양에서는 중국, 인도 등의 국가에서 물류 인프라의 급속한 발전과 대규모 상용선박의 확대가 가장 큰 시장 점유율을 견인하고 있습니다. RFID 추적, 예지보전, 자동 검사 라인과 같은 기술 혁신으로 타이어 리트레드는 단순한 비용 절감 방안에서 차량 최적화를 지원하는 데이터베이스 서비스로 변모하고 있습니다. 유럽에서는 광업 및 인프라 프로젝트를 위한 오프로드 타이어에 대한 투자와 함께 EU 순환 경제 행동 계획에 따라 타이어 재사용을 촉진하는 규제가 결합되어 시장 보급을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 103억 달러 |

| 예측액 | 184억 달러 |

| CAGR | 6% |

2025년에는 프리큐어 부문이 64%의 점유율을 차지하고 있으며, 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 나타낼 것으로 예측됩니다. 프리큐어 리트레드는 연마된 타이어 케이싱에 가황 전 트레드 스트립을 부착하는 공정으로, 사이클 시간 단축, 설비 투자 감소 및 예측 가능한 결과를 제공합니다. 이 비용 효율적이고 유연한 방법은 효율성과 확장성을 추구하는 독립적인 리트레드 업체 및 대규모 차량 운영자들이 선호하고 있습니다. 이러한 운영상의 장점으로 인해 앞으로도 가장 널리 채택되는 리트레드 기술이 될 것으로 예측됩니다.

레이디얼 타이어 부문은 2025년 59%의 점유율을 차지하며, 2026-2035년 연평균 5.5%의 성장률을 보일 것으로 예측됩니다. 레이디얼 타이어의 리트레드가 주류가된 것은 스틸 벨트 구조와 유연한 측벽과 같은 구조적 장점으로 인해 내구성, 연비 효율, 방열성을 향상시킬 수 있기 때문입니다. 이러한 특성으로 인해 레이디얼 타이어는 여러 번의 리트레드(retread)가 가능하여 차량의 총 운영 비용을 절감할 수 있으며, 상용차, 버스, 화물 운송에 매우 매력적인 선택이 될 수 있습니다.

중국의 타이어 리트레드 시장은 2025년 21억 달러에 달했습니다. 중국의 기존 리트레드 산업은 리트레드 타이어의 비용 효율성과 지속가능성에 힘입어 계속 확장되고 있습니다. 제조에서 재활용에 이르기까지 리트레드의 전체 수명주기가 널리 도입되고 있습니다. 산둥성, 칭다오 등 지역에서는 프리큐어와 핫몰드 공법이 널리 활용되고 있으며, 효율적인 생산이 가능하여 상용차 수요 증가에 대응할 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 프로세스별, 2022-2035

제6장 시장 추산·예측 : 타이어별, 2022-2035

제7장 시장 추산·예측 : 차량별, 2022-2035

제8장 시장 추산·예측 : 용도별, 2022-2035

제9장 시장 추산·예측 : 최종 용도별, 2022-2035

제10장 시장 추산·예측 : 지역별, 2022-2035

제11장 기업 개요

KSA 26.04.20The Global Tire Retreading Market was valued at USD 10.3 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 18.4 billion by 2035.

The market is witnessing strong growth as manufacturers and fleet operators increasingly invest in modern retreading plants, recognizing both the financial savings and environmental benefits of retreaded tires. Automation is revolutionizing production by streamlining operations and improving consistency, with advanced machinery for inspection, buffing, and tread application, enhancing precision and throughput. In the Asia-Pacific region, rapid growth in logistics infrastructure and large commercial fleets in countries such as China and India is driving the highest market share. Technological innovations like RFID tracking, predictive maintenance, and automated inspection lines are transforming tire retreading from a cost-saving measure into a data-driven service that supports fleet optimization. In Europe, investment in off-road tire applications for mining and infrastructure projects, coupled with regulations promoting tire reuse under the EU Circular Economy Action Plan, is further boosting market adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.3 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 6% |

The pre-cure segment held a 64% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. Pre-cure retreading involves applying pre-vulcanized tread strips to buffed tire casings, enabling shorter cycle times, lower capital investments, and predictable outcomes. This cost-effective and flexible method appeals to independent retreaders and large fleet operators seeking efficiency and scalability. It is anticipated to remain the most widely deployed retreading technique due to its operational advantages.

The radial tires segment accounted for 59% share in 2025 and is projected to grow at a CAGR of 5.5% between 2026 and 2035. Radial retreads dominate due to their structural benefits, including steel-belted construction and flexible sidewalls, which enhance durability, fuel efficiency, and heat dissipation. These properties allow radial tires to be retreaded multiple times, reducing overall fleet operating costs and making them highly attractive for commercial vehicles, buses, and freight transport.

China Tire Retreading Market reached USD 2.1 billion in 2025. The country's well-established retreading industry continues to expand, driven by the cost-effectiveness and sustainability of retreaded tires. The full retreading lifecycle, from production to recycling, is widely implemented. Both pre-cure and hot mold techniques are extensively utilized in provinces such as Shandong and Qingdao, enabling efficient production and meeting the growing demand from commercial fleets.

Key players operating in the Global Tire Retreading Market include Michelin, Sumitomo Rubber Industries, Southern Tire Mart, Pirelli & C, Yokohama Rubber Company, Bridgestone, Continental, Marangoni, The Goodyear Tire & Rubber, and MRF. Companies in the Tire Retreading Market are adopting strategies to strengthen their presence by investing in advanced automation technologies, including robotic inspection, buffing, and tread application systems, to increase production efficiency and product quality. Strategic partnerships with fleet operators and logistics companies allow manufacturers to expand service networks and enhance recurring demand for retreaded tires. Firms are also focusing on sustainability initiatives, promoting environmentally responsible practices, and leveraging regulatory incentives to boost adoption. Additionally, continuous R&D to improve tire longevity, fuel efficiency, and performance, combined with predictive maintenance solutions and digital monitoring platforms, helps companies maintain competitiveness and expand market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Process

- 2.2.3 Tire

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Retreading reduces raw rubber demand, extends tire life, and supports circular economy

- 3.2.1.2 Commercial operators adopted retreaded tires to lower total tire expenditure

- 3.2.1.3 Pre-cure and mold-cure retreading improvements and automated inspection.

- 3.2.1.4 Emerging markets see accelerated adoption due to rising logistics.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Passenger vehicle users remain hesitant to adopt retreads

- 3.2.2.2 High setup costs for retreading plants and equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in bus, aviation, and off-road vehicle retreading

- 3.2.3.2 Connected fleets and predictive maintenance adoption increase retread

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S. Federal Motor Vehicle Safety Standards (FMVSS 109 - New Pneumatic Tires for Motor Vehicles)

- 3.5.1.2 Canadian Motor Vehicle Safety Regulations (CMVSR - Tires Standard SOR/2007-102)

- 3.5.2 Europe

- 3.5.2.1 UNECE Regulation No. 108 (Retreaded Tires for Commercial Vehicles)

- 3.5.2.2 EU Tyre Labelling Regulation (Regulation (EC) No 1222/2009)

- 3.5.3 Asia-Pacific

- 3.5.3.1 AIS-142 (Automotive Industry Standard - Retreaded Tires, India)

- 3.5.3.2 China GB/T 1791-2018 (Retreaded Tires Specification)

- 3.5.4 Latin America

- 3.5.4.1 ABNT NBR 13671 (Brazil - Retreaded Tire Standards)

- 3.5.4.2 NOM-116-SCFI-2016 (Mexico - Tire Retreading Standard)

- 3.5.5 Middle East & Africa

- 3.5.5.1 SASO 2888/2018 (Saudi Arabia - Retreaded Tires)

- 3.5.5.2 SANS 1737 (South Africa - Retreaded Tire Specification)

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Use cases

- 3.10.1 Long-haul trucking & logistics fleet applications

- 3.10.2 Mining & off-road equipment tire management

- 3.10.3 Aviation tire retreading programs

- 3.10.4 Municipal & waste management fleet operations

- 3.10.5 Agricultural equipment tire lifecycle extension

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of Artificial Intelligence (AI)

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.12.4 Technology Access Barriers for Independent Retreaders

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Process, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Pre-Cure

- 5.3 Mold-Cure

Chapter 6 Market Estimates & Forecast, By Tire, 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Radial

- 6.3 Bias

- 6.4 Solid

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.2.1 Sedan

- 7.2.2 Hatchback

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light Commercial Vehicle

- 7.3.2 Medium Commercial Vehicle

- 7.3.3 Heavy Commercial Vehicle

- 7.4 Industrial Vehicles

- 7.4.1 Construction & Mining

- 7.4.2 Agriculture

- 7.4.3 Military & Defense

- 7.4.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 On-Road

- 8.3 Off-Road

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 OEM service providers

- 9.3 Independent retreaders

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Bridgestone

- 11.1.2 Continental

- 11.1.3 Marangoni

- 11.1.4 Michelin

- 11.1.5 MRF

- 11.1.6 Pirelli & C

- 11.1.7 Sumitomo Rubber Industries

- 11.1.8 The Goodyear Tire & Rubber

- 11.1.9 Yokohama Rubber Company

- 11.2 Regional players

- 11.2.1 Best-One Tire

- 11.2.2 Kal Tire

- 11.2.3 Oliver Rubber Company

- 11.2.4 Parrish Tire Company

- 11.2.5 Southern Tire Mart

- 11.2.6 Vipal Rubber

- 11.3 Emerging players

- 11.3.1 AcuTread

- 11.3.2 Hankook Tire

- 11.3.3 Qingdao Doublestar

- 11.3.4 Redburn Tire Company

- 11.3.5 TreadWright