|

시장보고서

상품코드

1940669

타이어 재생 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Tire Retreading - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

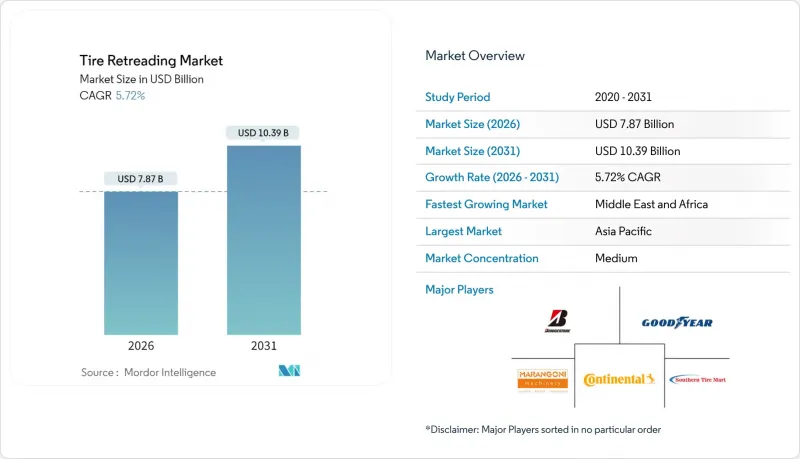

타이어 재생 시장은 2025년에 74억 4,000만 달러로 평가되었으며, 2026년 78억 7,000만 달러에서 2031년까지 103억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 5.72%로 예상됩니다.

원자재 가격 상승, 지속적인 탄소 감축 목표, 트럭 가동률 극대화가 요구되는 상황에 힘입어 재생 타이어 산업의 모멘텀이 지속되고 있습니다. 재생 타이어는 상당한 비용 절감을 실현하고 탄소 배출량과 에너지 소비를 현저하게 감소시켜 경제성과 환경성 모두에서 우위를 점하고 있습니다. 아시아태평양은 중국의 방대한 대형 차량 보유량과 인도의 급성장하는 물류 네트워크로 인해 시장에서 가장 큰 점유율을 차지하고 있습니다. 한편, 중동 및 아프리카는 광업 및 인프라 프로젝트의 급격한 성장에 따른 오프로드 타이어 사용 증가를 배경으로 가장 견조한 성장 지역으로 부상하고 있습니다. 또한, RFID 추적, 자동 검사 라인, 예지보전 분석과 같은 기술 혁신은 단순한 비용 절감 방안에서 종합적인 차량 계약에 필수적인 데이터 중심 서비스로 진화하고 있습니다.

세계 타이어 재활용 시장 동향과 인사이트

신품 타이어 대비 비용 절감 효과

현재 상업용 사업자들은 연간 예산 계획에 재생 타이어를 포함시키고 있습니다. 이는 재생 타이어 한 개가 동급 신품 타이어에 비해 구매 가격의 5분의 2를 절감할 수 있기 때문입니다. 합성 고무와 석유 가격의 상승에 따라 이 차이는 더욱 확대되고 있으며, 장거리 트럭 운송 및 택배 배송과 같은 고가동률 차량에서 재생 타이어의 비용 효율성이 강화되고 있습니다. 2025년 상반기에 약 30만 대의 트럭 판매를 기록한 중국의 대형 차량 부문은 이러한 비용 계산의 전형적인 예이며, 항공사도 얇은 영업이익을 유지하기 위해 항공 타이어의 수명을 여러 주기에 걸쳐 연장하고 있습니다.

순환경제와 CO2 규제 강화

EU 순환경제 행동계획의 규정에 따라 운송사업자는 폐기보다 재사용을 우선시해야 하며, 타이어 재생처리는 임의적 조치가 아닌 규제 준수를 위한 수단으로 변화하고 있습니다. 유로7 배출가스 기준은 조기 타이어 교체에 대한 처벌을 통해 이 의무를 강화하고 있으며, 북미와 아시아태평양의 주요 경제권에서도 유사한 규제가 도입되고 있습니다. 환경적 측면의 계산은 명확합니다: 리트레드 타이어 1개당 탄소배출량을 30%, 에너지 투입량을 70% 줄일 수 있으며, 이러한 지표는 운송회사가 Scope 3 보고 목표를 달성하는 데 도움이 될 수 있습니다.

변동하는 케이싱 고무 가격

천연고무의 기준가격과 석유 연동형 합성 고무 비용의 급격한 변동은 수익률을 잠식하고 재생타이어 공장의 가격 체계를 복잡하게 만듭니다. 소규모 독립 공장은 선물 구매 능력이 부족한 경우가 많아 현물 시장의 급변에 노출되어 조수익률이 압박을 받거나 가격 인상을 강요당하고 신규 수입품에 비해 재생 타이어의 비용 우위가 좁아지는 상황에 처하게 됩니다. 원자재 가격이 하락하면 새 타이어의 할인이 일시적으로 재생 타이어의 수요를 억제하고, 균형이 회복될 때까지 그 상태가 지속될 수 있습니다.

부문 분석

중대형 트럭은 2025년 매출의 45.02%를 차지했으며, 이는 높은 주행 주기가 간선 및 지역 운송 사업자에게 재생 타이어가 필수적이라는 것을 입증합니다. 화물 수요가 견조한 가운데, 이 부문은 2031년까지 타이어 재생 시장을 계속 지원할 것으로 예상됩니다. 오프로드 및 광산용 타이어는 5.96%의 CAGR을 기록할 것으로 예상됩니다. 이는 아프리카와 남미의 광물 채굴 활동의 확대에 힘입은 것으로, 이 지역에서는 전용 케이싱의 비용이 온로드용의 몇 배에 달합니다. 항공 분야의 틈새 시장에서는 4-10회 재생 주기가 승인되어 엄격한 안전 모니터링과 적극적인 비용 관리가 양립할 수 있음을 보여주고 있습니다. 이는 대부분의 지상 부문보다 높은 CAGR을 기록할 것으로 예상됩니다.

승용차용 리트레드는 안전에 대한 우려로 유럽과 북미에서는 여전히 작은 시장이지만, 규제 장벽이 낮은 라틴아메리카와 아시아에서는 어느 정도 기반을 유지하고 있습니다. E-Commerce 물류의 핵심인 소형 상용 밴의 경우, 도시 지역의 잦은 정차에 대응하기 위해 더 짧은 리트레드 사이클을 채택하고 있습니다. 일본에서 부상하고 있는 이중 굴절식 트레일러는 더 높은 축 중량에 대응할 수 있는 리트레드 설계가 요구되고 있으며, 이 기술적 능력은 현재 최첨단 독립형 리트레드 업체만이 제공하고 있습니다.

2025년 기준, 프리큐어 공법은 전 세계 매출의 60.95%를 차지하며, 대량 생산되는 트럭용 케이싱의 주류로 자리 잡고 있습니다. 그 경쟁 우위는 단위당 비용이 낮고 생산 속도가 빠르다는 점에서 비롯됩니다. 한편, 몰드큐어 제법은 정밀 가열 기술의 향상과 자동 프레스에 의한 사이클 타임 단축, 그리고 맞춤형 트레드 패턴의 실현으로 CAGR 5.88%로 점유율을 확대하고 있습니다. AI 기반 표면 검사부터 협업 로봇 핸들러에 이르는 자동화 기술은 품질 표준화와 노동력 투입을 줄여 두 가지 방식을 모두 지원합니다. 그러나 자본금 요건이 높아지면서 중소형 공장들이 설비 갱신 자금 조달에 어려움을 겪으면서 업계 구조조정이 가속화될 가능성이 있습니다.

성형가황라인을 통한 타이어 재생 시장 규모는 커스텀 패턴에 대한 차량 수요 증가에 따라 확대될 것으로 예상됩니다. 그러나, 프리큐어의 편리함과 낮은 에너지 부하로 인해 비용에 민감한 차량들이 여전히 선호하는 방법입니다. OEM 통합형 재생공장은 수주 구성과 케이싱 수급 상황에 따라 방식을 전환하는 하이브리드 시설을 운영하여 리스크 분산에 힘쓰고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 38.51%를 차지했습니다. 이는 중국의 거대한 트럭 함대와 인도의 인프라 정비 추진에 따른 고속도로 톤킬로미터 증가가 요인으로 작용하고 있습니다. 중국의 '대형 설비 갱신 행동 계획' 등 순환형 경제로의 전환을 중시하는 정부 정책은 차량이 신에너지 차량으로 전환하는 과정에서 리트레드 이용을 촉진하고 있습니다. 일본의 총소유비용(TLC) 모델링에 대한 강조는 예지보전 대시보드와 직접 연계된 고급 재생 서비스에 대한 수요로 이어지고 있습니다.

중동 및 아프리카는 CAGR 6.06%로 가장 빠르게 성장하고 있으며, 사막과 노천 광산에서 오프로드 타이어 사용을 증가시키는 에너지 및 광물 프로젝트의 혜택을 누리고 있습니다. 사우디의 재생 타이어 수입 금지와 국내 생산 장려책의 조합으로 현지 공장은 해외 가격 변동에 따른 영향으로부터 보호받고 있습니다. 남아프리카공화국과 보츠와나의 광업 회랑은 안정적인 수요를 뒷받침하고 있지만, 물류 제약으로 인해 장비의 다운타임을 줄이기 위해 이동식 검사 장치와 현장 연마 장비가 필요합니다.

북미는 성숙한 시장인 동시에 기술 혁신이 진행되고 있으며, RFID 프로그램과 정부 혜택이 공장 현대화를 촉진하고 있습니다. 캐나다에는 주로 트럭용 케이싱에 특화된 여러 개의 전용 재생시설이 존재하며, 미국에서 제안된 세액공제가 법제화되면 국내 생산량을 증가시킬 것으로 예상됩니다. 유럽에서는 유로7 규제와 폐기물 프레임워크 지침과 같은 규제적 측면의 순풍과 저가 수입품의 경쟁이 혼재되어 있으며, 재활용 업체들은 비용과 품질 우위를 확보하기 위해 자동 입체 촬영 기술 및 로봇 공학에 대한 투자를 촉진하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

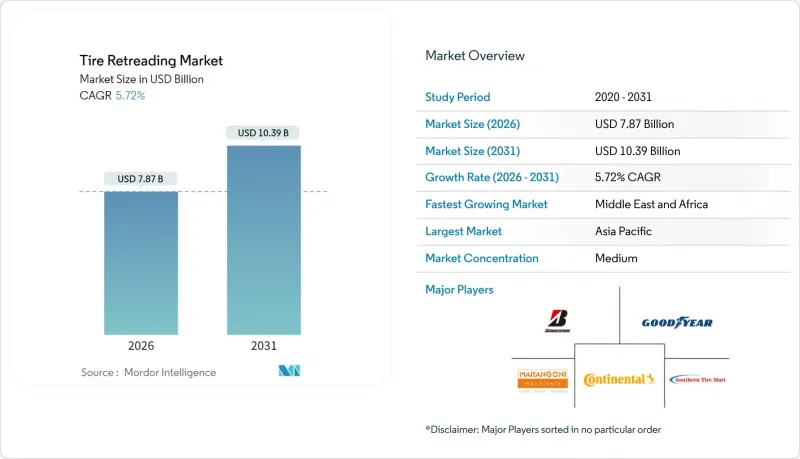

KSM 26.03.10The Tire Retreading Market was valued at USD 7.44 billion in 2025 and estimated to grow from USD 7.87 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

Driven by rising raw-material prices, ongoing carbon-reduction targets, and the imperative to maximize truck uptime, the momentum in the retreading industry continues. Retreaded casings offer significant cost savings and achieve notable reductions in carbon emissions and energy consumption, underscoring their dual economic and environmental advantages. The Asia-Pacific region commands the largest share of the market, thanks to China's expansive heavy-duty fleet and India's rapidly expanding logistics networks. In contrast, the Middle East & Africa emerge as the region with the most robust growth, driven by heightened off-road tire usage spurred by booming mining and infrastructure projects. Furthermore, advancements like RFID tracking, automated inspection lines, and predictive maintenance analytics are evolving from a mere cost-saving measure to a pivotal, data-centric service integral to comprehensive fleet contracts.

Global Tire Retreading Market Trends and Insights

Cost-savings Over New Tires

Commercial operators now embed retreading in annual budget planning because a single retread delivers two-fifths purchase-price relief versus a comparable new tire. That differential widens as synthetic rubber and petroleum costs trend upward, reinforcing retreading's payback in high-utilization fleets such as long-haul trucking and express-parcel delivery. China's heavy-duty sector, which logged almost 300,000 truck sales in the first half of 2025, epitomizes this cost calculus, while airlines stretch aviation-tire service life across multiple cycles to preserve thin operating margins .

Stricter Circular-Economy & CO2 Regulations

EU Circular Economy Action Plan rules oblige transport operators to prioritize reuse over disposal, turning tire retreading into a compliance tool rather than a discretionary measure. Euro 7 emission thresholds reinforce the mandate by penalizing premature tire replacement, and similar stimuli surface in North America and key Asia-Pacific economies. Environmental math is straightforward: every retread slashes carbon output by 30% and energy inputs by 70%, metrics that help carriers meet Scope 3 reporting targets .

Volatile Casing & Rubber Prices

Sudden swings in natural-rubber benchmarks and petroleum-linked synthetic rubber costs erode profit margins and complicate pricing grids for retread shops. Smaller independents often lack forward-buying capacity, exposing them to spot-market shocks that compress gross margin or force price hikes that narrow retread's cost edge against new imports. When raw material prices pull back, new-tire discounts can temporarily curb retread demand until equilibrium reasserts.

Other drivers and restraints analyzed in the detailed report include:

- Fleet-Mileage Growth From E-Commerce Logistics

- Government Tax-Credit Schemes For Domestic Retreads

- Influx Of Ultra-Low-Cost Import Tires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium and heavy-duty trucks generated 45.02% of 2025 revenue, confirming that high-mileage cycles make retreading indispensable for line-haul and regional-haul carriers. This segment will continue anchoring the tire retreading market through 2031 as freight demand remains resilient. Off-the-road and mining tires are charted for a 5.96% CAGR, riding on mineral extraction activity in Africa and South America, where specialized casings cost multiples of on-road equivalents. With its 4-10 approved retread cycles, the aviation niche reveals how rigorous safety oversight can coexist with aggressive cost management, forecasting a robust CAGR that outpaces most ground-based segments.

Passenger car retreading remains marginal in Europe and North America amid safety perceptions but maintains footholds in Latin America and Asia, where regulatory barriers are lower. Light commercial vans, pivotal in e-commerce logistics, now adopt shorter retread cycles adjusted to urban stop frequency. Emerging double-articulated rigs in Japan require retread designs capable of handling higher axle loads, a technical capability that only the most advanced independent retreaders currently offer.

The pre-cure process held 60.95% of global revenue in 2025 and remains the go-to for high-volume truck casings. Its competitive advantage stems from lower per-unit cost and faster throughput. Mold-cure is gaining a 5.88% CAGR owing to improved precision heating and automated presses that shorten cycle times while allowing bespoke tread patterns. Automation, from AI-based surface inspection to collaborative robotic handlers, props up both methods by standardizing quality and trimming labor input. However, capitalization requirements could accelerate industry consolidation as smaller shops struggle to fund upgrades.

The tire retreading market size attributed to mold-cure lines is projected to increase as fleet demand for custom patterns grows. Yet, pre-cure's simplicity and lower energy load keep it the preferred method for cost-sensitive fleets. OEM-integrated retread plants hedge their bets by running hybrid facilities that switch methods based on order mix and casing availability.

The Tire Retreading Market Report is Segmented by Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Production Method (Pre-Cure and Mold-Cure), Tire Type (Radial, Bias, and Solid/Foam-filled), Sales Channel (Independent Retreaders and More), End-User Industry (Transport & Logistics Fleets and More), Application (On-Road, Off-Road), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 38.51% revenue in 2025, due to China's gigantic truck fleet and India's infrastructure push that multiplies highway ton-kilometers. Government policies emphasizing circular-economy compliance, such as China's Large-scale Equipment Renewal Action Plan, channel fleets toward retreading while they phase into new-energy vehicles. Japan's emphasis on total-life cost modeling translates into sophisticated demand for retread services that plug directly into predictive maintenance dashboards.

Middle East & Africa, the fastest-advancing region at 6.06% CAGR, gains from energy and mineral projects that lift off-road tire usage in deserts and open-pit mines. Saudi Arabia's ban on retread imports, combined with incentives for domestic production, shields local plants from foreign price shocks. South Africa and Botswana mining corridors underpin steady demand, although logistical constraints require mobile inspection units and on-site buffing rigs to curtail equipment downtime.

North America remains a mature yet tech-progressive territory where RFID programs and government incentives foster plant modernization. Canada hosts multiple dedicated retread facilities focused mainly on truck casings, and proposed U.S. credits would boost domestic volumes if passed into law. Europe blends regulatory tailwinds, Euro 7 and waste-framework directives, with competitive headwinds from low-priced imports, prompting retreaters to invest in automated stereography and robotics to achieve cost and quality leadership.

- Bridgestone Corporation

- Michelin

- Goodyear

- Marangoni

- Continental AG

- Vipal Rubber

- Kal Tire

- Best-One Tire Group

- Southern Tire Mart

- Yokohama Rubber

- Hankook Tire

- Pirelli

- Sumitomo Rubber

- MRF

- Oliver Rubber

- TreadWright

- Qingdao Doublestar

- Rethread (Pty) Ltd

- Parrish Tire

- Redburn Tire

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Savings Over New Tires

- 4.2.2 Stricter Circular-Economy & Co2 Regulations

- 4.2.3 Fleet-Mileage Growth From E-Commerce Logistics

- 4.2.4 Government Tax-Credit Schemes for Domestic Retreads

- 4.2.5 RFID-Enabled Lifecycle Tracking & Warranty Analytics

- 4.2.6 Green Procurement Policies by Freight Majors

- 4.3 Market Restraints

- 4.3.1 Volatile Casing & Rubber Prices

- 4.3.2 Influx of Ultra-Low-Cost Import Tires

- 4.3.3 Passenger-Car Safety Perception Gaps

- 4.3.4 Limited EV-Ready Retread Designs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Medium & Heavy-Duty Truck

- 5.1.4 Bus & Coach

- 5.1.5 Off-the-Road & Mining

- 5.1.6 Agriculture & Specialty

- 5.2 By Production Method

- 5.2.1 Pre-cure

- 5.2.2 Mold-cure

- 5.3 By Tire Type

- 5.3.1 Radial

- 5.3.2 Bias

- 5.3.3 Solid / Foam-filled

- 5.4 By Sales Channel

- 5.4.1 Independent Retreaders

- 5.4.2 OEM / Captive Fleet Facilities

- 5.5 By End-user Industry

- 5.5.1 Transport & Logistics Fleets

- 5.5.2 Construction & Mining

- 5.5.3 Agriculture

- 5.5.4 Aviation

- 5.5.5 Military & Defense

- 5.5.6 Waste Management & Others

- 5.6 By Application

- 5.6.1 On-road

- 5.6.2 Off-road

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Russia

- 5.7.3.6 Spain

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bridgestone Corporation

- 6.4.2 Michelin

- 6.4.3 Goodyear

- 6.4.4 Marangoni

- 6.4.5 Continental AG

- 6.4.6 Vipal Rubber

- 6.4.7 Kal Tire

- 6.4.8 Best-One Tire Group

- 6.4.9 Southern Tire Mart

- 6.4.10 Yokohama Rubber

- 6.4.11 Hankook Tire

- 6.4.12 Pirelli

- 6.4.13 Sumitomo Rubber

- 6.4.14 MRF

- 6.4.15 Oliver Rubber

- 6.4.16 TreadWright

- 6.4.17 Qingdao Doublestar

- 6.4.18 Rethread (Pty) Ltd

- 6.4.19 Parrish Tire

- 6.4.20 Redburn Tire

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment