|

시장보고서

상품코드

1998758

음료 캔 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Beverage Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

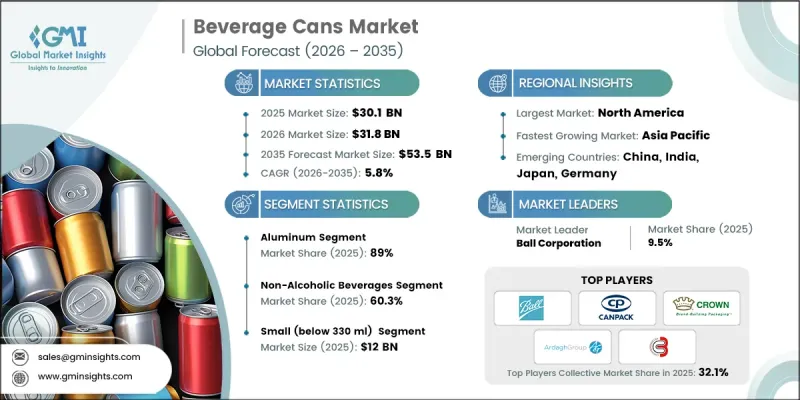

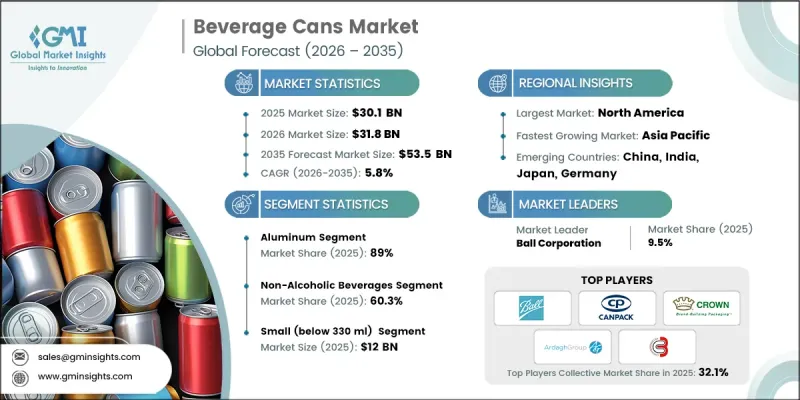

세계의 음료 캔 시장은 2025년에 301억 달러로 평가되며, CAGR 5.8%로 성장하며, 2035년까지 535억 달러에 달할 것으로 추정되고 있습니다.

이러한 시장 확대는 편의성이 높은 1회용 음료에 대한 세계 수요 증가와 에너지 음료 및 기능성 음료의 급속한 성장에 힘입은 바 큽니다. 음료 제조업체의 지속가능성 노력 강화와 더불어, 재활용 가능한 포장재를 장려하는 규제적 노력도 시장을 더욱 촉진하고 있습니다. 프리미엄 패키지를 통한 차별화, 신흥 국가에서의 생산 능력 확대, 일부 음료 부문에서 플라스틱병에서 알루미늄 캔으로 전환하는 것도 성장을 촉진하고 있습니다. 또한 경량화 설계의 혁신, 재활용 인프라 강화, 재택 소비 동향에 힘입어 음료 기업은 친환경 포장 솔루션을 유지하면서 공급망을 최적화할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 301억 달러 |

| 예측액 | 535억 달러 |

| CAGR | 5.8% |

탄산음료, 맥주, 기능성 음료에서 알루미늄 캔 음료의 소비 증가가 시장 성장의 주요 촉진요인으로 작용하고 있습니다. 고속 통조림 라인에 대한 투자, 에너지 음료 및 즉석 알코올 음료 제품 라인의 확대, 경량 캔 생산 기술 향상으로 시장 침투를 촉진하고 있습니다. 알루미늄 캔은 재활용성, 경량성, 빛과 산소에 대한 효과적인 차단 기능으로 제품의 보존 기간을 연장하고 순환 경제의 원칙에 부합하므로 시장을 독점하고 있습니다.

2025년 기준, 알루미늄 부문은 89%의 점유율을 차지했습니다. 그 보급은 우수한 재활용성, 탄산음료 및 기능성 음료와의 호환성, 그리고 운송비용을 절감하는 경량성으로 인해 확산되고 있습니다. 제품의 품질을 유지하면서 고품질 인쇄와 라벨링을 가능하게 하는 알루미늄의 특성은 그 매력을 더욱 높여줍니다. 전 세계에서 높은 재활용률과 지속가능한 포장에 대한 지속적인 규제적 지원은 전 세계 음료 생산에서 알루미늄의 우위를 유지하는 데 기여하고 있습니다.

소형 캔(330ml 미만) 부문은 2025년 120억 달러에 달했습니다. 1회 제공량 및 용량 조절이 가능한 음료에 대한 선호도가 높아지면서 컴팩트 캔에 대한 수요가 증가하고 있습니다. 이 사이즈는 에너지 음료, 기능성 음료, 프리미엄 탄산음료에 적합하며, 편의성을 중시하는 소비자와 빈번한 구매 기회를 타겟으로 하고 있습니다. 컴팩트 캔은 도시지역에서의 멀티팩 판매, 자동판매기 대응, 충동구매를 촉진합니다. 제조업체들은 소매점, 편의점, 오락시설 등의 채널을 통해 폭넓은 유통을 확보하여 주요 시장 전체에 제품을 안정적으로 공급함으로써 경쟁력을 유지하고 있습니다.

2025년 기준, 북미 음료용 캔 시장은 36%의 점유율을 차지했습니다. 이 지역의 성장은 강력한 지속가능성 규제, 확립된 재활용 체계, 페트병에서 알루미늄 캔으로 대체된 재활용 체계에 의해 지원되고 있습니다. 미국의 여러 주와 캐나다의 여러 주에서 도입된 보증금 반환 제도는 알루미늄의 재활용과 폐쇄형 공급망을 강화하고 있습니다. 주요 기업은 탄산음료, 에너지 음료, 즉석 알코올 음료 수요 증가에 대응하기 위해 생산 능력 확대와 첨단 경량 캔 제조 기술에 대한 투자를 진행하고 있습니다. 캔 제조의 기술적 진보와 지속가능한 노력의 결합으로 이 지역은 세계 음료 포장 시장에서 선도적인 위치를 유지하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 재료별, 2022-2035

제6장 시장 추산·예측 : 제품 유형별, 2022-2035

제7장 시장 추산·예측 : 용량별, 2022-2035

제8장 시장 추산·예측 : 용도별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Beverage Cans Market was valued at USD 30.1 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 53.5 billion by 2035.

The market's expansion is fueled by rising global demand for convenient, single-serve beverages and the rapid growth of energy drinks and functional beverages. Increasing sustainability commitments by beverage manufacturers, along with regulatory initiatives promoting recyclable packaging, are further supporting the market. Premium packaging differentiation, expanding production capacity in emerging economies, and the shift from plastic bottles to aluminum cans in several beverage segments are also driving growth. Additionally, innovations in lightweight design, enhanced recycling infrastructure, and at-home consumption trends have strengthened adoption, allowing beverage companies to optimize supply chains while maintaining environmentally responsible packaging solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.1 Billion |

| Forecast Value | $53.5 Billion |

| CAGR | 5.8% |

Rising aluminum beverage consumption across carbonated drinks, beer, and functional beverages is a key driver of market growth. Investments in high-speed canning lines, expansion of energy drink and ready-to-drink alcoholic beverage product lines, and improvements in lightweight can production have bolstered penetration. Aluminum cans dominate the market due to their recyclability, light weight, and ability to create effective barriers against light and oxygen, which extends product shelf life and aligns with circular economy principles.

The aluminum segment held 89% share in 2025. Its widespread adoption is driven by superior recyclability, compatibility with carbonated and functional beverages, and lightweight properties that reduce transportation costs. Aluminum's ability to maintain product integrity while supporting premium printing and labeling further enhances its appeal. High global recycling rates and ongoing regulatory support for sustainable packaging help maintain aluminum's dominance in beverage manufacturing worldwide.

The small-size cans segment (below 330 ml) reached USD 12 billion in 2025. The growing preference for single-serve and portion-controlled beverages has fueled demand for compact cans. These sizes cater to energy drinks, functional beverages, and premium carbonated drinks, targeting convenience-oriented consumers and frequent purchase occasions. Compact cans support multipack sales, vending machine compatibility, and impulse buying in urban environments. Manufacturers maintain competitive positioning by ensuring wide distribution through retail, convenience, and entertainment channels, ensuring consistent product availability across key markets.

North America Beverage Cans Market accounted for 36% share in 2025. Growth in this region is supported by strong sustainability regulations, established recycling frameworks, and the substitution of plastic bottles with aluminum cans. Deposit return schemes in multiple U.S. states and Canadian provinces strengthen aluminum recycling and closed-loop supply chains. Leading players are investing in capacity expansion and advanced lightweight canning technologies to meet increasing demand from carbonated beverages, energy drinks, and ready-to-drink alcoholic products. Technological advancements in can production, combined with sustainable practices, help the region maintain its leadership in global beverage packaging.

Key players operating in the Global Beverage Cans Market include Ball Corporation, Crown Holdings, Ardagh Group, Canpack, Showa Aluminum-Can Co., Ltd., Novelis, G3 Enterprises, Inc., Ceylon Beverage Can, Tata Steel, Visy, Baixicans, Envases Group, Scan Holdings, Toyo Seikan, GZI Industries, Orora Packaging, Speira GmbH, and Thai Beverage Can. Companies in the Global Beverage Cans Market are leveraging multiple strategies to strengthen their market position and growth. Investments in research and development focus on lightweight and eco-friendly aluminum designs to enhance recyclability while reducing carbon footprints. Expansion of production facilities and high-speed canning lines in emerging markets ensures capacity meets growing demand. Firms are collaborating with beverage manufacturers to offer customized, branded, and limited-edition cans that differentiate products on the shelf. Sustainability initiatives, such as closed-loop recycling partnerships and the adoption of low-carbon production practices, reinforce compliance with regulatory requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product type trends

- 2.2.3 Capacity trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global aluminum beverage consumption volumes

- 3.2.1.2 Premiumization of craft beer and RTD cocktails

- 3.2.1.3 High recyclability supporting circular packaging mandates

- 3.2.1.4 Brand shift from PET to infinitely recyclable cans

- 3.2.1.5 Expansion of energy drink and functional beverages

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile aluminum coil pricing pressures margins

- 3.2.2.2 Capacity constraints during peak seasonal demand

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in slim and sleek can formats

- 3.2.3.2 Increasing adoption in bottled water segment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 1-piece cans

- 6.3 2-piece cans

- 6.4 3-piece cans

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Small (below 330 ml)

- 7.3 Medium (330 ml - 500 ml)

- 7.4 Large (above 500 ml)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Alcoholic beverages

- 8.3 Non-alcoholic beverages

- 8.3.1 Carbonated soft drinks

- 8.3.2 Fruit & vegetable juices

- 8.3.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Ball Corporation

- 10.1.2 Crown Holdings

- 10.1.3 Ardagh Group

- 10.1.4 Novelis

- 10.1.5 Canpack

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 G3 Enterprises, Inc.

- 10.2.1.2 GZI Industries

- 10.2.1.3 Envases Group

- 10.2.2 Asia Pacific

- 10.2.2.1 Ceylon Beverage Can

- 10.2.2.2 Showa Aluminum-Can Co., Ltd.

- 10.2.2.3 Toyo Seikan

- 10.2.2.4 Thai Beverage Can

- 10.2.2.5 Orora Packaging

- 10.2.2.6 Tata Steel

- 10.2.2.7 Visy

- 10.2.3 Europe

- 10.2.3.1 Baixicans

- 10.2.3.2 Speira GmbH

- 10.2.3.3 Scan Holdings

- 10.2.3.4 Nampak

- 10.2.1 North America