|

시장보고서

상품코드

1998795

원격 무기 스테이션 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

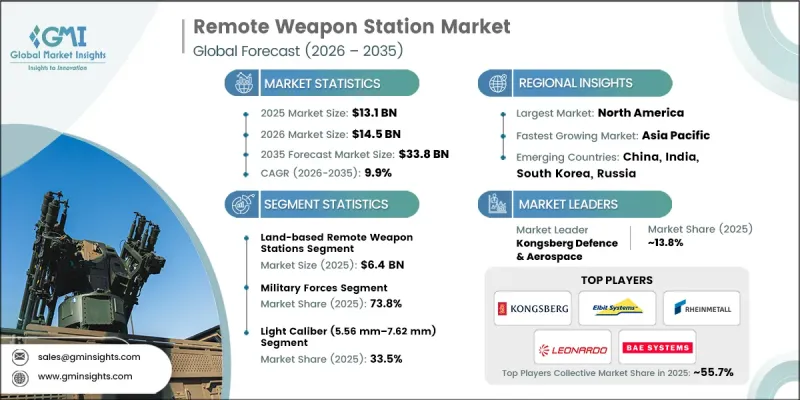

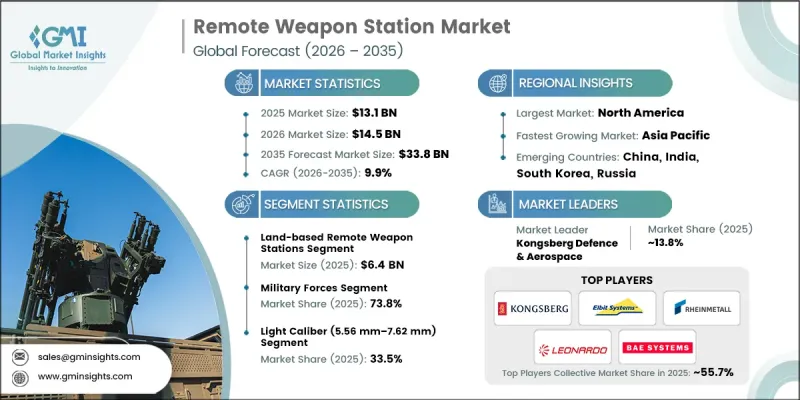

세계의 원격 무기 스테이션 시장은 2025년에 131억 달러로 평가되었고, CAGR 9.9%로 성장하여 2035년에는 338억 달러에 달할 것으로 예측됩니다.

시장 성장은 전 세계 국방 현대화 예산 증가, 비대칭적 위협 시나리오의 확대, 육해공 플랫폼의 부대 보호 솔루션에 대한 수요 증가에 의해 주도되고 있습니다. 무인 및 자율 플랫폼의 도입과 더불어 AI를 활용한 표적 포착 및 첨단 센서 융합 시스템의 도입으로 작전 능력은 변화하고 있으며, 현대 전장에서 보다 정밀하고 신속한 대응이 가능해졌습니다. 다른 촉진요인으로는 국경 간 안보에 대한 투자, 해군 및 해안 방어의 현대화, 국내 방위 생산을 지원하기 위한 정부의 이니셔티브 등이 있으며, 이러한 요인들이 결합되어 전 세계 원격 무기 스테이션의 배치를 가속화하고 있습니다. 국방비 증가와 더불어 기술 혁신과 전략적 조달 정책으로 인해 여러 군사 분야와 작전 지역에서 도입이 계속 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 131억 달러 |

| 예측액 | 338억 달러 |

| CAGR | 9.9% |

이 시장은 무기체계의 현대화, 함대의 즉각적인 대응력 향상, 무인 차량에 원격 무기 스테이션(RWS)을 통합하기 위한 정부의 투자에 크게 영향을 받고 있습니다. 비대칭 위협 증가, 해군 및 국경 보안을 위한 조달 확대, 정부 지원 현지 제조 프로그램 등이 시장 확대에 크게 기여하고 있습니다. AI를 활용한 표적 포착 및 센서 융합 기술을 통해 운영자는 보다 신속하고 정확한 판단을 내릴 수 있으며, 이는 원격 무기 스테이션의 도입을 더욱 촉진하고 있습니다.

육상용 원격 무기 스테이션(RWS) 부문은 2025년 64억 달러에 달했습니다. 이 시스템은 장갑차, 보병 전투 차량, 전투 트럭에 널리 배치되어 지속적인 전장 감시, 정밀한 표적 공격 및 고급 센서와의 통합을 실현하고 있습니다. 이 시스템은 작전적 다재다능함과 신뢰성으로 인해 강화된 방어 능력과 원격 공격 능력을 원하는 현대 군에 핵심적인 역할을 하고 있습니다.

2025년 기준 소구경(5.56mm-7.62mm) 부문은 33.5%의 점유율을 차지했습니다. 소구경 RWS는 정확도, 적은 반동, 그리고 수동/자동 이중 조작이 가능하여 선호되고 있습니다. 이러한 시스템은 민간인의 안전을 보장하면서 도시 및 분쟁지역에서의 전술 작전을 지원합니다. AI를 활용한 추적 기능과 전기 광학 센서의 통합으로 임무 효율성이 향상되어 소구경 RWS는 전 세계 군에 최적의 선택이 되고 있습니다.

2025년북미 원격 무기 스테이션(RWS) 시장은 33%의 점유율을 차지했습니다. 이 지역의 성장은 대규모 국방 현대화 프로그램, 국방비 증가, 무인 시스템 및 부대 보호에 대한 전략적 집중에 의해 주도되고 있습니다. 미 국방부의 AI 기반 표적 포착 및 센서 융합 기술에 대한 자금 지원은 이 지역의 성숙한 방위 산업 기반과 함께 RWS 도입에 있어 북미의 리더로서의 입지를 강화하고 있습니다. 국경 보안, 대테러 및 연합군 작전은 2035년까지 시장 확대를 더욱 촉진할 것입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 플랫폼 유형별, 2022-2035

제6장 시장 추산 및 예측 : 무기 유형별, 2022-2035

제7장 시장 추산 및 예측 : 모빌리티 유형별, 2022-2035

제8장 시장 추산 및 예측 : 최고 자율 레벨별, 2022-2035

제9장 시장 추산 및 예측 : 센서 스위트 구성별, 2022-2035

제10장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.04.23The Global Remote Weapon Station Market was valued at USD 13.1 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 33.8 billion in 2035.

Market growth is fueled by rising global defense modernization budgets, expanding asymmetric threat scenarios, and increasing demand for force protection solutions across land, sea, and air platforms. The adoption of unmanned and autonomous platforms, along with AI-enabled targeting and advanced sensor fusion systems, is transforming operational capabilities, enabling more precise and rapid responses on modern battlefields. Additional drivers include cross-border security investments, naval and coastal defense upgrades, and government initiatives supporting indigenous defense production, which together accelerate the deployment of remote weapon stations worldwide. Rising defense expenditures, coupled with technological innovation and strategic procurement policies, continue to strengthen adoption across multiple military domains and operational theaters.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.1 Billion |

| Forecast Value | $33.8 Billion |

| CAGR | 9.9% |

The market is strongly influenced by government investment in modernizing weapons systems, enhancing fleet readiness, and integrating RWS into unmanned vehicles. Rising asymmetric threats, increased naval and border security acquisitions, and government-backed local manufacturing programs are significant contributors to market expansion. AI-driven targeting and sensor fusion technologies allow operators to make faster, more accurate decisions, which further boosts adoption of remote weapon stations.

The land-based remote weapon stations segment reached USD 6.4 billion in 2025. These systems are widely deployed on armored vehicles, infantry fighting vehicles, and combat trucks, offering continuous battlefield surveillance, precise target engagement, and integration with advanced sensors. Their operational versatility and reliability make them a cornerstone for modern armies seeking enhanced protection and remote engagement capabilities.

The light-caliber (5.56 mm-7.62 mm) segment held 33.5% share in 2025. Light-caliber RWS are favored for their precision, minimal recoil, and dual manual and automatic operation. These systems support tactical operations in urban environments and conflict zones while ensuring civilian safety. AI-assisted tracking and electro-optical sensor integration enhance mission efficiency, making light-caliber RWS a preferred choice for militaries worldwide.

North America Remote Weapon Station Market held a 33% share in 2025. Growth in this region is driven by large-scale defense modernization programs, elevated defense spending, and strategic focus on unmanned systems and force protection. Funding from the U.S. Department of Defense for AI-enabled targeting and sensor fusion technologies, combined with the region's mature defense industrial base, strengthens North America's position as a leader in RWS adoption. Border security, counter-terrorism initiatives, and coalition operations further reinforce market expansion through 2035.

Prominent players in the Global Remote Weapon Station Market include Kongsberg Defence & Aerospace, Rheinmetall AG, Rafael Advanced Defense Systems, KNDS Group, BAE Systems plc, FN Herstal, Leonardo S.p.A., Elbit Systems Ltd., ST Engineering, Electro Optic Systems, Pro Optica, Norinco, Thales Group, ASELSAN A.S, General Dynamics Corporation, and Saab AB. Companies in the Global Remote Weapon Station Market are adopting multiple strategies to consolidate their presence and expand market share. These include investing heavily in R&D to develop AI-assisted targeting, sensor fusion, and modular platforms adaptable to multiple vehicles and environments. Strategic partnerships with defense ministries, technology firms, and OEMs help integrate advanced systems into operational fleets. Firms are also focusing on localized production and technology transfer initiatives to meet government requirements and reduce supply chain dependency. Expansion of regional service centers, training programs, and rapid upgrade capabilities ensures operational readiness while enhancing customer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Weapon type trends

- 2.2.3 Mobility type trends

- 2.2.4 Highest autonomy level trends

- 2.2.5 Sensor suite configuration trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense modernization spending

- 3.2.1.2 Increased asymmetric warfare and force-protection needs

- 3.2.1.3 Expansion of unmanned systems integration

- 3.2.1.4 Growing naval RWS deployments for coastal defense

- 3.2.1.5 Border security and homeland security procurements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex integration with legacy platforms

- 3.2.2.2 Cybersecurity and electronic warfare vulnerabilities

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven autonomous engagement systems

- 3.2.3.2 RWS on unmanned ground and aerial platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Land-based remote weapon stations

- 5.2.1 Light tactical vehicles

- 5.2.2 MRAP & armored vehicles (APCs + IFVs + MBTs)

- 5.2.3 Unmanned ground vehicles (UGVs)

- 5.3 Naval remote weapon stations

- 5.3.1 Small naval vessels (patrol boats, coast guard / border patrol)

- 5.3.2 Corvettes

- 5.3.3 Large naval vessels (frigates, destroyers, amphibious assault vessels)

- 5.4 Fixed / stationary installations

- 5.5 Airborne remote weapon stations

- 5.5.1 Helicopters

- 5.5.2 Unmanned aerial vehicles (UAVs)

Chapter 6 Market Estimates and Forecast, By Weapon Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Light caliber (5.56mm - 7.62mm)

- 6.3 Medium caliber (12.7mm / .50 cal)

- 6.4 Heavy caliber (14.5mm - 20mm)

- 6.5 Cannon (25mm - 40mm)

Chapter 7 Market Estimates and Forecast, By Mobility Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Mobile RWS

- 7.3 Stationary RWS

Chapter 8 Market Estimates and Forecast, By Highest Autonomy Level, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Manual remote operation only

- 8.3 Semi-autonomous

- 8.4 Autonomous engagement capable

Chapter 9 Market Estimates and Forecast, By Sensor Suite Configuration, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Basic (day camera only)

- 9.3 Standard (day + thermal)

- 9.4 Advanced (day + thermal + LRF)

- 9.5 Premium (Multi-Spectral + LRF + auto-tracking + AI)

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Military forces

- 10.3 Homeland security & border protection

- 10.4 Law enforcement & internal security

- 10.5 Commercial & critical infrastructure

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 BAE Systems plc

- 12.1.2 Rheinmetall AG

- 12.1.3 Leonardo S.p.A

- 12.1.4 Thales Group

- 12.1.5 Saab AB

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 General Dynamics Corporation

- 12.2.2 Asia Pacific

- 12.2.2.1 ASELSAN A.S

- 12.2.2.2 Norinco

- 12.2.2.3 ST Engineering

- 12.2.3 Europe

- 12.2.3.1 FN Herstal

- 12.2.3.2 KNDS Group

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Kongsberg Defence & Aerospace

- 12.3.2 Elbit Systems Ltd.

- 12.3.3 Electro Optic Systems

- 12.3.4 Rafael Advanced Defense Systems

- 12.3.5 Pro Optica