|

시장보고서

상품코드

1998799

냉동 베이커리 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Frozen Bakery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

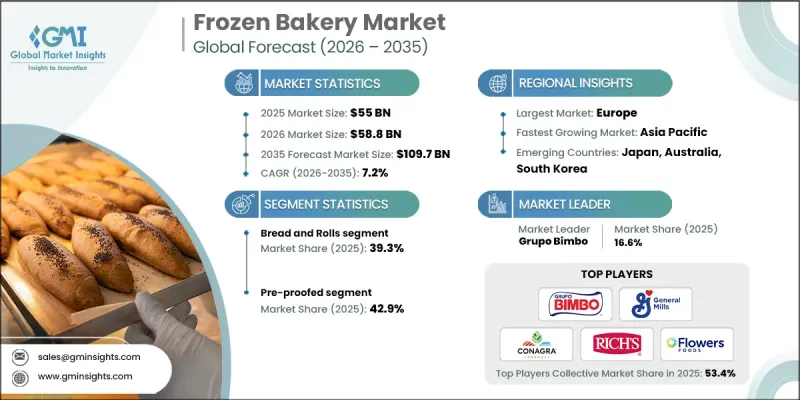

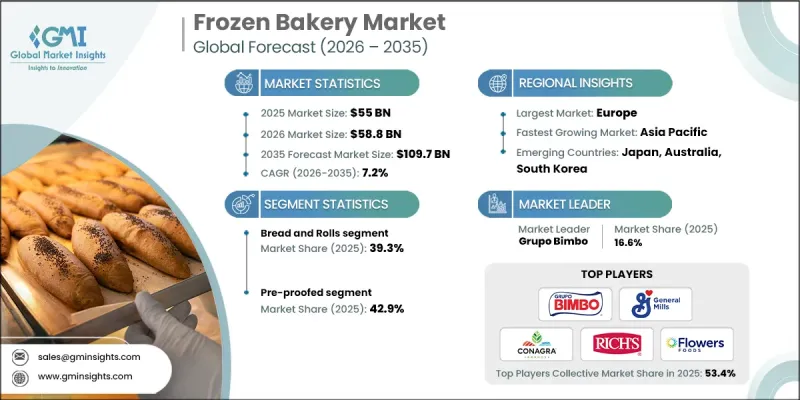

세계의 냉동 베이커리 시장은 2025년에 550억 달러로 평가되었고, CAGR 7.2%로 성장하여 2035년까지 1,097억 달러에 달할 것으로 예측됩니다.

냉동 베이커리 시장은 전통적인 제빵 방식과 현대 식품 가공 기술이 점점 더 융합됨에 따라 급속도로 발전하고 있습니다. 과거에는 순전히 편의성만을 강조하는 카테고리로 여겨지던 것이 이제는 외식 산업, 소매 유통 및 상업용 공급 시스템의 필수적인 요소로 자리 잡고 있습니다. 업계 관계자들은 업무 효율성 향상과 노동력 부족 문제에 대응하기 위해 자동화 및 첨단 생산 기술을 점점 더 우선순위에 두고 있습니다. 지속가능성에 대한 고려도 점점 더 중요해지고 있으며, 기업들은 폐기물을 줄이고, 에너지를 최적화하며, 환경적 기대에 부합하는 포장 전략을 개선하는 데 초점을 맞추었습니다. 식품 안전 및 원재료의 투명성에 대한 규제 기준 준수는 시장 진입을 위한 기본 요건이 되고 있습니다. 제품의 다양화도 시장을 형성하고 있으며, 제조업체들은 다양한 소비자의 취향과 업무상 필요에 부응하기 위해 다양한 냉동 베이커리 제품을 개발하고 있습니다. 냉동 베이커리 제품은 다양한 조리법과 베이킹 공정에 대응할 수 있어 제조업체와 외식업체 모두에게 유연성을 제공합니다. 또한, 새로운 유통 모델은 사업 확장 및 업무의 적응성 유지에 도움이 되고 있습니다. 물류 능력의 향상과 보다 효율적인 조달 전략은 냉동 베이커리 업계 전체공급망 복원력을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 550억 달러 |

| 예측 금액 | 1,097억 달러 |

| CAGR | 7.2% |

2025년, 예비 발효 부문이 42.9%의 점유율을 차지했습니다. 이 시장에는 제조업체가 다양한 비즈니스 요구 사항에 맞는 베이커리 제품을 공급할 수 있도록 여러 제조 및 조리 기술이 포함되어 있습니다. 예비 발효된 냉동 베이커리 제품은 냉동 전 발효 과정을 거치기 때문에 조리 현장에서 최종 발효와 소성까지 완료할 수 있습니다. 이 과정을 통해 향, 식감, 그리고 전체 제품의 품질에서 갓 구운 것과 같은 특징을 구현할 수 있습니다. 또 다른 일반적인 제조 방법은 냉동 전에 제품을 부분적으로 소성하는 것으로, 제품의 품질을 유지하면서 최종 소성 시 조리 시간을 단축할 수 있습니다. 이러한 프로세스를 통해 기업은 제품의 일관성을 유지하면서 조리 시간과 업무의 복잡성을 줄일 수 있기 때문에 냉동 베이커리 제품은 다양한 외식 산업 및 소매 환경에서 높은 적응력을 발휘할 수 있습니다.

북미의 냉동 베이커리 시장은 소비자의 라이프스타일 변화와 간편식에 대한 수요 증가에 힘입어 2025년 147억 달러 규모에 달했습니다. 소비자들은 높은 품질을 유지하면서 간편하게 조리할 수 있는 베이커리 제품에 점점 더 매력을 느끼고 있습니다. 여러 소매 및 외식 채널에서 냉동 베이커리 제품을 이용할 수 있게 됨에 따라 시장에서의 입지가 더욱 강화되었습니다. 외식업체와 소매 유통업체들 수요가 증가함에 따라 제조업체들은 제품 라인업과 생산 능력을 확대되고 있습니다. 대형 소매점 및 상업용 외식 시설의 냉동 베이커리 제품 보급이 이 지역의 꾸준한 시장 성장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 제법별, 2022-2035

제7장 시장 추산 및 예측 : 최종사용자 채널별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.04.23The Global Frozen Bakery Market was valued at USD 55 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 109.7 billion by 2035.

The frozen bakery market is undergoing a notable evolution as traditional baking practices are increasingly combined with modern food processing technologies. What was once considered a purely convenience-oriented category is now becoming an essential component of foodservice operations, retail distribution, and institutional supply systems. Industry participants are increasingly prioritizing automation and advanced production technologies to improve operational efficiency and manage workforce challenges. Sustainability considerations are also gaining importance, prompting companies to focus on waste reduction, energy optimization, and improved packaging strategies that align with environmental expectations. Compliance with regulatory standards related to food safety and ingredient transparency has become a fundamental requirement for market participation. Product diversification is also shaping the market, with manufacturers developing a wide range of frozen bakery items to meet varying consumer preferences and operational needs. Frozen bakery products provide flexibility for both manufacturers and foodservice operators by supporting different preparation methods and baking processes. In addition, emerging distribution models are helping businesses expand their reach while maintaining operational adaptability. Improved logistics capabilities and more efficient sourcing strategies are also strengthening supply chain resilience across the frozen bakery industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $55 Billion |

| Forecast Value | $109.7 Billion |

| CAGR | 7.2% |

The pre-proofed segment accounted for 42.9% share in 2025. The market includes several production and preparation approaches that allow manufacturers to supply bakery products tailored to diverse operational requirements. Pre-proofed frozen bakery items undergo fermentation prior to freezing, which allows final proofing and baking to be completed at the point of preparation. This process helps deliver freshly baked characteristics in terms of aroma, texture, and overall product quality. Another common production approach involves partially baking products before freezing them, which preserves product quality while allowing for faster preparation during final baking. These processes enable businesses to maintain product consistency while reducing preparation time and operational complexity, making frozen bakery products highly adaptable for a wide range of foodservice and retail environments.

North America Frozen Bakery Market was valued at USD 14.7 billion in 2025, supported by evolving consumer lifestyles and the increasing demand for convenient food options. Consumers are increasingly drawn to bakery products that offer easy preparation while maintaining high product quality. The availability of frozen bakery products across multiple retail and foodservice channels has further strengthened their market presence. Growing demand from foodservice operators and retail distributors is encouraging manufacturers to expand their product offerings and production capabilities. The widespread presence of frozen bakery products across large-scale retail outlets and commercial foodservice establishments continues to support steady market growth in the region.

Key companies operating in the Global Frozen Bakery Market include Grupo Bimbo, Aryzta AG, Europastry, Vandemoortele, Conagra Brands, Inc., General Mills, Flowers Foods, Rich Products Corporation, Dr. Oetker, Lantmannen Unibake, Canada Bread Company, Rhodes Bake-N-Serv, Accion Alimenticia, BredenMaster S.A., and Navona Kitchen LLP (Pizzo & Crozzo). Companies operating in the Frozen Bakery Market are implementing a variety of strategic initiatives to strengthen their competitive positions and expand their market presence. A major focus remains on product innovation, with manufacturers developing new frozen bakery formulations that align with evolving consumer preferences and foodservice requirements. Many companies are investing in advanced production technologies and automation to enhance efficiency, maintain consistent product quality, and address labor challenges within manufacturing operations. Strategic partnerships with foodservice providers, distributors, and retail chains are helping companies broaden their distribution networks and improve market reach. In addition, businesses are expanding production facilities and strengthening supply chain capabilities to meet rising global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Baking process

- 2.2.4 End-user channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for convenience food

- 3.2.1.2 Developing retail channels in emerging nations

- 3.2.1.3 Superior properties of frozen baked products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Mature conventional fresh baked products market demand

- 3.2.2.2 Short shelf life after thawing

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing urbanization and changing lifestyles

- 3.2.3.2 Expansion of modern retail channels and e-commerce

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bread and rolls

- 5.2.1 Specialty breads

- 5.2.2 Sandwich rolls

- 5.2.3 Burger buns

- 5.2.4 Others

- 5.3 Pizza crusts

- 5.3.1 Traditional pizza crusts

- 5.3.2 Thin crust

- 5.3.3 Specialty crust

- 5.4 Pastries and croissants

- 5.4.1 Danish pastries

- 5.4.2 Sweet pastries

- 5.4.3 Savory pastry

- 5.5 Sweet baked goods

- 5.5.1 Donuts

- 5.5.2 Sweet rolls

- 5.5.3 Muffins

- 5.5.4 Quick breads

- 5.5.5 Others

- 5.6 Specialty and artisanal products

- 5.6.1 Organic

- 5.6.2 Vegan/plant based

Chapter 6 Market Estimates and Forecast, By Baking Process, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pre-proofed

- 6.3 Partially

- 6.4 Fully

- 6.5 Ready-to-bake

Chapter 7 Market Estimates and Forecast, By End-User Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 In-store bakeries

- 7.2.1 Supermarket and hypermarket bakeries

- 7.2.2 Convenience store bakeries

- 7.2.3 Department store food courts

- 7.3 Quick service restaurants

- 7.3.1 Fast food chains

- 7.3.2 Fast casual restaurants

- 7.3.3 Coffee shops and cafes

- 7.4 Hotels and catering

- 7.4.1 Hotel food service

- 7.4.2 Catering and event services

- 7.4.3 Institutional foodservice

- 7.5 Independent bakeries

- 7.6 Emerging channel

- 7.6.1 Ghost kitchens

- 7.6.2 Cloud kitchens

- 7.6.3 Food trucks and mobile vendors

- 7.6.4 Online-to-offline (O2O) models

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Poland

- 8.3.7 Russia

- 8.3.8 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Thailand

- 8.4.5 Indonesia

- 8.4.6 Malaysia

- 8.4.7 Australia

- 8.4.8 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Accion Alimenticia

- 9.2 Aryzta AG

- 9.3 BredenMaster S.A.

- 9.4 Canada Bread Company

- 9.5 Conagra Brands, Inc.

- 9.6 Dr. Oetker

- 9.7 Europastry

- 9.8 Flowers Foods

- 9.9 General Mills

- 9.10 Grupo Bimbo

- 9.11 Lantmannen Unibake

- 9.12 Navona Kitchen LLP (Pizzo & Crozzo)

- 9.13 Rhodes Bake-N-Serv

- 9.14 Rich Products Corporation

- 9.15 Vandemoortele