|

시장보고서

상품코드

1998830

자전거용 기계식 디스크 브레이크 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bicycle Mechanical Disc Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

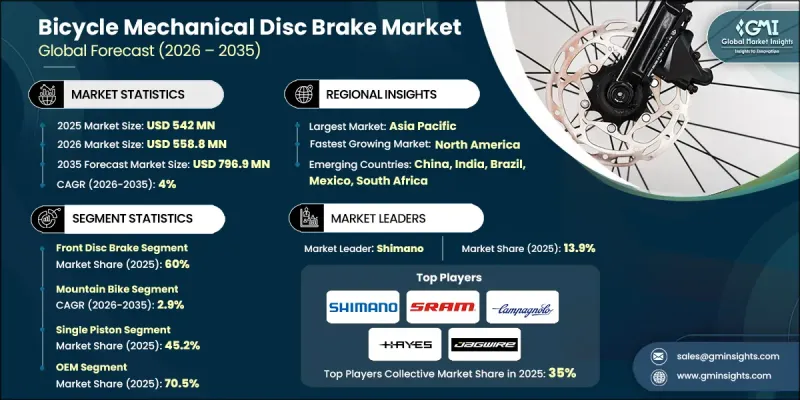

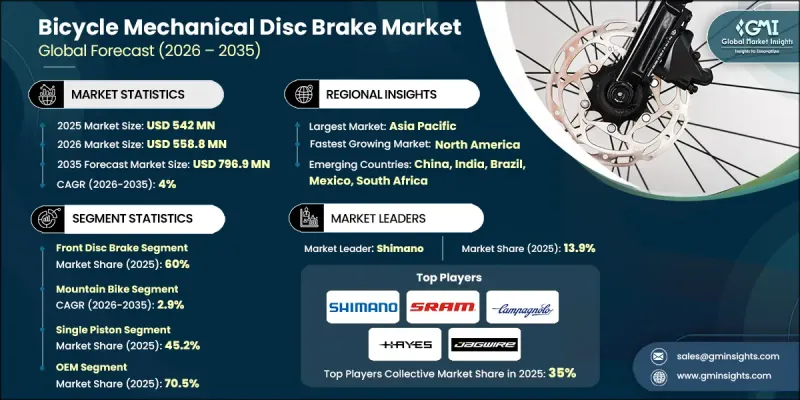

세계의 자전거용 기계식 디스크 브레이크 시장은 2025년에 5억 4,200만 달러로 평가되며, CAGR 4%로 성장하며, 2035년까지 7억 9,690만 달러에 달할 것으로 추정되고 있습니다.

이 시장은 도시 출퇴근, 레크리에이션으로서의 자전거 타기, 그리고 자전거 공유 프로그램의 확대에 힘입어 전 세계에서 자전거 보급이 확대되고 있는 것에 힘입어 성장하고 있습니다. 더 많은 도시들이 지속가능한 교통 계획에 자전거를 도입함에 따라 자전거 제조업체와 부품 공급업체들은 높아지는 안전 및 성능 기준을 충족하기 위해 더 많은 모델에 기계식 디스크 브레이크를 장착하고 있습니다. 환경에 대한 인식이 높아짐에 따라 라이더들은 자동차보다 자전거를 선택하게 되었습니다. 또한 일상적인 출퇴근 및 레저 활동에서 전기자전거의 급속한 보급은 다양한 주행 조건에서 안정적인 제동력을 제공하는 기계식 디스크 브레이크에 대한 수요를 더욱 강화시키고 있습니다. 브레이크 부품의 기술 혁신도 기계식 디스크 브레이크의 매력을 높이고 있습니다. 로터 설계, 케이블 시스템 및 재료의 발전으로 내마모성, 방열성 및 제동 제어성이 향상되어 기계식 시스템은 더 비싼 유압식 시스템과의 경쟁에서 경쟁력을 유지하고 있습니다. 이러한 개선을 통해 제조업체는 제품을 차별화하고 출퇴근용, 하이브리드, 자갈길, 산악자전거 등 각 부문에서 존재감을 유지할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 5억 4,200만 달러 |

| 예측액 | 7억 9,690만 달러 |

| CAGR | 4% |

프론트 디스크 브레이크 부문은 2025년 60%의 점유율을 차지하며, 2035년까지 연평균 복합 성장률(CAGR) 3.4%를 나타낼 것으로 예측됩니다. 프론트 디스크 브레이크는 제동력의 대부분을 담당하여 부드러운 제동 제어, 짧은 제동 거리, 습식 및 건식 조건 모두에서 신뢰할 수 있는 성능을 보장합니다. 이 기술의 채택은 안전 규정을 충족하고 산악자전거, 자갈길, 도로, 도시 및 전기자전거(e-bike) 플랫폼에서 고성능 브레이크 솔루션을 제공하고자 하는 OEM 및 부품 공급업체에게 최우선 순위가 되고 있습니다.

산악자전거 부문은 2025년 45.7%의 점유율을 차지하며, 2026-2035년 연평균 복합 성장률(CAGR) 2.9%로 성장할 것으로 전망됩니다. 기계식 디스크 브레이크는 진흙, 물, 이물질이 흩어져 있는 상황에서도 안정적인 제동력을 발휘하므로 오프로드 트레일, 가파른 내리막길, 험준한 지형에서 필수적입니다. 이러한 신뢰성은 산악자전거 제조업체, 프로 라이더, 트레일 사이클링 애호가들에게 없어서는 안 될 존재가 되었습니다.

미국 자전거용 기계식 디스크 브레이크 시장은 2025년 9,420만 달러에 달했습니다. 이 지역의 성장은 제조업체, 전기자전거 사업자 및 부품 유통업체들이 첨단 브레이크 솔루션을 채택하면서 성장세를 주도하고 있습니다. 정밀한 기계식 디스크 브레이크는 안정적인 성능을 보장하고, 라이더의 안전을 강화하며, 최신 프레임 표준과의 호환성을 유지하여 대량 생산 시장에서 브레이크 고장의 위험을 줄입니다. 또한 각 업체들은 기존 자전거와 전기자전거 모두에서 브레이크 성능을 최적화하기 위해 로터 설계와 모듈식 캘리퍼 플랫폼의 개선을 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 브레이크별, 2022-2035

제6장 시장 추산·예측 : 제공별, 2022-2035

제7장 시장 추산·예측 : 용도별, 2022-2035

제8장 시장 추산·예측 : 유통 채널별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Bicycle Mechanical Disc Brake Market was valued at USD 542 million in 2025 and is estimated to grow at a CAGR of 4% to reach USD 796.9 million by 2035.

The market is driven by rising global bicycle adoption, fueled by urban commuting, recreational cycling, and expanding bike-sharing programs. As more cities integrate cycling into sustainable transportation planning, bicycle manufacturers and component suppliers are equipping a wider range of models with mechanical disc brakes to meet increasing safety and performance standards. Growing environmental consciousness is encouraging riders to favor bicycles over motorized vehicles, while the rapid adoption of e-bikes for daily commuting and leisure activities further strengthens demand for mechanical disc brakes that provide dependable stopping power under varying riding conditions. Innovations in brake components are also enhancing the appeal of mechanical disc brakes. Advances in rotor design, cable systems, and materials improve wear resistance, heat dissipation, and braking modulation, keeping mechanical systems competitive against costlier hydraulic alternatives. These improvements allow manufacturers to differentiate products and maintain relevance across commuter, hybrid, gravel, and mountain bike segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $542 Million |

| Forecast Value | $796.9 Million |

| CAGR | 4% |

The front disc brake segment held a 60% share in 2025 and is expected to grow at a CAGR of 3.4% through 2035. Front disc brakes handle the majority of braking force, ensuring smooth modulation, shorter stopping distances, and reliable performance in both wet and dry conditions. Their integration is a top priority for OEMs and component suppliers aiming to meet safety regulations and deliver high-performance braking solutions across mountain, gravel, road, urban, and e-bike platforms.

The mountain bikes segment held a 45.7% share in 2025 and is forecasted to grow at a CAGR of 2.9% from 2026 to 2035. Mechanical disc brakes are essential for off-road trails, steep descents, and uneven terrain because they provide consistent stopping power in mud, water, and debris-laden conditions. This reliability makes them indispensable for mountain bike manufacturers, professional riders, and trail cycling enthusiasts.

U.S. Bicycle Mechanical Disc Brake Market reached USD 94.2 million in 2025. Growth in the region is driven by the adoption of advanced braking solutions by manufacturers, e-bike operators, and component distributors. Precision mechanical disc brakes ensure consistent performance, enhance rider safety, and maintain compatibility with modern frame standards, reducing brake failure risks in high-volume markets. Companies are also upgrading rotor designs and modular caliper platforms to optimize braking across both traditional and electric bicycles.

Major players operating in the Global Bicycle Mechanical Disc Brake Market include Shimano, SRAM, Campagnolo, Hayes, Jagwire, Magura, Cane Creek, Formula, Tektro, and Box Components. Key strategies adopted by companies in the Global Bicycle Mechanical Disc Brake Market include extensive R&D for improved rotor and caliper designs, developing lightweight and corrosion-resistant materials, and enhancing heat dissipation and modulation performance. Firms focus on expanding product portfolios across e-bikes, mountain, commuter, and hybrid segments to meet diverse customer needs. Strategic collaborations with bicycle OEMs and aftermarket distributors help integrate braking systems early in the design process. Market players also leverage marketing campaigns emphasizing safety, durability, and performance reliability, while establishing regional manufacturing hubs to improve supply chain efficiency, reduce costs, and strengthen global market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Brake

- 2.2.3 Offering

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in bicycle adoption across the world

- 3.2.1.2 Environmental awareness encourages the shift to eco-friendly transport

- 3.2.1.3 Technological advancements in brake components

- 3.2.1.4 Government initiatives supporting cycling infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High competition and price sensitivity

- 3.2.2.2 Shift toward hydraulic disc brakes

- 3.2.3 Market opportunities

- 3.2.3.1 Growing Demand in Emerging Markets

- 3.2.3.2 Expansion of Gravel, Hybrid, and Commuter Bikes

- 3.2.3.3 Aftermarket Upgrades and Replacement Segment

- 3.2.3.4 Rising Urban Commuting and Micro-Mobility Trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Consumer Product Safety Commission (CPSC)

- 3.4.1.2 ASTM International - Bicycle Standards (ASTM F2043 & F1952)

- 3.4.1.3 Canada: Canada Consumer Product Safety Act (CCPSA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO 4210 - Safety Requirements for Bicycles

- 3.4.2.2 EU General Product Safety Directive (GPSD) / General Product Safety Regulation (GPSR)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: GB Standards for Bicycle Components (GB 3565)

- 3.4.3.2 India: Bureau of Indian Standards (BIS) - IS 1570 & IS 15602

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ABNT NBR Standards for Bicycles

- 3.4.4.2 Mexico: NOM Standards for Bicycle Safety

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States: ESMA Product Safety Regulations

- 3.4.5.2 Saudi Arabia: SASO Bicycle and Consumer Product Standards

- 3.4.5.3 African Union (AU): African Continental Consumer Protection Framework

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Trade statistics (Driven by Paid Database)

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Business Models and Monetization Framework

- 3.11.1 Revenue Models

- 3.11.2 Value Chain and Ecosystem

- 3.11.3 Go-to-Market Strategy

- 3.12 Quality Standards, Compliance, and Product Risk

- 3.12.1 Component Safety and Regulatory Compliance

- 3.12.2 Product Performance and Durability Risk

- 3.12.3 Operational and Supply Chain Risks

- 3.13 Braking System Architecture

- 3.13.1 Multi-Component Brake Assembly Models

- 3.13.2 Bicycle-to-Infrastructure and Smart Mobility Integration

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.1.1 Predictive Maintenance & Operations Optimization

- 3.14.1.2 Automated design optimization

- 3.14.1.3 Supply chain AI for demand forecasting

- 3.14.1.4 GenAI use cases & adoption roadmap by segment

- 3.14.1 AI-driven disruption of existing business models

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable Manufacturing Practices

- 3.15.2 Energy efficiency in production

- 3.15.3 Carbon footprint considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Brake, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front disc brake

- 5.3 Rear disc brake

Chapter 6 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Single piston

- 6.3 Dual piston

- 6.4 Four piston

- 6.5 Multi-piston

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Road bike

- 7.3 Mountain bike

- 7.4 Racing bike

- 7.5 Gravel bikes

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Norway

- 9.3.9 Denmark

- 9.3.10 Netherlands

- 9.3.11 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.4.9 Malaysia

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Shimano

- 10.1.2 SRAM

- 10.1.3 Tektro / TRP (Tektro Racing Products)

- 10.1.4 Magura

- 10.1.5 Hayes Performance Systems

- 10.1.6 Campagnolo

- 10.1.7 Formula

- 10.1.8 Jagwire

- 10.1.9 Hope Technology

- 10.1.10 Clarks Cycle Systems

- 10.1.11 Promax

- 10.2 Regional players

- 10.2.1 Nutt Technology

- 10.2.2 MTX Braking

- 10.2.3 Kool-Stop International

- 10.2.4 Cane Creek

- 10.2.5 EBC Brakes

- 10.2.6 Galfer

- 10.2.7 Paul Component Engineering

- 10.2.8 Funn Components

- 10.2.9 Alligator Cables