|

시장보고서

상품코드

1998831

의료용 침대 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Medical Bed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

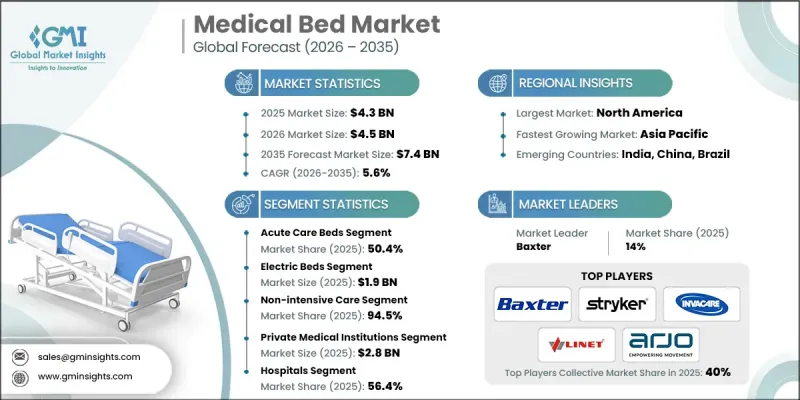

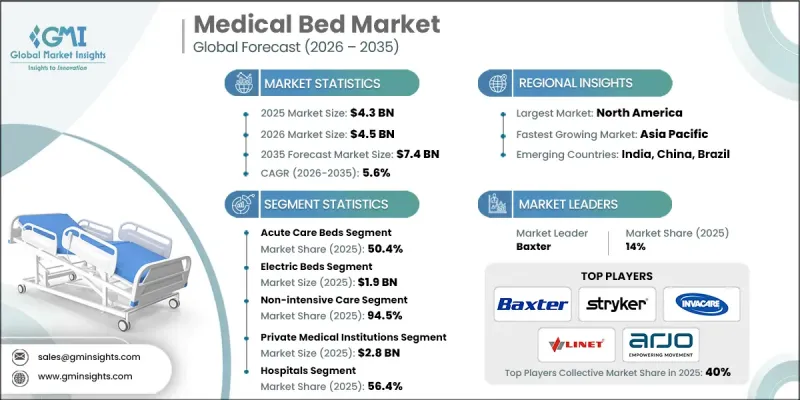

세계의 의료용 침대 시장은 2025년에 43억 달러로 평가되며, CAGR 5.6%로 성장하며, 2035년까지 74억 달러에 달할 것으로 추정되고 있습니다.

이러한 시장 확대는 전 세계 고령 인구 증가, 개발도상국의 의료 인프라 투자 확대, 만성질환 및 생활습관병으로 인한 입원 환자 수 증가 등 몇 가지 주요 요인에 의해 주도되고 있습니다. 신흥 시장의 민간 의료시설은 증가하는 환자 수에 대응하고, 의료관광을 지원하며, 늘어나는 중산층 인구에 서비스를 제공하기 위해 병상을 빠르게 늘리고 있습니다. 중환자실 및 중환자실 인프라 개선과 더불어 병원 현대화 노력도 수요를 더욱 자극하고 있습니다. 민간 병원은 환자 경험과 브랜드 평판을 높이기 위해 고품질의 편안하고 표준화된 침대 솔루션을 제공하는 데 주력하고 있습니다. 종합병원 및 병원 체인에 대한 수요 증가로 일반병동, 중환자실, 회복실용 침대의 대규모 조달이 진행되고 있습니다. 의료용 침대는 병원, 요양병원, 요양원, 홈케어 현장을 위해 설계된 전문 의료기기로, 환자 관리, 편안함, 재활의 필요를 지원하는 기능이 내장되어 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 43억 달러 |

| 예측액 | 74억 달러 |

| CAGR | 5.6% |

2025년 급성기 치료용 침대 부문은 50.4%의 점유율을 차지했습니다. 이 병상은 주로 내과 및 외과 병동, 응급실, 중환자실에서 환자의 단기 치료에 사용됩니다. 전동식 및 조정 가능한 급성기 치료용 침대는 환자의 체위 변경이 용이하고, 임상 처치를 단순화하며, 24시간 365일 모니터링 기능이 있으며, 선호되고 있습니다. 이러한 기능은 간병인의 부담을 줄이고 시간을 절약할 수 있으므로 현대 의료시설에서 매우 수요가 많은 기능입니다.

전동 침대 부문은 2025년 19억 달러에 달했습니다. 전동 침대는 모터 구동 메커니즘을 갖추고 있으며, 간병인이 전자식 또는 수동 조작 패널을 통해 환자의 높이와 자세를 조절할 수 있으며, 환자의 편안함을 높이고 간병인의 수고를 최소화할 수 있습니다. 이 침대는 병원, 장기 요양 시설 및 민간 의료시설에서 널리 사용되고 있습니다. 낮은 위치 설정, 위치 고정 기능, 모니터링 시스템과의 연동과 같은 안전 기능을 통해 임상 효과와 환자의 안전성을 향상시킵니다.

미국의 의료용 침대 시장은 첨단 의료 인프라, 높은 병원 침대 교체율, 기술적으로 진보된 장비 도입에 힘입어 2025년 15억 7,000만 달러에 달했습니다. 병원은 환자의 안전을 향상시키고, 간병인의 업무 부담을 줄이고, 가치 기반 의료(Value-based Care)를 지원하기 위해 병상 업그레이드를 우선순위에 두고 있습니다. 특히 급성기 및 중환자실 현장에서는 전동침대, 중환자실용 침대, 스마트 침대에 대한 수요가 특히 증가하고 있습니다. 고령화의 진전과 만성질환의 유병률 증가로 입원치료 및 장기입원 수요가 지속적으로 증가하고 있으며, 이는 시장의 꾸준한 성장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035

제6장 시장 추산·예측 : 침대 유형별, 2022-2035

제7장 시장 추산·예측 : 용도별, 2022-2035

제8장 시장 추산·예측 : 의료 시설별, 2022-2035

제9장 시장 추산·예측 : 최종 용도별, 2022-2035

제10장 시장 추산·예측 : 지역별, 2022-2035

제11장 기업 개요

KSA 26.04.20The Global Medical Bed Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 7.4 billion by 2035.

The market expansion is driven by several key factors, including a rising global geriatric population, growing investments in healthcare infrastructure across developing nations, and increasing hospital admissions due to chronic and lifestyle-related illnesses. Private healthcare facilities in emerging markets are rapidly adding hospital beds to meet rising patient volumes, support medical tourism, and cater to the expanding middle-class population. ICU and critical care infrastructure improvements, along with hospital modernization initiatives, further stimulate demand. Private hospitals focus on offering high-quality, comfortable, and standardized bed solutions to enhance patient experience and brand reputation. Increasing demand for multispecialty hospitals and hospital chains has led to large-scale procurement of beds for general wards, ICUs, and recovery units. Medical beds are specialized healthcare equipment designed for hospitals, nursing homes, and home care settings, incorporating features that support patient care, comfort, and rehabilitation needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 5.6% |

The acute care beds segment held a 50.4% share in 2025. These beds are primarily used for short-term treatment of patients in medical-surgical units, emergency departments, and ICUs. Fully electric and adjustable acute care beds are preferred due to their ease of patient repositioning, simplified clinical procedures, and 24/7 monitoring capabilities. These features reduce caregiver stress and save time, making them highly sought after in modern healthcare facilities.

The electric beds segment reached USD 1.9 billion in 2025. Electric beds feature motorized mechanisms that allow caregivers to adjust patient height and position via electronic or hand controls, enhancing patient comfort while minimizing caregiver effort. These beds are widely used across hospitals, long-term care centers, and private healthcare facilities. Safety features such as low-height settings, lockable positions, and integration with monitoring systems enhance clinical effectiveness and patient security.

U.S. Medical Bed Market reached USD 1.57 billion in 2025, fueled by advanced healthcare infrastructure, high hospital bed replacement rates, and adoption of technologically advanced equipment. Hospitals prioritize bed upgrades to improve patient safety, reduce caregiver workload, and support value-based care initiatives. Demand for electric, ICU, and smart beds is especially strong in acute and critical care settings. An aging population and rising prevalence of chronic diseases continue to drive inpatient care and long-term hospitalization needs, supporting consistent market growth.

Key players in the Global Medical Bed Market include ANTANO Group, Arjo, Baxter, BESCO, DiaMedical, DRIVE DEVILBISS HEALTHCARE, GENDRON, HARD Manufacturing Company, INVACARE, LINET, MALVESTIO, Midmark, PARAMOUNT BED, Savaria, STIEGELMEYER, Stryker, and Umano Medical. Companies in the medical bed industry are strengthening their market presence through strategic innovation, global expansion, and partnerships with healthcare institutions. Manufacturers focus on developing advanced electric and smart beds with integrated monitoring and safety features to differentiate their offerings. Collaboration with hospitals and long-term care providers ensures product customization and adoption. R&D investments enable the creation of ergonomically designed, technologically advanced beds that improve patient outcomes and caregiver efficiency. Expanding distribution networks, entering emerging markets, and providing maintenance and training services further enhance market foothold.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Bed type trends

- 2.2.4 Application trends

- 2.2.5 Medical facilities trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population worldwide

- 3.2.1.2 Increasing funding on healthcare infrastructure in developing economies

- 3.2.1.3 Surging hospital admissions due to chronic diseases

- 3.2.1.4 Rising volume of hospital beds in private hospitals in developing countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of specialty beds

- 3.2.3 Opportunities

- 3.2.3.1 Rapid expansion of home care and remote patient monitoring

- 3.2.3.2 Integration of IoT and AI in patient beds

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy landscape

- 3.7 Supply chain analysis

- 3.8 Smart bed feature benchmarking

- 3.9 Pricing analysis by bed type (Driven by Primary Research)

- 3.10 Rental and leasing model analysis (Driven by Primary Research)

- 3.11 Environmental and sustainability initiatives

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Consumer insights (Driven by Primary Research)

- 3.16 Future market trends (Driven by Primary Research)

- 3.17 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players (Driven by Primary Research)

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Acute care beds

- 5.2.1 MedSurg beds

- 5.2.2 ICU beds

- 5.2.3 Pediatric beds

- 5.2.4 Birthing beds

- 5.2.5 Other acute care beds

- 5.3 Long-term care beds

- 5.4 Psychiatric care beds

- 5.5 Bariatric care beds

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Bed Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Manual beds

- 6.3 Electric beds

- 6.4 Semi-electric beds

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Intensive care

- 7.3 Non-intensive care

Chapter 8 Market Estimates and Forecast, By Medical Facilities, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Private medical institutions

- 8.3 Public medical institutions

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Home care settings

- 9.4 Elderly care facilities

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ANTANO Group

- 11.2 Arjo

- 11.3 Baxter

- 11.4 BESCO

- 11.5 DiaMedical

- 11.6 DRIVE DEVILBISS HEALTHCARE

- 11.7 GENDRON

- 11.8 HARD Manufacturing Company

- 11.9 INVACARE

- 11.10 LINET

- 11.11 MALVESTIO

- 11.12 Midmark

- 11.13 PARAMOUNT BED

- 11.14 Savaria

- 11.15 STIEGELMEYER

- 11.16 Stryker

- 11.17 Umano Medical