|

시장보고서

상품코드

2019072

커넥티드카 기술 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Connected Vehicle Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

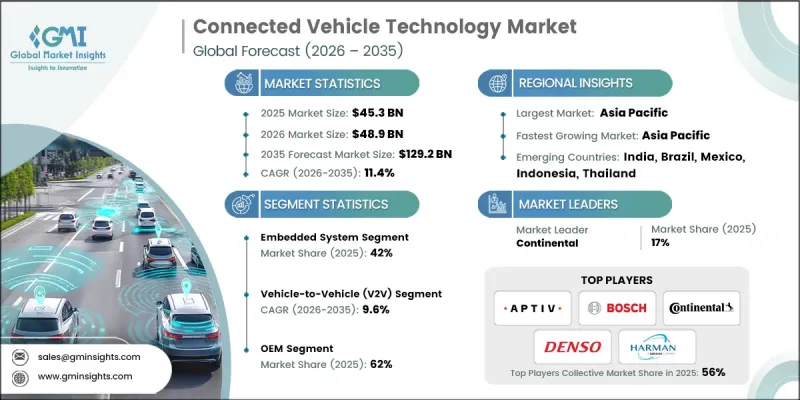

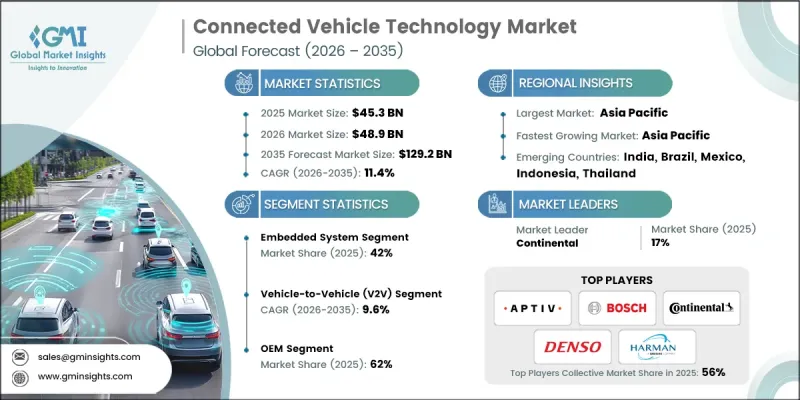

세계의 커넥티드카 기술 시장은 2025년에 453억 달러로 평가되었으며, CAGR 11.4%로 성장하여 2035년까지 1,292억 달러에 달할 것으로 추정됩니다.

이 시장의 성장은 ADAS(첨단 운전자 보조 시스템)의 보급에 힘입은 바 큽니다. ADAS는 안전, 내비게이션 및 운전자 인식 능력을 향상시키기 위해 현대 차량에 점점 더 많이 탑재되고 있습니다. 커넥티비티는 실시간 통신, 원격 진단, 무선 소프트웨어 업데이트 등 차량 플랫폼의 핵심 기능으로 자리 잡고 있습니다. 5G 네트워크의 구축은 V2X(Vehicle-to-Everything) 통신, 원격 차량 관리, 차세대 인포테인먼트에 필수적인 고속, 저지연 연결을 제공함으로써 이러한 변화를 가속화하고 있습니다. 전기자동차(EV)의 디지털 플랫폼과 중앙 집중식 소프트웨어 아키텍처는 배터리 관리, 텔레매틱스 업데이트, 운영 효율성 측면에서 커넥티비티의 중요성을 더욱 부각시키고 있습니다. 상용차 업체들은 경로 최적화, 자산 추적 및 운영 비용 절감을 위해 이러한 기술을 활용하고 있으며, 전 세계 승용차 및 상용차에서 광범위하게 도입하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 453억 달러 |

| 예측 규모 | 1,292억 달러 |

| CAGR | 11.4% |

임베디드 시스템 부문은 2025년 42%의 점유율을 차지했으며, 2035년까지 CAGR 10.5%로 성장할 것으로 예상됩니다. 자동차 제조업체들이 텔레매틱스 제어 장치, 센서, 차량용 컴퓨팅을 차량 시스템에 직접 통합함에 따라 임베디드 커넥티비티 솔루션의 인기가 높아지고 있습니다. 이 솔루션은 ADAS 기능, 원격 모니터링, 무선 업데이트 및 차량 수명주기 전반에 걸쳐 원활한 커넥티드 서비스를 제공하여 신뢰성과 사용자 경험을 향상시킵니다.

V2V(Vehicle-to-Vehicle) 부문은 35.8%의 점유율을 차지하고 있으며, 2035년까지 CAGR 9.6%로 성장할 것으로 예상됩니다. V2V 기술을 통해 차량은 속도, 위치, 진행 방향에 대한 정보를 교환할 수 있어 교통 안전이 향상되고, 자동 운전 시스템이 주변 교통 상황, 협동 제동 및 충돌 위험에 효과적으로 대응할 수 있게 됩니다.

미국의 커넥티드카 기술 시장은 2025년 120억 달러에 달했습니다. 미국에서의 성장은 지속적인 업데이트와 ADAS(첨단 운전자 보조 시스템) 및 진단 시스템 통합을 가능하게 하는 소프트웨어 정의 차량 아키텍처를 채택한 자동차 제조업체에 의해 뒷받침되고 있습니다. 자율주행차 및 반자율주행차 시범 프로그램은 교통 관리의 최적화와 안전한 운영을 보장하기 위해 V2X 연결성과 AI 기반 시스템에 크게 의존하고 있으며, 이는 이 나라에서 혁신과 보급을 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술별, 2022-2035

제6장 시장 추정 및 예측 : 통신 방식별, 2022-2035

제7장 시장 추정 및 예측 : 차종별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.05.06The Global Connected Vehicle Technology Market was valued at USD 45.3 billion in 2025 and is estimated to grow at a CAGR of 11.4% to reach USD 129.2 billion by 2035.

The market's growth is fueled by the widespread adoption of advanced driver assistance systems (ADAS), which are increasingly integrated into modern vehicles to enhance safety, navigation, and driver awareness. Connectivity is becoming a core feature of vehicle platforms, enabling real-time communication, remote diagnostics, and over-the-air software updates. The rollout of 5G networks is accelerating this shift by providing high-speed, low-latency connections essential for vehicle-to-everything (V2X) communications, remote fleet management, and next-generation infotainment. Digital platforms and centralized software architectures in electric vehicles are further emphasizing connectivity as critical for battery management, telematics updates, and operational efficiency. Commercial fleets are leveraging these technologies for route optimization, asset tracking, and reducing operational costs, driving broad adoption across passenger and commercial vehicles globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.3 Billion |

| Forecast Value | $129.2 Billion |

| CAGR | 11.4% |

The embedded systems segment held a 42% share in 2025 and is expected to grow at a CAGR of 10.5% through 2035. Embedded connectivity solutions are gaining popularity as automakers integrate telematics control units, sensors, and onboard computing directly into vehicle systems. These solutions facilitate ADAS functionality, remote monitoring, over-the-air updates, and seamless connected services throughout the vehicle's lifecycle, enhancing reliability and user experience.

The Vehicle-to-Vehicle (V2V) segment held a 35.8% share and is anticipated to grow at a CAGR of 9.6% through 2035. V2V technology enables vehicles to exchange information about speed, location, and direction, improving road safety and enabling automated systems to respond effectively to nearby traffic conditions, cooperative braking, and potential collision risks.

U.S. Connected Vehicle Technology Market reached USD 12 billion in 2025. Growth in the U.S. is supported by automakers adopting software-defined vehicle architectures, which allow continuous updates and integration of advanced driver assistance and diagnostic systems. Pilot programs for autonomous and semi-autonomous vehicles are heavily reliant on V2X connectivity and AI-enabled systems to optimize traffic management and ensure safe operation, driving innovation and adoption in the country.

Key players in the Global Connected Vehicle Technology Market include Aptiv, Bosch, Continental, Denso, Ericsson, Harman, Microsoft, Mobileye, NXP, and Qualcomm. Companies in the connected vehicle technology sector are strengthening their market position through extensive investment in R&D to develop AI-enabled ADAS, V2X communication modules, and embedded telematics solutions. They focus on strategic partnerships with automakers, software developers, and telecommunications providers to expand ecosystem integration and scale connectivity offerings. Firms emphasize over-the-air software platforms, cybersecurity solutions, and cloud-based fleet management services to enhance product value. Geographic expansion into emerging automotive markets and targeted collaboration with commercial fleet operators help secure recurring contracts. Continuous innovation in vehicle software, sensor integration, and connectivity solutions allows companies to differentiate products, improve adoption rates, and maintain a competitive edge in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Communication

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology Providers & Platform Developers

- 3.1.2 Automotive OEMs & Tier-1 Suppliers

- 3.1.3 Telecommunications Service Providers

- 3.1.4 Software & Application Developers

- 3.1.5 Aftermarket Solution Providers

- 3.1.6 End-Users & Fleet Operators

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of ADAS and vehicle safety technologies

- 3.2.1.2 Expansion of 5G and cellular connectivity infrastructure

- 3.2.1.3 Growing adoption of electric and software-defined vehicles

- 3.2.1.4 Rising demand for fleet management and mobility services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and data privacy concerns

- 3.2.2.2 High implementation and system integration costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of smart city and intelligent transportation infrastructure

- 3.2.3.2 Growth of Mobility-as-a-Service (MaaS) platforms

- 3.2.3.3 Vehicle data monetization and cloud-based services

- 3.2.3.4 Connected solutions for commercial fleets and logistics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Insurance Institute for Highway Safety (IIHS)

- 3.4.2 Europe

- 3.4.2.1 Euro NCAP (European New Car Assessment Programme)

- 3.4.2.2 UNECE Regulations (R94, R95, R129)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automobile Research Institute (JARI) / JIS Standards

- 3.4.3.2 China Automotive Technology & Research Center (CATARC) / Chinese NCAP (C-NCAP)

- 3.4.4 Latin America

- 3.4.4.1 Latin NCAP

- 3.4.4.2 ABNT NBR / National Automotive Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA Vehicle Safety Standards (UAE)

- 3.4.5.2 SABS Automotive Safety Standards (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.10.1 V2X Communication Technology Patents

- 3.10.2 ADAS & Autonomous Driving Patents

- 3.10.3 Cybersecurity & Encryption Patents

- 3.10.4 Patent Filing Trends by Geography

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Embedded Systems

- 5.3 Tethered Systems

- 5.4 Integrated Systems

- 5.5 V2X Communication Systems

Chapter 6 Market Estimates & Forecast, By Communication, 2022 - 2035 ($Mn, Mn Units)

- 6.1 Key trends

- 6.2 Vehicle-to-Vehicle (V2V)

- 6.3 Vehicle-to-Infrastructure (V2I)

- 6.4 Vehicle-to-Pedestrian (V2P)

- 6.5 Vehicle-to-Cloud (V2C)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Mn Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Safety & Security

- 8.3 Infotainment

- 8.4 Navigation & Telematics

- 8.5 Fleet Management

- 8.6 Driver Assistance Systems (ADAS)

- 8.7 Vehicle Diagnostics & Maintenance

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Aptiv

- 11.1.2 Bosch

- 11.1.3 Continental

- 11.1.4 Denso

- 11.1.5 Ericsson

- 11.1.6 Harman (Samsung)

- 11.1.7 Microsoft

- 11.1.8 Mobileye

- 11.1.9 NXP Semiconductors

- 11.1.10 Qualcomm

- 11.2 Regional players

- 11.2.1 Huawei

- 11.2.2 Maruti Suzuki

- 11.2.3 TomTom

- 11.2.4 Valeo

- 11.2.5 Verizon

- 11.2.6 Vodafone Automotive

- 11.3 Emerging players

- 11.3.1 Airbiquity

- 11.3.2 Cubic Telecom

- 11.3.3 Ficosa (Panasonic)

- 11.3.4 Otonomo