|

시장보고서

상품코드

2019080

트럭용 냉동 유닛 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Truck Refrigeration Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

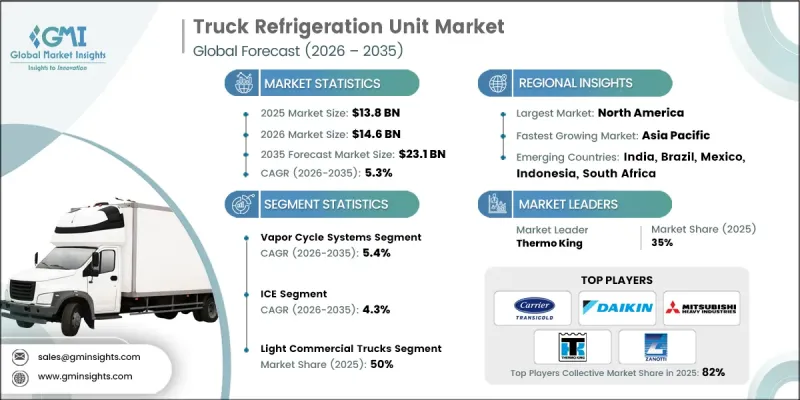

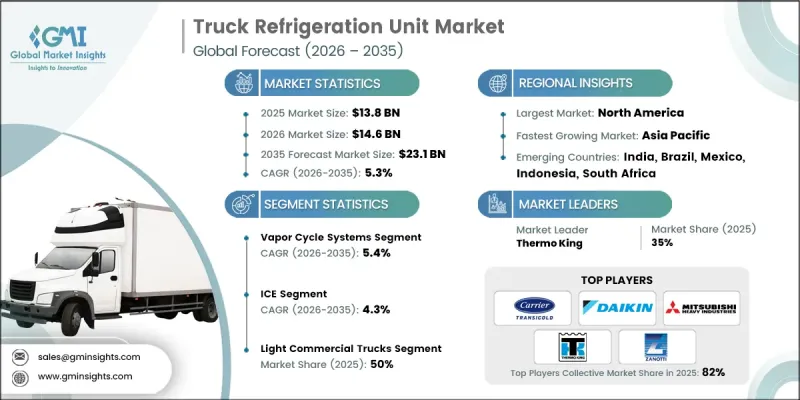

세계의 트럭용 냉동 유닛 시장은 2025년에 138억 달러로 평가되었으며, CAGR 5.3%로 성장하여 2035년까지 231억 달러에 달할 것으로 추정됩니다.

세계 트럭용 냉동 유닛 시장은 특히 공급망이 더욱 복잡해지고 지리적으로 분산됨에 따라 운송 중 제품의 품질을 유지해야 할 필요성이 증가함에 따라 견인되고 있습니다. 온도에 민감한 상품에 대한 수요 증가로 인해 물류 사업자들은 콜드체인 인프라를 강화해야 하는 상황에 직면해 있습니다. 여기에는 배송지에서부터 배송지까지 일관된 온도 관리를 보장하는 첨단 냉동 기술 도입이 포함됩니다. 신선식품의 소비 증가는 냉장 운송 솔루션에 대한 수요 확대에 기여하고 있으며, 이로 인해 차량 운영업체들은 운송 능력을 확대해야 하는 상황에 직면해 있습니다. 냉장 효율, 시스템 신뢰성 및 에너지 성능의 지속적인 개선은 장기적인 시장 성장을 뒷받침하고 있습니다. 각 산업계가 제품 품질과 규정 준수를 더욱 중요시하는 가운데, 트럭용 냉장 장치 시장은 현대 물류 요구 사항을 충족하도록 설계된 첨단 솔루션과 함께 계속 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 138억 달러 |

| 예측 규모 | 231억 달러 |

| CAGR | 5.3% |

트럭용 냉동 유닛 시장은 온도 관리가 필요한 화물의 운송을 규제하는 프레임워크의 강화로 인해 영향을 받고 있습니다. 당국은 공급망 전반에 걸쳐 온도 관리, 모니터링 정확도 및 데이터 기록에 대한 보다 엄격한 기준을 시행하고 있습니다. 이에 따라 정밀한 모니터링 및 추적 기능을 갖춘 첨단 냉동 시스템에 대한 수요가 증가하고 있습니다. 물류 사업자들은 컴플라이언스 준수, 업무 투명성 향상 및 운송 중 제품 안전성을 유지하기 위해 이러한 기술을 채택하고 있습니다.

2025년에는 스팀 사이클 시스템 부문이 72%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 5.4%로 성장할 것으로 예상됩니다. 이 부문은 입증된 신뢰성, 운영 효율성 및 광범위한 온도 범위에 대한 대응 능력으로 인해 지속적으로 선도적인 위치를 유지하고 있습니다. 현재 진행 중인 기술 혁신은 압축기 효율 향상, 친환경 냉매 채택, 디지털 모니터링 플랫폼과의 통합을 통한 시스템 성능 향상에 초점을 맞추고 있습니다. 이러한 개발을 통해 사업자들은 다양한 운송 조건에서 높은 성능 기준을 유지하면서 운영 비용을 절감할 수 있게 되었습니다.

소형 상용 트럭 부문은 2025년 50%의 점유율을 차지했으며, 2035년까지 연평균 4.1%의 성장률을 기록했습니다. 소형 운송 솔루션의 사용 확대는 소형 차량용으로 설계된 고효율 냉장 시스템에 대한 수요를 뒷받침하고 있습니다. 이 시스템은 도시 물류 업무에 최적화되어 있으며, 에너지 효율적인 성능과 배출가스 감소를 실현하고 있습니다. 정숙한 작동과 정밀한 온도 제어에 중점을 두어 잦은 배송 주기에 대한 적합성을 더욱 향상시켜 이 부문의 성장에 기여하고 있습니다.

미국 트럭용 냉동 유닛 시장은 2025년 45억 달러에 달했습니다. 이 나라의 성장은 온도 관리 물류에 대한 수요 증가와 냉장 운송 차량의 확대에 의해 주도되고 있습니다. 첨단 냉동 기술의 도입은 환경 규제와 지속가능성에 대한 노력으로 인해 더욱 가속화되고 있습니다. 사업자들이 배기가스 배출을 줄이고 효율성을 높이기 위해 전기 및 하이브리드 냉장 시스템으로 전환하는 움직임이 가속화되고 있습니다. 이러한 추세로 인해, 한국은 전체 트럭용 냉장 장치 시장에서 주요 기여자로서의 입지를 확고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 시스템별, 2022-2035

제6장 시장 추정 및 예측 : 추진 방식별, 2022-2035

제7장 시장 추정 및 예측 : 차종별, 2022-2035

제8장 시장 추정 및 예측 : 온도별, 2022-2035

제9장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.05.06The Global Truck Refrigeration Unit Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 23.1 billion by 2035.

The global truck refrigeration unit market is driven by the growing need to maintain product integrity throughout transportation, particularly as supply chains become more complex and geographically dispersed. Rising demand for temperature-sensitive goods is encouraging logistics providers to enhance their cold chain infrastructure. This includes the integration of advanced refrigeration technologies that ensure consistent temperature control from origin to delivery. Increased consumption of perishable products is also contributing to higher demand for refrigerated transport solutions, prompting fleet operators to expand their capacity. Continuous improvements in refrigeration efficiency, system reliability, and energy performance are supporting long-term market growth. As industries place greater emphasis on product quality and regulatory compliance, the truck refrigeration unit market continues to evolve with advanced solutions designed to meet modern logistics requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.8 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 5.3% |

The truck refrigeration unit market is also influenced by tightening regulatory frameworks governing the transportation of temperature-sensitive goods. Authorities are enforcing stricter standards related to temperature control, monitoring accuracy, and data recording throughout the supply chain. This has increased the need for advanced refrigeration systems equipped with precise monitoring and traceability features. Logistics operators are adopting these technologies to ensure compliance, improve operational transparency, and maintain product safety during transit.

In 2025, the vapor cycle systems segment accounted for 72% share and is expected to grow at a CAGR of 5.4% from 2026 to 2035. This segment continues to lead due to its proven reliability, operational efficiency, and ability to support a wide temperature range. Ongoing advancements are focused on enhancing system performance through improved compressor efficiency, environmentally friendly refrigerants, and integration with digital monitoring platforms. These developments are enabling operators to reduce operational costs while maintaining high performance standards across various transportation conditions.

The light commercial trucks segment held a 50% share in 2025 and is projected to grow at a CAGR of 4.1% through 2035. The increasing use of compact transport solutions is supporting demand for efficient refrigeration systems designed for smaller vehicles. These systems are optimized for urban logistics operations, offering energy-efficient performance and reduced emissions. The focus on quieter operation and precise temperature control is further enhancing their suitability for frequent delivery cycles, contributing to segment growth.

United States Truck Refrigeration Unit Market reached USD 4.5 billion in 2025. The country's growth is driven by increasing demand for temperature-controlled logistics and the expansion of refrigerated transport fleets. Adoption of advanced refrigeration technologies is being supported by environmental regulations and sustainability initiatives. The transition toward electric and hybrid refrigeration systems is gaining momentum as operators aim to reduce emissions and improve efficiency. These trends are reinforcing the country's position as a key contributor to the overall truck refrigeration unit market.

Key companies operating in the Global Truck Refrigeration Unit Market include Carrier Transicold, Daikin Industries, Frigoblock, Guchen Industry, Hubbard Products, Kingtec, MHI Thermal Systems, Schmitz Cargobull, Thermo King, and Zanotti. Companies in the Truck Refrigeration Unit Market are strengthening their market position through innovation, sustainability initiatives, and strategic partnerships. They are investing in advanced refrigeration technologies to improve energy efficiency, reduce emissions, and enhance system performance. Integration of digital solutions, such as real-time monitoring and predictive maintenance, is enabling better operational control and improved reliability. Market players are also expanding their product portfolios to address diverse transportation requirements. Collaborations with logistics providers and fleet operators are supporting wider adoption of advanced systems. Additionally, companies are focusing on developing eco-friendly refrigerants and electric-powered solutions to align with environmental regulations and evolving industry standards, ensuring long-term competitiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Temperature

- 2.2.6 End use industry

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for cold chain logistics

- 3.2.1.2 Increasing perishable food consumption

- 3.2.1.3 Stringent food safety regulations

- 3.2.1.4 Growth in pharmaceutical transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost

- 3.2.2.2 Maintenance and operational complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Electric and hybrid refrigeration units

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 IoT-enabled smart monitoring systems

- 3.2.3.4 Renewable energy-powered cooling solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Environmental Protection Agency (EPA)

- 3.4.1.2 California Air Resources Board (CARB)

- 3.4.2 Europe

- 3.4.2.1 European Commission - F-Gas Regulation

- 3.4.2.2 United Nations Economic Commission for Europe (UNECE) - ATP Agreement

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Ecology and Environment of China

- 3.4.3.2 Ministry of Land, Infrastructure, Transport and Tourism (MLIT), Japan

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Transportes Terrestres (ANTT), Brazil

- 3.4.4.2 Secretaria de Infraestructura, Comunicaciones y Transportes (SICT), Mexico

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by primary research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Vapor cycle systems

- 5.3 Cryogenic systems

- 5.4 Eutectic system

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Light commercial trucks

- 7.3 Medium-duty trucks

- 7.4 Heavy-duty trucks

Chapter 8 Market Estimates & Forecast, By Temperature, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Frozen

- 8.3 Chilled

- 8.4 Dual

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals & Healthcare

- 9.4 Chemicals

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Carrier Transicold

- 11.1.2 Daikin Industries

- 11.1.3 DENSO

- 11.1.4 Frigoblock

- 11.1.5 MHI Thermal Systems

- 11.1.6 Thermo King

- 11.1.7 Webasto Thermo

- 11.1.8 Zanotti

- 11.2 Regional players

- 11.2.1 Dongin Thermo

- 11.2.2 Guchen Industry

- 11.2.3 Hubbard Products

- 11.2.4 Hwasung Thermo

- 11.2.5 Kingtec

- 11.2.6 Schmitz Cargobull

- 11.2.7 Songz Auto

- 11.2.8 Subros

- 11.3 Emerging players

- 11.3.1 Advanced Temperature Control (ATC)

- 11.3.2 GAH Refrigeration

- 11.3.3 Great Dane

- 11.3.4 Sanden