|

시장보고서

상품코드

2038399

복합 필름 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Composite Film Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

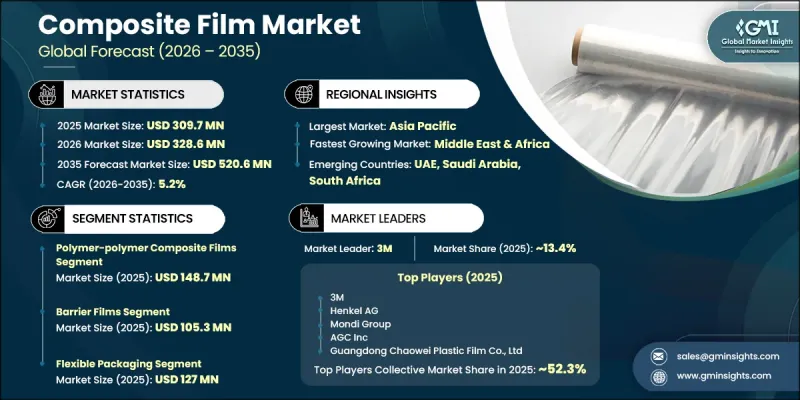

세계의 복합 필름 시장은 2025년에 3억 970만 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.2%로 성장할 전망이며, 5억 2,060만 달러에 이를 것으로 예측됩니다.

다양한 용도에서 뛰어난 내구성, 보호 성능, 기능적 효율성을 제공하는 고성능 다층 필름에 대한 산업계 수요가 증가함에 따라 시장은 꾸준히 확대되고 있습니다. 이 필름은 장벽 성능 향상, 강도 향상, 제품 수명 연장 등의 장점으로 인해 널리 사용되고 있습니다. 환경 규제와 기업의 지속가능성 목표에 따라 제조업체들이 재활용 가능한 바이오 솔루션을 우선시하는 가운데, 지속 가능한 소재로의 전환은 시장을 좌우하는 중요한 요소가 되고 있습니다. 재료 과학과 생산 기술의 지속적인 발전으로 더 높은 정밀도, 확장성 및 비용 효율성을 갖춘 복잡한 필름 구조를 만들 수 있게 되었습니다. 제품의 안전성을 보장하고 무결성을 유지하며 사용 기간을 연장하는 신뢰할 수 있는 포장 솔루션에 대한 수요가 증가하면서 시장 성장에 더욱 박차를 가하고 있습니다. 또한, 고도의 내열성, 기계적 보호 및 특수한 표면 특성을 필요로 하는 산업은 지속적인 수요에 기여하고 있으며, 현대 제조 및 포장 생태계에서 복합 필름의 중요성을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 3억 970만 달러 |

| 예측 기간 시장 규모 | 5억 2,060만 달러 |

| CAGR | 5.2% |

배리어 필름 부문은 2025년 1억 5,300만 달러 시장 규모를 차지한 것으로 평가되었으며, 다양한 분야에서의 채택이 확대되고 있음을 알 수 있습니다. 복합 필름 산업은 제품 카테고리별로 다른 성장세를 보이고 있지만, 배리어 필름은 보호 성능 향상과 보존 기간 연장에 효과적이기 때문에 여전히 지배적인 존재감을 유지하고 있습니다. 산업 및 포장 용도 분야에서 광범위하게 사용되는 것은 그 신뢰성과 기능적 성능을 반영합니다. 동시에 고도의 특성을 갖춘 고성능 필름은 정밀성, 내구성, 다기능성이 요구되는 분야에서 주목받고 있습니다. 성능 최적화와 제품 안전에 대한 관심이 높아짐에 따라 이 분야의 혁신이 지속적으로 추진되고 있으며, 제조업체들은 생산 공정의 효율성과 확장성을 유지하면서 필름의 특성을 개선하기 위해 노력하고 있습니다.

2025년 연포장 부문은 1억 2,700만 달러 시장 규모를 기록한 것으로 평가되었으며, 복합 필름 시장 수요를 견인하는 데 중요한 역할을 한 것으로 평가되었습니다. 용도 범위는 여전히 다양하지만, 제품의 보호성을 향상시키고, 보관 기간을 연장하고, 최종 사용자의 편의성을 높일 수 있기 때문에 연포장이 주요 촉진요인으로 부상하고 있습니다. 특히 각 산업계가 효율성과 지속가능성에 초점을 맞추고 있는 가운데, 가볍고 강력한 보호 기능을 갖춘 포장 솔루션에 대한 수요는 지속적으로 증가하고 있습니다. 제조업체들은 다양한 포장 형태에서 밀봉성, 내구성, 적응성을 향상시키고 열악한 환경에서도 안정적인 성능을 보장할 수 있는 첨단 필름 기술을 점점 더 많이 채택하고 있습니다.

2025년 북미의 복합 필름 시장 규모는 8,660만 달러에 달한 것으로 평가되었습니다. 이 지역은 공급업체와 최종 사용 산업과의 강력한 협력을 지원하는 잘 구축된 제조 인프라의 혜택을 누리고 있습니다. 시장 확대는 성능 기준과 재활용성을 중시하는 규제 프레임워크의 영향을 받고 있으며, 이는 첨단 복합 필름 솔루션의 채택을 촉진하고 있습니다. 산업 발전과 신기술 분야의 보호재에 대한 수요 증가는 이 지역의 성장을 지속적으로 뒷받침하고 있습니다. 혁신에 대한 집중과 지속가능성에 대한 요구가 결합되어 제품 개발의 방향을 결정하고 다양한 산업 분야에서 복합 필름 시장 입지를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 필름 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.05.28The Global Composite Film Market was valued at USD 309.7 million in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 520.6 million by 2035.

The market continues to advance steadily as industries increasingly demand high-performance, multi-layer films that offer superior durability, protection, and functional efficiency across diverse applications. These films are widely utilized due to their ability to deliver enhanced barrier performance, improved strength, and extended product lifespan. The shift toward sustainable materials is becoming a defining factor, as manufacturers prioritize recyclable and bio-based solutions to align with environmental regulations and corporate sustainability targets. Continuous developments in material science and production technologies are enabling the creation of complex film structures with higher precision, scalability, and cost efficiency. The increasing need for reliable packaging solutions that ensure product safety, maintain integrity, and extend usability further strengthens market growth. Additionally, industries requiring advanced thermal resistance, mechanical protection, and specialized surface properties are contributing to sustained demand, reinforcing the importance of composite films in modern manufacturing and packaging ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $309.7 Million |

| Forecast Value | $520.6 Million |

| CAGR | 5.2% |

The barrier films segment accounted for a USD 105.3 million in 2025, highlighting their strong adoption across multiple sectors. The composite film industry demonstrates varied growth dynamics across different product categories, with barrier films maintaining a dominant presence due to their effectiveness in enhancing protection and prolonging shelf life. Their widespread use in industrial and packaging applications reflects their reliability and functional performance. At the same time, high-performance films with advanced properties are gaining traction in sectors that demand precision, durability, and multifunctional capabilities. The growing emphasis on performance optimization and product safety continues to drive innovation within this segment, encouraging manufacturers to enhance film properties while maintaining efficiency and scalability in production processes.

The flexible packaging segment captured USD 127 million in 2025, emphasizing its critical role in driving demand within the composite film market. The application landscape remains diverse, with flexible packaging emerging as a key growth driver due to its ability to improve product protection, extend shelf life, and enhance convenience for end users. The demand for packaging solutions that combine lightweight properties with strong protective capabilities continues to rise, particularly as industries focus on efficiency and sustainability. Manufacturers are increasingly adopting advanced film technologies that enable improved sealing, durability, and adaptability across various packaging formats, ensuring consistent performance in demanding environments.

North America Composite Film Market accounted for USD 86.6 million in 2025. The region benefits from a well-established manufacturing infrastructure that supports strong collaboration between suppliers and end-use industries. Market expansion is influenced by regulatory frameworks that emphasize performance standards and recyclability, encouraging the adoption of advanced composite film solutions. Industrial development and increasing demand for protective materials in emerging technology sectors continue to support regional growth. The focus on innovation, combined with evolving sustainability requirements, is shaping product development and strengthening the market presence of composite films across various industries.

Key companies operating in the Global Composite Film Market include 3M, Mondi Group, Henkel AG, AGC Inc, Park Aerospace Corp., Benison, Hysum, Fengchen Group Co., Ltd, Shandong Top Leader Plastic Packing Co., Ltd, Guangdong Chaowei Plastic Film Co., Ltd, Huizhou Yangrui Printing & Packaging Co., Ltd, and Krus Company. Companies in the Composite Film Market are actively strengthening their position through continuous investment in research and development to enhance product performance and sustainability. Manufacturers are focusing on developing advanced multi-layer films with improved barrier properties, durability, and recyclability to meet evolving regulatory and consumer expectations. Strategic partnerships and collaborations with end-use industries are enabling companies to better align product innovation with application-specific requirements. Expansion of production capacities and adoption of advanced manufacturing technologies are improving operational efficiency and scalability. Additionally, firms are emphasizing sustainable material sourcing, circular economy initiatives, and eco-friendly product portfolios to gain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in gold & silver mining activities

- 3.2.1.2 Rising gold prices & investment demand

- 3.2.1.3 Technological advancements in cyanidation processes.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns & catastrophic spill incidents

- 3.2.2.2 Stringent regulatory constraints & compliance costs.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing mining activities in emerging economies

- 3.2.3.2 Advancements in safer cyanide handling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Polymer-Polymer Composite Films

- 5.2.1 PE/PP Combinations

- 5.2.2 PET/PA Combinations

- 5.2.3 Multi-Layer Polyolefin Structures

- 5.2.4 Specialty Polymer Blends

- 5.3 Polymer-Metal Composite Films

- 5.3.1 Metallized Films (Aluminum Deposition)

- 5.3.2 Metal Foil Laminated Films

- 5.4 Polymer-Paper Composite Films

- 5.4.1 Paper-Polymer Laminates

- 5.4.2 Coated Paper Composite Structures

- 5.5 Specialty Composite Films

- 5.5.1 Biodegradable & Compostable Composites

- 5.5.2 Ceramic-Enhanced Films

- 5.5.3 Hybrid Multi-Substrate Films

Chapter 6 Market Estimates and Forecast, By Film Type, 2022 - 2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Barrier Films

- 6.2.1 Moisture Barrier Films

- 6.2.2 Oxygen Barrier Films

- 6.2.3 Light Barrier Films

- 6.2.4 Multi-Barrier Films

- 6.3 Conductive Films

- 6.3.1 Electrically Conductive Films

- 6.3.2 Thermally Conductive Films

- 6.4 Adhesive Films

- 6.4.1 Pressure-Sensitive Adhesive Films

- 6.4.2 Heat-Activated Adhesive Films

- 6.5 Optical Films

- 6.5.1 Transparent Films

- 6.5.2 Reflective Films

- 6.5.3 Diffusion Films

- 6.6 Protective Films

- 6.6.1 Scratch-Resistant Films

- 6.6.2 UV-Protective Films

- 6.6.3 Surface Protection Films

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Flexible Packaging

- 7.2.1 Food Packaging

- 7.2.2 Beverage Packaging

- 7.2.3 Pharmaceutical Packaging

- 7.2.4 Personal Care Packaging

- 7.3 Industrial Applications

- 7.3.1 Construction Films

- 7.3.2 Insulation Films

- 7.3.3 Protective Wrapping

- 7.4 Electronics & Electrical

- 7.4.1 Display Films

- 7.4.2 Circuit Board Films

- 7.4.3 Capacitor Films

- 7.5 Automotive & Transportation

- 7.5.1 Interior Trim Films

- 7.5.2 Glazing Films

- 7.5.3 Protective Films

- 7.6 Aerospace & Defense

- 7.6.1 Structural Composite Films

- 7.6.2 Protective Coating Films

- 7.7 Medical & Healthcare

- 7.7.1 Medical Device Packaging

- 7.7.2 Diagnostic Films

- 7.7.3 Sterile Barrier Films

- 7.8 Agriculture

- 7.8.1 Greenhouse Films

- 7.8.2 Mulch Films

- 7.8.3 Silage Wraps

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Benison

- 9.3 Fengchen Group Co.,Ltd

- 9.4 Guangdong Chaowei Plastic Film Co., Ltd

- 9.5 Shandong Top Leader Plastic Packing Co.,Ltd

- 9.6 Hysum

- 9.7 Huizhou Yangrui Printing & Packaging Co.,Ltd

- 9.8 Henkel AG

- 9.9 Mondi Group

- 9.10 AGC Inc

- 9.11 Krus company

- 9.12 Park Aerospace Corp