|

시장보고서

상품코드

2073323

유럽의 SPC 바닥재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Stone Plastic Composite (SPC) Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

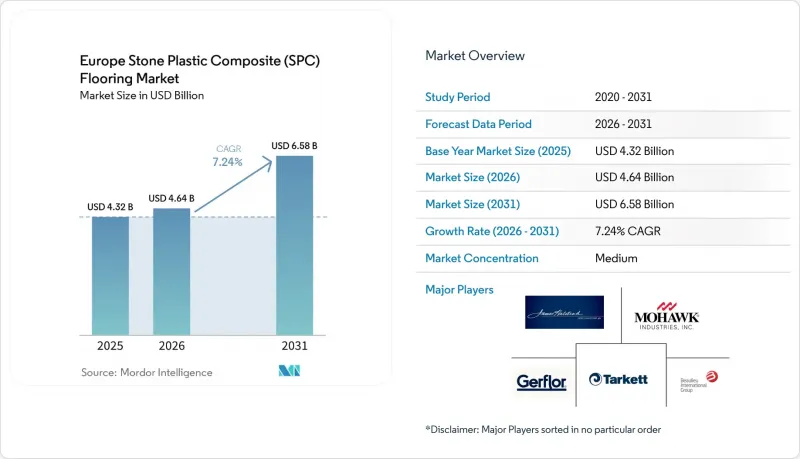

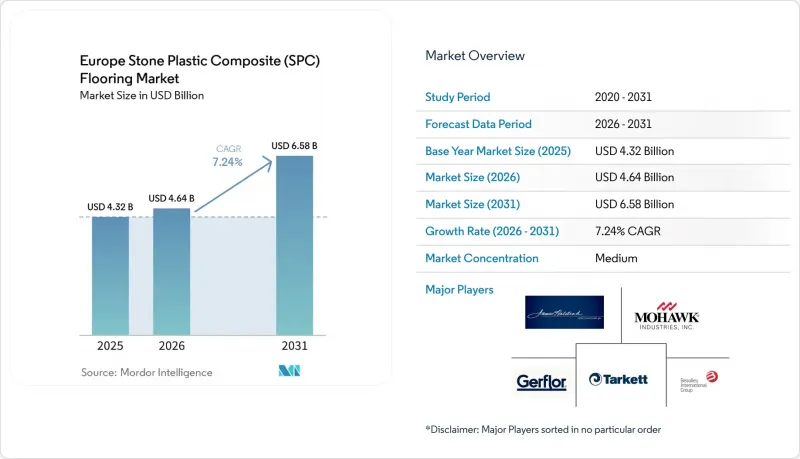

Mordor Intelligence에 의하면, 유럽의 SPC 바닥재 시장 규모는 2025년 43억 2,000만 달러로 평가되었습니다. 2026년에는 46억 4,000만 달러로 확대되어 2031년까지 65억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 7.24%로 성장할 전망입니다.

본 보고서는 제품 유형(SPC 타일, SPC 플랭크), 제품 두께(4.0-5.0 mm, 5.1-6.0 mm, 6.1-6.5 mm, 6.5 mm 이상), 최종 사용자(주거용, 상업용), 유통 채널(B2C/소매, B2B/시공업체), 지역(영국, 독일, 프랑스, 스페인, 이탈리아, 베네룩스, 북유럽 국가, 기타 유럽)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 SPC 바닥재 시장 동향 및 분석

건축물 에너지 성능 지침(EPBD) 개정과 리모델링 붐, 공사에 미치는 영향을 최소화한 신속한 바닥재에 대한 수요

EPBD 개정안에 따라, 회원국들은 개정된 에너지 성능 규정을 국내법에 반영하고, 신축 건물에 대해 전 생애 주기에 걸친 평가를 도입해야 합니다. 이에 따라 개보수 공사에서 시공의 신속성, 탄소 효율성, 그리고 운영에 미치는 영향을 최소화할 수 있는 자재의 중요성이 강조되고 있습니다. SPC의 경질 광물 코어 덕분에 기존의 다양한 바닥 바탕재 위에 직접 시공이 가능해졌으며, 시공업체는 입주자가 거주 중인 건물이나 영업을 계속해야 하는 공공시설에서 공사 기간을 단축할 수 있습니다. 프랑스의 SPC 판매량은 2024년에 1,390만 m²에 달했으며, 유틸리티 및 소비자의 선호도가 신속한 시공 솔루션과 부합함에 따라 2년 연속 독일의 판매량을 앞질렀습니다. 유럽 제조업계의 자본 투자도 이러한 추세를 뒷받침하고 있으며, 그 예로 유니린(Unilin)이 2025년에 리모델링 용도를 겨냥한 경질 포맷의 생산 및 표면 맞춤화를 가속화하기 위한 투자를 단행할 예정이라는 점을 들 수 있습니다. 북유럽 시장에서는 정책과 제품 선택 간의 연관성이 더욱 강화되고 있으며, 덴마크와 노르웨이에서는 엄격한 공공 조달 기준을 배경으로 견조한 성장이 이어지는 가운데, 2024년에 각각 SPC 판매량이 100만 m²를 넘어섰습니다. 이러한 상황들이 맞물리면서, 행정 기관이나 건물 소유주들이 업무에 미치는 지장을 최소화하며 시공할 수 있는 인증 제품을 우선적으로 선택함에 따라, 예산과 사양이 유럽의 SPC 바닥재 시장으로 집중되고 있습니다.

MMF 시장에서 SPC의 점유율 확대, 리지드 코어 사양으로의 전환

유럽의 다층 모듈러 바닥재(MMF) 시장에서 SPC의 점유율은 2023년 65%에서 2024년 75%로 성장했습니다. 이는 사양을 결정한 측에서 나뭇결이나 돌무늬의 범용성뿐만 아니라 치수 안정성도 중시했기 때문입니다. 이 카테고리의 변화는 구매자들이 습도 변동이나 심한 통행에 강한 리지드 코어 제품에 주목함에 따라, LVT의 클릭률(CTR) 및 EPC 하락과 상관관계를 보였습니다. 이탈리아와 폴란드 등 시장에서는 2024년에 폴리머 제품의 매출이 크게 증가했습니다. 이는 보수 공사에서 방수성과 내마모성이 뛰어난 표면을 선호하는 소비자 및 공공기관의 프로젝트가 배경에 있습니다. 2025년 3월 MMFA가 SPC의 환경제품선언서(EPD)를 공표함에 따라, 회원사들은 공공 조달 기관에 환경 성능을 표준화된 방식으로 제시할 수 있게 되었으며, 검증된 수명주기 데이터가 요구되는 입찰 과정에서 규정 준수 및 서류 작성을 지원받게 되었습니다. 2024년 스페인의 회복 추세에서는 객실 회전율 향상과 유동 인구가 많은 공간의 체계적인 유지 관리를 중시하며, 리지드 코어 타일의 외관을 선호하는 호텔·리조트 업계와 복합 용도 프로젝트가 두드러졌습니다. 이러한 선택 경향에 따라 사양은 계속해서 SPC로 전환되고 있으며, 신축 사이클의 둔화에도 불구하고 유럽 SPC 바닥재 시장의 판매량 증가를 뒷받침하고 있습니다.

PFAS 관련 탑코트 재조성에 따른 위험

EU의 REACH 규정에 따른 PFAS 제한은 고성능 표면 처리에 사용되는 도료 및 첨가제에 불확실성을 초래하고 있으며, 공급업체들은 대체 화학 물질의 검증을 조기에 진행하도록 촉구받고 있습니다. 많은 브랜드들이 문제가 있는 첨가제에 의존하지 않으면서도 가혹한 사용 조건 기준을 충족하는 저배출·고내구성 마감재를 강조하고 있으며, 이러한 추세는 ECHA의 PFAS 제안이 진전됨에 따라 계속되고 있습니다. 공공 프로젝트의 조달 기준에서는 일반적으로 문서화 및 제3자 기관의 시험이 평가 대상이 되므로, 기업들은 코팅 시스템이 예상되는 규정을 준수하도록 권장받고 있습니다. 이로 인해 공급업체는 사양을 유지하기 위해 EN 13329에 따른 마모 시험과 배출량 측정 결과를 함께 실시해야 하므로, 제품 개발에 시간과 비용이 소요될 수 있습니다. 각 브랜드가 제품 라인업을 PFAS 무함유 제품으로 전환함에 따라, 유럽 SPC 바닥재 시장의 프리미엄 라인 출시 일정 및 제품 구성 결정에 전환 기간의 영향이 미칠 가능성이 있습니다.

부문별 분석

2025년, 유럽 SPC 바닥재 시장에서 SPC 플랭크는 69.50%의 시장 점유율을 차지했습니다. 이는 나뭇결 무늬 디자인을 선호하는 소비자의 취향과, 리모델링 프로젝트에서 신속한 플로팅 시공을 필요로 하는 시공업체의 요구를 반영한 것입니다. 유럽의 SPC 바닥재 시장은 이 제품이 동일한 코어 크기와 내마모층을 사용함으로써 DIY 시장과 전문가용 유통 채널을 연결해 줄 수 있다는 장점에 힘입어 성장하고 있습니다. 이를 통해 재고 관리가 간소화되고, 거주 중인 현장에서의 시공 시간이 단축됩니다. 클릭식 프로파일이나 일체형 하부재는 소음 전달을 줄이는 데 도움이 되며, 이는 공동주택이나 최상층의 리모델링 공사에서 여전히 중요한 요소로 남아 있습니다. 또한, 유럽의 SPC 바닥재 시장에서는 견고한 마모층과 레지스터 엠보싱 가공의 질감을 결합하여 주거 공간이나 소매 공간의 현실감을 높여주는 제품 라인에도 가치가 인정받고 있습니다. 이러한 시공 속도, 미관, 그리고 시공 다음 날 바로 유지보수가 가능하다는 장점들이 결합되어, 플랭크는 주택 리모델링 분야에서 가장 먼저 고려되는 선택지가 되었으며, 소규모 상업시설 프로젝트에서도 널리 사용되고 있습니다.

SPC 타일은 호텔·리조트, 의료시설, 복합 용도 시설의 리노베이션 과정에서 운영 시간을 유지할 수 있는 대형 석재풍 디자인과 미끄럼 방지 처리가 우선시됨에 따라, 2031년까지 연평균 성장률(CAGR) 7.40%를 기록하며 성장할 것으로 전망됩니다. 유럽의 SPC 바닥재 시장에서 타일 형태 시장 규모는 공공 프로젝트 및 호텔 객실용으로 크기, 두께, 마감 처리를 최적화한 지역 특화형 제품의 출시와 함께 확대될 것으로 예측됩니다. 타일 배치를 통해 정사각형 방이나 개방된 공간에서 발생하는 폐기물을 줄일 수 있으며, 복도나 로비에 접착 시공을 하면 트롤리나 들것이 빈번하게 사용되는 장소에서 점하중을 견디는 능력을 높일 수 있습니다. 그리스 시장에 출시된 Elegance Rigid 55를 포함한 남유럽용 신규 제품 라인업은 각 브랜드가 명확한 성능 평가를 바탕으로 고부하 주거용 및 중부하 상업용 시장에 미네랄 코어 타일을 어떻게 포지셔닝하고 있는지를 보여줍니다. 공공 조달 분야에서 인증된 자재와 예측 가능한 유지보수가 중요시되는 가운데, 석재와 같은 미적 통일감과 뛰어난 청결성을 살릴 수 있는 프로젝트에서 타일 디자인은 유럽의 SPC 바닥재 시장에서 꾸준히 시장 점유율을 확대해 나갈 것입니다.

5.1-6.0 mm 두께 대는 2025년에 33.60%의 시장 점유율을 차지했으며, 일상적인 사용에 있어 비용, 무게, 성능의 균형을 맞추는 것으로 이 카테고리의 판매량 중심을 지탱하고 있습니다. 이 두께 범위는 중급 주택이나 경량 상업시설에 적합하며, 플로팅 시공과 일체형 하부재의 조합을 통해 쾌적성과 방음성을 손쉽게 실현할 수 있습니다. 이 범위의 제품 라인업에서는 포름알데히드가 없거나 휘발성이 낮다는 점을 강조할 뿐만 아니라, 클래스 23 또는 31 인증을 획득하여 설치 가능한 공간의 범위를 넓힌 사례가 많이 보입니다. 시장에서의 구체적인 예로는 현대식 아파트용으로 클릭식 시공의 용이성, 내구성, 그리고 표준 바닥 난방 시스템과의 호환성을 강조하며 가성비가 뛰어난 리지드 코어 제품 라인을 들 수 있습니다. 유럽의 SPC 바닥재 시장은 이러한 최적의 조건을 바탕으로 전문 소매점 및 업자용 계정 모두에서 안정적인 판매 실적을 유지하고 있습니다.

고급 주택 및 프리미엄 상업시설의 사양 담당자들이 바닥의 견고성과 충격음 성능 향상을 요구하는 가운데, 두께 6.5mm를 초과하는 제품은 2031년까지 연평균 성장률(CAGR) 7.85%를 나타낼 것으로 예측됩니다. 이러한 두께를 가진 프로파일을 사용하는 유럽의 SPC 바닥재 시장 규모는 방음 성능 향상과 굴림 하중에 대한 함몰 저항성을 중시하는 프로젝트가 확대됨에 따라 더욱 성장할 것으로 보입니다. 소매 시장에서는 코어 밀도 향상과 일체형 단열재의 채택을 통해, 이용 빈도가 높은 공간에서도 클릭식 시공의 편의성을 유지하면서 사용 등급 클래스 23 및 34의 요건을 충족한다는 사실이 입증되었습니다. 프랑스의 EPR 에코모듈레이션 프레임워크는 암반 단면에 손상을 주지 않으면서도 해체 및 재설치를 견딜 수 있는 설계를 더욱 장려하고 있으며, 이를 통해 순환형 모델에 견고한 코어를 도입하는 것이 더욱 타당해졌습니다. 예측 기간 동안, 제곱미터당 비용 대비 뛰어난 음향 성능과 내구성이 중시되는 공간에서는 두꺼운 형식 시장 침투율이 계속해서 높아질 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe stone plastic composite flooring market size is expected to increase from USD 4.32 billion in 2025 to USD 4.64 billion in 2026 and reach USD 6.58 billion by 2031, growing at a CAGR of 7.24% over 2026-2031.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, Above 6. 5 Mm), End User (Residential, Commercial), Distribution Channel (B2C/Retail, B2B/Contractors), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Energy Performance of Buildings Directive (EPDB) Recast and Renovation Wave, Fast Low-Disruption Flooring Demand

The EPBD recast requires member states to transpose updated energy performance rules and to adopt whole-life-cycle assessments for new buildings, which underscores the importance of materials that combine speed, carbon efficiency, and low operational disruption in retrofit work. SPC's rigid mineral core enables direct installation over many existing substrates, helping contractors compress schedules in occupied buildings and public facilities that must remain open. SPC volumes in France reached 13.9 million m2 in 2024, surpassing Germany for a second year as public programs and consumer preferences aligned with quick install solutions. Capital deployment within European manufacturing reinforces this direction, including Unilin's 2025 investment to accelerate production and surface customization for rigid formats that target renovation use cases. Nordic markets reinforce the connection between policy and product choice, with Denmark and Norway each exceeding 1 million m2 of SPC in 2024 alongside strong growth from a base of demanding public procurement standards. These conditions collectively channel budget and specifications toward the European SPC flooring market as agencies and building owners prioritize certified products that can be installed with minimal disruption.

SPC Share Gains Within MMF, Rigid Core Specification Shift

Within Europe's multilayer modular flooring (MMF) ecosystem, SPC expanded its share to 75% of the MMF category in 2024, up from 65% in 2023, as specifiers favored dimensional stability alongside wood- and stone-look versatility. The category shift correlated with declines in LVT click-through rate (CTR) and EPC as buyers converged on rigid cores that better withstand moisture variation and heavy traffic. Markets such as Italy and Poland posted strong 2024 increases in polymer products, reflecting consumer and institutional projects that prefer waterproof, scratch-resistant surfaces in refurbishments. The publication of an SPC EPD by MMFA in March 2025 provides members with a standardized way to communicate environmental performance to public buyers, supporting bid compliance and documentation in tenders that require verified life-cycle data. Spain's 2024 rebound highlighted hospitality and mixed-use projects that favor rigid-core tile looks for faster room turns and coordinated maintenance in high-traffic spaces. This set of choices continues to move specifications toward SPC, supporting volume growth in the European SPC flooring market even as new-build cycles soften.

PFAS-Related Topcoat Reformulation Risks

The EU REACH PFAS restriction creates uncertainty for coatings and auxiliaries used in high-performance surface treatments, prompting suppliers to validate alternative chemistries early. Many brands have highlighted low-emission, durable finishes that meet intensive-use standards without relying on problematic additives, and this trend continues as the ECHA PFAS proposal evolves. Procurement criteria in public projects typically reward documentation and third-party testing, incentivizing companies to align coating systems with anticipated restrictions. This can add time and cost to product development as suppliers test EN 13329 wear testing alongside emissions outcomes to maintain specifications. As brands move their ranges toward PFAS-free products, the transition period may shift launch calendars and assortment decisions for premium lines in the European SPC flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Phthalate Free Rigid LVT/SPC, VOC Rules Speed Substitution

- EU Circularity Programs, EPR, and Ecolabels Accelerate Recycled Content Use

- Construction Slowdown and Raw Material Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 69.50% of Europe's SPC flooring market share in 2025, reflecting consumer preference for wood look visuals and installers' need for fast, floating systems in renovation projects. The European SPC flooring market benefits from this format's ability to bridge the DIY and professional channels by using the same core sizes and wear layers, simplifying inventory and shortening installation time on occupied sites. Click profiles and integrated underlays help reduce noise transmission, which remains important in multi-family buildings and top-floor conversions. The European SPC flooring market also sees value in product lines that pair robust wear layers with embossed-in-register textures to improve realism in living spaces and retail zones. This combination of speed, aesthetics, and day-two maintenance advantages makes planks the default choice in residential upgrades and a mainstay in light commercial programs.

SPC tiles are projected to grow at a 7.40% CAGR to 2031 as hospitality, healthcare, and mixed-use refurbishments prioritize large-format stone looks and slip-resistant finishes that maintain uptime. The European SPC flooring market size for tile formats is expected to expand alongside region-specific launches that tailor formats, thicknesses, and finishes for public projects and hotel rooms. Tile layouts can reduce waste in square rooms and open areas, and glue-down installation in corridors or lobbies can enhance point load resilience where trolleys or gurneys are common. New assortments for Southern Europe, including Elegance Rigid 55, introduced for Greece, show how brands position mineral core tiles for heavy residential and moderate commercial applications with clear performance ratings. As public procurement emphasizes certified materials and predictable maintenance, tile designs will steadily capture a larger slice of the European SPC flooring market in projects that benefit from stone aesthetic continuity and robust cleanability.

The 5.1-6.0 mm band captured a 33.60% share in 2025, anchoring the volume center of the category by balancing cost, weight, and performance for everyday use. This range serves mid-tier residential and light commercial environments where floating installation and integrated underlay offer a straightforward path to comfort and sound control. Company assortments in this zone often highlight formaldehyde-free and low-emission claims, as well as Class 23 or 31 ratings that broaden placement options across rooms. Examples on the market include budget-oriented rigid core lines that promote click ease, durability, and compatibility with standard underfloor heating systems for modern apartments. The European SPC flooring market relies on this sweet spot to deliver consistent throughput across both specialty retail and trade accounts.

Formats above 6.5 mm are projected to grow at a 7.85% CAGR through 2031 as specifiers in luxury residential and premium commercial segments seek greater underfoot solidity and improved impact sound performance. The European SPC flooring market size for these thicker profiles will scale with projects that emphasize acoustic upgrades and dent resistance under rolling loads. Retail offerings demonstrate how added core density and integrated insulation help meet Class 23 and 34 use ratings while preserving click install convenience in intensive spaces. France's EPR eco-modulation framework further favors designs that withstand disassembly and reinstallation without damage to locking profiles, thereby strengthening the case for robust cores in circular models. Over the forecast, thicker formats will continue to gain penetration in rooms where premium acoustics and durability carry more weight than cost per square meter.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B/Contractors/Builders

- B2C/Retail

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX

- NORDICS

- Rest of Europe

List of Companies Covered in this Report:

- Mohawk Industries (Unilin/Quick-Step

- IVC/Moduleo)

- Tarkett

- Gerflor

- Beaulieu International Group (BerryAlloc)

- James Halstead plc (Polyflor)

- Karndean Designflooring

- CFL Flooring (FirmFit, NovoCore)

- Kahrs Group

- Kronospan

- Parador

- Decora S.A. (Arbiton, Afirmax)

- Amtico (Mannington)

- COREtec (USFloors Europe/Shaw)

- Moduleo (Unilin Flooring)

- Quick-Step (Unilin/Mohawk)

- BerryAlloc (Beaulieu International Group)

- Polyflor (James Halstead)

- Windmoller (wineo)

- Novalis International

- PROJECT FLOORS GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy Performance of Buildings Directive recast and Renovation Wave accelerate residential and public building retrofits (demand pull for fast, low-disruption flooring)

- 4.2.2 SPC's rising share within multilayer modular flooring (MMF) channels shifts specifications toward rigid core designs

- 4.2.3 Low-VOC and phthalate restrictions drive phthalate-free rigid LVT/SPC adoption

- 4.2.4 Brand and EU circularity programs (VinylPlus, EU Ecolabel/CPR/ESPR) reward recycled content and traceability

- 4.2.5 REACH diisocyanates training nudges installers from glue-down to click rigid-core systems

- 4.2.6 Under-the-radar: France PMCB EPR eco-modulation (bonuses/penalties) favors recyclable, detachable, take-back-ready SPC

- 4.3 Market Restraints

- 4.3.1 Broad PFAS restriction proposals could affect topcoats/auxiliaries, raising reformulation risk

- 4.3.2 Construction slowdown and logistics/raw-material cost swings pressure demand and margins

- 4.3.3 France PMCB EPR eco-contributions increase producer/importer compliance costs

- 4.3.4 EU fire classification (Bfl-s1/s1 smoke) plus acoustic layers add testing/CE-mark costs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B/Contractors/Builders

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Spain

- 5.6.5 Italy

- 5.6.6 BENELUX

- 5.6.7 NORDICS

- 5.6.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Mohawk Industries (Unilin/Quick-Step; IVC/Moduleo)

- 6.4.2 Tarkett

- 6.4.3 Gerflor

- 6.4.4 Beaulieu International Group (BerryAlloc)

- 6.4.5 James Halstead plc (Polyflor)

- 6.4.6 Karndean Designflooring

- 6.4.7 CFL Flooring (FirmFit, NovoCore)

- 6.4.8 Kahrs Group

- 6.4.9 Kronospan

- 6.4.10 Parador

- 6.4.11 Decora S.A. (Arbiton, Afirmax)

- 6.4.12 Amtico (Mannington)

- 6.4.13 COREtec (USFloors Europe/Shaw)

- 6.4.14 Moduleo (Unilin Flooring)

- 6.4.15 Quick-Step (Unilin/Mohawk)

- 6.4.16 BerryAlloc (Beaulieu International Group)

- 6.4.17 Polyflor (James Halstead)

- 6.4.18 Windmoller (wineo)

- 6.4.19 Novalis International

- 6.4.20 PROJECT FLOORS GmbH

7 Market Opportunities & Future Outlook

- 7.1 Retrofit-in-a-day SPC packages: click SPC with integrated acoustic underlay and doorway transition systems to minimize downtime for EPBD-driven renovations

- 7.2 Low-embodied-carbon, PFAS-free SPC with verified EPD/DPP to win green public procurement and healthcare/education tenders