|

시장보고서

상품코드

2038406

페인트 보호 필름 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Paint Protection Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

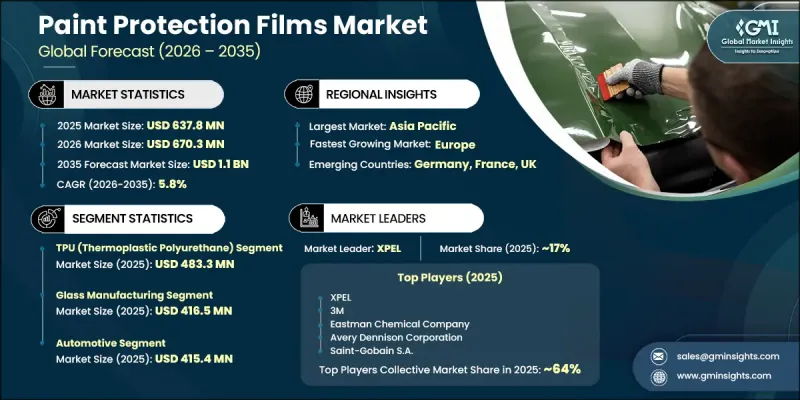

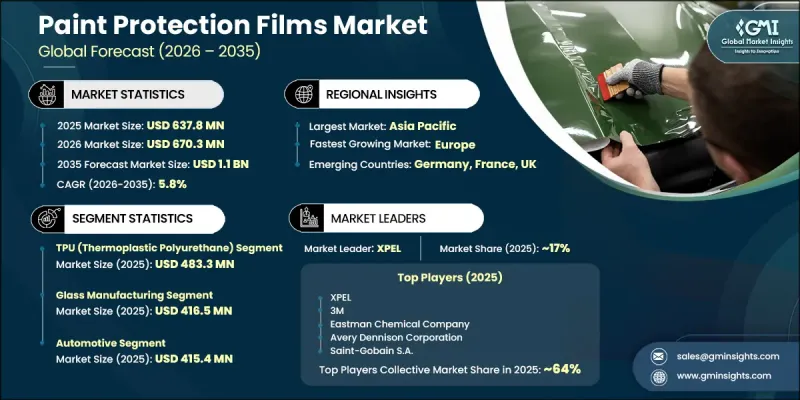

세계의 페인트 보호 필름 시장은 2025년에 6억 3,780만 달러로 평가되었고 CAGR 5.8%로 성장하여 2035년까지 11억 달러에 이를 것으로 예측됩니다.

OEM 및 애프터마켓 채널 모두에서 차량 표면 보호에 대한 수요가 지속적으로 증가함에 따라 시장은 꾸준히 성장하고 있습니다. 이러한 성장은 장기적인 자산 보호와 외관 유지를 중시하는 소유주가 많은 프리미엄 및 고급차 판매 증가와 밀접한 관련이 있습니다. 또한, 가처분 소득이 증가함에 따라 소비자들은 차량의 상태와 재판매 가치를 유지하는 데 도움이 되는 고성능 외장 보호 솔루션에 적극적으로 투자하고 있습니다. 또한 스크래치, 자외선, 변색 및 환경적 마모로부터의 보호에 대한 소비자의 인식이 높아짐에 따라 시장 확대가 가속화되고 있습니다. 도시 소비자들은 차량 사용 빈도가 높고 재판매 가격을 중시하는 경향이 강하기 때문에 페인트 보호 필름의 채택이 증가하고 있습니다. 내구성, 광학 투명도, 자기복원 특성이 향상된 첨단 소재로의 전환은 모든 차종 부문에서 제품 채택을 촉진하고 있습니다. 필름 배합의 지속적인 혁신을 통해 시공 효율과 장기적인 성능의 신뢰성을 향상시키고 있습니다. 자동차 제조업체들은 페인트 보호 필름을 단순한 옵션 액세서리가 아닌 필수적인 자동차 유지보수 솔루션으로 포지셔닝하는 추세이며, 이에 따라 전 세계적으로 미드레인지 및 프리미엄 차종 카테고리에서 페인트 보호 필름의 보급이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 6억 3,780만 달러 |

| 예측 규모 | 11억 달러 |

| CAGR | 5.8% |

2025년 기준, TPU 부문은 4억 8,330만 달러를 차지했습니다. 소재 유형에 따른 시장 세분화는 내구성, 성능 효율성 및 비용 구조의 차이를 반영합니다. 열가소성 폴리우레탄(TPU) 필름은 뛰어난 유연성, 높은 투명성, 자기복원 기능으로 인해 고급 자동차 용도에 매우 적합하여 수요가 많습니다. 첨단 재료공학에 대한 관심이 높아지면서 제조업체들은 마모, 자외선 및 환경적 악화에 대한 내성을 강화하기 위해 노력하고 있습니다. 이로 인해 전 세계 자동차 보호 솔루션에서 TPU의 채택이 더욱 확대되고 있습니다.

광택 마감 부문은 2025년 4억 1,650만 달러를 차지할 것으로 예측됩니다. 마감재에 따른 세분화는 차량 미관 및 표면의 외관 개선에 대한 소비자의 선호도 변화에 따라 형성되고 있습니다. 광택 유형의 보호 필름은 특히 고급차 분야에서 광택과 시각적 매력을 향상시켜 공장 출고 시와 같은 광택과 마감을 구현하기 위해 지속적으로 수요를 주도하고 있습니다. 이러한 선호는 고급차 및 고성능 자동차 카테고리 전반에서 꾸준한 채택을 촉진하고 있습니다.

2025년 북미 페인트 보호 필름 시장은 1억 9,250만 달러 규모를 차지했습니다. 이 지역 시장 확대는 소비자의 높은 구매력, 뿌리 깊은 자동차 커스터마이징 문화, 첨단 TPU 기반 보호 기술에 대한 선호도 증가로 뒷받침되고 있습니다. 딜러, 디테일링 서비스 제공업체, 디지털 소매 플랫폼 등 이미 구축된 유통 네트워크의 존재는 제품의 접근성을 향상시키고 있습니다. 차량의 외관을 유지하면서 재판매 가치를 높이는 것에 대한 소비자의 관심이 높아지면서 이 지역의 자동차 애프터마켓 전체 수요를 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 마감 유형별, 2022-2035년

제7장 시장 추산 및 예측 : 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.05.29The Global Paint Protection Films Market was valued at USD 637.8 million in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 1.1 billion by 2035.

The market is advancing steadily as demand for vehicle surface preservation continues to rise across both OEM and aftermarket channels. Growth is strongly linked to increasing sales of premium and luxury automobiles, where owners prioritize long-term asset protection and visual appeal retention. Rising disposable incomes are also encouraging consumers to invest in high-performance exterior protection solutions that help maintain vehicle condition and resale value. The market expansion is further supported by growing consumer awareness regarding protection against scratches, UV exposure, discoloration, and environmental wear. Urban consumers are adopting paint protection films more frequently due to higher vehicle usage and stronger emphasis on resale pricing. The shift toward advanced materials with enhanced durability, optical clarity, and self-repairing characteristics is strengthening product adoption across vehicle segments. Continuous innovation in film formulations is also improving installation efficiency and long-term performance reliability. Manufacturers are increasingly positioning paint protection films as essential automotive maintenance solutions rather than optional accessories, which is expanding their penetration across mid-range and premium vehicle categories globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $637.8 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 5.8% |

The TPU segment accounted for USD 483.3 million in 2025. Market segmentation based on material type reflects differences in durability, performance efficiency, and cost structure. Thermoplastic polyurethane films are witnessing strong demand due to their excellent flexibility, high transparency, and self-healing functionality, making them highly suitable for high-end automotive applications. Increasing focus on advanced material engineering is driving manufacturers to enhance resistance against abrasion, UV exposure, and environmental degradation. This is further strengthening TPU adoption across global automotive protection solutions.

The gloss finish segment represented USD 416.5 million in 2025. Finish-based segmentation is shaped by evolving consumer preferences for vehicle aesthetics and surface appearance enhancement. Gloss-style protective films continue to dominate demand as they deliver a polished, factory-like finish while improving shine and visual appeal, particularly in premium vehicle applications. This preference is reinforcing steady adoption across luxury and performance vehicle categories.

North America Paint Protection Films Market accounted for USD 192.5 million in 2025. Market expansion in the region is supported by high consumer purchasing power, strong automotive customization culture, and increasing preference for advanced TPU-based protection technologies. The presence of well-established distribution networks, including dealerships, detailing service providers, and digital retail platforms, is improving product accessibility. Rising consumer inclination toward maintaining vehicle appearance while enhancing resale value continues to drive demand across the regional automotive aftermarket.

Major players operating in the Global Paint Protection Films Industry are 3M, Avery Dennison Corporation, Eastman Chemical Company, BASF SE, XPEL, Saint-Gobain S.A., ORAFOL Europe GmbH, ClearPro, Profilm, GLOBAL WINDOW FILMS, STEK-USA, Bluegrass Protective Films LLC, Madico, Inc., and Nexfil. Companies operating in the Paint Protection Films Market are focusing on strengthening product innovation pipelines by investing in advanced polymer technologies that enhance durability, clarity, and self-healing performance. Many players are expanding manufacturing capacities and improving coating technologies to achieve higher efficiency and consistent quality output. Strategic partnerships with automotive OEMs and aftermarket service providers are being used to secure long-term supply agreements and improve brand visibility. Firms are also increasing their presence through digital sales channels and installation service networks to reach a wider customer base. Sustainability-focused product development, including recyclable film materials and environmentally friendly adhesives, is gaining traction as regulatory pressure increases.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Finish Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for luxury and premium vehicles

- 3.2.1.2 Increasing focus on vehicle aesthetics and resale value

- 3.2.1.3 Advancements in self-healing TPU technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and product cost

- 3.2.2.2 Availability of substitute solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Rising penetration in electric and premium vehicle segment

- 3.2.3.2 Expansion in emerging markets and aftermarket channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Form

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million) (000' Square Meters)

- 5.1 Key trends

- 5.2 TPU

- 5.3 PVC

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Finish Type, 2022 - 2035 (USD Million) (000' Square Meters)

- 6.1 Key trends

- 6.2 Gloss

- 6.3 Matte

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (000' Square Meters)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 Passenger cars

- 7.2.1.1 Compact

- 7.2.1.2 Midsize

- 7.2.1.3 SUV

- 7.2.1.4 Luxury

- 7.2.2 Light commercial vehicles

- 7.2.3 Heavy commercial vehicles

- 7.2.4 Off-highway vehicles

- 7.2.1 Passenger cars

- 7.3 Electrical & electronics

- 7.4 Construction

- 7.5 Aerospace & defence

- 7.6 Others (industrial, energy, marine)

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (000' Square Meters)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Eastman Chemical Company

- 9.2 3M

- 9.3 Avery Dennison Corporation

- 9.4 BASF SE

- 9.5 XPEL

- 9.6 Saint-Gobain S.A.

- 9.7 ORAFOL Europe GmbH

- 9.8 ClearPro

- 9.9 Profilm

- 9.10 GLOBAL WINDOW FILMS

- 9.11 STEK-USA

- 9.12 Bluegrass Protective Films LLC

- 9.13 Madico, Inc.

- 9.14 Nexfil