|

시장보고서

상품코드

2011930

페인트 보호 필름 시장 : 유형별, 마감 유형별, 최종 이용 산업별, 시스템별, 지역별 - 세계 예측(-2030년)Paint Protection Films Market by Type (TPU, PVC, PET), System (Waste-based, Solvent-based), Finish Type (Matte, Gloss, Satin), End-use Industry (Automotive & Transportation, Electrical & Electronics), and Region - Global Forecast to 2030 |

||||||

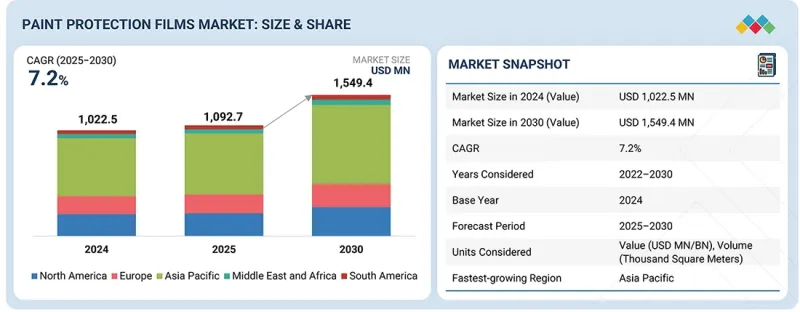

페인트 보호 필름 시장 규모는 2025년에 10억 9,270만 달러이며, 예측 기간 동안 CAGR 7.2%를 기록하며 2030년까지 15억 4,940만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만/10억 달러) 및 수량(1,000평방 미터) |

| 부문 | 유형별, 마감 유형별, 최종 이용 산업별, 시스템별, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

"필름 소재와 코팅 기술의 발전이 시장을 주도"

재료 과학 및 코팅 기술의 지속적인 혁신으로 페인트 보호 필름(PPF)의 성능 특성이 크게 향상되어 자동차 산업 전반에 걸쳐 채택이 확대되고 있습니다. 초기 보호 필름은 황변, 내구성 저하, 광학 투명도 저하 등의 문제를 안고 있는 경우가 많았습니다. 그러나 열가소성 폴리우레탄(TPU) 소재, 엘라스토머 코팅 및 접착제 배합의 발전으로 제조업체는 내구성, 투명성, 시공 용이성이 향상된 고성능 필름을 개발할 수 있게 되었습니다. 가장 주목할 만한 혁신 중 하나는 열을 가하면 미세한 스크래치나 스월마크가 자동으로 복구되는 자가복원 필름의 도입입니다. 이 기능은 보호된 표면의 내구성과 외관을 크게 향상시켜 장기적인 보호를 원하는 차량 소유자에게 PPF를 더욱 매력적인 솔루션으로 만듭니다. 또한, 자외선 저항성과 발수성이 향상되어 원래의 도장 마감을 유지하면서 세척 및 유지보수를 간소화할 수 있게 되었습니다.

또한, 각 제조사들은 복잡한 차량 표면에 밀착력을 높인 필름에 투자하고 있으며, 이를 통해 시공의 복잡성을 줄이고 미관도 개선하고 있습니다. 이러한 기술적 진보로 인해 기존 PPF 제품의 많은 문제점이 해결되었고, 이 기술에 대한 소비자의 신뢰도도 높아졌습니다. 각 제조사들이 조사개발에 지속적으로 투자함에 따라 제품의 성능은 더욱 향상될 것으로 예상되며, 이는 세계 시장의 지속적인 성장을 뒷받침할 것으로 보입니다.

폴리염화비닐(PVC) 유형은 예측 기간 동안 수량 기준으로 세계 페인트 보호 필름 시장에서 두 번째로 큰 규모를 차지할 것으로 추정됩니다.

폴리염화비닐(PVC)은 주로 가성비 및 접근성 때문에 판매량 기준으로 페인트 보호 필름 시장에서 두 번째로 큰 비중을 차지하고 있습니다. PVC 기반 필름은 경미한 스크래치, 마모 및 환경 노출에 대한 충분한 보호 기능을 제공하므로 저렴한 가격과 기본적인 표면 보호가 중요한 고려 사항인 응용 분야에 적합합니다. 이 필름은 엔트리 레벨 보호 솔루션이나 고급 자가 복구 기능과 같은 고급 기능이 필요하지 않은 용도에 주로 사용됩니다. 또한, PVC 필름은 뛰어난 유연성과 시공 용이성으로 인해 보다 광범위한 고객층을 위한 경제적인 보호 솔루션을 원하는 자동차 애프터마켓 서비스 제공업체에게 매력적인 선택이 될 수 있습니다. 프리미엄 부문에서는 열가소성 폴리우레탄이 주류를 이루고 있지만, PVC 기반 필름은 상대적으로 저렴한 비용과 충분한 기능적 성능으로 인해 특히 가격에 민감한 시장과 대량 애프터마켓 시공에서 강력한 수요를 유지하고 있습니다.

전기 및 전자 산업 부문은 도료 보호 필름 시장에서 수량 기준으로 용도별 산업별로는 두 번째 규모가 될 것으로 예상됩니다.

수량 기준으로 볼 때, 예측 기간 동안 전기 및 전자 산업은 페인트 보호 필름 시장에서 두 번째로 큰 최종 사용 산업이 될 것입니다. 페인트 보호 필름은 디스플레이, 제어판, 장치 외장 등 섬세한 전자 장비의 표면을 긁힘, 마모 및 환경 노출로부터 보호하기 위해 점점 더 널리 사용되고 있습니다. 스마트폰, 태블릿, 노트북, 웨어러블 기기 등 소비자 전자제품의 생산과 소비가 증가함에 따라 제품의 미관과 내구성을 유지하는 보호 솔루션에 대한 요구가 증가하고 있습니다. 이 필름은 기기의 기능성과 가시성을 손상시키지 않으면서도 높은 투명성, 스크래치 방지 및 표면 보호 기능을 제공합니다. 전자기기의 소형화 및 디자인 중시 추세에 따라 제조업체와 소비자는 제품의 수명을 연장하고 기기 표면의 품질을 유지하기 위해 보호 필름을 채택하는 경향이 증가하고 있으며, 이는 전자 분야에서의 페인트 보호 필름에 대한 안정적인 수요를 뒷받침하고 있습니다.

아시아태평양은 자동차 산업의 급속한 성장과 신흥 경제국의 자동차 보유량 증가에 힘입어 예측 기간 동안 페인트 보호 필름 시장에서 가장 높은 성장률을 보일 것으로 예상됩니다. 중국, 인도, 일본, 한국 등의 국가에서는 승용차 생산이 꾸준히 증가하고 있으며, 프리미엄 및 고급차의 존재감이 높아짐에 따라 고급 표면 보호 솔루션에 대한 수요가 가속화되고 있습니다. 또한, 차량 외관 및 유지보수에 대한 소비자의 인식이 높아지고, 자동차 애프터마켓 및 디테일링 산업의 급속한 확장은 이 지역 전체에서 페인트 보호 필름의 보급을 더욱 촉진하고 있습니다. 전문 시공 서비스 제공업체의 증가와 차량 커스터마이징의 인기 증가도 아시아태평양의 페인트 보호 필름 시장의 강력한 성장 모멘텀에 기여하고 있습니다.

본 보고서에 소개된 주요 기업으로는 3M(미국), XPEL, Inc(미국), Eastman Chemical Company(미국), Avery Dennison Corporation(미국), Saint-Gobain(프랑스), Lubrizol(미국), CCL Industries(캐나다), Hexis S.A.S.(캐나다), Hexis S.A.S.(프랑스), ORAFOL Europe GmbH(독일), Garware. Lubrizol(미국), CCL Industries(캐나다), Hexis S.A.S.(프랑스), ORAFOL Europe GmbH(독일), Garware Hi-Tech Films(인도) 및 기타 기업(15개사)이 포함됩니다.

조사 범위

이 보고서는 페인트 보호 필름 시장을 유형, 마감 유형, 시스템, 최종 사용 산업 및 지역별로 세분화하고 각 지역의 시장 규모로 추정치(단위 - 백만 달러/십억 달러)를 제공합니다. 이 보고서는 주요 업계 플레이어에 대한 상세한 분석을 통해 페인트 보호 필름 시장과 관련된 사업 개요, 서비스 및 주요 전략에 대한 인사이트를 제공합니다.

이 보고서를 구매해야 하는 이유

이 보고서는 산업 분석(업계 동향), 주요 기업의 시장 점유율 분석, 기업 프로파일 등 다각적인 분석에 중점을 두었으며, 이를 종합하여 페인트 보호 필름 시장의 경쟁 상황, 신흥 및 고성장 부문, 고성장 지역, 시장 촉진요인, 저해요인 및 기회를 종합적으로 분석했습니다. 제약 및 기회에 대한 전체적인 그림을 제공합니다.

본 보고서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 시장 침투도 : 세계 시장의 주요 기업이 제공하는 페인트 보호 필름에 대한 종합적인 정보

- 주요 촉진요인 분석 : 촉진요인(프리미엄 및 고급 차량에 대한 수요 증가, 자동차 애프터마켓의 커스터마이징 및 디테일링 산업의 성장, 필름 소재 및 코팅 기술의 발전, 차량 유지보수 및 자산 보호에 대한 소비자의 인식 증가), 제약요인(재료별 초기 비용 및 전문 시공에 대한 인식의 차이, 신흥국에서는 대체 도장 보호 솔루션의 존재) 요인(재료 및 전문 업체별 시공에 대한 높은 초기 비용, 신흥 시장에서의 낮은 인지도와 인식된 가치의 격차, 대체 페인트 보호 솔루션의 존재), 기회(전기자동차 보급 확대, 자동차 이외의 응용 분야에서의 채택 확대), 도전과제(제품 위조 위험 및 품질 품질 편차, 복잡한 공급망, 첨단 소재에 대한 의존도)

- 제품 개발 및 혁신 : 페인트 보호 필름 시장의 미래 기술, 연구 개발 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 지역별 페인트 보호 필름의 수익성 높은 신흥 시장에 대한 종합적인 정보

- 시장 다각화 : 세계 페인트 보호 필름 시장의 신제품, 미개척 지역 및 최근 동향에 대한 종합적인 정보를 제공합니다.

- 경쟁 분석 : 페인트 보호 필름 시장에서 주요 기업의 시장 점유율, 전략, 제품 및 제조 능력에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제8장 지속가능성과 규제 상황

제9장 페인트 보호 필름 시장(유형별)

제10장 페인트 보호 필름 시장(마감 유형별)

제11장 페인트 보호 필름 시장(최종 이용 산업별)

제12장 페인트 보호 필름 시장(시스템별)

제13장 페인트 보호 필름 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

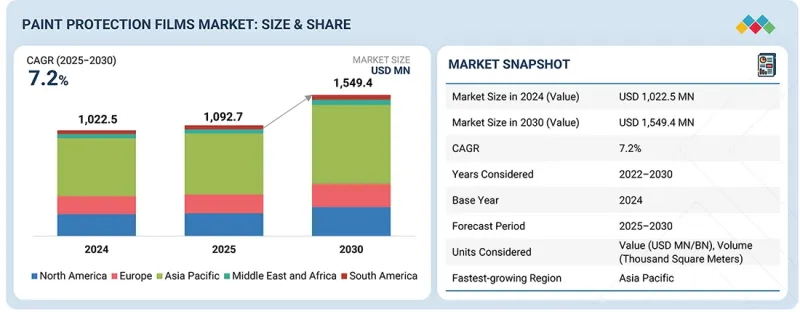

KSM 26.04.30The paint protection films market size was USD 1,092.7 million in 2025 and is projected to reach USD 1,549.4 million by 2030, at a CAGR of 7.2%, during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) and Volume (Thousand Square Meter) |

| Segments | Type, Finish Type, System, End-use Industry, and Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

"Technological advancements in film materials and coating technologies to drive the market"

Continuous innovation in material science and coating technologies has significantly improved the performance characteristics of paint protection films, thereby driving their broader adoption across the automotive sector. Early generations of protective films were often associated with issues such as yellowing, limited durability, and reduced optical clarity. However, advancements in thermoplastic polyurethane (TPU) materials, elastomeric coatings, and adhesive formulations have enabled manufacturers to develop high-performance films with enhanced durability, transparency, and ease of installation. One of the most notable innovations is the introduction of self-healing films that can automatically repair minor scratches and swirl marks when exposed to heat. This feature significantly enhances the longevity and visual appeal of protected surfaces, making PPF a more compelling solution for vehicle owners seeking long-term protection. Additionally, improvements in UV resistance and hydrophobic surface properties help maintain the original paint finish while simplifying cleaning and maintenance.

Manufacturers are also investing in films that provide better conformability to complex vehicle surfaces, reducing installation complexity and improving aesthetic outcomes. These technological developments have addressed many of the limitations associated with earlier PPF products and have strengthened consumer confidence in the technology. As manufacturers continue to invest in research and development, product performance is expected to improve further, supporting sustained growth in the global market.

The polyvinyl chloride type segment is estimated to be the second-largest type of the global paint protection films market, in terms of volume, during the forecast period.

Polyvinyl chloride (PVC) represents the second-largest type segment in the paint protection films market in terms of volume, primarily due to its cost-effectiveness and widespread availability. PVC-based films offer adequate protection against minor scratches, abrasions, and environmental exposure, making them suitable for applications where affordability and basic surface protection are key considerations. These films are commonly used in entry-level protective solutions and in applications where high-end features such as advanced self-healing are not essential. In addition, PVC films provide good flexibility and ease of installation, which makes them attractive for automotive aftermarket service providers seeking economical protective solutions for a broader consumer base. Although thermoplastic polyurethane dominates the premium segment, the relatively lower cost and functional performance of PVC-based films continue to support their strong demand, particularly in price-sensitive markets and high-volume aftermarket installations.

The electrical & electronics industry segment is projected to be the second-largest segment by end-use industry in the paint protection films market, in terms of volume.

In terms of volume, the electrical & electronics industry represents the second-largest end-use industry in the paint protection films market during the forecast period. Paint protection films are increasingly used to safeguard sensitive electronic surfaces such as displays, control panels, and device exteriors from scratches, abrasions, and environmental exposure. With the growing production and consumption of consumer electronics, including smartphones, tablets, laptops, and wearable devices, there is a rising need for protective solutions that maintain product aesthetics and durability. These films offer high transparency, scratch resistance, and surface protection without affecting device functionality or visual clarity. As electronic devices continue to become more compact and design-focused, manufacturers and consumers are increasingly adopting protective films to enhance product lifespan and maintain the quality of device surfaces, thereby supporting the steady demand for paint protection films in the electronics sector.

"Asia Pacific is the fastest-growing region of the global paint protection films market."

The Asia Pacific region is projected to grow at the fastest rate in the paint protection films market during the forecast period, driven by the rapid expansion of the automotive industry and increasing vehicle ownership across emerging economies. Countries such as China, India, Japan, and South Korea are witnessing strong growth in passenger vehicle production and a rising presence of premium and luxury vehicles, which is accelerating the demand for advanced surface protection solutions. In addition, growing consumer awareness regarding vehicle aesthetics and maintenance, along with the rapid expansion of the automotive aftermarket and detailing industry, is further supporting the adoption of paint protection films across the region. The increasing number of professional installation service providers and the rising popularity of vehicle customization are also contributing to the strong growth momentum of the paint protection films market in Asia Pacific.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 18%, and Rest of the World - 7%

The key players profiled in the report include 3M (US), XPEL, Inc (US), Eastman Chemical Company (US), Avery Dennison Corporation (US), Saint-Gobain (France), Lubrizol (US), CCL Industries (Canada), Hexis S.A.S. (France), ORAFOL Europe GmbH (Germany), Garware Hi-Tech Films (India), and other players (15).

Study Coverage

This report segments the market for paint protection films based on type, finish type, system, end-use industry, and region, and provides estimations of value (in USD Million/Billion) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies associated with the paint protection films market.

Reasons to Buy this Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the paint protection films market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights into the following points:

- Market Penetration: Comprehensive information on paint protection films offered by top players in the global market

- Analysis of key drivers: drivers (Rising demand for premium and luxury vehicles, growth of the automotive aftermarket customization and detailing industry, technological advancements in film materials and coating technologies, increasing consumer awareness of vehicle maintenance and asset protection), restraints (High initial cost of material and professional installation, limited awareness and perceived value gap in emerging markets, availability of alternative paint protection solutions), opportunities (Expansion of electric vehicle adoption, growing adoption in non-automotive applications), and challenges (risk of product counterfeiting and quality variability, complex supply chain, dependence on advance material inputs)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the paint protection films market

- Market Development: Comprehensive information about lucrative emerging markets for paint protection films across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global paint protection films market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the paint protection films market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.3.4.1 Currency/Value unit

- 1.3.4.2 Volume unit

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PAINT PROTECTION FILMS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PAINT PROTECTION FILMS MARKET

- 3.2 PAINT PROTECTION FILMS MARKET, BY TYPE

- 3.3 PAINT PROTECTION FILMS MARKET, BY SYSTEM

- 3.4 PAINT PROTECTION FILMS MARKET, BY FINISH TYPE

- 3.5 PAINT PROTECTION FILMS MARKET, BY END-USE INDUSTRY

- 3.6 PAINT PROTECTION FILMS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for premium and luxury vehicles

- 4.2.1.2 Growth of automotive aftermarket customization and detailing industry

- 4.2.1.3 Technological advancements in film materials and coating technologies

- 4.2.1.4 Increasing consumer awareness of vehicle maintenance and asset protection

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial cost of material and professional installation

- 4.2.2.2 Limited awareness and perceived value gap in emerging markets

- 4.2.2.3 Availability of alternative paint protection solutions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of electric vehicle (EV) adoption

- 4.2.3.2 Growing adoption in non-automotive applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Risk of product counterfeiting and quality variability

- 4.2.4.2 Complex supply chain and dependence on advanced material inputs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PAINT PROTECTION FILMS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GLOBAL GDP TRENDS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 391990)

- 5.6.2 EXPORT SCENARIO (HS CODE 391990)

- 5.7 KEY CONFERENCES AND EVENTS

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 EXPANDING AUTOMOTIVE SURFACE PROTECTION THROUGH ADVANCED PAINT PROTECTION FILM SOLUTIONS

- 5.10.2 ENHANCING VEHICLE PAINT DURABILITY USING SELF-HEALING PROTECTIVE FILM TECHNOLOGY

- 5.11 2025 US TARIFF

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON KEY REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.4 UNMET NEEDS IN VARIOUS APPLICATIONS

- 6.5 MARKET PROFITIBILITY

- 6.5.1 REVENUE POTENTIAL

- 6.5.2 COST DYNAMICS

- 6.5.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 EMBEDDED MICRO-SENSOR TECHNOLOGY IN SMART PAINT PROTECTION FILMS

- 7.1.2 AI-ENHANCED CUSTOM PAINT PROTECTION FILM APPLICATION

- 7.1.3 ECO-FRIENDLY AND SELF-REGENERATING PAINT PROTECTION FILMS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 AI-POWERED DETAILING TOOLS & SMART CAR CARE TECHNOLOGY

- 7.2.2 UV-PROTECTIVE NANOCOATING TECHNOLOGY FOR ENHANCED SURFACE DURABILITY

- 7.2.3 GRAPHENE-ENHANCED COATINGS FOR AUTOMOTIVE SURFACE PROTECTION

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 STEAM CLEANING & ECO-FRIENDLY WATERLESS DETAILING

- 7.3.2 LOTUS-EFFECT NANOCOATING TECHNOLOGY FOR SELF-CLEANING

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 7.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 7.4.3 LONG-TERM (2030-2035+) | SMART & SUSTAINABLE PROTECTION SYSTEMS

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS & COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 8.2.1.1 Carbon impact reduction and eco-material strategies

- 8.2.1.2 Eco applications

- 8.2.1 MATERIAL PERFORMANCE, ENVIRONMENT, AND SAFETY INITIATIVES

- 8.3 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 8.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 PAINT PROTECTION FILMS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 THERMOPLASTIC POLYURETHANE

- 9.2.1 HIGH FLEXIBILITY, SELF-HEALING PERFORMANCE, AND SUPERIOR IMPACT RESISTANCE

- 9.3 POLYVINYL CHLORIDE

- 9.3.1 COST-EFFECTIVE PROTECTION, HIGH DIMENSIONAL STABILITY, AND GOOD CHEMICAL-WEATHER RESISTANCE

- 9.4 POLYETHYLENE TEREPHTHALATE

- 9.4.1 HIGH SURFACE HARDNESS, EXCELLENT OPTICAL CLARITY, AND SUPERIOR DIMENSIONAL STABILITY

- 9.5 OTHER TYPES

10 PAINT PROTECTION FILMS MARKET, BY FINISH TYPE

- 10.1 INTRODUCTION

- 10.2 GLOSS

- 10.2.1 SUPERIOR AESTHETIC APPEAL AND HIGH CONSUMER PREFERENCE

- 10.3 MATTE

- 10.3.1 RISE IN DEMAND FOR VEHICLE CUSTOMIZATION

- 10.4 SATIN

- 10.4.1 BALANCED AESTHETIC APPEAL AND NICHE CUSTOMIZATION

11 PAINT PROTECTION FILMS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 AUTOMOTIVE & TRANSPORTATION

- 11.2.1 PRIMARY APPLICATION AREA DRIVEN BY AESTHETIC PRESERVATION, DURABILITY, AND GROWING OEM ADOPTION

- 11.3 ELECTRICAL & ELECTRONICS

- 11.3.1 GROWING APPLICATIONS IN DISPLAYS, INTERIOR INTERFACES, AND HIGH-WEAR ELECTRONIC COMPONENT SURFACES

- 11.4 CONSTRUCTION

- 11.4.1 SURFACE PRESERVATION FOR ARCHITECTURAL GLASS, METAL PANELS, INTERIORS, AND HIGH-VALUE BUILDING MATERIALS

- 11.5 AEROSPACE & DEFENSE

- 11.5.1 HIGH-PERFORMANCE SURFACE PROTECTION FOR AIRCRAFT COMPONENTS, AVIONICS, AND DEFENSE EQUIPMENT

- 11.6 OTHER END-USE INDUSTRIES

12 PAINT PROTECTION FILMS MARKET, BY SYSTEM

- 12.1 INTRODUCTION

- 12.2 WATER-BASED SYSTEMS

- 12.2.1 INCREASING ADOPTION DRIVEN BY STRINGENT ENVIRONMENTAL REGULATIONS AND LOW-VOC REQUIREMENTS

- 12.3 SOLVENT-BASED SYSTEMS

- 12.3.1 PREFERRED FOR HIGH-PERFORMANCE DURABILITY AND STRONG ADHESION IN DEMANDING APPLICATIONS

13 PAINT PROTECTION FILMS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Strong automotive aftermarket and high-premium vehicle ownership

- 13.2.2 CANADA

- 13.2.2.1 Growing automotive ownership and rising premium vehicle protection demand

- 13.2.3 MEXICO

- 13.2.3.1 Expanding industrial manufacturing and surface protection demand

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Strong industrial base and premium mobility culture

- 13.3.2 UK

- 13.3.2.1 Expanding aerospace, construction, and premium vehicle services

- 13.3.3 FRANCE

- 13.3.3.1 Growing aerospace, luxury mobility, and construction activities

- 13.3.4 ITALY

- 13.3.4.1 Rising premium mobility, manufacturing activities, and surface protection awareness

- 13.3.5 SPAIN

- 13.3.5.1 Expanding construction activity and industrial manufacturing

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Massive manufacturing base and expanding electronics & construction sectors

- 13.4.2 JAPAN

- 13.4.2.1 Advanced electronics manufacturing and high-value mobility industry

- 13.4.3 INDIA

- 13.4.3.1 Rapid infrastructure expansion and strong automotive & electronics manufacturing

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Strong electronics manufacturing and advanced mobility industry

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.2 SAUDI ARABIA

- 13.5.2.1 Large-scale infrastructure projects and Vision 2030 investments

- 13.5.3 UAE

- 13.5.3.1 Luxury automotive culture and premium infrastructure development

- 13.5.4 REST OF GCC COUNTRIES

- 13.5.5 SOUTH AFRICA

- 13.5.5.1 Expanding infrastructure development and automotive manufacturing

- 13.5.6 REST OF MIDDLE EAST & AFRICA

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Growing economic strength and expanding electrical & electronics sector

- 13.6.2 ARGENTINA

- 13.6.2.1 Stringent environmental regulations to drive market

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.4.1 XPEL

- 14.4.2 3M

- 14.4.3 EASTMAN CHEMICAL

- 14.4.4 AVERY DENNISON

- 14.4.5 SAINT-GOBAIN

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Finish type footprint

- 14.7.5.5 System footprint

- 14.7.5.6 End-use industry footprint

- 14.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2024

- 14.8.5.1 List of start-ups/SMEs

- 14.8.5.2 Competitive benchmarking of start-ups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 DEALS

- 14.9.2 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 3M

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 XPEL, INC

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Expansions

- 15.1.2.3.3 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 EASTMAN CHEMICAL COMPANY

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Expansions

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 AVERY DENNISON CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 SAINT-GOBAIN

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 LUBRIZOL

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Expansions

- 15.1.6.4 MnM view

- 15.1.7 CCL INDUSTRIES

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.4 MnM view

- 15.1.8 HEXIS S.A.S.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.4 MnM view

- 15.1.9 ORAFOL EUROPE GMBH

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Expansions

- 15.1.9.3.3 Deals

- 15.1.9.4 MnM view

- 15.1.10 GARWARE HI-TECH FILMS

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Expansions

- 15.1.10.4 MnM view

- 15.1.1 3M

- 15.2 OTHER PLAYERS

- 15.2.1 SWM

- 15.2.2 RENOLIT SE

- 15.2.3 THE OFFICIAL KDX WINDOW FILM SITE

- 15.2.4 STEK-USA

- 15.2.5 UPPF

- 15.2.6 CERAMIC PRO

- 15.2.7 BLUEGRASS PROTECTIVE FILMS LLC

- 15.2.8 KPMF

- 15.2.9 REFLEK TECHNOLOGIES: CORPORATION

- 15.2.10 BORITA GROUP OF COMPANIES

- 15.2.11 WRAPSTYLE

- 15.2.12 TOPAZ DETAILING

- 15.2.13 MANMACHINE GROUP

- 15.2.14 CLEARPRO

- 15.2.15 GRAFITYP

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS