|

시장보고서

상품코드

2038695

폴리염화비닐 수지 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Polyvinyl Chloride Resin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

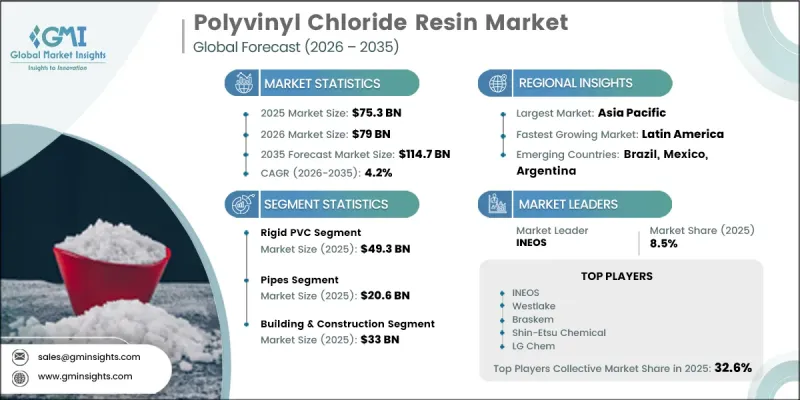

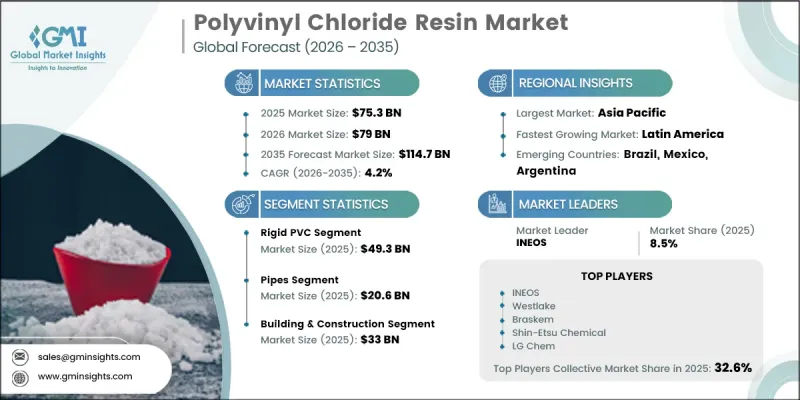

세계의 폴리염화비닐(PVC) 수지 시장은 2025년에 753억 달러로 평가되었고 CAGR 4.2%로 성장하여 2035년에는 1,147억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 건설, 인프라, 포장, 자동차, 전기 산업의 견고하고 지속적인 수요에 의해 주도되고 있습니다. 이러한 산업에서 PVC 수지는 내구성과 비용 효율성으로 인해 널리 사용되고 있습니다. 경질 및 연질 응용 분야에서 이 소재의 다재다능함은 전 세계적으로 그 보급을 더욱 촉진하고 있습니다. 인프라 개발 및 도시 확장의 진전은 특히 건축자재 및 공공 설비 시스템에서 PVC 계열 제품의 소비 확대를 뒷받침하고 있습니다. 산업 활동의 활성화와 더불어 가볍고 부식에 강하며 수명이 긴 소재에 대한 수요가 증가하고 있는 것도 시장 성장을 더욱 촉진하고 있습니다. 압출, 성형, 캘린더링 등 중합 기술과 가공 방법을 지속적으로 개선하여 생산 효율과 제품 맞춤화 능력을 향상시키고 있습니다. PVC 수지는 습기, 화학물질 및 환경적 마모에 대한 내성을 가지고 있어 실내 및 실외 모두에 적합하며, 긴 수명을 제공합니다. 재료 효율성과 재활용 가능성에 대한 관심이 높아지면서 생산 전략에도 영향을 미치고 있으며, 제조업체들은 지속 가능한 배합과 수명주기 성능 향상에 초점을 맞추었습니다. 전반적으로 PVC 수지는 기능적 적응성과 우수한 기계적 특성으로 인해 현대 산업 및 건설 생태계에서 여전히 중요한 재료로 남아 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 753억 달러 |

| 예측 규모 | 1,147억 달러 |

| CAGR | 4.2% |

2025년에는 경질 PVC가 493억 달러로 가장 큰 시장 규모를 차지했습니다. 경질 PVC 수요는 주로 대규모 건설 및 인프라 개발 활동에 의해 주도되고 있으며, 강도, 안정성 및 내식성으로 인해 이러한 용도에 매우 적합합니다. 이 소재는 내구성과 낮은 유지보수성이 요구되는 용도에 널리 선호되고 있으며, 구조물 및 공공시설 설치에 널리 활용되고 있습니다.

건축 및 건설 부문은 2025년 330억 달러에 달했습니다. PVC 수지는 내후성, 내식성 및 장기적인 구조적 신뢰성이 요구되는 용도에 적합하기 때문에 이 분야에서 널리 사용되고 있습니다. 건설 관련 부품의 지속적인 사용은 전 세계 인프라 개발 프로젝트 전반에 걸쳐 안정적인 수요를 유지하고 있습니다.

북미 폴리염화비닐(PVC) 수지 시장은 2025년 141억 달러에서 2035년 220억 달러로 성장할 것으로 예측됩니다. 이 지역의 성장은 인프라 갱신 활동, 리노베이션 프로젝트, 건설 및 전기 분야의 안정적인 수요에 의해 주도되고 있습니다. 재활용에 대한 노력과 규제 준수에 대한 관심이 높아지는 것도 시장 역학을 형성하고 있습니다. 미국에서는 여러 지역의 지속적인 주택 개발 및 산업 생산의 안정화를 배경으로 주택 건설, 유틸리티 설비 교체, 배관 시스템, 전선 피복 용도로 견조한 수요가 예상됩니다.

INEOS, Braskem, 신에츠화학공업, Westlake, LG Chem, Mitsubishi Chemical, Nexeo Plastics, LLC, SCG Chemicals, Solvay, SNG Microns, Chemplast Sanmar는 폴리염화비닐(PVC) 수지 시장에서 사업을 사업을 전개하는 주요 기업 중 일부입니다. 폴리염화비닐(PVC) 수지 시장의 업체들은 경쟁력 강화를 위해 생산능력 확대, 제품 혁신, 그리고 지속가능성 중심의 생산 전략에 집중하고 있습니다. 제조업체들은 효율성, 균일성 및 비용 효율성을 향상시키기 위해 첨단 중합 기술에 투자하고 있습니다. 또한, 환경 규제 및 지속가능성 목표에 대응하기 위해 재활용이 가능하고 친환경적인 PVC 배합 개발에도 중점을 두고 있습니다. 건설 산업 및 산업 분야의 최종 사용자와의 전략적 제휴 및 장기 공급 계약은 각 사가 안정적인 수요를 확보하는 데 도움이 되고 있습니다. 또한, 기업들은 공급망 효율화를 위해 전 세계 유통망 확대와 지역별 제조 거점 강화에 나서고 있습니다. 경질 및 연질 PVC의 고성능 등급에 대한 지속적인 연구로 용도의 다양성이 향상되고, 생산의 디지털화 및 공정 최적화로 인해 운영 성능과 시장 경쟁력이 더욱 향상되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.05.29The Global Polyvinyl Chloride (PVC) Resin Market was valued at USD 75.3 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 114.7 billion in 2035.

Market expansion is driven by strong and sustained demand across construction, infrastructure, packaging, automotive, and electrical industries, where PVC resin is widely used due to its durability and cost efficiency. The material's versatility across rigid and flexible applications continues to reinforce its global adoption. Increasing infrastructure development and urban expansion are supporting higher consumption of PVC-based products, particularly in building materials and utility systems. Rising industrial activity, coupled with demand for lightweight, corrosion-resistant, and long-lasting materials, is further strengthening market growth. Continuous improvements in polymerization techniques and processing methods, such as extrusion, molding, and calendering, are enhancing production efficiency and product customization capabilities. PVC resin's resistance to moisture, chemicals, and environmental wear makes it suitable for both indoor and outdoor applications, supporting long service life. The growing emphasis on material efficiency and recyclability is also influencing production strategies, as manufacturers focus on sustainable formulations and improved lifecycle performance. Overall, PVC resin remains a critical material in modern industrial and construction ecosystems due to its functional adaptability and strong mechanical properties.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $75.3 Billion |

| Forecast Value | $114.7 Billion |

| CAGR | 4.2% |

Rigid PVC accounted for the largest market value of USD 49.3 billion in 2025. Demand for rigid PVC is primarily driven by large-scale construction and infrastructure development activities, where its strength, stability, and resistance to corrosion make it highly suitable. The material is widely preferred in applications requiring durability and low maintenance, supporting its extensive use in structural and utility-based installations.

The building and construction segment reached USD 33 billion in 2025. PVC resin is extensively utilized in this sector due to its suitability for applications that require resistance to weather conditions, corrosion protection, and long-term structural reliability. Its consistent use in construction-related components continues to support steady demand across global infrastructure development projects.

North America Polyvinyl Chloride (PVC) Resin Market is projected to grow from USD 14.1 billion in 2025 to USD 22 billion in 2035. Growth in the region is influenced by infrastructure renewal activities, renovation projects, and stable demand from the construction and electrical sectors. Increased focus on recycling initiatives and regulatory compliance is also shaping market dynamics. In the United States, strong demand is supported by residential construction, utility upgrades, piping systems, and wire insulation applications, driven by ongoing housing development and industrial manufacturing stability across multiple regions.

INEOS, Braskem, Shin-Etsu Chemical, Westlake, LG Chem, Mitsubishi Chemical Corporation, Nexeo Plastics, LLC., SCG Chemicals, Solvay, SNG Microns, and Chemplast Sanmar are among the key companies operating in the polyvinyl chloride (PVC) resin market. Companies in the Polyvinyl Chloride (PVC) Resin Market are focusing on capacity expansion, product innovation, and sustainability-driven production strategies to strengthen their competitive position. Manufacturers are investing in advanced polymerization technologies to improve efficiency, consistency, and cost-effectiveness. There is also a strong emphasis on developing recyclable and eco-friendly PVC formulations in response to environmental regulations and sustainability goals. Strategic collaborations and long-term supply agreements with construction and industrial end users are helping companies secure stable demand. In addition, firms are expanding their global distribution networks and strengthening regional manufacturing bases to improve supply chain efficiency. Continuous research into high-performance grades of rigid and flexible PVC is enabling better application versatility, while digitalization in production and process optimization is further enhancing operational performance and market competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding infrastructure and construction activities

- 3.2.1.2 Cost-effective material for diverse applications

- 3.2.1.3 Demand for durable electrical insulation materials

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Environmental concerns related to PVC disposal

- 3.2.2.2 Regulatory pressure on plastic material usage

- 3.2.3 Opportunities

- 3.2.3.1 Development of sustainable PVC formulations

- 3.2.3.2 Growth in medical and healthcare applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Rigid PVC

- 5.3 Flexible PVC

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dashboards

- 6.3 Consumer electronics

- 6.4 Sealants

- 6.5 Electric wires

- 6.6 Flooring

- 6.7 Pipes

- 6.8 Cable insulation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Building & construction

- 7.4 Electrical & electronics

- 7.5 Medical & pharmaceuticals

- 7.6 Consumer goods

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Braskem

- 9.2 Nexeo Plastics, LLC.

- 9.3 Chemplast Sanmar

- 9.4 INEOS

- 9.5 LG Chem

- 9.6 Mitsubishi Chemical Corporation

- 9.7 Shin-Etsu Chemical

- 9.8 Solvay

- 9.9 SCG Chemicals

- 9.10 SNG Microns

- 9.11 Westlake