|

시장보고서

상품코드

2038706

소형 상용차 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Light Commercial Vehicle (LCV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

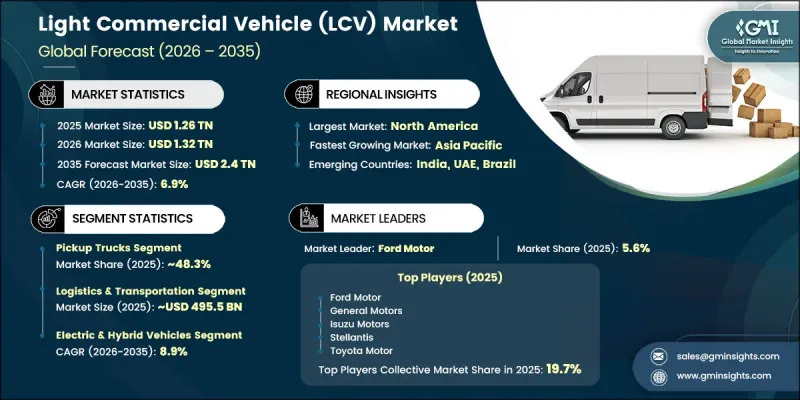

세계의 소형 상용차(LCV) 시장은 2025년에 1조 2,600억 달러로 평가되었고, CAGR 6.9%로 성장할 전망이며, 2035년까지 2조 4,000억 달러에 이를 것으로 추정되고 있습니다.

시장의 성장은 효율적이고 유연한 운송 솔루션이 필수적인 여러 최종 사용 부문에서 견조한 수요에 의해 주도되고 있습니다. 소형 상용차는 화물 운송, 여객 운송, 농업 작업, 지방 교통망, 지방 자치 단체 서비스 등 다양한 분야에서 활용도가 높아 중형 및 대형 차량 카테고리를 능가하는 실적을 유지하고 있습니다. 컴팩트한 구조로 도시 물류, 특히 라스트마일 배송 업무에서 매우 높은 효과를 발휘합니다. 동시에, 규제 당국과 이해관계자들이 저배출 교통수단을 점점 더 많이 추진하고 있는 가운데, 더 깨끗한 모빌리티 솔루션으로의 전환은 업계의 판도를 바꾸고 있습니다. 이러한 전환은 배출 기준의 강화와 지속가능성 목표에 힘입어 소형 상용차 도입이 가속화되고 있습니다. 또한, 전자상거래의 성장과 배송 네트워크의 급속한 확장은 효율적인 소형 차량에 의한 물류 솔루션에 대한 수요를 촉진하고 있습니다. 시장에서는 혼잡한 도시 환경에 맞게 설계된 소형 전기자동차의 설계에 대한 지속적인 혁신이 이루어지고 있으며, 인구 밀집 지역에서의 배송 효율성과 운영 실용성이 향상되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 1조 2,600억 달러 |

| 예측 시장 규모 | 2조 4,000억 달러 |

| CAGR | 6.9% |

2025년 픽업 트럭 부문은 48.3%의 점유율을 차지했으며 6,074억 달러 시장 규모를 창출했습니다. 이 부문은 승용차 및 화물 운송에 모두 적응할 수 있기 때문에 계속해서 선도적인 위치를 유지하고 있습니다. 다기능 설계로 개인 이동 수단뿐만 아니라 상업적 용도로도 적합하며, 건설, 농업 및 소규모 사업 운영 수요를 뒷받침합니다. 높은 실용성과 운영의 유연성은 시장에서 선도적 지위를 유지하는 중요한 요소로 작용하고 있습니다.

물류 및 운송 부문은 2025년 39.4%의 점유율을 차지했으며, 시장 규모는 4,955억 달러에 달했습니다. 이 부문 수요는 주로 도시 지역의 배송 시스템 확대와 도시 간 화물 운송 증가에 의해 주도되고 있습니다. 소형 상용차는 라스트 마일 배송 및 지역 간 화물 운송을 지원하는 중심적인 역할을 하고 있으며, 물류는 시장에서 가장 큰 용도 분야 중 하나입니다.

미국 소형 상용차(LCV) 시장은 2025년 6,103억 달러에 달했으며, 2026-2035년 연평균 6%의 성장률을 보일 것으로 전망됩니다. 견조한 경제 활동, 상업용 운송에 대한 높은 의존도, 개인 및 상업용 목적으로 픽업 트럭이 널리 사용되고 있다는 점이 주요 성장 요인으로 작용하고 있습니다. 이 나라의 광활한 국토는 산업을 막론하고 효율적인 운송 솔루션에 대한 지속적인 수요를 더욱 부추기고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 차량별(2022-2035년)

제6장 시장 추산 및 예측 : 추진력별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 총중량별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Light Commercial Vehicle (LCV) Market was valued at USD 1.26 trillion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 2.4 trillion by 2035.

Market growth is driven by strong demand across multiple end-use sectors where efficient and flexible transportation solutions are essential. Light commercial vehicles continue to outperform medium and heavy-duty categories due to their versatility in goods movement, passenger applications, agricultural operations, rural connectivity, and municipal services. Their compact structure makes them highly effective for urban logistics, particularly in last-mile delivery operations. At the same time, the global shift toward cleaner mobility solutions is reshaping the industry, as regulatory bodies and industry stakeholders increasingly promote low-emission transportation. This transition is accelerating the adoption of electric light commercial vehicles, supported by tightening emission standards and sustainability targets. Growth in e-commerce and rapid expansion of delivery networks are also reinforcing demand for efficient small-vehicle logistics solutions. The market is witnessing ongoing innovation in compact electric vehicle designs tailored for congested urban environments, improving delivery efficiency and operational practicality in high-density regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.26 Trillion |

| Forecast Value | $2.4 Trillion |

| CAGR | 6.9% |

The pickup trucks segment held a share of 48.3% in 2025, generating USD 607.4 billion. This segment continues to lead due to its adaptability for both passenger use and cargo transport. Its multifunctional design makes it suitable for personal mobility as well as commercial applications, supporting demand across construction, agriculture, and small business operations. Strong utility and operational flexibility remain key factors sustaining its market leadership.

The logistics and transportation segment accounted for 39.4% share in 2025, valued at USD 495.5 billion. Demand in this segment is primarily driven by the expansion of urban distribution systems and intercity freight movement. Light commercial vehicles play a central role in supporting last-mile delivery and regional cargo transport, making logistics one of the largest application areas within the market.

U.S. Light Commercial Vehicle (LCV) Market reached USD 610.3 billion in 2025 and is projected to grow at a CAGR of 6% between 2026 and 2035. Strong economic activity, high reliance on commercial transportation, and widespread use of pickup trucks for dual personal and business purposes are key growth drivers. The large geographic scale of the country further supports sustained demand for efficient transport solutions across industries.

Key companies operating in the Global Light Commercial Vehicle (LCV) Market include Ford Motor, Toyota Motor, General Motors, Stellantis, Volkswagen, Daimler, Hyundai Motor, Isuzu Motors, Mitsubishi, and Volvo. Companies in the Light Commercial Vehicle (LCV) Market are focusing on electrification and product innovation to strengthen their competitive position. Manufacturers are investing heavily in the development of electric and hybrid models to meet evolving emission regulations and sustainability goals. Strategic partnerships with technology providers are enabling advancements in battery systems, connectivity features, and vehicle efficiency. Expansion of production capabilities and localization of supply chains are helping companies reduce costs and improve delivery timelines. Firms are also enhancing their product portfolios to cater to diverse commercial applications, including logistics, construction, and urban mobility. In addition, flexible financing solutions and fleet management services are being introduced to attract business customers, while digital sales channels are improving customer engagement and market reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Gross Weight

- 2.2.5 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce and rising demand for efficient last-mile delivery services

- 3.2.1.2 Rapid urbanization coupled with ongoing infrastructure development

- 3.2.1.3 Total cost of ownership advantages offered by electric light commercial vehicles

- 3.2.1.4 Government Mandates for Emissions Reduction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Range limitations, payload constraints, and operational concerns

- 3.2.2.2 Insufficient charging infrastructure, especially in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption in emerging markets and accelerated fleet electrification

- 3.2.3.2 Battery-as-a-Service models reducing upfront investment barriers

- 3.2.3.3 Development and deployment of autonomous delivery vehicles

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 Anti-lock Braking System (ABS)

- 3.3.1.2 Telematics and fleet management system integration

- 3.3.1.3 Automated Manual Transmission (AMT)

- 3.3.2 Emerging technologies

- 3.3.2.1 Electric Vehicle (EV) drivetrains

- 3.3.2.2 Advanced Driver Assistance Systems (ADAS)

- 3.3.2.3 Vehicle-to-Everything (V2X) communication

- 3.3.2.4 Hydrogen fuel cell technology

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - National Highway Traffic Safety Administration

- 3.6.1.2 Canada - Transport Canada

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission

- 3.6.2.2 UK - Department for Transport (DfT)

- 3.6.3 Asia Pacific

- 3.6.3.1 India - Ministry of Road Transport and Highways

- 3.6.3.2 China - Ministry of Industry and Information Technology (MIIT)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - National Traffic Department (DENATRAN / SENATRAN)

- 3.6.4.2 Argentina - National Road Safety Agency (ANSV)

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Arabia - Saudi Standards Metrology and Quality Organization

- 3.6.5.2 UAE - Federal Authority for Land and Maritime Transport

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Cost breakdown analysis

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Cost breakdown analysis

- 3.14 Powertrain transition & electrification

- 3.14.1 ICE to Electric Transition Timelines by Region

- 3.14.2 Hybrid as Bridging Technology

- 3.14.3 Hydrogen Fuel Cell Development Roadmap

- 3.14.4 Infrastructure Readiness & Charging Networks

- 3.14.5 OEM Electrification Strategies

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($Bn, Thousand Units)

- 5.1 Key trends

- 5.2 Pickup trucks

- 5.3 Vans & minibuses

- 5.4 Light-duty trucks

Chapter 6 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($Bn, Thousand Units)

- 6.1 Key trends

- 6.2 Internal Combustion Engine (ICE)

- 6.3 Electric & hybrid vehicles

- 6.3.1 Battery Electric Vehicle (BEV)

- 6.3.2 Fuel Cell Electric Vehicles (FCEV)

- 6.3.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 6.3.4 Hybrid Electric Vehicle (HEV)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($Bn, Thousand Units)

- 7.1 Key trends

- 7.2 Logistics & transportation

- 7.2.1 E-commerce last-mile delivery

- 7.3 Construction & mining

- 7.4 Utility services

- 7.5 Rental & leasing

- 7.6 Passenger transport

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By Gross Weight, 2022 - 2035 ($Bn, Thousand Units)

- 8.1 Key trends

- 8.2 6000 - 9000 lbs.

- 8.3 9000 - 12000 lbs.

- 8.4 12000 - 14000 lbs.

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Switzerland

- 9.3.9 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Indonesia

- 9.4.8 Vietnam

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Ford Motor

- 10.1.2 General Motors

- 10.1.3 Volkswagen

- 10.1.4 Daimler

- 10.1.5 Stellantis

- 10.1.6 Toyota Motor

- 10.1.7 Isuzu Motors

- 10.1.8 Volvo

- 10.1.9 Nissan Motor

- 10.1.10 Hyundai Motor

- 10.1.11 Mitsubishi

- 10.2 Regional players

- 10.2.1 Tata Motors

- 10.2.2 Mahindra & Mahindra

- 10.2.3 Ashok Leyland

- 10.2.4 Dongfeng Motor

- 10.2.5 VE Commercial Vehicles

- 10.2.6 Euler Motors

- 10.3 Emerging players

- 10.3.1 SAIC Motor

- 10.3.2 Fujian New Longma Automobile

- 10.3.3 Hubei Qixing