|

시장보고서

상품코드

2038745

항공기 페어링 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Fairings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

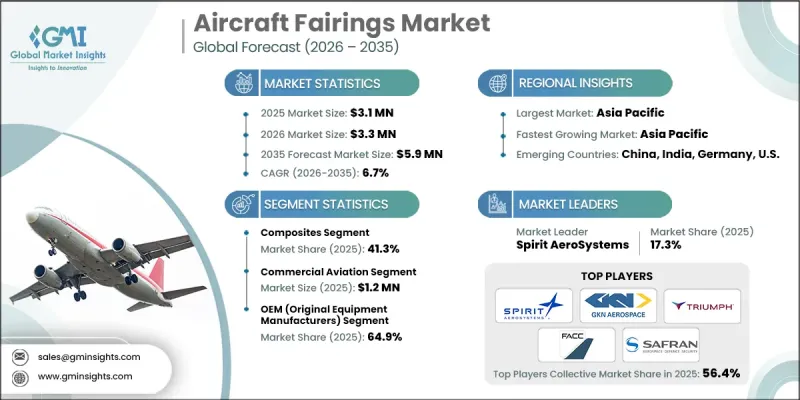

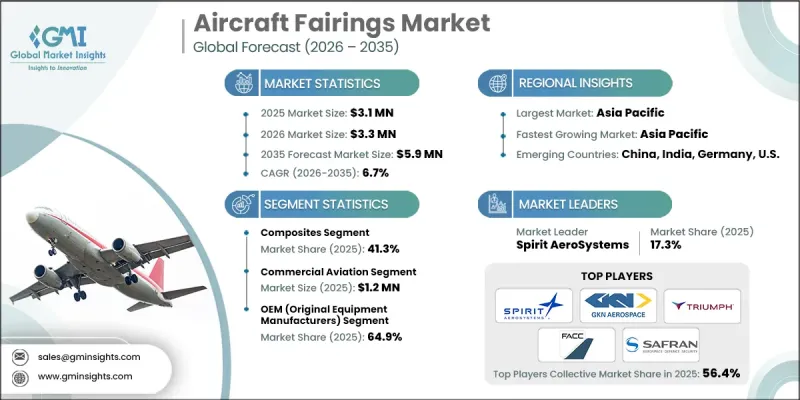

세계의 항공기 페어링 시장은 2025년에 310만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.7%로 성장할 전망이며, 590만 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 민간 항공기 생산 증가, 공기역학적 효율성에 대한 관심 증가, 전체 항공기의 연료 효율 최적화에 대한 수요 증가로 인해 주도되고 있습니다. 제조업체들이 경량화와 성능 향상을 우선시함에 따라 경량 복합재 구조의 채택이 가속화되고 있습니다. 또한, 유지보수, 수리, 정비(MRO) 활동의 확대는 항공기 페어링에 대한 견고한 애프터마켓 수요를 뒷받침하고 있습니다. 국방 항공 분야의 현대화 프로그램도 첨단 외부 구조 부품의 지속적인 조달에 기여하고 있습니다. 항공사와 항공기 OEM 업체들은 연비와 운영 효율성 향상에 점점 더 집중하고 있으며, 이는 첨단 페어링 설계의 추가 통합을 촉진하고 있습니다. 지속적인 기체 수 확대와 높은 항공기 가동률은 애프터마켓의 교체 주기를 촉진하고 있습니다. 재료 공학 및 구조 설계의 기술 발전으로 내구성과 공기역학적 성능을 향상시킬 수 있게 되었습니다. 모듈식 및 플랫폼 기반 페어링 설계 접근 방식으로의 전환은 제조 전략을 더욱 재구성하고, 생산 효율성을 개선하며, 민간 및 군용 항공 분야 모두에서 장기적인 시장 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 310만 달러 |

| 예측 시장 규모 | 590만 달러 |

| CAGR | 6.7% |

2025년 복합 재료 부문은 41.3%의 점유율을 차지했습니다. 이러한 우위는 민간 항공기와 방산 항공기 모두에서 탄소섬유 및 강화 복합재료가 널리 사용되고 있기 때문입니다. 이 소재들은 강도 대 중량비, 내식성, 복잡한 공기역학적 구조물을 지지하는 능력으로 인해 OEM 생산 및 애프터마켓 응용 분야에서 지속적인 수요를 확보하고 있습니다.

2025년 민간 항공기 부문은 120만 달러를 차지했습니다. 견조한 항공기 생산량과 동체, 날개, 엔진 어셈블리 전체에 페어링을 광범위하게 적용하는 것이 이 부문을 뒷받침하는 주요 요인입니다. 현재 진행 중인 기체 보강 및 업데이트 프로그램으로 인해 민간 항공기 제조 및 정비 업무에서 페어링에 대한 수요는 안정적으로 유지되고 있습니다.

2025년 북미의 항공기 페어링 시장은 31.4%의 점유율을 차지했습니다. 이 지역의 성장은 주요 항공기 OEM 제조업체와 1등급 항공기 구조 부품 공급업체의 강력한 입지와 상업용 및 방위산업용 항공기로 구성된 대규모 운영 항공기 군단에 의해 뒷받침되고 있습니다. 활발한 생산 활동과 첨단 복합소재 및 공기역학 기술의 조기 도입이 전체 신규 항공기 프로그램 수요를 지속적으로 견인하고 있습니다. 또한, 이 지역은 이미 구축된 MRO 생태계와 안정적인 방위비 지출의 혜택을 누리고 있으며, 이는 항공기 페어링의 갱신 및 업그레이드 요구 사항을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 플랫폼별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Aircraft Fairings Market was valued at USD 3.1 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 5.9 million by 2035.

Market expansion is driven by rising commercial aircraft production, increasing emphasis on aerodynamic efficiency, and growing demand for fuel optimization across aviation fleets. The adoption of lightweight composite structures is accelerating as manufacturers prioritize weight reduction and performance enhancement. In addition, expanding maintenance, repair, and overhaul activities are supporting steady aftermarket demand for aircraft fairings. Defense aviation modernization programs are also contributing to sustained procurement of advanced external structural components. Airlines and aircraft OEMs are increasingly focused on improving fuel economy and operational efficiency, which is encouraging greater integration of advanced fairing designs. Continuous fleet expansion and high aircraft utilization rates are reinforcing aftermarket replacement cycles. Technological progress in materials engineering and structural design is enabling improved durability and aerodynamic performance. The shift toward modular and platform-based fairing design approaches is further reshaping manufacturing strategies, improving production efficiency, and supporting long-term market growth across both commercial and military aviation sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Million |

| Forecast Value | $5.9 Million |

| CAGR | 6.7% |

The composites segment held a 41.3% share in 2025. This dominance is driven by widespread use of carbon fiber and reinforced composite materials in both commercial and defense aircraft. These materials are highly valued for their strength-to-weight efficiency, corrosion resistance, and capability to support complex aerodynamic structures, ensuring continued demand across OEM production and aftermarket applications.

The commercial aviation segment accounted for USD 1.2 million in 2025. Strong aircraft production volumes and extensive integration of fairings across fuselage, wing, and engine assemblies are key factors supporting this segment. Ongoing fleet expansion and replacement programs are sustaining consistent demand for fairings in commercial aircraft manufacturing and maintenance operations.

North America Aircraft Fairings Market held a 31.4% share in 2025. The region's growth is supported by the strong presence of leading aircraft OEMs, tier-1 aerostructure suppliers, and a large operational fleet of commercial and defense aircraft. High production activity and early adoption of advanced composite and aerodynamic technologies continue to drive demand across new aircraft programs. The region also benefits from a well-established MRO ecosystem and consistent defense spending, which further support replacement and upgrade requirements for aircraft fairings.

Key companies operating in the Global Aircraft Fairings Market include Spirit AeroSystems, GKN Aerospace, Triumph Group, Safran, FACC AG, Leonardo S.p.A., Aernnova Aerospace, Kaman Corporation, Senior plc, Stelia Aerospace, MTorres, Meggitt, Nordam Group, ShinMaywa Industries, and AVIC. Companies in the Aircraft Fairings Market are strengthening their position through continuous investment in advanced composite materials and lightweight structural technologies. Manufacturers are focusing on improving aerodynamic efficiency and reducing aircraft weight to meet evolving fuel efficiency targets. Strategic partnerships with aircraft OEMs and defense contractors are enabling long-term supply agreements and program integration. Firms are also expanding their aftermarket service capabilities to capture maintenance-driven demand. Increased investment in digital design tools, simulation technologies, and automated manufacturing processes is enhancing production accuracy and reducing lead times. Additionally, companies are developing modular and platform-based fairing solutions to improve scalability and cost efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Platform trends

- 2.2.3 Application rends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising production of commercial aircraft

- 3.2.1.2 Growing focus on fuel efficiency and drag reduction

- 3.2.1.3 Increased use of advanced composite materials

- 3.2.1.4 Expansion of the aircraft MRO and aftermarket segment

- 3.2.1.5 Rising defense aircraft modernization and fleet upgrades

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High design complexity and certification requirements

- 3.2.2.2 Exposure to aircraft production delays and program disruptions

- 3.2.3 Market opportunities

- 3.2.3.1 Rising development of advanced air mobility and electric vertical take-off and landing (eVTOL) aircraft platforms

- 3.2.3.2 Adoption of additive manufacturing and rapid tooling for fairing production

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Composites

- 5.3 Metals

- 5.4 Hybrids

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets

- 6.3 Military Aviation

- 6.3.1 Fighter aircraft

- 6.3.2 Transport aircraft

- 6.3.3 Military UAVs

- 6.4 General aviation

- 6.5 Helicopters (rotary-wing)

- 6.5.1 Civil helicopters

- 6.5.2 Military helicopters

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fuselage fairings

- 7.3 Wing fairings

- 7.4 Landing gear fairings

- 7.5 Propulsion fairings

- 7.6 Control surface fairings

- 7.7 Radars & antenna fairings

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 OEM (original equipment manufacturers)

- 8.3 Aftermarket (MRO & replacement)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Spirit AeroSystems

- 10.1.2 GKN Aerospace

- 10.1.3 Triumph Group

- 10.1.4 FACC AG

- 10.1.5 Safran

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Kaman Corporation

- 10.2.1.2 Nordam Group

- 10.2.1.3 Meggitt

- 10.2.2 Asia Pacific

- 10.2.2.1 ShinMaywa Industries

- 10.2.2.2 AVIC

- 10.2.3 Europe

- 10.2.3.1 Leonardo S.p.A.

- 10.2.3.2 Senior plc

- 10.2.3.3 Aernnova Aerospace

- 10.2.3.4 Stelia Aerospace

- 10.2.3.5 MTorres

- 10.2.1 North America