|

시장보고서

상품코드

2038749

서큘러 폴리머 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Circular Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

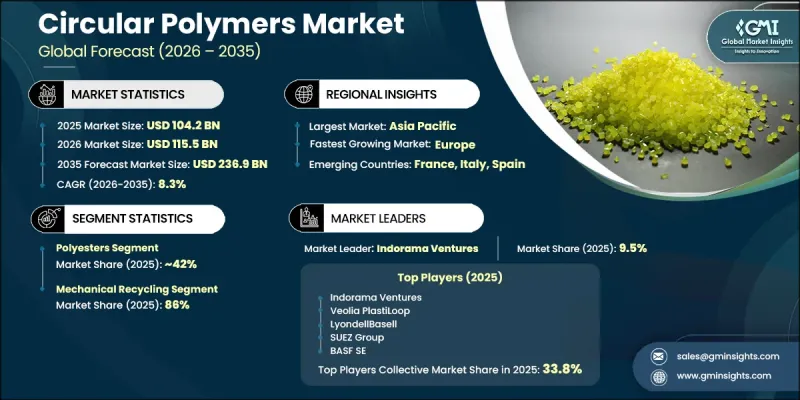

세계의 서큘러 폴리머 시장은 2025년에 1,042억 달러로 평가되었고, CAGR 8.3%로 성장할 전망이며, 2035년까지 2,369억 달러에 이를 것으로 추정되고 있습니다.

각 분야에서 지속가능성에 대한 우선순위가 높아짐에 따라 재료의 사용 형태가 재구성되고 있으며, 이 산업은 지속적으로 추진력을 얻고 있습니다. 기업들은 폐기물을 최소화하고 라이프사이클 성능을 향상시키기 위해 점점 더 많은 자원 효율적 접근방식을 채택하고 있습니다. 소비자의 환경에 대한 인식이 높아짐에 따라, 특히 포장 및 소비재 분야에서 재활용 및 재사용이 가능한 재료로의 전환이 가속화되고 있습니다. 서큘러 폴리머는 제품의 내구성을 유지하면서 플라스틱 폐기물을 줄일 수 있어 선호되는 대안으로 떠오르고 있습니다. 재활용 인프라의 발전과 더불어 선별, 세척, 재처리 기술의 혁신으로 재료의 품질과 실용성이 향상되고 있습니다. 재활용 소재의 사용을 촉진하고 환경 친화적인 생산을 장려하는 규제 프레임워크도 시장 확대를 더욱 촉진하고 있습니다. 산업계의 지속가능성 목표와 소비자의 기대치가 점점 더 일치함에 따라 제조, 자동차, 포장 산업 전반에 걸쳐 채택이 강화되고 있으며, 장기적인 성장을 위한 탄탄한 토대가 마련되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 1,042억 달러 |

| 예측 시장 규모 | 2,369억 달러 |

| CAGR | 8.3% |

기계식 재활용 부문은 비용 효율성과 잘 구축된 인프라에 힘입어 2025년 86%의 점유율을 차지했습니다. 이 방법은 화학 성분을 변경하지 않고 플라스틱 폐기물을 재사용 가능한 재료로 변환하는 물리적 처리 기술에 의존하며, 널리 사용되는 폴리머에 매우 적합합니다. 편리성, 확장성, 기존 시스템과의 호환성을 바탕으로 다양한 산업 분야에서 그 우위를 계속 강화해 나가고 있습니다.

폴리에스테르 부문은 2025년 42%의 점유율을 차지했으며, 2035년까지 연평균 7.2%의 성장률을 보일 것으로 전망됩니다. 뛰어난 재활용성, 내구성, 적응성으로 인해 다양한 분야에서 선호되는 선택이 되고 있습니다. 포장 및 섬유 생산에서 지속 가능한 소재에 대한 수요가 증가함에 따라 폴리에스테르 기반 순환형 솔루션의 채택이 계속 증가하고 있습니다.

북미의 서큘러 폴리머 시장은 2026-2035년 연평균 복합 성장률(CAGR) 7.8%를 나타낼 것으로 예측됩니다. 이 지역의 성장은 환경 규제 강화, 재활용 능력 향상, 지속가능성에 대한 소비자의 인식이 높아짐에 따라 성장세를 보이고 있습니다. 첨단 재활용 시스템과 친환경 제조 방식에 대한 투자가 지역 시장 확대에 더욱 박차를 가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 폴리머 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 재활용 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJYThe Global Circular Polymers Market was valued at USD 104.2 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 236.9 billion by 2035.

The industry continues to gain traction as sustainability priorities reshape material usage across sectors. Companies are increasingly adopting resource-efficient practices to minimize waste and improve lifecycle performance. Rising environmental awareness among consumers is accelerating the shift toward recyclable and reusable materials, particularly in packaging and consumer goods. Circular polymers are emerging as a preferred alternative due to their ability to reduce plastic waste while maintaining product durability. Advancements in recycling infrastructure, combined with innovations in sorting, cleaning, and reprocessing technologies, are improving material quality and usability. Regulatory frameworks promoting recycled content usage and incentivizing eco-friendly production further support market expansion. Growing alignment between industrial sustainability goals and consumer expectations is reinforcing adoption across manufacturing, automotive, and packaging industries, creating a strong foundation for long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $104.2 Billion |

| Forecast Value | $236.9 Billion |

| CAGR | 8.3% |

The mechanical recycling segment captured a share of 86% in 2025, supported by its cost efficiency and well-established infrastructure. This method relies on physical processing techniques to convert plastic waste into reusable material without altering its chemical composition, making it highly suitable for widely used polymers. Its simplicity, scalability, and compatibility with existing systems continue to strengthen its dominance across multiple industries.

The polyesters segment held a 42% share in 2025 and is forecast to grow at a CAGR of 7.2% through 2035. Their strong recyclability, durability, and adaptability make them a preferred choice for a wide range of applications. Increasing demand for sustainable materials in packaging and textile production continues to drive the adoption of polyester-based circular solutions.

North America Circular Polymers Market is expected to grow at a CAGR of 7.8% between 2026 and 2035. Growth in the region is driven by stricter environmental regulations, improved recycling capabilities, and heightened consumer awareness regarding sustainability. Investments in advanced recycling systems and eco-conscious manufacturing practices are further strengthening regional market expansion.

Key participants in the Global Circular Polymers Market include Amcor, Brightmark, BASF SE, Carbios, Eastman, Enka, Gr3n, Indorama Ventures, KW Plastics, Loop Industries, LyondellBasell, MBA Polymers, Plastic Energy, Plastipak, PureCycle Technologies, SUEZ Group, and Veolia PlastiLoop. Companies operating in the circular polymers market are focusing on expanding recycling capabilities, investing in advanced processing technologies, and forming strategic collaborations to strengthen their competitive position. Many players are prioritizing chemical recycling innovations to complement mechanical methods and improve material recovery rates. Partnerships across the value chain, including waste management firms and packaging companies, are helping ensure consistent raw material supply. Businesses are also emphasizing product innovation by developing high-quality recycled polymers that meet performance standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer type

- 2.2.3 Recycling technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising awareness among various industries to use recycled materials to reduce their carbon footprints

- 3.2.1.2 Increasing adoption of recyclable materials in the packaging industry is driving the market

- 3.2.1.3 Favorable initiatives to promote recycled plastics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High recycling costs hinder profitability for circular polymers

- 3.2.2.2 Limited consumer awareness reduces demand for recycled polymers

- 3.2.3 Market opportunities

- 3.2.3.1 Growing regulatory support promotes adoption of circular polymers

- 3.2.3.2 Increasing global demand for sustainable packaging solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By polymer type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyesters

- 5.2.1 PET (Polyethylene Terephthalate)

- 5.2.2 PTT (Polytrimethylene Terephthalate)

- 5.2.3 PBT (Polybutylene Terephthalate)

- 5.3 Polyolefins

- 5.3.1 Polyethylene (PE)

- 5.3.2 Polypropylene (PP)

- 5.4 Vinyl Polymers

- 5.4.1 PVC (Polyvinyl Chloride)

- 5.4.2 PVA (Polyvinyl Alcohol)

- 5.5 Styrenics

- 5.5.1 Polystyrene (PS)

- 5.5.2 ABS (Acrylonitrile Butadiene Styrene)

- 5.5.3 SAN (Styrene Acrylonitrile)

- 5.6 Engineering & Specialty Polymers

- 5.6.1 Polyamides (PA/Nylon)

- 5.6.2 Polycarbonate (PC)

- 5.6.3 Other Engineering Polymers

Chapter 6 Market Estimates and Forecast, By Recycling Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Mechanical recycling

- 6.2.1 Post-consumer recycled (PCR)

- 6.2.2 Post-industrial recycled (PIR)

- 6.3 Chemical recycling

- 6.3.1 Pyrolysis

- 6.3.2 Depolymerization

- 6.3.3 Solvent-based purification

- 6.3.4 Gasification

- 6.4 Bio-based circular polymers

- 6.4.1 Drop-in bio-based polymers

- 6.4.2 Novel bio-polymers

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.2.1 Food-grade packaging

- 7.2.2 Non-food packaging

- 7.2.3 Flexible packaging

- 7.2.4 Rigid packaging

- 7.3 Building & construction

- 7.3.1 Insulation materials

- 7.3.2 Pipes & plumbing systems

- 7.3.3 Profiles & fittings

- 7.3.4 Flooring, decking & roofing

- 7.4 Automotive

- 7.4.1 Interior components

- 7.4.2 Exterior components

- 7.4.3 Under-the-hood components

- 7.4.4 Structural & safety components

- 7.5 Electrical & electronics

- 7.5.1 Consumer electronics

- 7.5.2 Cables & wiring

- 7.5.3 Components & connectors

- 7.5.4 White goods & appliances

- 7.6 Agriculture

- 7.6.1 Films

- 7.6.2 Irrigation systems

- 7.6.3 Containers & storage

- 7.7 Textiles & apparel

- 7.7.1 Polyester fibers (rPET)

- 7.7.2 Nylon fibers (recycled pa)

- 7.7.3 Non-woven fabrics

- 7.8 Consumer goods & others

- 7.8.1 Furniture & home goods

- 7.8.2 Toys & recreational products

- 7.8.3 Other applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Amcor

- 9.2 BASF SE

- 9.3 Brightmark

- 9.4 Carbios

- 9.5 Eastman

- 9.6 Enka

- 9.7 Gr3n

- 9.8 Indorama Ventures

- 9.9 KW Plastics

- 9.10 Loop Industries

- 9.11 LyondellBasell

- 9.12 MBA Polymers

- 9.13 Plastic Energy

- 9.14 Plastipak

- 9.15 PureCycle Technologies

- 9.16 SUEZ Group

- 9.17 Veolia PlastiLoop