|

시장보고서

상품코드

2038768

임업 장비 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Forestry Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

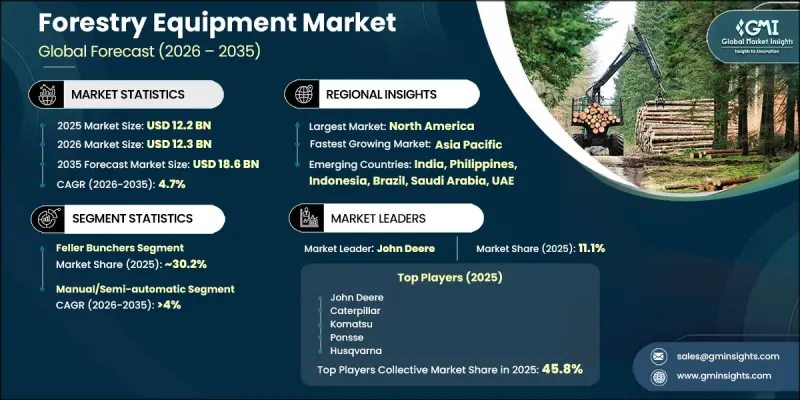

세계의 임업 장비 시장은 2025년에 122억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 전망이며, 186억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 목재, 펄프 및 바이오매스 자원에 대한 수요 증가에 힘입어 임업 및 토지 개발 활동의 확대에 의해 주도되고 있습니다. 도시화와 인프라 건설의 확대, 상업용 임업 사업의 성장에 따라 고효율 벌채 기계에 대한 수요가 크게 증가하고 있습니다. 업계는 수작업과 반 기계화 벌채 방식에서 생산성을 높이고 업무 효율성을 높이며 인력 의존도를 낮추는 고도의 기계화 시스템으로 점차 전환하고 있습니다. 또한, 현대의 임업 장비는 열악한 산림 환경에서의 안전 기준을 향상시키는 데에도 중요한 역할을 하고 있습니다. 기업들은 인력 부족을 해결하고 벌목 작업에 따른 작업장 위험을 최소화하기 위해 기계화 솔루션을 점점 더 많이 도입하고 있습니다. 이 기계들은 밀폐형 운전자 캐빈과 인체공학적 제어 시스템 등 고도의 안전 기능을 갖추고 있어 복잡한 임업 작업을 보다 안전하게 수행할 수 있도록 설계되었습니다. 비용 최적화와 업무 효율성에 대한 관심이 높아지면서 다운타임을 줄이면서 대량의 목재를 처리할 수 있는 대용량 장비의 활용이 더욱 촉진되고 있습니다. 자동화, GPS 기반 내비게이션, 유압 시스템의 발전 등 지속적인 기술 개선으로 정밀도와 생산성이 더욱 향상되어 세계 임업 장비 시장의 전반적인 확장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 122억 달러 |

| 예측 시장 규모 | 186억 달러 |

| CAGR | 4.7% |

페러밴처 부문은 2025년 30.2%의 점유율을 차지했으며, 2035년까지 연평균 4.9%의 성장률을 보일 것으로 전망됩니다. 이 기계는 수작업을 크게 줄이면서 효율적으로 나무를 벌채, 집적, 가공할 수 있기 때문에 기계화 벌채 작업에 널리 사용되고 있습니다. 다양한 나무 크기와 임업 조건에 대한 적응성으로 인해 대규모 목재 수확에 선호되는 선택이 되었습니다. 자동화 기술, 유압 시스템, GPS 지원 제어 장치의 통합이 진행됨에 따라 현대 임업 작업의 정확성, 효율성 및 생산성이 더욱 향상되고 있습니다.

수동 및 반자동 부문은 2025년에 53.4%의 점유율을 차지했으며, 2026-2035년 연평균 복합 성장률(CAGR) 4%를 나타낼 것으로 예측됩니다. 이 부문은 저렴한 가격, 운영의 유연성, 중소규모의 임업 활동에 대한 적합성으로 인해 계속해서 시장을 장악하고 있습니다. 이 부문은 기계화가 진행되지 않은 지역이나 대형 기계 도입이 어려운 세분화된 산림지역에서 널리 활용되고 있습니다. 이러한 시스템은 선택적 벌채나 가파른 경사면이나 환경적으로 민감한 지역과 같은 어려운 지형에서 작업할 때 특히 효과적이며, 대규모 토지 개조를 하지 않고도 지속적으로 목재를 채취할 수 있습니다.

2025년 미국의 임업 장비 시장은 83.58%의 점유율을 차지했으며, 30억 4,000만 달러의 매출을 기록했습니다. 이 나라의 성장은 건설, 가구, 포장 산업의 확장에 힘입어 목재, 펄프, 종이 제품에 대한 수요 증가에 의해 주도되고 있습니다. 수확기, 스키더, 포워더, 페러번처 등 기계화 임업 장비 도입 확대로 작업 효율이 향상되고 인건비가 절감되며 벌채 작업의 안전성이 향상되고 있습니다. GPS 장착 기계, 텔레매틱스 시스템, 원격 모니터링 솔루션과 같은 기술 발전은 자원 활용을 더욱 최적화하고 작업 속도를 향상시켜 전체 시장의 성장을 가속하고 있습니다.

Komatsu, John Deere, Caterpillar, Volvo, Ponsse, Tigercat, Husqvarna, Gremo, Barko Hydraulics 및 Timber Florestal 등은 임업 장비 산업을 선도하는 주요 기업입니다. 임업 장비 시장의 각 업체들은 경쟁력을 강화하기 위해 자동화와 디지털 통합에 집중하고 있습니다. 또한, 작업의 정확성과 생산성을 높이기 위해 GPS 네비게이션, 텔레매틱스, 실시간 모니터링 시스템을 탑재한 첨단 기계에 투자하고 있습니다. 또한, 각 제조업체들은 운영 비용을 절감하고 대규모 임업 작업에서 성능을 향상시키기 위해 저연비, 고용량 장비 개발에 우선순위를 두고 있습니다. 전략적 제휴와 신흥 임업 지역으로의 진출은 각 기업이 시장에서의 영향력을 확대하는 데 도움이 되고 있습니다. 또한, 안전 기능, 인체공학적 설계 및 기계 내구성에 대한 지속적인 혁신이 도입 확대를 뒷받침하고 있습니다. 또한, 각 업체들은 고객 유지율 향상과 장기적인 시장 입지를 강화하기 위해 애프터 서비스, 장비 유지보수 솔루션, 렌탈 기반 비즈니스 모델에도 주력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기기 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 전력별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

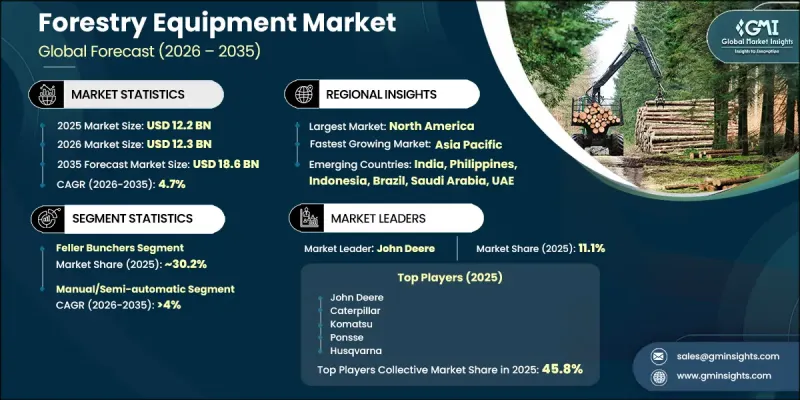

AJY 26.06.11The Global Forestry Equipment Market was valued at USD 12.2 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 18.6 billion by 2035.

Market growth is driven by rising forestry and land development activities supported by increasing demand for timber, pulpwood, and biomass resources. Expanding urbanization and infrastructure construction, along with the growth of commercial forestry operations, are significantly boosting the need for high-efficiency logging machinery. The industry is gradually shifting from manual and semi-mechanized harvesting methods toward advanced mechanized systems that improve productivity, enhance operational efficiency, and reduce dependence on manual labor. Modern forestry equipment also plays a key role in improving safety standards in challenging forest environments. Companies are increasingly adopting mechanized solutions to address labor shortages and minimize workplace risks associated with logging operations. These machines are designed with advanced safety features, including enclosed operator cabins and ergonomic control systems, enabling safer handling of complex forestry tasks. Rising focus on cost optimization and operational efficiency is further encouraging the use of high-capacity equipment capable of processing large volumes of timber with reduced downtime. Continuous technological improvements, including automation, GPS-based navigation, and hydraulic system advancements, are further enhancing precision and productivity, supporting the overall expansion of the forestry equipment market globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.2 Billion |

| Forecast Value | $18.6 Billion |

| CAGR | 4.7% |

The feller bunchers segment held a share of 30.2% in 2025 and is projected to grow at a CAGR of 4.9% through 2035. These machines are widely used in mechanized logging operations due to their ability to efficiently cut, collect, and process trees while significantly reducing manual intervention. Their adaptability to different tree sizes and forestry conditions makes them a preferred choice for large-scale timber harvesting. Increasing integration of automation technologies, hydraulic systems, and GPS-enabled controls is further improving operational accuracy, efficiency, and productivity in modern forestry operations.

The manual and semi-automatic segment accounted for 53.4% share in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. This segment continues to dominate due to its affordability, operational flexibility, and suitability for small and medium-scale forestry activities. It is widely used in regions with limited mechanization or fragmented forest areas where large equipment cannot be easily deployed. These systems are particularly effective in selective logging and operations in difficult terrains such as steep or environmentally sensitive areas, ensuring continued timber extraction without extensive land modification.

United States Forestry Equipment Market held an 83.58% share in 2025, generating revenue of USD 3.04 billion. Growth in the country is driven by rising demand for timber, pulp, and paper products supported by expansion in the construction, furniture, and packaging industries. Increasing adoption of mechanized forestry equipment such as harvesters, skidders, forwarders, and feller bunchers is improving operational efficiency, reducing labor costs, and enhancing safety in logging activities. Technological advancements including GPS-enabled machinery, telematics systems, and remote monitoring solutions, are further optimizing resource utilization and increasing operational speed, strengthening overall market growth.

Komatsu, John Deere, Caterpillar, Volvo, Ponsse, Tigercat, Husqvarna, Gremo, Barko Hydraulics, and Timber Florestal are among the leading companies operating in the forestry equipment industry. Companies in the Forestry Equipment Market are focusing on automation and digital integration to strengthen their competitive position. They are investing in advanced machinery equipped with GPS navigation, telematics, and real-time monitoring systems to enhance operational precision and productivity. Manufacturers are also prioritizing the development of fuel-efficient and high-capacity equipment to reduce operational costs and improve performance in large-scale forestry operations. Strategic partnerships and expansion into emerging forestry regions are helping companies broaden their market reach. In addition, continuous innovation in safety features, ergonomic design, and machine durability is supporting increased adoption. Firms are also focusing on after-sales services, equipment maintenance solutions, and rental-based models to improve customer retention and long-term market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Technology

- 2.2.4 Power Source

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for timber and wood products

- 3.2.1.2 Shift toward mechanized forestry operations

- 3.2.1.3 Expansion of infrastructure and land development projects

- 3.2.1.4 Advancements in machine technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 High maintenance and operating costs

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of hybrid and fuel-efficient machines

- 3.2.3.2 Growth in emerging markets

- 3.2.3.3 Integration with smart forestry systems

- 3.2.3.4 Expansion in biomass and renewable energy sector

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory guideline

- 3.5.1 North America

- 3.5.1.1 U.S.: Clean Air Act (CAA) emission standards for non-road diesel engines (Tier 4 compliance)

- 3.5.1.2 Canada: Canadian Environmental Protection Act (CEPA) emission norms for off-road engines

- 3.5.2 Europe

- 3.5.2.1 Germany: EU Stage V emission standards for non-road mobile machinery (NRMM)

- 3.5.2.2 UK: UK NRMM emission regulations (post-Brexit alignment with EU Stage V)

- 3.5.2.3 France: National Forest Code governing mechanized logging practices

- 3.5.2.4 Italy: Legislative Decree on forest management and biomass utilization

- 3.5.3 Asia Pacific

- 3.5.3.1 China: China Stage IV emission standards for non-road diesel machinery

- 3.5.3.2 India: Bharat (CEV/TREM) emission norms for construction and forestry equipment

- 3.5.3.3 Japan: Off-road vehicle emission standards under the Air Pollution Control Act

- 3.5.3.4 Australia: National Forest Policy Statement regulating forestry practices

- 3.5.4 Latin America

- 3.5.4.1 Brazil: Brazilian Forest Code governing logging and land use

- 3.5.4.2 Mexico: General Law of Sustainable Forestry Development

- 3.5.4.3 Argentina: Native Forest Protection Law regulating deforestation and equipment use

- 3.5.5 MEA

- 3.5.5.1 UAE: Federal environmental regulations on land use and conservation

- 3.5.5.2 Saudi Arabia: National Environment Strategy regulating land and vegetation use

- 3.5.5.3 South Africa: National Forests Act governing commercial forestry operations

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.9 Trade Data Analysis (Based on Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Production Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Technology and Innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.14.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Feller bunchers

- 5.2.1 Wheeled feller bunchers

- 5.2.2 Tracked feller bunchers

- 5.3 Skidders

- 5.3.1 Grapple skidders

- 5.3.2 Cable skidders

- 5.4 Loaders

- 5.4.1 Knuckleboom loaders

- 5.4.2 Heel boom loaders

- 5.5 Chippers and processors

- 5.5.1 Whole tree chippers

- 5.5.2 In-woods processors

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual/semi-automatic

- 6.3 Fully automatic

Chapter 7 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel-powered

- 7.3 Hybrid

- 7.4 Electric

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Logging

- 8.3 Land clearing

- 8.4 Construction

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Forestry companies

- 9.3 Government agencies

- 9.4 Construction companies

- 9.5 Individual

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 John Deere

- 11.1.2 Komatsu Forest

- 11.1.3 Ponsse

- 11.1.4 Tigercat Industries

- 11.1.5 Caterpillar

- 11.1.6 Rottne

- 11.1.7 HSM Hohenloher

- 11.1.8 EcoLog

- 11.1.9 Logset

- 11.1.10 Bell Equipment

- 11.2 Regional Players

- 11.2.1 Civemasa

- 11.2.2 Sthel

- 11.2.3 Timber Florestal

- 11.2.4 Juliomaq

- 11.2.5 Valmet Log

- 11.2.6 Gremo

- 11.2.7 Barko Hydraulics

- 11.2.8 Pierce Pacific

- 11.2.9 Sampo Rosenlew

- 11.2.10 Timberpro

- 11.3 Emerging Players

- 11.3.1 AFM Forest

- 11.3.2 Madill Equipment

- 11.3.3 Malwa Forest

- 11.3.4 Konrad Forsttechnik

- 11.3.5 Eschlbock