|

시장보고서

상품코드

2045724

디지털 서보 모터 및 드라이브 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Digital Servo Motors and Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

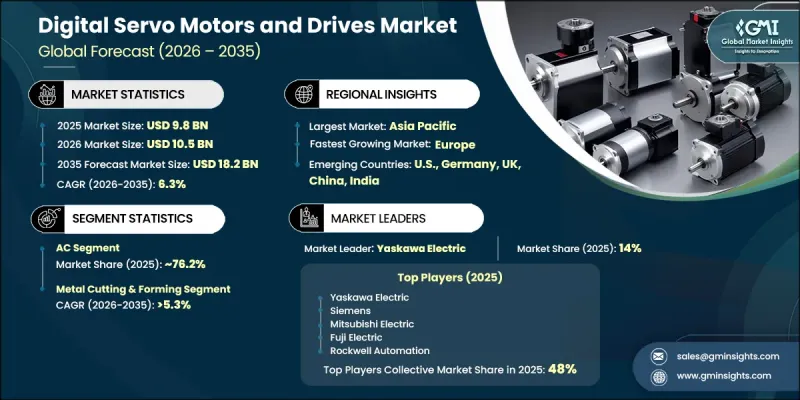

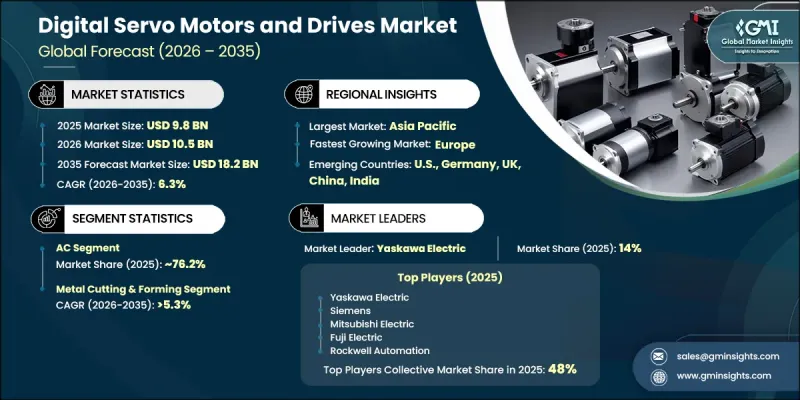

세계의 디지털 서보 모터 및 드라이브 시장은 2025년에 98억 달러로 평가되었고 CAGR 6.3%를 나타내 2035년까지 182억 달러에 이를 것으로 예측됩니다.

에너지 절약 기술 채택 확대와 더불어 산업 에너지 소비 감소에 초점을 맞춘 규제 강화는 시장 확대를 크게 촉진하고 있습니다. 산업 인프라 현대화를 위한 투자 증가와 고도화된 자동화 기술에 대한 수요 증가도 산업 성장에 힘을 실어주고 있습니다. 디지털 서보 모터 및 드라이브는 정확한 속도 제어, 운영 효율성 향상, 공정 정확도 향상, 시스템 성능 최적화를 가능하게 하여 현대 산업 활동에서 없어서는 안 될 필수 요소로 자리 잡았습니다. 로봇 공학, 스마트 제조 시스템, 산업 자동화 기술의 급속한 통합으로 인해 전 세계적으로 첨단 모터 제어 솔루션에 대한 수요가 가속화되고 있습니다. 또한, 사물인터넷(IoT) 기술과 인더스트리 4.0 이니셔티브의 도입 확대는 연결성, 생산 유연성, 운영 효율성을 향상시켜 제조 환경을 혁신적으로 변화시키고 있습니다. 제조 시설 전반의 산업 배출량 감소와 에너지 관리 개선에 대한 관심이 높아진 것도 디지털 서보 시스템 도입 확대에 기여하고 있습니다. 자동화 기술의 지속적인 발전과 지능형 제조 방법의 채택이 확대됨에 따라 향후 몇 년 동안 디지털 서보 모터 및 드라이브 산업의 전망은 더욱 강화될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 98억 달러 |

| 예측 금액 | 182억 달러 |

| CAGR | 6.3% |

AC 부문은 2025년 76.2%의 점유율을 차지했으며, 2035년까지 연평균 6.5%의 성장률을 나타낼 것으로 전망됩니다. 산업 시설의 지속적인 현대화, 개조 및 확장으로 인해 다양한 산업 분야에서 첨단 AC 서보 시스템에 대한 강력한 수요가 발생하고 있습니다. 산업 환경에서 자동화 기술과 디지털 통신 인프라의 통합이 진행되면서 제품 채택이 더욱 가속화되고 있습니다. AC 서보 모터 및 드라이브는 정하중 및 가변 부하 조건에서 효율적으로 작동하고 정밀한 모션 제어와 신뢰할 수 있는 성능을 발휘할 수 있어 널리 선호되고 있습니다. 유연성, 에너지 효율성, 첨단 산업 자동화 시스템과의 호환성을 바탕으로 세계 시장에서의 입지를 더욱 공고히 하고 있습니다.

금속 절단 및 성형 부문은 2025년 18억 달러 시장 규모를 기록했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예측됩니다. 생산 정확도 향상, 가동 속도 향상, 제조 유연성 향상에 대한 수요 증가가 이 부문의 성장에 크게 기여하고 있습니다. 정확한 위치 결정, 동기화 동작, 빠른 응답 능력을 필요로 하는 첨단 가공 기술 및 성형 공정의 채택 확대는 디지털 서보 시스템에 대한 수요를 더욱 촉진하고 있습니다. 로봇 공학, CNC 공작기계, 자동 제조 라인 및 지능형 생산 기술의 사용 확대는 전체 금속 가공 응용 분야에서 제품 도입을 촉진하고 있습니다.

미국의 디지털 서보 모터 및 드라이브 시장은 2025년 75% 점유율을 차지하며 18억 달러 시장 규모를 기록했습니다. 제조, 반도체 제조 장비, 자동차, 기타 산업 분야에서 산업 자동화 및 로봇의 도입이 활발해지면서 고정밀 서보 모터 및 드라이브에 대한 수요가 증가하고 있습니다. 스마트 제조 인프라, 첨단 생산 기술 및 산업 효율성 향상을 위한 지속적인 투자가 미국 전역 시장 성장을 더욱 촉진하고 있습니다. 미국 시장 전체에서 운영의 정확성, 생산성 향상 및 에너지 효율이 높은 산업 시스템에 대한 관심이 높아짐에 따라 제품 수요는 지속적으로 증가할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 구동 방식별(2022-2035년)

제6장 시장 규모 및 예측 : 용도별(2022-2035년)

제7장 시장 규모 및 예측 : 지역별(2022-2035년)

제8장 기업 개요

KTH 26.06.10The Global Digital Servo Motors and Drives Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 18.2 billion by 2035.

Increasing adoption of energy-efficient technologies, combined with stricter regulations focused on reducing industrial energy consumption, is significantly supporting market expansion. Growing investments in industrial infrastructure modernization and the rising demand for advanced automation technologies are further strengthening industry growth. Digital servo motors and drives enable accurate speed control, improved operational efficiency, enhanced process precision, and optimized system performance, making them essential across modern industrial operations. The rapid integration of robotics, smart manufacturing systems, and industrial automation technologies is accelerating demand for advanced motor control solutions worldwide. In addition, the increasing implementation of Internet of Things technologies and Industry 4.0 initiatives is reshaping manufacturing environments by improving connectivity, production flexibility, and operational efficiency. Rising emphasis on reducing industrial emissions and improving energy management across manufacturing facilities is also contributing to increased deployment of digitally enabled servo systems. Continuous advancements in automation technologies and the growing adoption of intelligent manufacturing practices are expected to further strengthen the outlook for the digital servo motors and drives industry over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $18.2 Billion |

| CAGR | 6.3% |

The AC segment held a 76.2% share in 2025 and is anticipated to grow at a CAGR of 6.5% through 2035. Ongoing modernization, retrofitting, and expansion of industrial facilities are creating strong demand for advanced AC servo systems across multiple industries. Increasing integration of automation technologies and digital communication infrastructure within industrial environments is further accelerating product adoption. AC servo motors and drives are widely preferred due to their capability to operate efficiently under both constant and variable load conditions while delivering precise motion control and reliable performance. Their flexibility, energy efficiency, and compatibility with advanced industrial automation systems continue to strengthen their position across the global market.

The metal cutting and forming segment generated USD 1.8 billion in 2025 and is projected to grow at a CAGR of 5.3% from 2026 to 2035. Rising demand for greater production precision, faster operational speed, and improved manufacturing flexibility is contributing significantly to segment growth. Increasing adoption of advanced machining technologies and shaping processes requiring accurate positioning, synchronized movement, and rapid response capabilities is further supporting demand for digital servo systems. The growing utilization of robotics, CNC machinery, automated manufacturing lines, and intelligent production technologies is also driving product deployment across metal processing applications.

U.S. Digital Servo Motors and Drives Market accounted for 75% share in 2025 and generated USD 1.8 billion. Strong adoption of industrial automation and robotics across manufacturing operations, semiconductor equipment production, automotive applications, and other industrial sectors is fueling demand for high-precision servo motors and drives. Continued investments in smart manufacturing infrastructure, advanced production technologies, and industrial efficiency improvements are further supporting market growth throughout the country. The increasing focus on operational accuracy, productivity enhancement, and energy-efficient industrial systems is expected to continue driving product demand across the U.S. market.

Leading companies operating in the Global Digital Servo Motors and Drives Market include ABB, Siemens, Mitsubishi Electric, Yaskawa Electric, Schneider Electric, Rockwell Automation, Bosch Rexroth, Omron, Panasonic Industry, Delta Electronics, Danfoss, Fuji Electric, Kollmorgen, Beckhoff Automation, Leadshine, Advanced Motion Controls, Allient, Applied Motion Products, Baumuller, Elmo Motion Control, Festo, Harmonic Drive, Infranor, and Nidec. Companies operating in the digital servo motors and drives market focus on multiple strategic initiatives to strengthen their competitive position and expand global market presence. Manufacturers are increasing investments in research and development to introduce highly efficient servo systems with enhanced precision, connectivity, and energy-saving capabilities. Many companies are integrating artificial intelligence, IoT technologies, and advanced analytics into servo solutions to support smart manufacturing environments and predictive maintenance applications. Strategic collaborations, mergers, and acquisitions are also helping market participants expand technological expertise and strengthen regional distribution networks. In addition, businesses are focusing on customized automation solutions tailored to industry-specific requirements across manufacturing, robotics, and industrial processing sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Drive trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of digital servo motors and drives

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

- 3.10 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.10.1 By drive (Driven by Primary Research)

- 3.10.2 By region (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-Driven production optimization (Solution Core)

- 3.11.2 Predictive maintenance & fault detection (Solution Core)

- 3.12 Capacity & production landscape (Driven by Primary Research)

- 3.12.1 Capacity by region & key producer (Driven by Primary Research)

- 3.12.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Drive, 2022 - 2035 (USD Million, '000 Units)

- 5.1 Key trends

- 5.2 AC

- 5.3 DC

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, '000 Units)

- 6.1 Key trends

- 6.2 Oil and Gas

- 6.3 Metal Cutting & Forming

- 6.4 Material Handling Equipment

- 6.5 Packaging and Labeling Machinery

- 6.6 Robotics

- 6.7 Medical Robotics

- 6.8 Rubber & Plastics Machinery

- 6.9 Warehousing

- 6.10 Automation

- 6.11 Extreme Environment Applications

- 6.12 Semiconductor Machinery

- 6.13 AGV

- 6.14 Electronics

- 6.15 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Norway

- 7.3.7 Sweden

- 7.3.8 Denmark

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Thailand

- 7.4.7 Malaysia

- 7.4.8 Philippines

- 7.4.9 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.5.5 Nigeria

- 7.5.6 Egypt

- 7.5.7 Algeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Advanced Motion Controls

- 8.3 Allient

- 8.4 Applied Motion Products

- 8.5 Baumuller

- 8.6 Beckhoff Automation

- 8.7 Bosch Rexroth

- 8.8 Danfoss

- 8.9 Delta Electronics

- 8.10 Elmo Motion Control

- 8.11 Festo

- 8.12 Fuji Electric

- 8.13 Harmonic Drive

- 8.14 Infranor

- 8.15 Kollmorgen

- 8.16 Leadshine

- 8.17 Mitsubishi Electric

- 8.18 Nidec

- 8.19 Omron

- 8.20 Panasonic Industry

- 8.21 Rockwell Automation

- 8.22 Schneider Electric

- 8.23 Siemens

- 8.24 Yaskawa Electric