|

시장보고서

상품코드

2045874

리클로저 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Recloser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

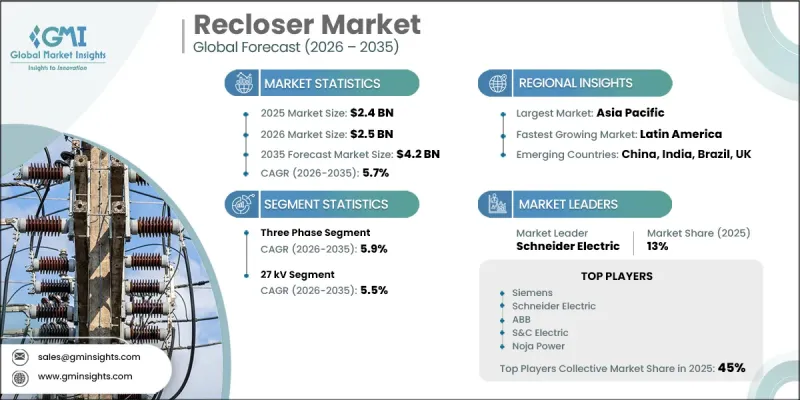

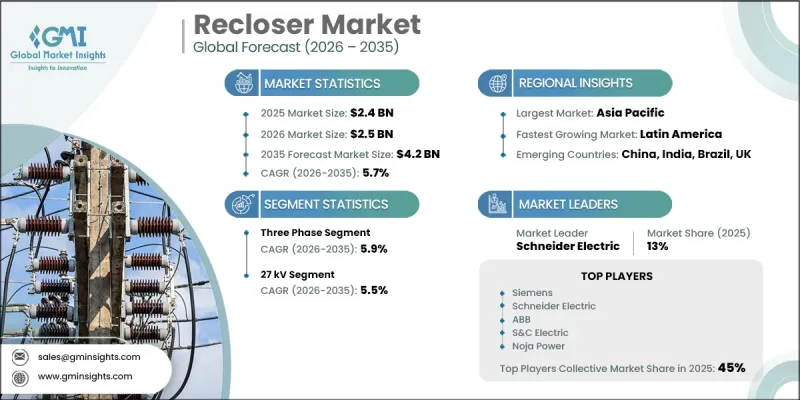

세계의 리클로저 시장은 2025년에 24억 달러로 평가되었고, CAGR 5.7%로 성장할 전망이며, 2035년까지 42억 달러에 이를 것으로 추정되고 있습니다.

선진국의 노후화된 전력 인프라 현대화를 위한 투자 증가로 인해 리클로저 산업은 꾸준히 성장하고 있습니다. 전력회사 및 송전망 운영 사업자는 시스템 신뢰성 향상, 다운타임 감소, 고장 관리 능력 향상을 위해 설비 업그레이드를 우선순위에 두고 있습니다. 급속한 도시화, 산업 확장, 인구 증가에 따른 전력 수요 증가는 배전망에 대한 부담을 더욱 가중시키고 있습니다. 리클로저는 고장을 자동으로 감지하고 격리하여 계통의 안정성을 유지하는 데 중요한 역할을 하며, 이를 통해 신속하고 효율적인 전력 복구를 가능하게 합니다. 일시적 장애와 영구적 장애를 모두 관리할 수 있는 능력은 서비스 연속성 향상에 필수적입니다. 전력회사가 자동화, 원격 모니터링, 첨단 보호 시스템에 집중하는 가운데, 스마트 그리드 기술의 도입은 수요를 더욱 가속화시키고 있습니다. 배전 설비 업그레이드에 대한 지속적인 투자와 송전망의 복원력에 대한 관심이 높아지면서 시장 성장을 견인하고 있습니다. 또한, 규제 프레임워크의 발전과 신뢰할 수 있고 효율적인 전력 공급을 위한 세계 각국의 움직임은 현대 에너지 인프라에서 첨단 리클로저 시스템의 중요성을 더욱 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 24억 달러 |

| 예측 시장 금액 | 42억 달러 |

| CAGR | 5.7% |

삼상 리클로저 시장은 2035년까지 연평균 복합 성장률(CAGR) 5.9%를 나타낼 것으로 예측됩니다. 이 부문은 전력 시스템의 모든 상들을 동시에 관리할 수 있는 능력으로 부하 밸런스를 유지하고 시스템의 불안정성을 방지할 수 있어 주목받고 있습니다. 자동 고장 감지 및 격리 기능은 운영 효율성을 향상시키고 정전 시간을 단축시킵니다. 전력망 전반에 걸친 도입 확대는 고급 그리드 용도에서 이러한 시스템의 채택을 촉진하고 있습니다.

15kV 리클로저 시장은 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 이 시장의 성장은 진화하는 전력 인프라에 적합한 컴팩트하고 효율적인 배전 장비에 대한 수요 증가에 힘입어 성장하고 있습니다. 도시 지역의 확대와 지속적인 인프라 개발이 도입 확대에 기여하고 있습니다. 또한, 친환경 제조 공정으로의 전환과 시스템 효율성 향상도 이러한 리클로저의 보급을 촉진하고 있습니다.

미국의 리클로저 시장은 안정적인 전력 분배와 그리드 성능 향상에 대한 수요 증가로 인해 2025년 2억 5,910만 달러 규모로 성장했습니다. 도시개발의 확대와 산업활동의 활성화로 인해 기존 전력시스템에 대한 부하가 증가하고 있으며, 고도의 고장관리 솔루션이 요구되고 있습니다. 전력회사들은 특히 인프라 노후화 및 이상기후로 인한 정전에 대응하기 위해 정전시간 단축, 운영 효율성 향상, 그리드 복원력 강화를 위해 리클로저 시스템에 대한 투자를 확대되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 상별(2022-2035년)

제6장 시장 규모 및 예측 : 제어 방식별(2022-2035년)

제7장 시장 규모 및 예측 : 차단별(2022-2035년)

제8장 시장 규모 및 예측 : 전압별(2022-2035년)

제9장 시장 규모 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.15The Global Recloser Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 4.2 billion by 2035.

The recloser industry is experiencing steady growth due to increasing investments in modernizing aging electrical infrastructure across developed economies. Utilities and grid operators are prioritizing upgrades to enhance system reliability, reduce downtime, and improve fault management capabilities. Rising electricity demand, driven by rapid urbanization, industrial expansion, and population growth, is further intensifying pressure on power distribution networks. Reclosers play a critical role in maintaining grid stability by automatically detecting and isolating faults, which helps restore power quickly and efficiently. Their ability to manage both temporary and permanent faults makes them essential for improving service continuity. The adoption of smart grid technologies is further accelerating demand, as utilities focus on automation, remote monitoring, and advanced protection systems. Continuous investments in power distribution upgrades and increasing emphasis on grid resilience are shaping market growth. Additionally, evolving regulatory frameworks and the global push toward reliable and efficient electricity delivery are reinforcing the importance of advanced recloser systems in modern energy infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 5.7% |

The three-phase recloser segment is projected to grow at a CAGR of 5.9% through 2035. This segment is gaining traction due to its ability to simultaneously manage all phases of electrical systems, which helps maintain load balance and prevents system instability. Its automatic fault detection and isolation capabilities improve operational efficiency and reduce outage duration. Increasing deployment across distribution networks is supporting the adoption of these systems in advanced grid applications.

The 15 kV recloser segment is expected to grow at a CAGR of 5% by 2035. Growth in this segment is driven by the rising need for compact and efficient distribution equipment suitable for evolving power infrastructure. Expanding urban areas and ongoing infrastructure development are contributing to increased deployment. The shift toward environmentally responsible manufacturing processes and improved system efficiency is also supporting broader adoption of these reclosers.

U.S. Recloser Market was valued at USD 259.1 million in 2025, driven by increasing demand for reliable electricity distribution and enhanced grid performance. Expanding urban development and rising industrial activity are placing greater pressure on existing power systems, requiring advanced fault management solutions. Utilities are increasingly investing in recloser systems to reduce outage duration, improve operational efficiency, and enhance grid resilience, particularly in response to infrastructure aging and extreme weather-related disruptions.

Key companies operating in the Global Recloser Market include ABB, Eaton, Schneider Electric, Siemens, S&C Electric, G&W Electric, Hubbell, Tavrida Electric, Arteche, Ensto, Noja Power, Hughes Power System, Wenzhou Rockwill Electric, SUN-WA TECHNOS America Inc., Entec, Rade Koncar, Rymel, and Shinsung. Companies in the recloser market are adopting several strategic approaches to strengthen their market position and expand operational reach. Organizations are heavily investing in advanced research and development to enhance product performance, automation capabilities, and fault detection accuracy. Integration of digital technologies and smart grid compatibility is becoming a key focus area to improve system efficiency and remote monitoring capabilities. Companies are also expanding manufacturing capacities and optimizing supply chains to meet rising demand from utilities and infrastructure projects. Strategic partnerships with power distribution companies are supporting long-term contracts and wider market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Phase trends

- 2.1.3 Control trends

- 2.1.4 Interruption trends

- 2.1.5 Voltage rating trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Cost structure analysis of recloser

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (Driven by Primary Research)

- 3.11.1 By phase, (USD/Unit)

- 3.12 Impact of AI & Generative AI on the market (Solution Core)

- 3.12.1 AI-driven production optimization

- 3.12.2 Predictive maintenance & fault detection

- 3.13 Trade data analysis (Driven by Primary Research)

- 3.13.1 Import/export volume & value trends

- 3.13.2 Key trade corridors & tariff impact

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 key developments

- 4.5.1 Merger & acquisition

- 4.5.2 Partnership & collaboration

- 4.5.3 New product launched

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Phase, 2022 - 2035 (Units, USD Million)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Control, 2022 - 2035 (Units, USD Million)

- 6.1 Key trends

- 6.2 Electronic

- 6.3 Hydraulic

Chapter 7 Market Size and Forecast, By Interruption, 2022 - 2035 (Units, USD Million)

- 7.1 Key trends

- 7.2 Oil

- 7.3 Vacuum

Chapter 8 Market Size and Forecast, By Voltage, 2022 - 2035 (Units, USD Million)

- 8.1 Key trends

- 8.2 15 kV

- 8.3 27 kV

- 8.4 38 kV

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (Units, USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Russia

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Chile

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Arteche

- 10.3 Eaton

- 10.4 Entec

- 10.5 Ensto

- 10.6 G&W Electric

- 10.7 Hubbell

- 10.8 Hughes Power System

- 10.9 Noja Power

- 10.10 Rade Koncar

- 10.11 Rymel

- 10.12 S&C Electric

- 10.13 Schneider Electric

- 10.14 Shinsung

- 10.15 Siemens

- 10.16 SUN-WA TECHNOS America Inc.

- 10.17 Tavrida Electric

- 10.18 Wenzhou Rockwill Electric