|

시장보고서

상품코드

2063258

리클로저 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Recloser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

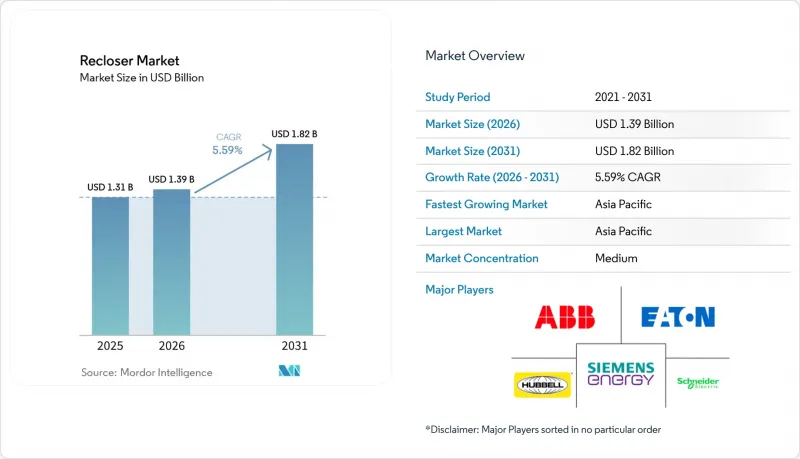

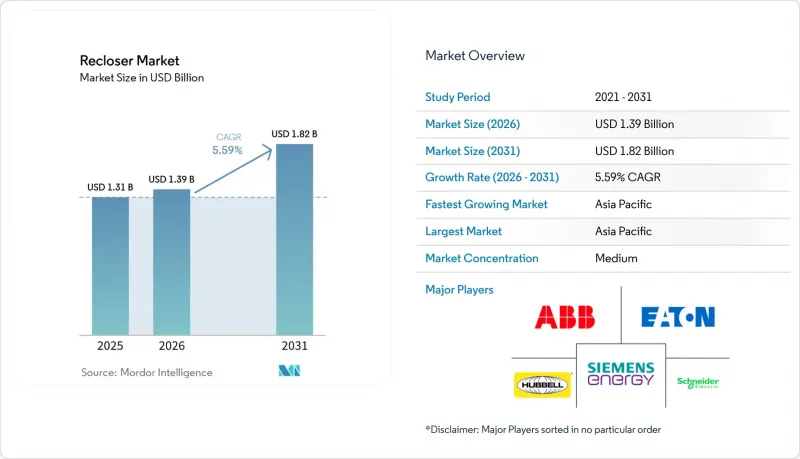

Mordor Intelligence에 의하면, 리클로저 시장 규모는 2025년 13억 1,000만 달러로 평가되었습니다. 2026년 13억 9,000만 달러에서 2031년까지 18억 2,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.59%를 나타낼 것으로 예측됩니다.

본 보고서는 차단 매체(유절연 등), 상수(단상 등), 제어 방식(유압식 등), 전압 등급(15 kV 이하 등), 설치 장소(전주 설치형 등), 최종 사용자(유틸리티, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 리클로저 시장 동향 및 인사이트

송배전망 현대화 프로그램과 송배전 자동화에 대한 지출 급증

전력 회사는 2025년에 송전망 업그레이드에 4,800억 달러를 배정했고, 2035년까지 5조 8,000억 달러를 투자할 계획이며, 그중 약 3분의 1을 고속 리클로저를 포함한 배전 자동화에 할당할 예정입니다. 에버소스사는 140만 명의 고객에게 서비스를 제공하는 뉴잉글랜드 지역 전체 전력망에 스마트 그리드 오버레이를 구축하기 위해, 2025년부터 2029년까지의 자본 계획 중 162억 달러를 배정했습니다. 중국 국가전망은 서부 각 성에 걸쳐 총 13만 7,500 회로 킬로미터에 달하는 피더에 자금을 투입하고 있으며, 정격 27kV 및 38kV 진공 차단기와 관련된 획기적인 수주를 성사시키고 있습니다. 앨버타주의 20년간 51억 달러 규모의 계획에서는 지출의 3분의 2를 재생에너지를 중심으로 한 배전선 자동화에 할당하고 있습니다. 한편, 미국의 GRIP 프로그램은 해안 홍수 위험 지역에서 지상 설치형 리클로저 사용을 규정하는 산불 대책 프로젝트에 76억 달러의 보조금을 지급했습니다.

중전압 수준에서 재생에너지의 계통 연계 가속화

2026년 초, 계통 연계 대기 목록에는 태양광, 풍력, 에너지 저장 설비가 총 2,600GW에 달했으며, 대기 기간의 중앙값은 36개월을 초과함에 따라 전력 회사는 양방향 전류를 관리할 수 있는 IEEE 1547-2018 표준을 준수하는 재폐로 장치의 도입을 서둘러야 하는 상황에 놓여 있습니다. 인도의 450GW라는 재생에너지 목표를 달성하기 위해서는 210억 달러 규모의 송전망 업그레이드가 필요하며, 그 대부분은 33kV 및 11kV 계통에서 이루어지며, 리클로저가 첫 번째 보호 계층을 형성하고 있습니다. 듀크 에너지 플로리다사는 17GW 규모의 데이터센터 부하가 대기자 명단에 올라 있다는 점을 언급하며, 이것이 현재 24kV 루프 전체에 걸쳐 지능형 리클로저의 도입을 가속화하게 된 결정적인 요인이라고 밝혔습니다. 아세안(ASEAN) 국가들은 국경을 초월한 전력 거래를 뒷받침하기 위해 2040년까지 3,000억 달러 규모의 송전망 투자를 해야 하는 상황에 직면해 있으며, 이로 인해 15-38kV급 설비에 대한 지속적인 수요가 더욱 강화되고 있습니다. 매사추세츠주의 전력 회사는 30초 이내에 전력을 우회시키는 ADMS 소프트웨어와 리클로저를 결합함으로써, 2025년까지 고장 복구 시간을 60% 단축했습니다.

자본 집약적인 구형 유압 설비의 개보수

유압식 장비는 3-5년마다 오일 교체가 필요하며, 수리 비용은 1회당 600-1,000달러가 소요되지만, 새로운 진공식 유닛은 1만 5,000-4만 달러로 가격이 비싸며, 투자 회수에는 10년이 걸립니다. 이튼의 Form 7 개조 키트는 전신주 구조를 재사용함으로써 설치 비용을 40% 절감하지만, 유럽의 프로젝트에서는 PCB 폐기 처리 비용으로 추가로 2,000-5,000달러가 소요되어 공사 기간이 길어지고 있습니다. ABB의 배터리가 필요 없는 Eagle 단상 모델은 유압 장치와의 1대1 교체를 염두에 두고 있으며, 현장 작업자를 위한 Wi-Fi를 통한 시운전 통신을 암호화하고 있습니다.

부문별 분석

진공 차단기는 연평균 성장률(CAGR) 8.0%로 성장을 주도했으나, 가스 및 SF6가 포함되지 않은 고체 차단기는 2025년 리클로저 시장에서 60.3%라는 최대 점유율을 유지했습니다. 유럽의 전력 회사들이 2026년 1월부터 금지될 SF6 장비의 교체를 시작함에 따라, 진공 기술을 활용한 리클로저 시장 규모는 급속히 확대될 전망입니다.

진공 기술로 전환한 전력 회사는 가스 보충 없이 1만 회 작동이 가능한 설계 덕분에 유지보수 비용을 절감했다고 보고하고 있습니다. ABB의 ‘SafePlus Air’와 슈나이더 일렉트릭의 ‘GM AirSeT’는 기존 설치 공간에 적합한 개조 사례를 제시함으로써 규제 당국의 승인을 쉽게 받을 수 있도록 돕고 있습니다. 유입식 유닛은 여전히 극한 추위 지역이나 지진이 빈번한 지역의 배전실에서 사용되고 있지만, -50°C까지 견딜 수 있는 새로운 밀폐형 진공 보틀이 그 틈새 시장을 축소시키고 있습니다.

2025년 리클로저 시장에서 3상형 장치는 48.9%의 점유율을 차지했으나, 2031년까지 연평균 성장률(CAGR) 6.5%를 기록하며 3상 단선형 모델이 이를 추월할 것으로 전망됩니다. 관개 시설이나 유전 부하를 처리하는 지역 회로에서는 고장 난 상만 차단함으로써 고객에게 미치는 정전 발생을 30-40% 줄일 수 있습니다.

허브벨(Hubbell)사의 ‘LineDefender’와 ABB사의 ‘Eagle’은 육안으로 확인할 수 있는 고장 표시 기능과 자가 전원 공급 방식을 갖추고 있어, 송전선 작업자가 크레인을 사용하지 않고도 설치할 수 있습니다. 마이크로프로세서의 로직이 독립된 극을 동기화하기 위해, 전력회사는 분산형 에너지 자원(DER)의 수용 능력을 최적화하기 위해 27kV 간선 지선에서도 트리플-싱글 방식의 도입이 확대될 것으로 전망하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 42.8%를 차지했으며, 중국의 5,740억 달러 규모의 배전망 확장 및 500GW의 비화석 연료 발전 목표를 세운 인도의 930억 달러 규모 변전소 계획에 힘입어, 연평균 성장률(CAGR) 6.2%를 나타낼 것으로 전망됩니다. 국가전망은 주로 35kV 신규 송전선로 13만 7,500 회로킬로미터를 부설할 계획이며, 이를 통해 지역 리클로저 시장이 직접적으로 활성화될 것입니다. 태평양 제도에서는 ‘REnew Pacific’ 계획에 따라 5MW 규모의 미니 그리드에 자금이 투입되었으며, 사이클론 발생 시에도 중단 없는 섬 내 운영을 가능하게 하는 단상 유닛의 유효성이 입증되었습니다.

북미에서는 미국의 GRIP 프로그램이 50개 주에 걸친 산불 대책 및 송전선 지하화 사업에 76억 달러를 투입하고 있습니다. 에버소스사의 162억 달러 규모의 배전 계획과 캐나다 NRCan의 보조금은 전력 사업자의 안정적인 지출을 뒷받침하고 있습니다. 버지니아주, 플로리다주, 텍사스주의 데이터센터 클러스터에서는 IEC 61850 Edition 2.1 사이버 보안 표준을 준수하는 34.5kV 패드 마운트형 리클로저가 지정되어 있으며, 공급업체에 대해 MACsec 및 역할 기반 접근 제어의 추가가 요구되고 있습니다.

유럽에서는 SF6 사용 금지로 인해 5만-7만 대의 중전압 설비에 대한 개조가 시급한 상황입니다. ABB는 기한보다 앞서 독일의 E.ON사에 SafeRing Air 개폐기를 출하했습니다. 또한 슈나이더 일렉트릭은 Ringmaster AirSeT 생산을 위해 리즈 공장에 960만 달러를 투자했습니다. Landsnet 등 북유럽의 배전 사업자(DSO)들은 광섬유를 통해 리클로저 PMU를 통합한 완전 디지털 변전소를 선도적으로 도입하고 있으며, 이러한 모델은 발트 국가들과 중부 유럽으로도 확산되고 있습니다.

남미 지역의 성장은 브라질 국가전력규제청(ANEEL)이 의무화한 손실 감축 이니셔티브와 칠레 아타카마 지역의 광업 설비 투자 증가에 힘입어 이루어지고 있습니다. 해발 4,500미터까지의 환경에 대응하도록 설계된 패드 마운트형 리클로저가 현재, 전기식 운반 트럭을 지탱하기 위해 광구 주변의 송전망에서 사용되고 있습니다.

중동 및 아프리카에서는 사우디아라비아 전력공사가 NEOM 및 홍해 재생에너지 프로젝트를 위해 5,000-7,000대의 진공 개폐기를 발주함에 따라, DEWA가 모하메드 빈 라시드 알 막툼 태양광 발전소에 자동 리클로저를 도입함에 따라 시장이 확대될 전망입니다. 남아프리카공화국의 Eskom이 안고 있는 2만 대의 노후화된 설비에 대한 미처리 물량은 재정 개혁의 결과에 따라 잠재적인 교체 수요원이 될 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the recloser market size is projected to expand from USD 1.31 billion in 2025 and USD 1.39 billion in 2026 to USD 1.82 billion by 2031, registering a CAGR of 5.59% between 2026 to 2031.

This report is Segmented by Interruption Medium (Oil-Insulated, and More), Phase (Single-Phase, and More), Control Type (Hydraulic, and More), Voltage Class (Up To 15 KV, and More), Installation Location (Pole-Mounted, and More), End-User (Utilities, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Recloser Market Trends and Insights

Grid-Modernization Programs and T&D Automation Spending Surge

Utilities allocated USD 480 billion to grid upgrades in 2025 and plan to invest USD 5.8 trillion through 2035, funneling roughly one-third toward distribution automation that includes high-speed reclosers . Eversource earmarked USD 16.2 billion of its 2025-2029 capital plan for smart-grid overlays across New England circuits serving 1.4 million customers . China State Grid is funding 137,500 circuit-kilometers of feeders in western provinces, creating landmark orders for vacuum units rated at 27 kV and 38 kV. Alberta's 20-year USD 5.1 billion blueprint dedicates two-thirds of spending to renewable-driven feeder automation, while the U.S. GRIP program has awarded USD 7.6 billion to wildfire-hardening projects that specify pad-mounted reclosers in coastal flood zones.

Accelerated Renewable Energy Interconnections at Medium-Voltage Levels

Interconnection queues held 2,600 GW of solar, wind, and storage in early 2026, stretching median wait times beyond 36 months and pushing utilities to adopt IEEE 1547-2018-compliant reclosers able to manage bidirectional flows. India's 450 GW renewables target demands USD 21 billion in transmission upgrades, much at 33 kV and 11 kV, where reclosers form the first protection layer. Duke Energy Florida cites 17 GW of queued data-center load that now dictates accelerated deployment of intelligent reclosers across 24 kV loops. ASEAN nations face USD 300 billion in grid investment by 2040 to support cross-border power trade, reinforcing sustained demand for 15-38 kV devices. Massachusetts utilities cut fault-restoration times 60% in 2025 by pairing reclosers with ADMS software that reroutes power within 30 seconds.

Capital-Intensive Retrofit of Legacy Hydraulic Fleets

Hydraulic devices need oil changes every 3-5 years and cost USD 600-1,000 per repair, yet new vacuum units range USD 15,000-40,000, stretching payback to a decade. Eaton's Form 7 retrofit kit slashes install cost 40% by re-using the pole structure, but European projects bear extra USD 2,000-5,000 PCB disposal fees that extend timelines . ABB's battery-free Eagle single-phase model targets one-to-one hydraulic swaps and encrypts Wi-Fi commissioning traffic for field crews.

Other drivers and restraints analyzed in the detailed report include:

- Reliability Mandates Under IEEE 1366 SAIDI/SAIFI Tightening (North America)

- AI-Enabled Predictive Maintenance Lowering Total Asset Lifecycle Cost

- Lengthy Utility Qualification Cycles and Type-Test Backlogs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vacuum interrupters dominated growth with an 8.0% CAGR, while gas and SF6-free solids retained the largest 60.3% 2025 recloser market share. The recloser market size for vacuum technology is set to expand rapidly as utilities in Europe replace banned SF6 equipment starting January 2026.

Utilities that migrated to vacuum report maintenance savings because the design delivers 10,000 operations without gas top-ups. ABB's SafePlus Air and Schneider's GM AirSeT illustrate retrofits that fit existing footprints, easing regulatory approval. Oil-filled units persist in arctic and seismic vaults, but new hermetic vacuum bottles rated -50 °C are narrowing that niche.

Three-phase devices held 48.9% of the 2025 recloser market share, yet triple-single models will outpace at a 6.5% CAGR through 2031. Rural circuits carrying irrigation and oil-field loads gain 30-40% fewer customer interruptions when only the faulted phase is opened.

Hubbell's LineDefender and ABB's Eagle demonstrate visible fault indication and self-powered operation that linemen can install without cranes. As micro-processor logic synchronizes independent poles, utilities foresee triple-single adoption even on 27 kV backbone laterals to optimize DER hosting capacity.

Geography Analysis

Asia-Pacific secured 42.8% of 2025 revenue and is forecast to grow at 6.2% CAGR, buoyed by China's USD 574 billion distribution expansion and India's USD 93 billion substation program targeting 500 GW of non-fossil power. State Grid aims to wire 137,500 circuit-kilometers of new lines, most at 35 kV, directly lifting the regional recloser market. Pacific Islands funded 5 MW of mini-grids under the REnew Pacific scheme, validating single-phase units that enable seamless islanding during cyclones.

In North America, the U.S. GRIP program injects USD 7.6 billion into wildfire mitigation and undergrounding across 50 states. Eversource's USD 16.2 billion distribution plan and Canada's NRCan grants underscore stable utility spending. Data-center clusters in Virginia, Florida, and Texas are specifying 34.5 kV pad-mounted reclosers with IEC 61850 Edition 2.1 cybersecurity, pushing suppliers to add MACsec and role-based access control.

In Europe, the SF6 ban forces the retrofit of 50,000-70,000 medium-voltage devices. ABB shipped SafeRing Air switchgear to E.ON Germany ahead of the deadline, and Schneider invested USD 9.6 million in its Leeds plant for Ringmaster AirSeT production. Nordic DSOs such as Landsnet pioneered fully digital substations that integrate recloser PMUs over fiber, a blueprint spreading to the Baltics and Central Europe.

Growth in South America is driven by ANEEL-mandated loss reduction initiatives in Brazil and increased mining capital expenditure in Chile's Atacama region. Pad-mounted reclosers, designed for altitudes of up to 4,500 meters, are now being utilized in pit-rim networks to support electric haul trucks.

The Middle East and Africa will grow as Saudi Electricity Company orders 5,000-7,000 vacuum units for NEOM and Red Sea renewables, and DEWA deploys automated reclosers across the Mohammed bin Rashid Al Maktoum solar park. South Africa's Eskom backlog of 20,000 aging units remains a latent replacement pool, contingent on fiscal reform.

- ABB Ltd

- Eaton Corporation plc

- Siemens Energy AG

- Schneider Electric SE

- Hubbell Power Systems

- S&C Electric Company

- NOJA Power Switchgear

- G&W Electric Company

- Tavrida Electric

- GE Grid Solutions

- Schweitzer Engineering Laboratories (SEL)

- Arteche Group

- ERMCO Inc.

- Ningbo Tianan (Group) Co.

- Zhejiang Zhegui Electric

- CG Power & Industrial Solutions

- Myers Power Products

- Brush Group

- Mitsubishi Electric Power Products

- Powell Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-modernization programs & T&D automation spending surge

- 4.2.2 Accelerated renewable energy interconnections at medium-voltage levels

- 4.2.3 Reliability mandates under IEEE 1366 SAIDI/SAIFI tightening (North America)

- 4.2.4 AI-enabled predictive maintenance lowering total asset lifecycle cost (under-the-radar)

- 4.2.5 Fast-rising micro-grid deployments in islanded & remote grids (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Capital-intensive retrofit of legacy hydraulic fleets

- 4.3.2 Lengthy utility qualification cycles & type-test backlogs

- 4.3.3 Cyber-security compliance costs for IEC 61850-based recloser controls (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Interruption Medium

- 5.1.1 Oil-insulated

- 5.1.2 Vacuum

- 5.1.3 Gas/SF6-free Solid

- 5.2 By Phase

- 5.2.1 Single-Phase

- 5.2.2 Three-Phase

- 5.2.3 Triple-Single

- 5.3 By Control Type

- 5.3.1 Hydraulic

- 5.3.2 Electric

- 5.3.3 Microprocessor/IED

- 5.4 By Voltage Class

- 5.4.1 Up to 15 kV

- 5.4.2 16 to 27 kV

- 5.4.3 28 to 38 kV

- 5.5 By Installation Location

- 5.5.1 Pole-Mounted Overhead

- 5.5.2 Pad-Mounted

- 5.5.3 Underground Vault

- 5.6 By End-User

- 5.6.1 Utilities (T&D)

- 5.6.2 Industrial (Manufacturing, Mining, Oil & Gas)

- 5.6.3 Commercial and Institutional

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Eaton Corporation plc

- 6.4.3 Siemens Energy AG

- 6.4.4 Schneider Electric SE

- 6.4.5 Hubbell Power Systems

- 6.4.6 S&C Electric Company

- 6.4.7 NOJA Power Switchgear

- 6.4.8 G&W Electric Company

- 6.4.9 Tavrida Electric

- 6.4.10 GE Grid Solutions

- 6.4.11 Schweitzer Engineering Laboratories (SEL)

- 6.4.12 Arteche Group

- 6.4.13 ERMCO Inc.

- 6.4.14 Ningbo Tianan (Group) Co.

- 6.4.15 Zhejiang Zhegui Electric

- 6.4.16 CG Power & Industrial Solutions

- 6.4.17 Myers Power Products

- 6.4.18 Brush Group

- 6.4.19 Mitsubishi Electric Power Products

- 6.4.20 Powell Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment