|

시장보고서

상품코드

2061286

상용차 플릿 정비 서비스 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Commercial Vehicle Fleet Maintenance Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

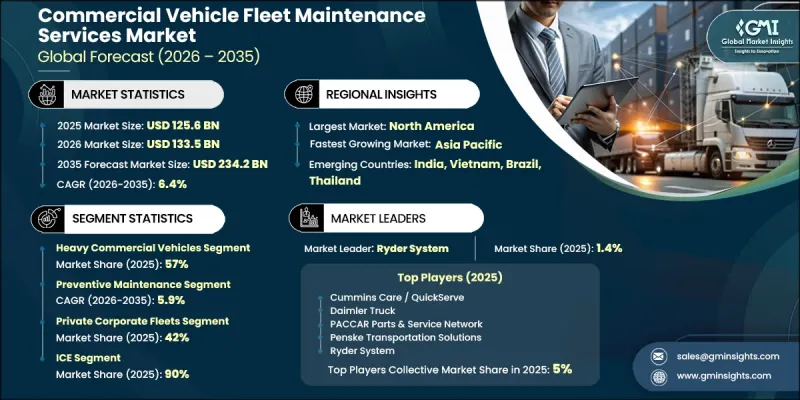

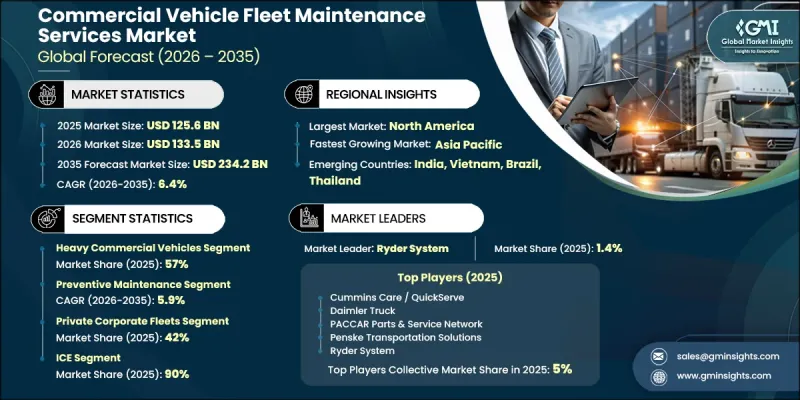

세계의 상용차 플릿 정비 서비스 시장은 2025년에 1,256억 달러로 평가되고 CAGR 6.4%로 성장하며, 2035년까지 2,342억 달러에 달할 것으로 추정되고 있습니다.

이 시장의 성장은 운송 및 물류 네트워크 전반에 걸친 상용차 도입 확대와 더불어 전 세계 화물 운송량의 증가에 힘입어 이루어지고 있습니다. E-Commerce 활동의 확대와 라스트 마일 배송 생태계의 급속한 발전이 차량 운용률을 크게 끌어올리고 있습니다. 동시에, 텔레매틱스 및 커넥티드 카 기술의 도입으로 실시간 모니터링이 강화되어, 보다 효율적인 유지보수 계획 수립과 업무 최적화가 가능해졌습니다. 함대 운영사들은 가동 중단 시간을 줄이고 서비스의 연속성을 확보하기 위해 예방적 및 예측적 유지보수 방식을 점점 더 중요하게 여기고 있습니다. 모바일 유지보수 솔루션과 현장 수리 서비스의 보급이 확대되고 있는 점도 시장 수요를 더욱 부추기고 있습니다. 또한 전기 상용차의 도입으로 인해 배터리 시스템, 전력 전자 장치, 첨단 진단과 관련된 새로운 유지보수 요건이 생겨나면서, 업계 전반의 서비스 수요가 더욱 다양해지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 1,256억 달러 |

| 예측액 | 2,342억 달러 |

| CAGR | 6.4% |

대형 상용차 부문은 2025년에 57%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 5.8%로 성장할 것으로 전망됩니다. 이러한 우위는 장거리 운송 및 중량 화물 운반 업무에서 광범위하게 활용되는 데 기인하며, 그 결과 더 가벼운 차량 등급에 비해 마모와 손상이 심하고, 더 복잡한 정비 요건이 발생합니다. 이 차량들은 운용 효율을 확보하고 성능 기준을 준수하기 위해 엔진, 브레이크 어셈블리, 변속기, 타이어, 배기가스 제어 부품 등 주요 시스템에 대한 정비를 자주 실시해야 합니다. 대형 운송 자산에 대한 의존도가 높아짐에 따라 전 세계 시장에서 일관된 정비 수요가 계속해서 증가하고 있습니다.

2025년에는 민간 기업이 보유한 차량 부문이 42%의 점유율을 차지했습니다. 이는 물류, 소매 유통, 산업 활동, 건설 활동 및 E-Commerce 공급망 전반에 걸친 광범위한 차량 도입에 힘입은 결과입니다. 이러한 차량들은 업무 차질을 최소화하고 차량의 신뢰성을 높이기 위해 체계적인 정비 프로그램에 크게 의존하고 있습니다. 전 세계 도로 화물 운송의 높은 이용률은, 특히 배송 효율과 비용 최적화에 주력하는 민간 기업이 운영하는 상용 밴, 트럭 및 다목적 차량 분야에서 유지보수 서비스에 대한 지속적인 수요를 창출하고 있습니다.

2025년, 미국의 상용차 차량 관리 서비스 시장은 392억 달러의 시장 규모를 기록하며 85%의 점유율을 차지했습니다. 해당 국가의 시장 확대는 화물 운송 활동의 증가, E-Commerce에 따른 출하량 확대, 그리고 물류·유통 네트워크의 지속적인 확장에 힘입어 이루어지고 있습니다. 전미의 차량 운영 사업자들은 가동 중단 시간을 줄이고 생산성을 높이기 위해 예방 정비 체계를 점점 더 많이 도입하고 있습니다. 텔레매틱스 시스템과 예측 유지보수의 통합을 통해, 차량 함대 운영 전반에 걸친 정비 정확도와 운영 관리가 한층 더 향상되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차량별, 2022-2035년

제6장 시장 추산·예측 : 서비스별, 2022-2035년

제7장 시장 추산·예측 : 플릿 소유 형태별, 2022-2035년

제8장 시장 추산·예측 : 추진력별, 2022-2035년

제9장 시장 추산·예측 : 서비스 제공별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.25The Global Commercial Vehicle Fleet Maintenance Services Market was valued at USD 125.6 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 234.2 billion by 2035.

The market growth is supported by the rising deployment of commercial vehicles across transportation and logistics networks, along with increasing freight movement volumes worldwide. Expanding e-commerce activities and the rapid development of last-mile delivery ecosystems are significantly boosting fleet utilization rates. At the same time, the adoption of telematics and connected vehicle technologies is enhancing real-time monitoring, enabling more efficient maintenance scheduling and operational optimization. Fleet operators are increasingly prioritizing preventive and predictive maintenance approaches to reduce downtime and ensure uninterrupted service continuity. The rising penetration of mobile maintenance solutions and on-site repair services is further strengthening market demand. Additionally, the integration of electric commercial vehicles is introducing new maintenance requirements related to battery systems, power electronics, and advanced diagnostics, further diversifying service needs across the sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $125.6 Billion |

| Forecast Value | $234.2 Billion |

| CAGR | 6.4% |

The heavy commercial vehicles segment held a 57% share in 2025 and is forecast to grow at a CAGR of 5.8% between 2026 and 2035. This dominance is attributed to their extensive usage in long-distance transportation and freight-heavy operations, which results in higher wear and tear and more complex servicing requirements compared to lighter vehicle categories. These vehicles require frequent upkeep of critical systems including engines, braking assemblies, transmissions, tires, and emission control components to ensure operational efficiency and compliance with performance standards. The growing dependency on heavy-duty transportation assets continues to reinforce consistent maintenance demand across global markets.

The private corporate fleets segment accounted for 42% share in 2025, driven by widespread fleet deployment across logistics, retail distribution, industrial operations, construction activities, and e-commerce supply chains. These fleets depend heavily on structured maintenance programs to minimize operational disruptions and enhance vehicle reliability. The high utilization of road-based freight transport globally continues to generate sustained demand for maintenance services, particularly for commercial vans, trucks, and utility vehicles operated by private enterprises focused on delivery efficiency and cost optimization.

United States Commercial Vehicle Fleet Maintenance Services Market held a share 85% of generating USD 39.2 billion in 2025. Market expansion in the country is supported by rising freight transportation activity, growing e-commerce shipments, and the continuous scaling of logistics and distribution networks. Fleet operators across the country are increasingly adopting preventive maintenance frameworks to reduce downtime and improve productivity. The integration of telematics systems and predictive diagnostics is further enhancing maintenance precision and operational control across fleet operations.

Major participants in the Global Commercial Vehicle Fleet Maintenance Services Market include Cummins, Daimler Truck, Element Fleet Management, Holman, MAN Truck & Bus, PACCAR, Penske Transportation Solutions, Ryder System, Scania, and Volvo. Companies operating in the commercial vehicle fleet maintenance services market are actively strengthening their market position through multiple strategic initiatives. A key approach includes expanding digital fleet management capabilities supported by telematics, IoT-based monitoring systems, and predictive analytics tools that enable real-time diagnostics and proactive maintenance scheduling. Market players are also focusing on building integrated service networks by expanding mobile repair units, authorized service centers, and on-site maintenance solutions to improve service accessibility and reduce vehicle downtime. Strategic partnerships with logistics providers, fleet operators, and technology firms are further helping companies enhance service efficiency and broaden customer reach. In addition, organizations are investing in workforce training programs to address the growing complexity of modern vehicle systems, especially electric and connected fleets.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Service

- 2.2.4 Fleet Ownership

- 2.2.5 Propulsion

- 2.2.6 Service Delivery

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of freight transportation and logistics networks

- 3.2.1.2 Growing adoption of telematics and predictive diagnostics

- 3.2.1.3 Increasing outsourcing of fleet maintenance operations

- 3.2.1.4 Rising ecommerce and last mile delivery activity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High labor and technician shortage

- 3.2.2.2 Rising costs of spare parts and advanced diagnostics equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in electric commercial vehicle maintenance services

- 3.2.3.2 Expansion of mobile fleet maintenance solutions

- 3.2.3.3 Integration of artificial intelligence and predictive analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 FMCSA Part 396 interstate repair and maintenance mandates

- 3.6.1.2 U.S. DOT periodic commercial vehicle inspection standards

- 3.6.1.3 OSHA 29 CFR 1910 service shop safety and compliance

- 3.6.1.4 EPA Section 609 motor vehicle air conditioning certifications

- 3.6.1.5 Transport Canada National Safety Code (NSC) Standard 11

- 3.6.2 Europe

- 3.6.2.1 EU Roadworthiness Directive 2014/45/EU for technical inspections

- 3.6.2.2 EU Regulation 2018/858 on vehicle and part market surveillance

- 3.6.2.3 Euro 6 and Euro 7 emission system maintenance requirements

- 3.6.2.4 Waste Framework Directive for hazardous fluid and battery disposal

- 3.6.2.5 EU Mobility Package II digital maintenance and tachograph rules

- 3.6.3 Asia Pacific

- 3.6.3.1 China GB 18565 technical safety and maintenance standards

- 3.6.3.2 China Administration of Automobile Maintenance and Repair Industry regulations

- 3.6.3.3 India CMVR and BS-VI exhaust/engine compliance standards

- 3.6.3.4 Japan "Shaken" mandatory periodic vehicle inspections

- 3.6.3.5 Australia National Heavy Vehicle Inspection Manual (NHVIM)

- 3.6.4 Latin America

- 3.6.4.1 Brazil CONTRAN mandatory periodic technical inspections (ITV)

- 3.6.4.2 Mexico NOM-068-SCT physical-mechanical safety standards

- 3.6.4.3 Argentina RTO mandatory technical review for freight transport

- 3.6.4.4 Chile Decree 156 preventive maintenance and inspection protocols

- 3.6.4.5 Mercosur technical roadworthiness for cross-border transport

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi SASO workshop certifications and spare part requirements

- 3.6.5.2 UAE ESMA technical regulations for commercial vehicle safety

- 3.6.5.3 South Africa Road Transport Management System (RTMS) standards

- 3.6.5.4 Qatar GSO 42/2015 motor vehicle periodic inspection rules

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Light Commercial Vehicles (LCV)

- 5.2.1 Pickup Trucks

- 5.2.2 Cargo Vans

- 5.2.3 Panel Vans

- 5.2.4 Others

- 5.3 Medium Commercial Vehicles (MCV)

- 5.3.1 Medium-Duty Trucks

- 5.3.2 Box Trucks

- 5.3.3 Flatbed Trucks

- 5.3.4 Others

- 5.4 Heavy Commercial Vehicles (HCV)

- 5.4.1 Heavy-Duty Trucks

- 5.4.2 Tractor-Trailers / Semi-Trucks

- 5.4.3 Buses & Public Transport

- 5.4.4 Others

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Preventive Maintenance

- 6.3 Predictive Maintenance

- 6.4 Body-shop Collision Repairs

- 6.5 Emergency/Corrective Repairs

- 6.6 Tires, Brakes, Batteries & Lubricants

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Fleet Ownership, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Private Corporate Fleets

- 7.3 Government Fleets

- 7.4 Rental and Leasing Companies

- 7.5 Mobility Service Providers

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Service Delivery, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 In-House/Captive Workshops

- 9.3 Outsourced Service Providers

- 9.4 Mobile/On-Site Services

- 9.5 Hybrid Models

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Cummins

- 11.1.2 Daimler Truck

- 11.1.3 Isuzu Motors

- 11.1.4 IVECO

- 11.1.5 MAN Truck & Bus

- 11.1.6 PACCAR

- 11.1.7 Penske Transportation Solutions

- 11.2 Regional Players

- 11.2.1 Ryder System

- 11.2.2 Scania

- 11.2.3 Volvo

- 11.2.4 Holman (ARI Fleet Services)

- 11.2.5 Element Fleet Management

- 11.2.6 Enterprise Fleet Management

- 11.2.7 Ashok Leyland

- 11.2.8 Al-Futtaim Motors Fleet Services

- 11.2.9 Grupo Comfortrans

- 11.3 Emerging Players

- 11.3.1 Fleetio

- 11.3.2 Ridecell

- 11.3.3 OTONOMO

- 11.3.4 Mahindra Last Mile Mobility (MLLM)