|

시장보고서

상품코드

2061325

육상 C4ISR 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Land-Based C4ISR Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

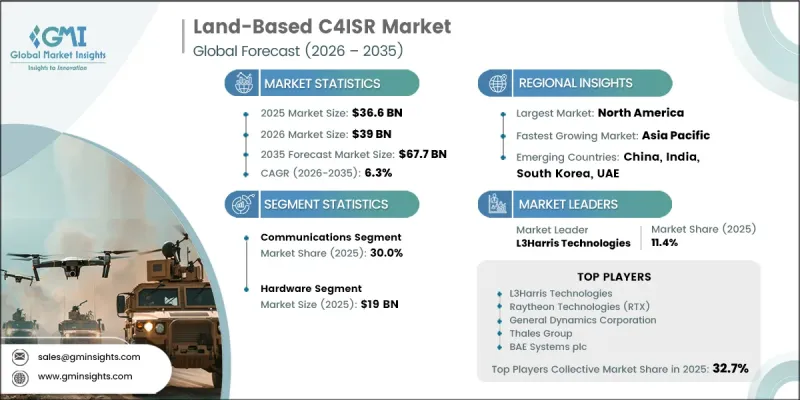

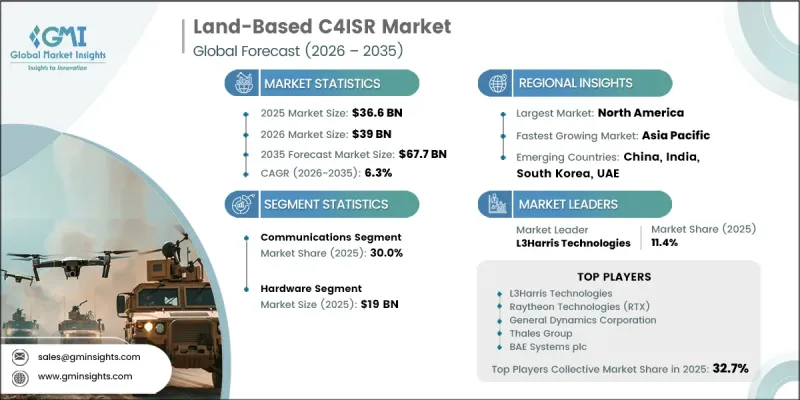

세계의 육상 C4ISR 시장은 2025년에 366억 달러로 평가되었으며, CAGR 6.3%로 성장하여 2035년까지 677억 달러에 달할 것으로 추정됩니다.

이 시장의 성장은 다중 도메인 전장 상황 인지에 대한 수요 증가와, 현대 방위 작전 전반에 걸쳐 실시간 협력을 가능하게 하는 네트워크 중심 전쟁 프레임워크의 채택 확대에 힘입어 이루어지고 있습니다. 국경 경비 요건의 강화, 대테러 작전, 그리고 지상 부대의 통신 시스템에 대한 지속적인 현대화 역시 이러한 도입을 더욱 뒷받침하고 있습니다. 자율형 플랫폼과 첨단 감지 기술의 통합 또한 육상 방위 환경 전반에 걸쳐 작전 효과를 높이고 있습니다. 육·공·사이버·우주 등 각 분야에 걸친 통합적인 상황 인지에 대한 중요성이 커짐에 따라, 대규모 데이터 스트림을 실용적인 지휘 판단으로 통합할 수 있는 통합 정보 시스템에 대한 수요가 급증하고 있습니다. 고도로 연결된 전장 생태계로의 전환은 지휘 센터와 최전방 부대 간의 지속적이고 안전한 통신 연결의 필요성을 더욱 강조하고 있습니다. 클라우드 컴퓨팅, 엣지 처리, AI 기반 분석 및 모듈식 시스템 아키텍처의 발전은 지상군의 정보 역량을 한층 더 혁신하고 있으며, 세계 시장에서의 조달 주기 단축과 장기적인 국방 현대화 프로그램을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 366억 달러 |

| 시장 규모 예측 | 677억 달러 |

| CAGR | 6.3% |

통신 부문은 지휘·통제·정보·감시 작전 수행 시 안전하고 대용량의 데이터 교환을 가능하게 하는 데 중요한 역할을 하고 있어, 2025년에는 30%의 점유율을 차지했습니다. 첨단 통신 인프라에 대한 강력한 수요는 상비군에서의 대규모 도입과, 점점 더 복잡해지고 경쟁이 치열해지는 전자기 환경에서 운용하기 위해 필요한 지속적인 업그레이드에 의해 주도되고 있습니다. 군에서 실시간 전장 조정을 위해 내결함성과 상호운용성을 갖춘 통신 네트워크를 우선시함에 따라, 이 부문의 중요성은 계속해서 높아지고 있습니다.

하드웨어 부문은 모든 C4ISR 기능이 물리적 시스템 및 인프라에 필수적으로 의존하고 있기 때문에 2025년에는 190억 달러를 차지했습니다. 여기에는 차량 및 야전 부대에 배치되는 견고한 컴퓨팅 장치, 레이더 및 탐지 시스템, 안테나 기술, 무선 주파수(RF) 부품, 전기광학 및 적외선 시스템, 통합 처리 장치 등이 포함됩니다. 하드웨어에 대한 지속적인 투자는 진행 중인 현대화 프로그램, 플랫폼 업데이트, 그리고 지상 방어 시스템에 첨단 센서 페이로드를 지속적으로 통합하는 데 힘입어 이루어지고 있습니다.

북미의 지상 C4ISR 시장은 광범위하고 지속적인 자금 지원을 받고 있는 국방 현대화 이니셔티브에 힘입어 2025년에는 39.3%의 시장 점유율을 기록했습니다. 이 지역의 성장은 전술 네트워크 업그레이드, 전자전 능력 강화, 자율형 감지 시스템 통합, 그리고 현대적인 다영역 작전 전략에 부합하는 데이터 중심의 지휘통제 아키텍처로의 전환에 중점을 둔 체계적인 장기 조달 프로그램에 힘입어 추진되고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 시스템 종류별(2022-2035년)

제6장 시장 추정 및 예측 : 플랫폼별(2022-2035년)

제7장 시장 추정 및 예측 : 구성요소별(2022-2035년)

제8장 시장 추정 및 예측 : 최종사용자별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KSM 26.06.22The Global Land-Based C4ISR Market was valued at USD 36.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 67.7 billion by 2035.

The market growth is driven by rising demand for multi-domain battlefield awareness and increasing adoption of network-centric warfare frameworks that enable real-time coordination across modern defense operations. Growing border security requirements, counter-terrorism missions, and ongoing modernization of ground force communication systems are further strengthening adoption. Integration of autonomous platforms and advanced sensing technologies is also enhancing operational effectiveness across land-based defense environments. Increasing emphasis on unified situational awareness across land, air, cyber, and space domains is accelerating demand for integrated intelligence systems capable of merging large-scale data streams into actionable command insights. The shift toward highly connected battlefield ecosystems is reinforcing the need for persistent, secure communication links between command centers and frontline units. Advancements in cloud computing, edge processing, AI-enabled analytics, and modular system architectures are further transforming land force intelligence capabilities, supporting faster procurement cycles and long-term defense modernization programs across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.6 Billion |

| Forecast Value | $67.7 Billion |

| CAGR | 6.3% |

The communications segment held a 30% share in 2025, supported by its critical role in enabling secure, high-capacity data exchange across command, control, intelligence, and surveillance operations. Strong demand for advanced communication infrastructure is driven by large-scale deployment across standing land forces and continuous upgrades required to operate in increasingly complex and contested electromagnetic environments. The segment's importance continues to grow as militaries prioritize resilient and interoperable communication networks for real-time battlefield coordination.

The hardware segment accounted for USD 19 billion in 2025 owing to the essential reliance of all C4ISR functions on physical systems and infrastructure. This includes rugged computing units, radar and sensing systems, antenna technologies, radio frequency components, electro-optical and infrared systems, and integrated processing units deployed across vehicles and field units. Sustained investment in hardware is driven by ongoing modernization programs, platform upgrades, and the continuous integration of advanced sensor payloads into land-based defense systems.

North America Land-Based C4ISR Market held 39.3% share in 2025, supported by extensive and consistently funded defense modernization initiatives. The region's growth is reinforced by structured long-term procurement programs focused on upgrading tactical networks, enhancing electronic warfare capabilities, integrating autonomous sensing systems, and transitioning toward data-centric command architectures aligned with modern multi-domain operational strategies.

Key players operating in the Global Land-based C4ISR Market include Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc, RTX Corporation, Thales Group, L3Harris Technologies, General Dynamics Corporation, Elbit Systems Ltd., Saab AB, Rheinmetall AG, Leonardo S.p.A., Bharat Electronics Limited (BEL), Israel Aerospace Industries (IAI), HENSOLDT AG, CACI International Inc., Kratos Defense & Security Solutions, Inc., Leidos Holdings, Inc., and Aselsan A.S. Companies in the land-based C4ISR market are focusing on advanced capability development and strategic defense partnerships to strengthen their competitive position. A major emphasis is placed on integrating AI-driven analytics, edge computing, and secure cloud-enabled architectures to enhance real-time battlefield intelligence. Firms are investing heavily in modular and open-system designs to ensure interoperability across diverse defense platforms and simplify upgrades. Collaboration with defense agencies is enabling tailored solution development aligned with evolving mission requirements. Companies are also expanding their presence through long-term government contracts and lifecycle support services to ensure sustained revenue streams. In addition, continuous investment in sensor fusion, cybersecurity enhancements, and next-generation communication technologies is improving system resilience and operational efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Platform trends

- 2.2.3 Component trends

- 2.2.4 End-User trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for multi-domain battlefield awareness

- 3.2.1.2 Growing adoption of network-centric warfare architectures

- 3.2.1.3 Increasing border security and counter-terrorism operations

- 3.2.1.4 Modernization of ground force communication infrastructure

- 3.2.1.5 Integration of autonomous systems and advanced sensor technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration complexity across multi-domain platforms

- 3.2.2.2 Cybersecurity vulnerabilities in network-centric defense systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of secure tactical communication networks in emerging defense regions

- 3.2.3.2 Increasing investments in simulation and training systems integrated with C4ISR platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Command & control (C2)

- 5.3 Communications

- 5.4 Intelligence, surveillance & reconnaissance (ISR)

- 5.5 Electronic warfare (EW)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Dismounted soldier systems

- 6.3 Vehicle-mounted platforms

- 6.4 Fixed/stationary infrastructure

- 6.5 Unmanned ground vehicles (UGVs)

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense forces (military)

- 8.3 Homeland security & border guard

- 8.4 Civil defense & emergency response

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Infineon Technologies AG

- 10.1.2 L3Harris Technologies

- 10.1.3 Raytheon Technologies (RTX)

- 10.1.4 General Dynamics Corporation

- 10.1.5 Thales Group

- 10.1.6 BAE Systems plc

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Lockheed Martin Corporation

- 10.2.1.2 Northrop Grumman Corporation

- 10.2.1.3 CACI International Inc.

- 10.2.1.4 Kratos Defense & Security Solutions, Inc.

- 10.2.1.5 Leidos Holdings, Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Bharat Electronics Limited (BEL)

- 10.2.3 Europe

- 10.2.3.1 Saab AB

- 10.2.3.2 Rheinmetall AG

- 10.2.3.3 Leonardo S.p.A.

- 10.2.3.4 HENSOLDT AG

- 10.2.4 Middle East & Africa

- 10.2.4.1 Aselsan A.S.

- 10.2.4.2 Elbit Systems Ltd.

- 10.2.4.3 Israel Aerospace Industries (IAI)

- 10.2.1 North America