|

시장보고서

상품코드

2061326

지향성 에너지 C-UAS(대무인항공시스템) 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Directed Energy Counter-UAS Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

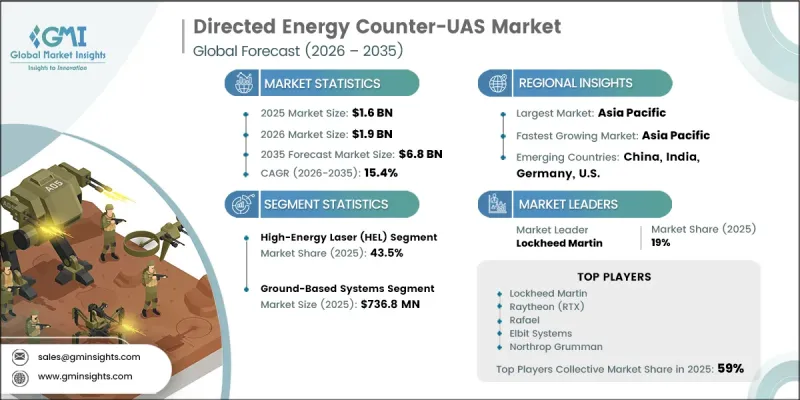

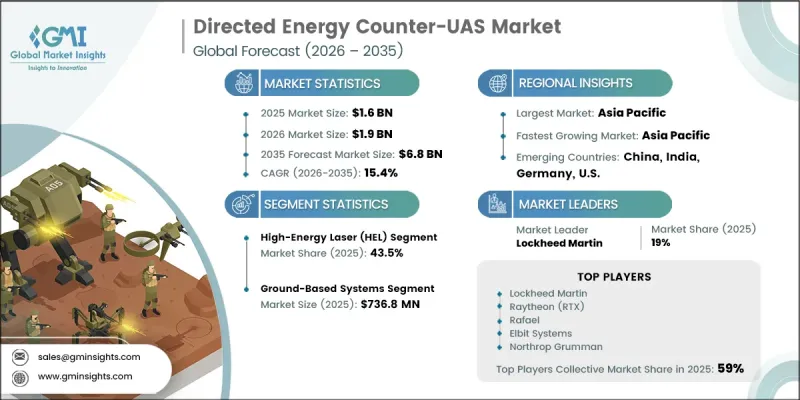

세계의 지향성 에너지 C-UAS(대무인항공시스템) 시장은 2025년에 16억 달러로 평가되었으며, 2035년까지 CAGR 15.4%로 성장하여 68억 달러에 달할 것으로 추정됩니다.

이 시장의 성장은 드론과 군집 비행체에 의한 위협이 심화되고 빈번해짐에 따라 주도되고 있으며, 이러한 위협은 기존 방공 시스템에 막대한 부담을 주고 있습니다. 비용 효율이 높고 확장성이 뛰어나며 지속가능한 요격 기술에 대한 수요가 증가함에 따라, 방위 및 보안 분야에서 지향성 에너지 솔루션의 도입이 가속화되고 있습니다. 방위 현대화 노력의 확대에 더해, 중요 인프라 보호에 대한 수요가 증가함에 따라 시장 확대가 더욱 가속화되고 있습니다. 레이저 시스템, 전력 전자공학 및 에너지 관리 기술의 지속적인 발전으로 인해 시스템의 성능, 신뢰성 및 구축 유연성이 향상되고 있습니다. 군과 치안 부대가 더 신속하고, 더 정확하며, 비용 효율적인 요격 수단을 모색하는 가운데, 비살상형 방어 능력에 대한 관심이 높아지고 있는 점도 이러한 수단의 광범위한 도입에 기여하고 있습니다. 자율형 드론의 능력과 전자적 내성을 갖춘 플랫폼의 진화는 전 세계 국방 환경에서 첨단 지향성 에너지 대응책의 필요성을 더욱 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 16억 달러 |

| 시장 규모 예측 | 68억 달러 |

| CAGR | 15.4% |

고출력 마이크로파(HPM) 부문은 2026년부터 2035년까지 연평균 성장률(CAGR) 17.2%를 기록하며 성장할 것으로 전망됩니다. 이 부문의 성장은 여러 대의 무인항공기가 일으키는 위협을 동시에 무력화할 수 있는 능력에 힘입은 것으로, 무리 지어 공격해 오는 적에 대해 매우 높은 효과를 발휘합니다. HPM 시스템은 광범위한 비살상형 교란 능력을 제공하며, 현대의 위협 환경에서 그 중요성이 점점 더 커지고 있습니다. 연구개발 투자 증가에 더해, 이동형 및 단거리형 드론 대응 시스템에 대한 수요가 높아지면서 방위 및 보안 분야에서의 도입이 더욱 가속화되고 있습니다.

지상형 시스템 부문은 2025년에 7억 3,680만 달러에 달했습니다. 이러한 압도적인 시장 점유율은 군사 시설, 국경 경비 구역, 중요 인프라 시설, 도시 방어 구역 등에 광범위하게 배치된 데 기인합니다. 지상형 지향성 에너지 시스템은 높은 출력 용량, 기존 레이더 및 지휘통제 네트워크와의 원활한 통합, 이동식 플랫폼에 비해 낮은 운용 위험 등 강력한 운용상의 이점을 제공합니다. 이러한 비용 효율성, 확장성, 그리고 입증된 운영 신뢰성 덕분에 대규모의 영구적인 대UAS 장비 배치에 있어 가장 선호되는 솔루션으로 자리매김하고 있습니다.

북미의 지향성 에너지 방식 대 UAS 장비 시장은 2025년에 31.4%의 점유율을 기록했습니다. 이 지역의 성장은 국내 치안에 대한 우려가 커지고, 주요 시설 인근에서 무허가 드론 활동이 증가하며, 공역 보호에 대한 관심이 높아짐에 따라 주도되고 있습니다. 군사 기지, 국경 지역 및 고가치 인프라 자산이 밀집해 있다는 점이 해당 지역 전체에 걸쳐 첨단 비살상형 요격 시스템에 대한 수요를 더욱 부추기고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술 종류별(2022-2035년)

제6장 시장 추정 및 예측 : 플랫폼 종류별(2022-2035년)

제7장 시장 추정 및 예측 : 출력별(2022-2035년)

제8장 시장 추정 및 예측 : 용도별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KSM 26.06.22The Global Directed Energy Counter-UAS Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 15.4% to reach USD 6.8 billion by 2035.

The market growth is driven by the increasing intensity and frequency of drone-based and swarm-enabled aerial threats, which are placing significant pressure on conventional air defense systems. Rising demand for cost-efficient, scalable, and sustainable interception technologies is accelerating the adoption of directed energy solutions across defense and security applications. Expanding defense modernization initiatives, along with the growing need to secure critical infrastructure, are further supporting market expansion. Continuous advancements in laser systems, power electronics, and energy management technologies are enhancing system performance, reliability, and deployment flexibility. Increasing focus on non-kinetic defense capabilities is also contributing to broader adoption, as military and security forces seek faster, more precise, and lower-cost interception methods. The evolution of autonomous drone capabilities and electronically resilient platforms is further reinforcing the need for advanced directed energy countermeasures across global defense environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 15.4% |

The high-power microwave (HPM) segment is projected to grow at a CAGR of 17.2% during 2026-2035. Growth in this segment is driven by its ability to neutralize multiple unmanned aerial threats simultaneously, making it highly effective against swarm-based attacks. HPM systems provide wide-area, non-kinetic disruption capabilities that are increasingly relevant in modern threat environments. Rising investment in research and development, along with growing demand for mobile and short-range counter-drone systems, is further accelerating adoption across defense and security applications.

The ground-based systems segment reached USD 736.8 million in 2025. This dominance is attributed to its widespread deployment across military installations, border security zones, critical infrastructure sites, and urban defense areas. Ground-based directed energy systems offer strong operational advantages, including higher power capacity, seamless integration with existing radar and command-and-control networks, and reduced operational risk compared to mobile platforms. Their cost efficiency, scalability, and proven operational reliability make them the preferred solution for large-scale and permanent counter-UAS deployments.

North America Directed Energy Counter-UAS Market accounted for 31.4% share in 2025. The region's growth is driven by rising homeland security concerns, increasing incidents of unauthorized drone activity near sensitive installations, and heightened emphasis on airspace protection. A dense network of military bases, border regions, and high-value infrastructure assets is further supporting demand for advanced non-kinetic interception systems across the region.

Key companies operating in the Global Directed Energy Counter-UAS Market include Lockheed Martin, Raytheon (RTX), Northrop Grumman, Boeing, L3Harris, BAE Systems, Leonardo, Thales, Rheinmetall, General Atomics, Kratos, Rafael, Elbit Systems, Epirus, and QinetiQ. Companies in the directed energy counter-UAS market are focusing on advancing high-energy weapon technologies and strengthening system integration capabilities to expand their market presence. A key strategy involves heavy investment in laser systems, microwave technologies, and power optimization solutions to improve interception accuracy and operational range. Firms are prioritizing the development of modular and scalable platforms that can be deployed across fixed and mobile defense environments. Strategic partnerships with defense agencies are enabling faster testing, validation, and deployment of next-generation systems. Companies are also enhancing R&D efforts in thermal management, energy efficiency, and beam control technologies to improve reliability under operational stress. Expansion into multi-domain defense applications and integration with existing command-and-control systems is further strengthening adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Platform type trends

- 2.2.3 Power output trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption increasing IGBT and SiC demand

- 3.2.1.2 Industrial automation growth raising demand for power modules

- 3.2.1.3 Energy efficiency regulations mandating advanced power electronics

- 3.2.1.4 Data center power optimization increasing MOSFET consumption

- 3.2.1.5 Fast-charging infrastructure expansion boosting wide-bandgap semiconductors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost of SiC and GaN devices

- 3.2.2.2 Supply chain dependence on limited wafer suppliers

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of SiC in 800V electric vehicle platforms

- 3.2.3.2 Smart grid upgrades increasing demand for high-power discrete devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 High-energy laser (HEL)

- 5.2.1 Solid-state lasers

- 5.2.2 Fiber Lasers

- 5.3 High-power microwave (HPM)

- 5.3.1 Narrow-band HPM

- 5.3.2 Wide-band HPM

- 5.4 Emerging technologies

Chapter 6 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Ground-based systems

- 6.2.1 Mobile/transportable systems

- 6.2.2 Fixed installations

- 6.3 Naval/maritime systems

- 6.3.1 Ship-mounted systems

- 6.3.2 Coastal/port defense systems

- 6.4 Airborne systems

- 6.4.1 UAV-mounted systems

- 6.4.2 Aircraft-integrated system

Chapter 7 Market Estimates and Forecast, By Power Output, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low power (<10 kW)

- 7.3 Medium power (10-50 kW)

- 7.4 High power (>50 kW)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Military & Defense Operations

- 8.2.1 Base Defense

- 8.2.2 Battlefield Use

- 8.2.3 Strategic Asset Protection

- 8.3 Border & Perimeter Security

- 8.4 Critical Infrastructure Protection

- 8.4.1 Airports

- 8.4.2 Ports & Maritime

- 8.4.3 Energy & Utilities

- 8.4.4 Government Facilities

- 8.5 Civil & Commercial Security

- 8.5.1 Public Events & Stadiums

- 8.5.2 Corporate & Industrial Sites

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Lockheed Martin

- 10.1.2 Raytheon (RTX)

- 10.1.3 Rafael

- 10.1.4 Elbit Systems

- 10.1.5 Northrop Grumman

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Boeing

- 10.2.1.2 L3Harris

- 10.2.1.3 General Atomics

- 10.2.1.4 Kratos

- 10.2.2 Europe

- 10.2.2.1 BAE Systems

- 10.2.2.2 Leonardo

- 10.2.2.3 Thales

- 10.2.2.4 Rheinmetall

- 10.2.2.5 QinetiQ

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Epirus